Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.99 Billion |

| Market Size (2026) | USD 4.14 Billion |

| Market Size (2031) | USD 5.27 Billion |

| Growth Rate (2026 - 2031) | 4.98% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Washing Machine Market Analysis by Mordor Intelligence

The India Washing Machine Market size is projected to expand from USD 3.99 billion in 2025 and USD 4.14 billion in 2026 to USD 5.27 billion by 2031, registering a CAGR of 4.98% between 2026 to 2031.

Near-term growth continues to be shaped by India’s Production Linked Incentive framework, which committed USD 729.4 million (INR 6,238 crore) to approved participants and is steering domestic value addition toward a 75-80% target by FY 2028-29.[1]Source: Press Information Bureau, “PLI Scheme: Powering India’s Industrial Renaissance,” Government of India, pib.gov.in Regional dynamics remain uneven within the India washing machine market, with North India at 34.98% share in 2025 and South India leading growth at a 9.78% CAGR through 2031. Connectivity and automation are shifting product mix, as conventional units held 88.46% share in 2025, while smart-connected models posted the fastest trajectory at 15.49% CAGR. Brand evidence points to the same pivot, with AI-enabled ranges now central to launch pipelines and to sales contribution in India’s premium and mainstream segments.

Key Report Takeaways

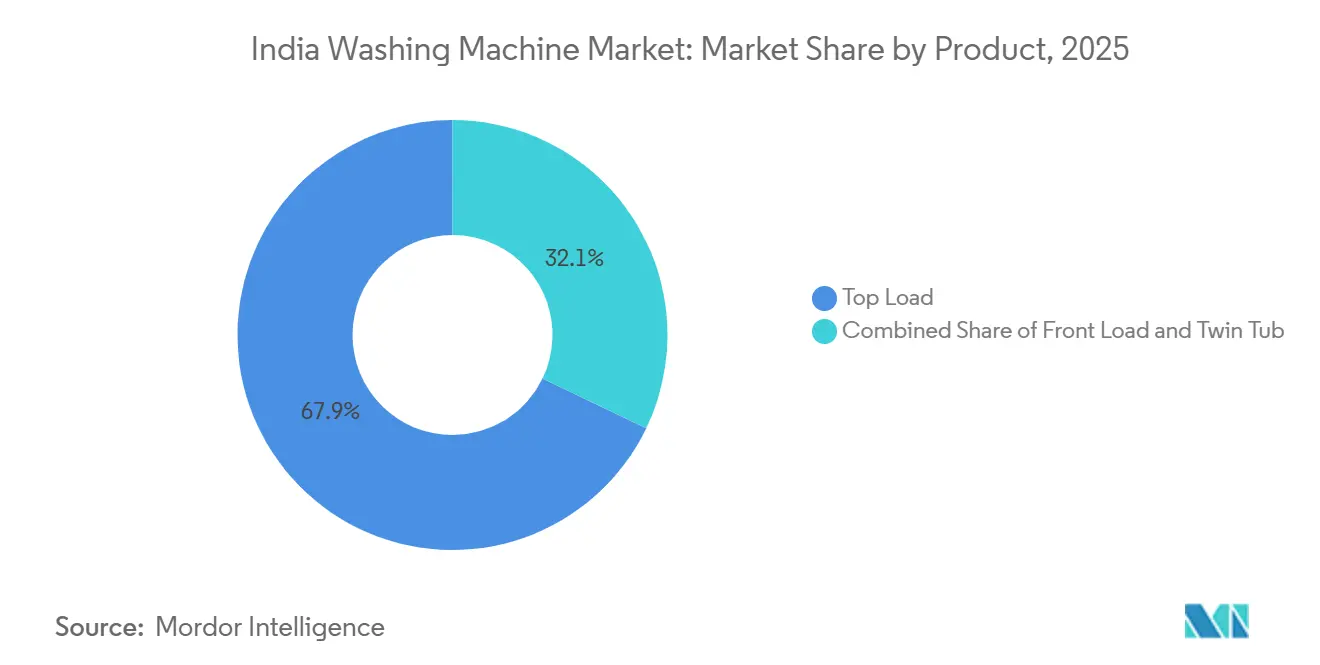

- By product, top-load machines led with 67.85% of the India washing machine market share in 2025, while front-load models are projected to expand at an 8.44% CAGR through 2031.

- By technology, fully automatic systems accounted for 54.65% of the India washing machine market size in 2025 and are advancing at a 9.33% CAGR through 2031.

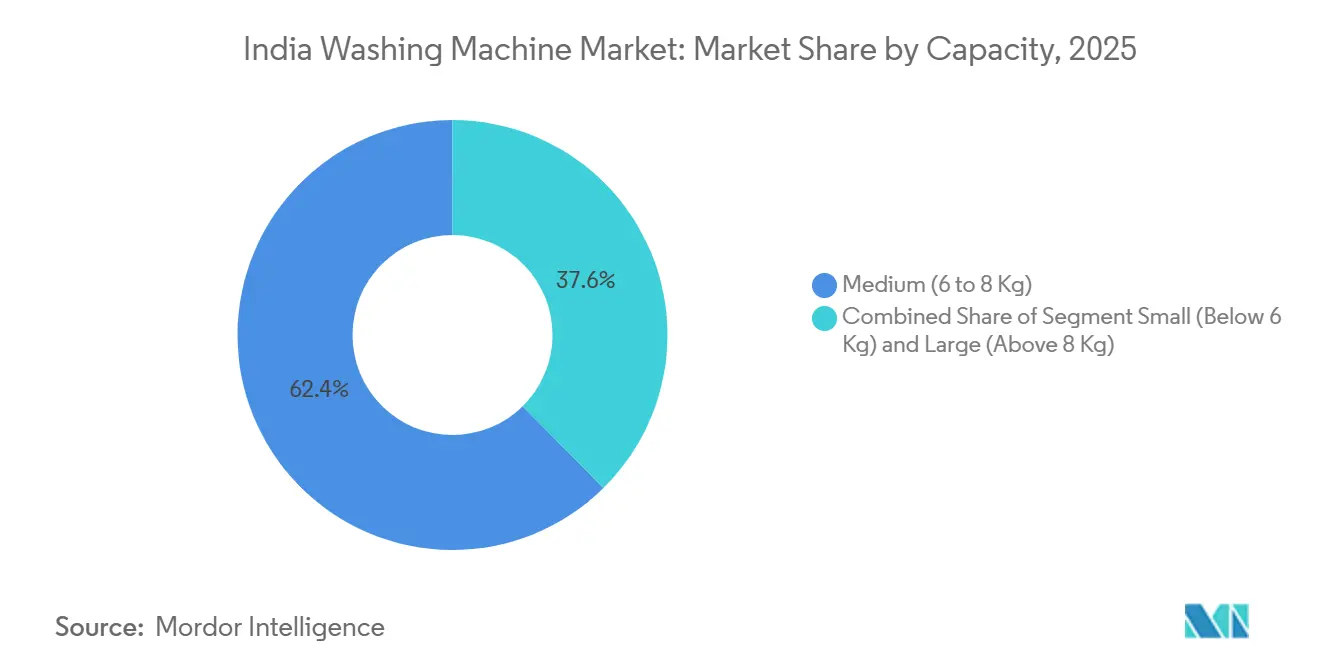

- By capacity, the 6-8 kg bracket held 62.39% of the India washing machine market share in 2025, while above-8 kg units are set to grow at a 9.98% CAGR to 2031.

- By connectivity, conventional models captured 88.46% of the India washing machine market share in 2025, and smart-connected models are forecast to grow at a 15.49% CAGR through 2031.

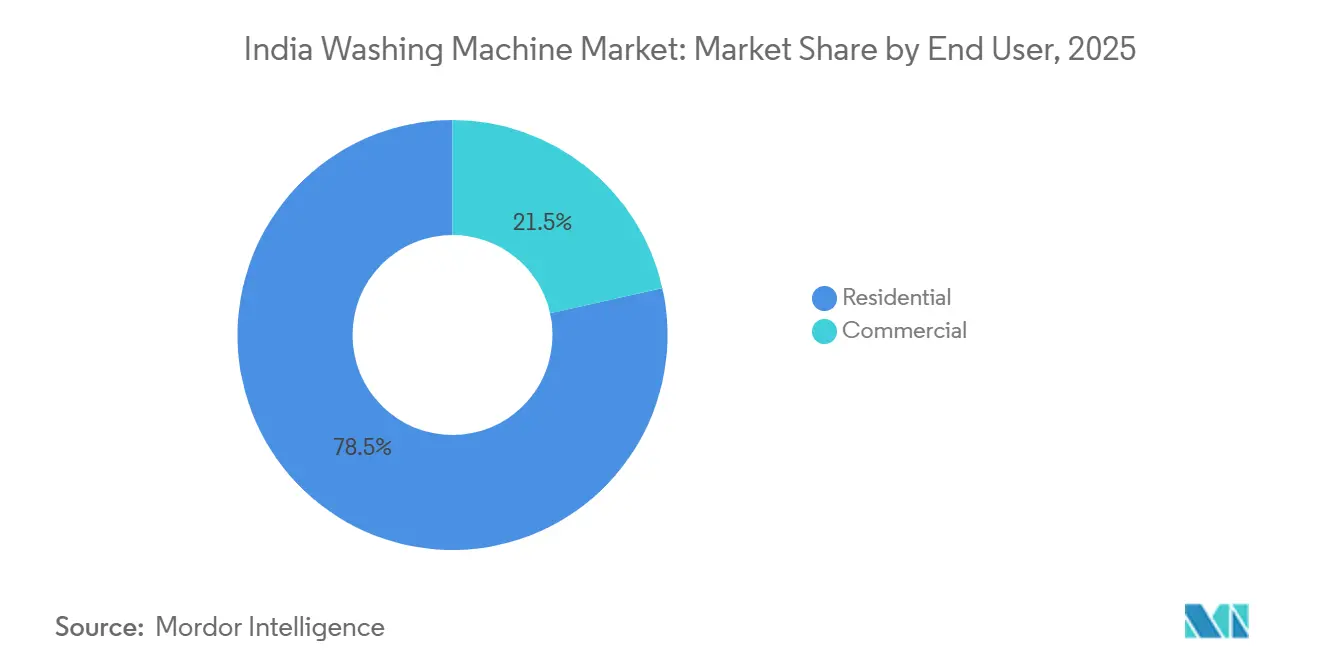

- By end user, residential installations commanded 78.49% of the India washing machine market share in 2025, and commercial adoption is projected to post a 9.37% CAGR to 2031.

- By distribution channel, B2C/Retail accounted for 81.39% of the India washing machine market share in 2025, while the online sub-channel within B2C is expected to register the fastest CAGR at 10.84% through 2031.

- By geography, North India held 34.98% of the India washing machine market share in 2025, and South India is set to be the fastest-growing region at a 9.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Washing Machine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tier-II and Tier-III Cities Witness A Surge In Disposable Income | +1.2% | National, concentrated in tier-2/3 urban clusters | Medium term (2-4 years) |

| Urbanization Accelerates, and Nuclear Households become the Norm | +0.9% | National, spill-over from metros to tier-2 | Long term (≥ 4 years) |

| E-Commerce And Omni-Channel Retail Continue to Expand | +0.8% | Pan-India, 70% tier-2/3 contribution | Short term (≤ 2 years) |

| Technological Shift Towards Fully-Automatic and Inverter Motors | +1.4% | Urban core, early tier-2 adopters | Medium term (2-4 years) |

| Production-Linked Incentive (PLI) Scheme is Bolstering Local Output | +0.6% | Manufacturing hubs: Chennai, Pune, Greater Noida, Goa | Long term (≥ 4 years) |

| Smart-Home And IoT Features Are Paving the Way for Subscription Add-ons | +0.5% | Metro and tier-1, nascent tier-2 penetration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Technological Shift Towards Fully-Automatic and Inverter Motors

Fully automatic machines held 54.65% market share in 2025 and are advancing at a 9.33% CAGR through 2031, which signals a rapid pivot toward higher-efficiency platforms within the India washing machine market. Inverter architectures are central to that shift and are highlighted by brand-launched platforms in India that deliver sizable energy savings and intelligent cycle control. IFB localized high-efficiency drive components and moved commercial BLDC motor production into steady state by FY 2024-25, which reduces import reliance and supports sustained cost control. Premium platforms with AI-enabled fabric care, load sensing, and remote diagnostics have deepened differentiation versus semi-automatic designs, which is improving perceived durability and total cost of ownership in the India washing machine market. Regulatory emphasis on higher energy performance is reinforcing the engineering cycle around motors and controllers and guiding product portfolios toward inverter-led roadmaps that satisfy long-term efficiency thresholds. Together, these technology and policy vectors are accelerating the upgrade path from semi-automatic to fully automatic configurations across urban and early tier-2 demand pools in the India washing machine market.

Production-Linked Incentive (PLI) Scheme is Bolstering Local Output

The white-goods PLI program announced a multi-year outlay of USD 729.4 million (INR 6,238 crore) and is engineered to raise domestic value addition toward 75-80% by FY 2028-29, which is catalyzing a new supplier base for motors, controllers, and other shared components used in washers. The incentive design links payouts to incremental sales and progressively higher local-content thresholds, encouraging phased tooling, localization, and process upgrades across India washing machine market participants and adjacent suppliers. IFB documented PLI and M-SIPS-linked receipts that underwrote capacity and controller localization, aligning its washing machine operations with policy-led supply security and cost-down objectives. BSH expanded assembly capacity in Chennai and launched new India-made front-load ranges, supporting a deeper local bill of materials and shorter inbound cycles.[2]Source: Bosch Siemens Home, “BSH opens immersive Bosch and Siemens Brand Store in Kolkata,” BSH Home Appliances, bosch-home.in Over time, the policy push should compress lead times and reduce import duty exposure in the India washing machine market while raising the industry’s quality baseline through mandated certification and testing regimes. The cumulative effect is a gradual margin reset, with localization gains offsetting short-term cost friction as supply chains reconfigure under the PLI glide path.

Smart-Home And Iot Features Are Paving the Way for Subscription Add-ons

Smart-connected machines represented a minority of installed units in 2025, yet they recorded the fastest expansion rate at a 15.49% CAGR through 2031, marking a clear digital step-up within the India washing machine market. Samsung’s AI portfolio has become a material contributor to washer sales in India and integrates energy monitoring, remote control, and downloadable cycles that shift the product from a one-time purchase to an ongoing service platform. LG ThinQ enables customized programs and predictive maintenance notifications that deepen user engagement and lengthen brand stickiness during the replacement cycle. Haier’s Hai Smart App around its new front-load range illustrates how companion software unlocks features such as Smart Refresh and remote management to extend garment life and reduce wash frequency.[3]Source: Haier India, “Smart Home Devices to Kickstart Your 2025 New Year,” Haier India, shop.haierindia.com IFB has started to monetize post-purchase essentials through direct-to-consumer channels, pairing consumables with connected guidance to broaden lifetime revenue. As energy management features like AI Energy Mode become mainstream, the value proposition of connected machines strengthens for households attentive to electricity costs in the India washing machine market.

Urbanization Accelerates, and Nuclear Households become the Norm

India’s urban population ratio continued to rise through 2026, tightening living spaces and reinforcing demand for compact, high-efficiency front-loaders and fully automatic top-loaders within the India washing machine market. Household migration patterns and the shift toward smaller family units increase the appeal of 6-8 kg machines that balance space with throughput for weekly laundry loads. Product engineering in India has responded with features that handle low water pressure conditions common in high-rises and peri-urban areas, improving cycle reliability and consumer satisfaction. As urban incomes stabilize, premium features such as steam hygiene, anti-allergen cycles, and high spin speeds are becoming decisive, which supports faster adoption of front-load models in emerging city clusters. The same shift is visible in the forecast, where front-load platforms are set to grow at an 8.44% CAGR to 2031 off a smaller base, reshaping the mid-to-premium end of the India washing machine market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumers Grapple with High Upfront Costs Versus Their Discretionary Income | -0.7% | Rural India, lower-income urban pockets | Short term (≤ 2 years) |

| Price-Sensitive Rural Consumers Lean Towards Semi-Automatic Models | -0.4% | Rural belts, Uttar Pradesh, Bihar, Madhya Pradesh | Medium term (2-4 years) |

| Volatility in the Supply Chain And Commodity Prices Poses Challenges | -0.5% | National, manufacturer cost pass-through | Short term (≤ 2 years) |

| Drought-Prone States Face Regulations due to Water Scarcity | -0.3% | Rajasthan, Haryana, Punjab, Maharashtra (Marathwada) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Consumers Grapple with High Upfront Costs Versus their Discretionary Income

Upfront pricing remains a barrier for many households, which sustains interest in lower-cost semi-automatic models and slows upgrade cycles in value-driven cohorts within the India washing machine market. Financing programs and promotional constructs continue to ease adoption, but price sensitivity has translated into cautious demand for premium variants when macro uncertainty is elevated. Mixed product momentum has also shown up in company disclosures, where selective categories experienced flat sales and margin pressure despite the availability of higher-efficiency platforms and richer feature sets. Retail distribution is responding with more no-cost EMI options, faster installation, and regional targeting to broaden reach in price-sensitive areas. Over the medium term, localization of motors and controllers and more efficient logistics should help narrow price gaps between entry and mid-tier options in the India washing machine market.

Volatility in the Supply Chain And Commodity Prices Poses Challenges

Manufacturing energy use, material costs, and logistics variability have kept pressure on operating margins for appliance producers, which elevates the importance of local sourcing and energy-efficient operations in the India washing machine market. Several brands initiated structured cost-down programs focused on weight optimization, electronics sourcing, and deeper localization of critical modules to offset external volatility. Capacity additions and localized production of premium front-load ranges also reduce exposure to imported content and delays while aligning with PLI and certification requirements. Together, these measures aim to stabilize supply and improve cost absorption, strengthening the runway for premiumization in the India washing machine market. Over time, higher energy efficiency in factories and greater use of renewable power can further mitigate operating-cost swings in the production base serving India.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Front-Load Gains as Premiumization Accelerates

Top-load models captured the largest market share at 67.85% in 2025, reflecting price-led preferences, while front-load models are projected to expand at an 8.44% CAGR through 2031 within the India washing machine market. New front-load launches emphasize high spin speeds, fabric-care cycles, and rapid programs that compress cycle time without eroding wash quality. Urban households are showing growing willingness to trade up to drum-based platforms to gain energy savings and features such as steam hygiene. This feature stack is also widening differentiation versus semi-automatic designs and reducing perceived maintenance risk in the India washing machine market. Over the forecast horizon, front-load penetration remains the key mix driver, with brands aligning merchandising and capacity planning to sustain interest from tier-1 and emerging tier-2 clusters.

Front-load positioning focuses on long-term cost of ownership, gentle fabric care, and digital control, which resonate with dual-income urban buyers. Top-load machines continue to draw value-focused consumers who want familiar ergonomics, perceived water control, and lower entry pricing in the India washing machine market. At the premium end, integrated washer-dryer propositions target space-constrained apartments and highlight time savings and one-touch care. Product life-cycle communications are also shifting toward energy ratings, AI cycle selection, and fabric protection guarantees to reinforce upgrade intent. These elements collectively underpin the expected share gains for front-load formats within the India washing machine market.

By Technology: Fully Automatic Dominance Underpinned by Rural Electrification

Fully automatic systems accounted for 54.65% market share in 2025 and are set to grow at a 9.33% CAGR through 2031, outpacing semi-automatic platforms in the India washing machine market size trajectory for technology segments. Inverter motors and intelligent dosing are becoming table stakes, which raises the bar for energy performance and noise reduction. Localized production of BLDC motors, controllers, and other critical nodes is improving cost structures and reducing exposure to currency and freight volatility. Semi-automatic machines continue to serve water-scarce environments and price-sensitive users, but are structurally disadvantaged in cycle automation and energy efficiency in the India washing machine market. The widening feature gap and policy incentives for higher-efficiency appliances are expected to sustain the momentum of fully automatic adoption.

The technology roadmap is also becoming more software-centric, with AI control and downloadable programs optimizing wash performance across fabrics. Manufacturers are backing platforms with longer warranties, which signals confidence in component reliability and supports total cost of ownership arguments in the India washing machine market. As localized content rises, mid-tier fully automatic machines can absorb richer feature sets without pricing out mainstream users. The interplay of better energy labels, in-home service networks, and financing options further strengthens the use case for fully automatic formats in the India washing machine industry. As a result, the India washing machine market is expected to tilt steadily toward automated, connected platforms across the forecast window.

By Capacity: Large Loads Surge as Household Incomes Rise

The 6-8 kg middle-capacity band held 62.39% of the market size in 2025, reflecting the most common household size and budget range within the India washing machine market. Above-8 kg machines are projected to grow at a 9.98% CAGR through 2031, which points to rising preference for fewer, larger loads and improved time management. Product development has moved to bolster drum design, balance systems, and high-spin performance suitable for bulky items like linens and winter wear. The energy penalty from larger capacities is being mitigated by inverter control and adaptive load sensing, a trend seen across recent premium launches in India. These shifts indicate that capacity upgrades are likely to remain a central lever of premiumization in the India washing machine industry.

Smaller formats under 6 kg continue to serve single-occupant households and hostels but face growth limits as nuclear families in urban settings choose 6-8 kg or larger. In larger homes, 10-12 kg front-loaders help consolidate laundry into fewer cycles and align with high-efficiency programs that protect fabrics and cut energy use. Unit economics benefit from localized sourcing of motors and control electronics, which reduces cost pressure as brands scale larger formats in the India washing machine market. Retailers have responded with broadened assortments and rapid delivery and installation that support purchase confidence for heavier units. The net effect is a gradual upshift in preferred load sizes across urban and peri-urban buyer groups in the India washing machine market.

By Connectivity: IoT Penetration Accelerates from Low Base

Conventional models still dominate with 88.46% market share in 2025, but smart-connected machines are forecast to grow the fastest at a 15.49% CAGR through 2031 in the India washing machine market. Brand ecosystems now bundle energy monitoring, predictive maintenance, and cloud-linked cycle libraries to extend product utility beyond the initial sale. LG ThinQ and comparable platforms enable cycle downloads, device diagnostics, and notification layers that reduce friction in day-to-day use. Haier has emphasized remote management and refresh functions that decrease wash frequency, tying connectivity to garment care and time savings. These capabilities position connected models as credible upgrades in the India washing machine market as household Wi-Fi access rises.

Price gaps versus non-connected models have narrowed at mid-tier price points, aided by localized electronics and scale economics. Energy-saving modes that optimize temperature and motion profiles are helping justify connectivity premiums for cost-conscious users. Over-the-air improvements and app-based guidance also lengthen functional life and increase customer engagement during the replacement cycle in the India washing machine market. On the retail side, standardized information via QR and digital product pages is reinforcing users’ comfort with app interfaces even before purchase. Together, these trends underline the sustained advantage for smart-connected washers in the India washing machine industry.

By End User: Commercial Segment Climbs as Industrial Laundry Expands

Residential applications accounted for 78.49% market share in 2025, while commercial deployments are projected to grow at a 9.37% CAGR through 2031 in the India washing machine market. Commercial buyers prioritize throughput, total cost of ownership, and service coverage, which is driving demand for ruggedized washer-extractors and dryers. Industrial partnerships with institutions and hospitality align capacity planning with predictable demand and structured maintenance programs. Residential buyers, by contrast, balance price with energy ratings, cycle convenience, and fabric care performance when upgrading. These diverging priorities shape product portfolios and merchandising in the India washing machine market.

Commercial engineering has progressed toward IE3 and IE4 motor efficiency, material-light platforms, and water-saving cycles to reduce utility costs. Residential replacement cycles are shortening as inverter-led products and connected features render older machines less compelling on running costs and convenience. Brand service networks and direct-to-consumer channels are important levers for both segments, enabling faster installation and higher attach rates for accessories and consumables. As commercial contracts scale, the segment can sustain double-digit tender pipelines and export-led opportunities for Indian-made systems. This shift supports a broader base for growth in the India washing machine market beyond residential upgrades alone.

By Distribution Channel: Online Retail Erodes Brick-and-Mortar Share

B2C/Retail accounted for an 81.39% market share in 2025 and remains the core route to market, while the online sub-channel within B2C is projected to grow at a 10.84% CAGR to 2031 in the India washing machine market. Brand-owned portals and marketplaces are replicating the in-store value proposition with fast delivery, installation, and extended support. Financing tools that reduce upfront burden have expanded adoption in non-metro markets and increased consideration for fully automatic machines. Exclusive online launches for premium machines have also become common, using digital discovery to seed interest before broader retail rollout in the India washing machine market. These shifts are gradually reallocating demand across retail formats while preserving the primacy of physical stores for experience-led validation.

B2B sales remain an important secondary channel for commercial buyers that require integration with service contracts and predictable supply. Specialty and multi-brand chains continue to anchor the last mile for demonstrations, exchanges, and immediate fulfillment in the India washing machine market. Retail footprints owned or controlled by brands help improve margin capture and facilitate deeper customer education. As QR-linked product information and energy data standardize discovery across channels, switching frictions between online and offline paths are decreasing. The result is a more fluid omnichannel environment for the India washing machine market over the forecast period.

Geography Analysis

North India accounted for a 34.98% market share in 2025, and South India is forecast to grow the fastest at a 9.78% CAGR through 2031 in the India washing machine market. North India’s mix reflects strong demand from Delhi NCR and prosperous agricultural belts, while urban hubs across the South sustain premium adoption of front-load models. Product planning in both regions now emphasizes energy efficiency, AI-enabled care, and faster cycles to match apartment living and busy schedules. East India’s improving base for premium appliances is supported by brand investments in stores and localized ranges, which are widening access to high-capacity formats. The India washing machine market continues to broaden geographically as digital discovery and nationwide service networks lower adoption barriers beyond metros.

Manufacturing and sourcing footprints are anchored in North and South corridors, where supply bases and logistics nodes have matured. Renewable-power adoption within major plants in India has advanced and is helping brands manage energy cost risk while aligning with corporate sustainability goals. Policy-led localization under the white-goods PLI program supports component depth in hubs such as Chennai and Greater Noida, which benefits washer assembly and cost curves. East and West regions are seeing capacity and retail investments that close distribution gaps and raise the availability of premium SKUs in the India washing machine market. Over the forecast horizon, regional growth is likely to be led by southern urban clusters and by improving demand from secondary cities across the eastern belt.

Environmental constraints, particularly in water-stressed states, are steering households toward efficient front-loaders and shorter-use cycles that conserve resources in the India washing machine market. Product features like low-pressure operation and microplastic capture are creating tangible value for consumers facing irregular supply and rising awareness of environmental impacts. Connected energy monitoring further increases control over running costs, which amplifies the appeal of premium, inverter-led platforms. As brands scale local assembly and strengthen service networks across all regions, product availability and after-sales support will continue to improve. These factors together support sustained regional expansion in the India washing machine market through 2031.

Competitive Landscape

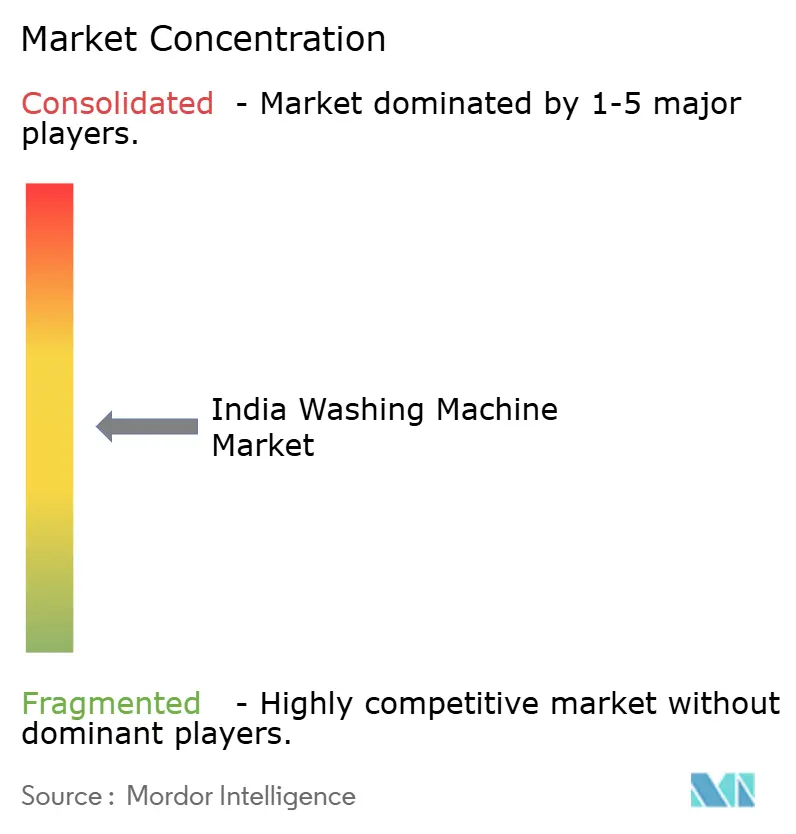

The India washing machine market is concentrated, with LG, Samsung, Whirlpool, IFB, and Haier together accounting for significant market share in 2025. Korean majors defend share with vertically integrated supply, AI-enabled platforms, and long-run warranty commitments that reinforce perceived durability and value. IFB remains the leading Indian-origin player in the top tier and has localized key components, reduced debt, and expanded commercial laundry capabilities. Premium competition from BSH focuses on design, cycle speed, and fabric protection, supported by local assembly and capacity additions in Chennai. Collectively, these moves illustrate a sector shifting from assembly-led strategies to technology- and feature-led differentiation in the India washing machine market.

Recent launch activity underscores the premium tilt and the centrality of AI features. Samsung’s latest AI-enabled front-loaders emphasize energy control, downloadable cycles, and faster programs that serve urban households. Haier’s India-first AI Color Panel and remote-management features show how brands are using software and UI innovation to differentiate. IFB’s localization of BLDC motors and controller electronics closes critical cost loops and should support more accessible pricing for advanced platforms in the India washing machine market. BSH’s high-capacity 9-10 kg ranges manufactured in India round out a competitive set that is aligning closely with urban capacity and feature needs.

At the end, semi-automatic models maintain a presence for large rural households with intermittent water supply, supported by 5-star offerings and large-capacity twin-tubs. Electrolux and other established names continue to build out localized assortments and service to address mainstream and premium needs in India. Awards and brand campaigns help sustain top-of-mind status for leaders who are pushing AI control and digital integration across home appliances. Core competitive variables now include energy performance, smart-home interoperability, warranty depth, and service footprint, each of which contributes to narrowing differentiation in the India washing machine market. With policy nudges and localized sourcing accelerating, incumbents with engineering depth and scale appear best positioned to defend and extend share through 2031 in the India washing machine market.

India Washing Machine Industry Leaders

LG Electronic Inc.

Samsung India Electronics Ltd

Whirlpool Corporation

IFB

Godrej

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Haier Appliances India launched the F9 Front Load Washing Machine series featuring India's first AI Color Panel with One Touch technology, a 525 mm Super Drum, Direct Motion Motor, and AI Dynamic Balance System, aligning with the Make in India initiative.

- January 2025: Samsung India introduced new 9 kg Front Load Washing Machines as part of the Bespoke AI Laundry Series, equipped with AI Energy Mode, AI Control, AI Ecobubble, Super Speed, and Hygiene Steam, designed specifically for modern Indian households.

- August 2024: BSH Home Appliances Pvt. Ltd. doubled its Chennai factory capacity by adding a second assembly line and launched a new range of Made-in-India Bosch and Siemens front-loading washing machines (9-10 kg capacity), manufactured to German standards and featuring SuperQuick 15'/30' cycles, Speed Perfect for 60-minute full loads, and TUV certification for fabric integrity retention after 50 washes.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines India's washing-machine market as yearly sales of new household washers that clean textiles through water cycles. Coverage spans fully-automatic, semi-automatic, twin-tub, and smart-connected units sold offline, online, and to institutions nationwide.

Scope Exclusion: industrial or coin-laundry machines, aftermarket parts, and refurbished units are not covered.

Segmentation Overview

- By Product

- Front Load

- With Dryers

- Without Dryers

- Top Load

- With Dryers

- Without Dryers

- Twin Tub

- Front Load

- By Technology

- Fully Automatic

- Semi-Automatic

- By Capacity

- Small (Below 6 Kg)

- Medium (6 to 8 Kg)

- Large (Above 8 Kg)

- By Connectivity

- Smart Connected

- Conventional

- By End User

- Residential

- Commercial

- By Distribution Channel

- B2C/Retail

- Multi-brand Stores

- Exclusive Brand Outlets

- Online

- Other Distribution Channels

- B2B/Directly from the Manufacturers

- B2C/Retail

- By Geography

- North India

- West India

- South India

- East India

Detailed Research Methodology and Data Validation

Primary Research

We talk with OEM managers, big-box and regional retailers across tier-I and tier-II cities, logistics firms, and poll recent buyers online. These conversations check unit splits, average prices, and the rise of smart models.

Desk Research

Mordor analysts blend National Statistical Office spend tables, DGCI&S import lines, Bureau of Energy Efficiency star-label logs, and GST dashboards. Trade briefs from the Consumer Electronics & Appliances Manufacturers Association, leading business dailies, and audited filings retrieved through D&B Hoovers plus Dow Jones Factiva refine price curves and channel mix. Many other open sources underpin the file.

Market-Sizing & Forecasting

A top-down household-penetration build layers urban and rural population, new dwelling completions, and ownership ratios, then meets spot bottom-up reads such as factory dispatch snapshots and retailer sell-out audits. Key variables like per-capita income, inverter-motor uptake, e-commerce share, ticket size, and PLI-driven local output feed an ARIMA forecast we stress-test with interviewees. Gaps are bridged by interpolation tied to the nearest audited signal.

Data Validation & Update Cycle

Outputs are matched against customs values, BEE shipment rolls, and quarterly disclosures; anomalies trigger swift reconfirmation calls. Models refresh yearly, with interim tweaks when major policy or supply shifts loom.

Why Mordor's India Washing Machine Baseline Commands Reliability

Published numbers vary because firms choose different scopes, price bases, and refresh speeds. Gaps often arise when others skip premium smart units, fix exchange rates, or roll pandemic rebounds forward; we realign every year, hold figures in constant-2025 rupees, and anchor judgments in sell-through evidence.

This comparison shows how our clear scope, steady refreshes, and dual validation steps give decision-makers a balanced baseline they can trust.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.39 B (2025) | Mordor Intelligence | - |

| USD 3.07 B (2024) | Regional Consultancy A | Fixed FX; omits premium smart units |

| USD 1.90 B (2024) | Industry Journal B | Semi-automatic only; shipment value not marked-up |

| USD 2.29 B (2023) | Global Consultancy C | Trend roll-forward; ignores PLI output bump |

This comparison shows how our clear scope, steady refreshes, and dual validation steps give decision-makers a balanced baseline they can trust.

Key Questions Answered in the Report

What is the India washing machine market size in 2026, and where is it projected by 2031?

The India washing machine market size is USD 4.14 billion in 2026 and is projected to reach USD 5.27 billion by 2031, at a 4.98% CAGR.

Which product type is growing fastest in India through 2031?

Front-load models are the fastest-growing product type, with an expected 8.44% CAGR to 2031 as premium features and efficiency gains attract urban buyers.

What capacity range leads demand in India, and what is the upgrade trend?

The 6-8 kg capacity band leads with 62.39% share in 2025, while above-8 kg models are set to grow at a 9.98% CAGR through 2031, reflecting demand for larger loads and fewer cycles.

How is policy support influencing domestic manufacturing for washers?

The white-goods PLI program targets higher local value addition and incentivizes capacity and component localization, which supports lower import exposure over time.

What role is connectivity playing in consumer adoption?

Smart-connected washers are projected to grow at a 15.49% CAGR as AI-enabled control, energy monitoring, and app-linked programs enhance convenience and lifetime value.

Which region currently leads, and which is the fastest growing?

North India leads with a 34.98% share in 2025, while South India is the fastest-growing region at a 9.78% CAGR through 2031.

Page last updated on: