Smart Insulin Pens Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

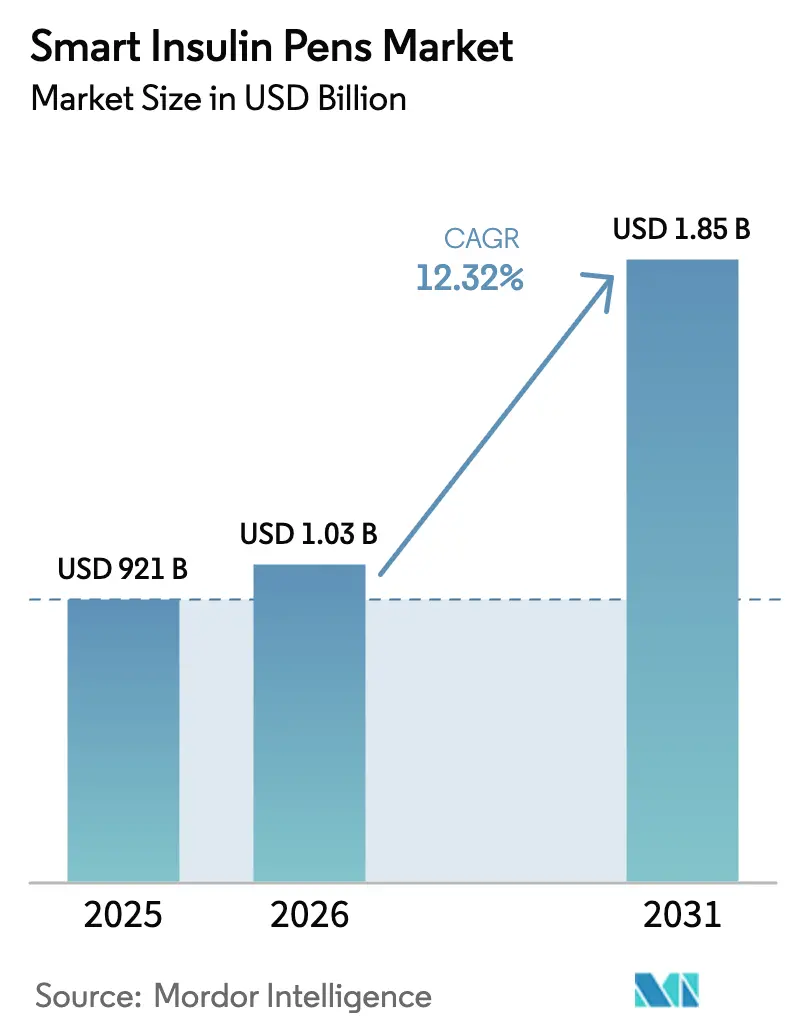

| Market Size (2026) | USD 1.03 Billion |

| Market Size (2031) | USD 1.85 Billion |

| Growth Rate (2026 - 2031) | 12.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Insulin Pens Market Analysis by Mordor Intelligence

smart insulin pens market size in 2026 is estimated at USD 1.03 billion, growing from 2025 value of USD 921 million with 2031 projections showing USD 1.85 billion, growing at 12.32% CAGR over 2026-2031. Rising diabetes prevalence, wider deployment of connected drug-delivery ecosystems, and supportive reimbursement measures remain the primary growth catalysts. Regulatory focus on device cybersecurity and data interoperability continues to favor companies with deeper engineering resources, while the addressable population of untreated adults with diabetes creates a long-run volume opportunity. Ongoing manufacturing expansions by large insulin producers further confirm demand visibility and help stabilize supply across key regions.

Key Report Takeaways

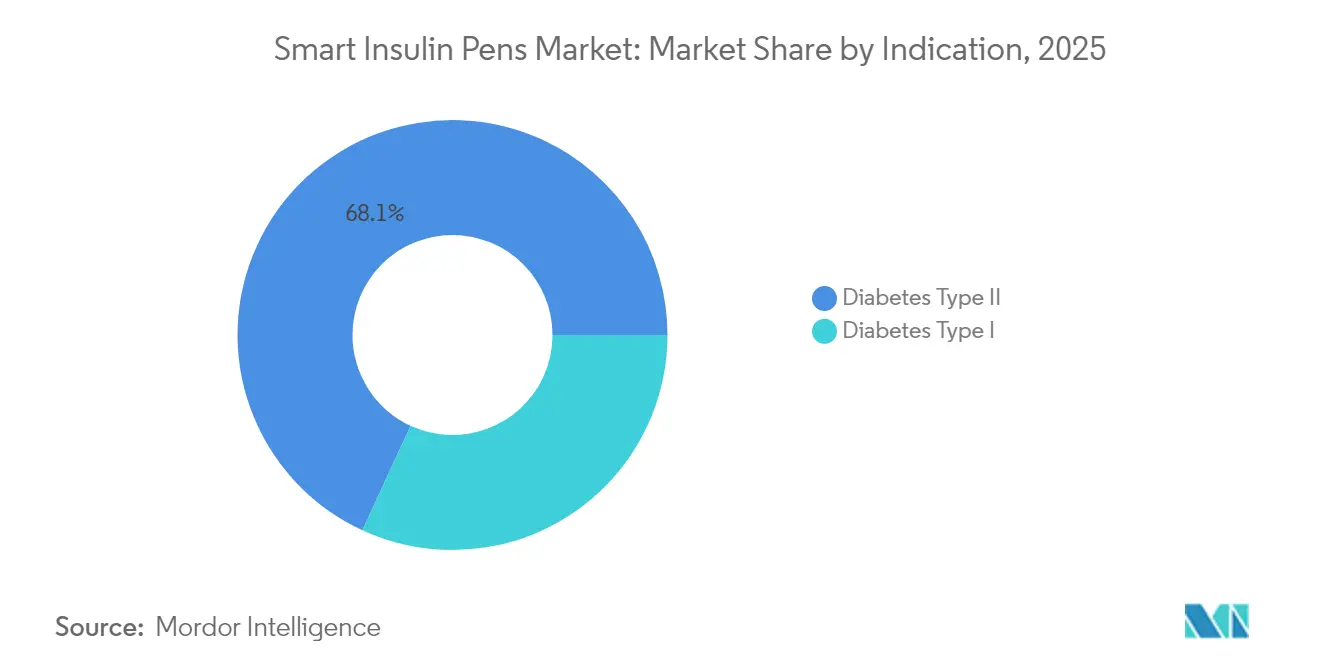

- By indication, Type 2 diabetes held 68.12% of smart insulin pens market share in 2025, whereas Type 1 diabetes is projected to grow at 14.02% CAGR to 2031.

- By product type, reusable devices led with 55.78% revenue share in 2025; disposable variants are set to post a 13.84% CAGR through 2031.

- By connectivity, Bluetooth-enabled models commanded 70.62% of the smart insulin pens market size in 2025; multi-protocol solutions will accelerate at 14.09% CAGR to 2031.

- By insulin-type compatibility, rapid-acting analogs were the dominant class in 2025, whereas long-acting analogs are set to expand at a 13.21% CAGR from 2026 to 2031.

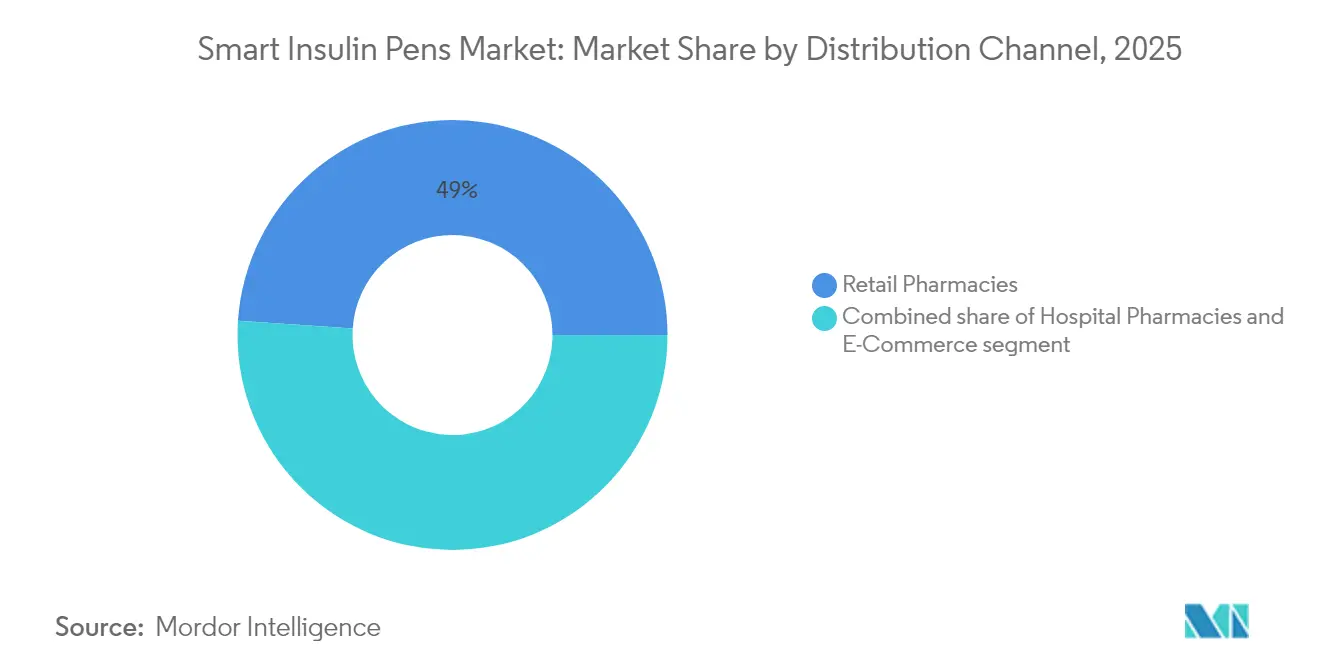

- By distribution channel, retail pharmacies held 48.95% share in 2025, while e-commerce platforms are poised to record a 14.58% CAGR over the same period MORDORINTELLIGENCE.COM.

- By end user, hospitals and clinics accounted for 51.72% share in 2025, whereas home-care settings are projected to deliver a 14.76% CAGR through 2031 MORDORINTELLIGENCE.COM.

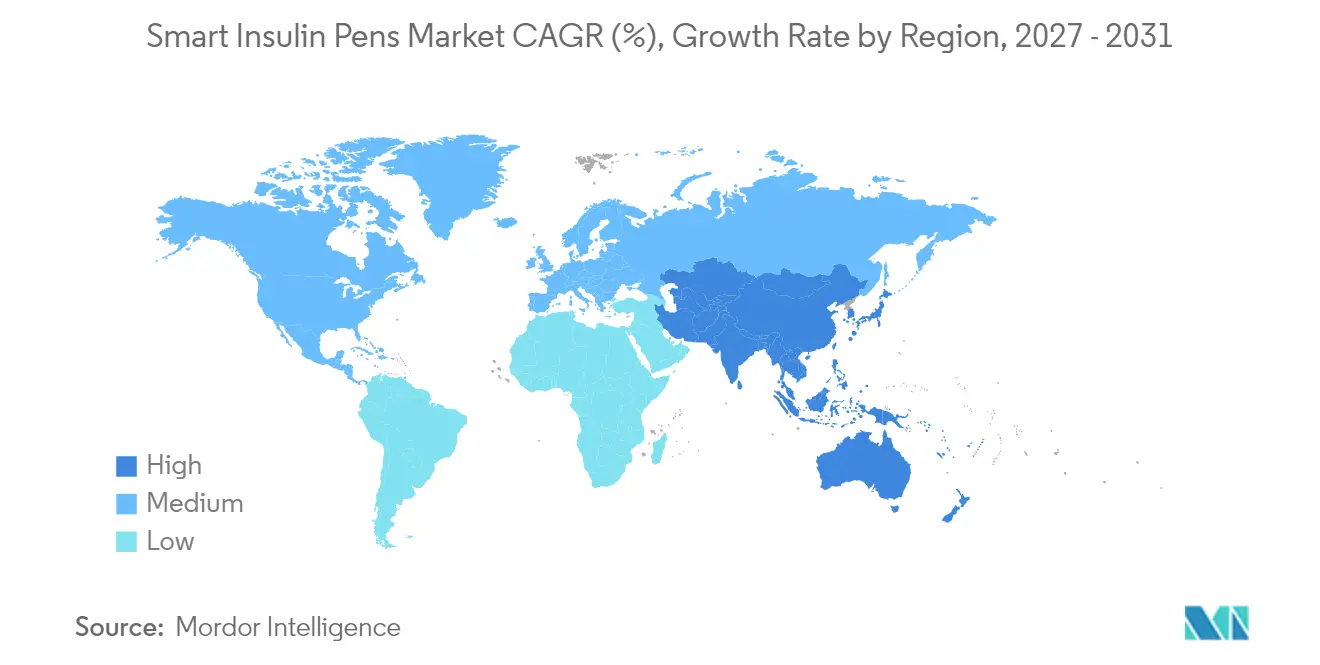

- By geography, North America accounted for 38.10% revenue share in 2025, while Asia-Pacific is expected to register the fastest 13.18% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Smart Insulin Pens Market*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Global Diabetes Burden | +3.2% | Global (high in Asia-Pacific & Middle East & Africa) | Long term (≥ 4 years) |

| Shift Toward Connected Drug Delivery | +2.8% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Favorable Government Reimbursement Policies | +2.1% | North America & Europe, selective Asia-Pacific | Short term (≤ 2 years) |

| Continuous Glucose Monitoring Integration | +2.4% | Global, led by North America & Europe | Medium term (2-4 years) |

| Growing Adoption Of Digital Health Platforms | +1.7% | Global (early in developed markets) | Medium term (2-4 years) |

| Rising Investments In Diabetes Technology | +1.3% | Global (concentrated in North America & Europe) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Global Diabetes Burden

More than 800 million people live with diabetes, and cases are projected to reach 783.2 million by 2045, underscoring the sustained demand outlook for the smart insulin pens market[1]Centers for Disease Control and Prevention, “National Diabetes Statistics Report,” cdc.gov. The Western Pacific region alone counts 206 million cases, amplifying the need for scalable insulin delivery solutions[2] U.S. Food and Drug Administration, “Cybersecurity in Medical Devices,” fda.gov Source: International Diabetes Federation, “IDF Diabetes Atlas,” idf.org. Diabetes-related mortality is on track to rise 10% by 2030, pressuring health systems to adopt technologies that reduce complications through tighter glycemic control mdpi.com. Economic costs already exceed USD 966 billion globally and are set to top USD 1 trillion by 2045, strengthening the value-based argument for connected dosing devices that cut hospitalization rates. Against this backdrop, precise dosing support, missed-injection alerts, and cloud-based reporting position smart pens as essential tools in chronic-care pathways.

Shift Toward Connected Drug Delivery

Smart insulin pens now function as nodes within broader digital ecosystems. Tandem’s FDA clearance for Control-IQ+ in March 2025 widened automated insulin therapy to Type 2 patients, validating platform scalability. Studies show connected delivery can boost time-in-range by 22.4% and trim HbA1c by 1.6%. AI-driven dose advisors are moving from in-silico trials to commercial products, extending competitive moats for first movers. Interoperability designations let users combine components from multiple vendors while maintaining safety, reinforcing network effects that favor integrated offerings over standalone pens.

Favorable Government Reimbursement Policies

The Medicare USD 35 monthly insulin cap slashes out-of-pocket costs, encouraging technology upgrades among older patients[3]Centers for Medicare & Medicaid Services, “Insulin Coverage Updates,” cms.gov. Disposable insulin delivery devices now gain Part D coverage pathways, while pumps fall under Part B, creating parallel reimbursement routes that producers can tap. Remote-patient-monitoring programs that incorporate smart insulin pen data have delivered 5% fewer emergency department visits, helping payers justify device funding. These combined policies move smart pens from discretionary purchases to reimbursable tools inside value-based models.

Continuous Glucose Monitoring Integration

Abbott and Medtronic’s 2024 alliance to merge FreeStyle Libre data with InPen dosing established the first FDA-cleared Smart-MDI system. Real-world evidence confirms superior time-in-range and fewer missed bolus doses when smart pens synchronize with CGM feeds. Further, algorithms that parse CGM patterns now produce predictive dosing suggestions, shifting care from reactive adjustments to proactive optimization.

Restraints Impact Analysis of Smart Insulin Pens Market*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium Pricing And Affordability Issues | -2.1% | Global (highest in emerging markets) | Medium term (2-4 years) |

| Data Security And Regulatory Compliance Challenges | -1.8% | Global (strict in North America & Europe) | Short term (≤ 2 years) |

| Limited Healthcare Infrastructure In Emerging Markets | -1.4% | Asia-Pacific, Middle East & Africa, Latin America | Long term (≥ 4 years) |

| Preference For Alternative Non-Invasive Therapies | -0.9% | Global (greater in developed markets) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium Pricing and Affordability Issues

An insured U.S. patient may pay USD 35 monthly for Medtronic’s InPen, yet uninsured users can face bills exceeding USD 200. In China, only 11.4% of Type 1 patients adopt insulin pumps due largely to cost hurdles, signaling a similar affordability gap for smart pens. Tiered pricing and patient-assistance programs have emerged, but broader uptake still hinges on proof that premium devices cut long-term spending through fewer acute events.

Data Security and Regulatory Compliance Challenges

FDA Section 524B now compels every connected pen to file cybersecurity plans and software bills of materials, raising development costs and timelines. The EU Medical Device Regulation and GDPR add parallel obligations around data protection and post-market vigilance, advantages that scale better for large incumbents. Persistent alerts about potential pump vulnerabilities show that compliance is a journey, not a milestone, requiring ongoing investment in secure coding, patch management, and incident response.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Smart Insulin Pens Market Segment Analysis

By Indication:

Type 2 Diabetes Dominance Drives Volume GrowthType 2 diabetes commanded 68.12% of smart insulin pens market size in 2025 and remains the largest revenue generator. Uptake is propelled by rising early-insulin initiation and education programs that normalize injection therapy in Asia-Pacific clinics. Clinical studies report 1.6% HbA1c reductions and 22.4% higher time-in-range with automated dosing for this cohort, supporting further penetration. Concurrently, Type 1 diabetes exhibits a 14.02% CAGR, the fastest among all indications. Pediatric approvals for automated dosing systems broaden exposure to technology at a young age, driving lifetime use of app-connected devices. Strong advocacy communities facilitate quick dissemination of best practices, reinforcing demand for advanced pens with predictive algorithms.

The segment mix underscores how indication-specific needs shape feature prioritization. Type 2 users often prefer simplified titration-support functions integrated within primary-care workflows. Type 1 users seek real-time data sharing and customizable alerts that accommodate intensive management. Together, these patterns emphasize that a one-size-fits-all strategy will not maximize the smart insulin pens market; rather, tailored device-software bundles are required to unlock full adoption across indications.

By Product Type:

Reusable Platforms Enable Ecosystem Lock-inReusable devices captured 55.78% revenue in 2025 following vendor emphasis on annual-use pens linked to insulin cartridges and subscription analytics platforms. Repeat consumable sales strengthen customer retention and enable continuous firmware upgrades. Attachments that convert existing analog pens into connected systems grow quickly by offering budget-friendly entry points. Disposable smart pens, however, are pacing at 13.84% CAGR by aligning with single-use preferences in infection-control-sensitive environments and cost-sensitive markets. With streamlined regulatory pathways and lighter electronics, these pens reduce production complexity.

The coexistence of both product types reflects divergent purchasing criteria. High-volume urban centers might favor reusable pens for sustainability and data richness, whereas rural clinics opt for disposables that minimize maintenance. Manufacturers increasingly develop hybrid lines combining reusable electronics with disposable reservoirs, balancing feature depth and affordability. As price sensitivity remains a restraint, product modularity will become central to defending and expanding smart insulin pens market share.

By Connectivity Technology:

Multi-Protocol Solutions Drive InteroperabilityBluetooth leads with 70.62% of 2025 sales, thanks to near-universal smartphone compatibility and proven battery efficiency. However, multi-protocol designs that blend Bluetooth, NFC, and cellular radios are advancing at 14.09% CAGR as payers, providers, and caregivers demand frictionless data flows. NFC addresses secure point-of-care transfers in settings where Wi-Fi or cellular service is inconsistent, while integrated LTE modems ensure continuous cloud sync for pediatric or geriatric users without smartphones. Regulatory encouragement for interoperable platforms accelerates migration toward multi-protocols.

Redundant connectivity minimizes data gaps that could compromise clinical insights. Over time, the migration to flexible radio stacks will help vendors secure hospital contracts that require high uptime and robust encryption. As a result, connectivity innovation remains a key battlefront within the smart insulin pens market and an area where smaller entrants can differentiate without needing extensive consumable portfolios.

By Insulin-Type Compatibility:

Rapid-Acting Dominance Reflects Clinical PreferencesRapid-acting analogs remain the leading compatible class because they serve both basal-bolus and mealtime dosing needs efficiently. Smart pens optimize these insulins by timestamping boluses and prompting corrections when doses are missed. Long-acting analogs, however, show the highest 13.21% CAGR as next-generation weekly formulations lower adherence friction. Pens suited to these long-interval dosings benefit from reminders and adherence dashboards, deepening their value proposition.

Compatibility diversification enables physicians to personalize regimens based on lifestyle data harvested by connected devices. As precision-medicine paradigms take hold, pens that flexibly support multiple insulin types will leverage a broader formulary network, further widening the overall smart insulin pens market size during late-forecast years.

By Distribution Channel:

E-Commerce Disrupts Traditional Pharmacy ModelsRetail pharmacies accounted for 48.95% of 2025 revenues due to established insurance workflows and device training services. Yet e-commerce platforms are set to grow 14.58% CAGR, spurred by direct-to-consumer pricing, automatic refills, and telehealth integration. Subscription models such as Sequel’s USD 50-per-month program demonstrate how online fulfillment can bypass insurer frictions while enhancing adherence. Hospital pharmacies preserve niche roles in acute-care initiation but face budget constraints that limit broader penetration.

Digital-first distribution improves patient convenience, especially in rural zones where brick-and-mortar access is limited. As teleconsultations become routine, digital storefronts stand to become default fulfillment hubs for replacement pens and sensors. This shift forces incumbents to recalibrate channel strategies or risk ceding share to agile e-commerce-native rivals.

By End User:

Home-Care Settings Drive Market TransformationHospitals and clinics retained 51.72% revenue share in 2025, benefiting from bulk purchasing and structured diabetes-education programs. However, home-care environments are expanding fastest at 14.76% CAGR as payers push chronic-care management into community settings. Connected pens transmit dosing data directly into provider dashboards, enabling remote titration and early intervention. Clinical pilots show 1.4% HbA1c improvement and a 5% reduction in emergency visits when home monitoring is combined with structured coaching.

The COVID-19 pandemic normalized telehealth and home-delivery services, permanently altering patient expectations. Smart insulin pens align with these expectations by offering dosing intelligence within personal living spaces. Vendors that provide comprehensive virtual support will be best positioned to capitalize on this transition and enlarge the smart insulin pens market in the latter half of the decade.

Geography Analysis

North America Smart Insulin Pens Market

North America generated 38.10% of 2025 revenue, underpinned by Medicare’s USD 35 monthly insulin cap and well-established reimbursement for connected devices. FDA cybersecurity mandates act as entry barriers that protect incumbent positions while encouraging continued R&D investment. Significant capital commitments—such as Novo Nordisk’s USD 4.1 billion North Carolina expansion—signal long-term confidence in regional demand. Canada and Mexico contribute incremental growth, though fragmented payer landscapes require tailored pricing strategies.

Europe Smart Insulin Pens Market

Europe maintains steady momentum thanks to the Medical Device Regulation, which offers a single CE marking pathway across 27 countries. GDPR compliance raises fixed costs but provides clarity on data-privacy standards. Nations like Italy demonstrate positive cost-effectiveness for advanced insulin delivery, supporting coverage decisions even amid tight national health budgets. Ongoing EUR 1.3 billion insulin-pen investment by Sanofi in Germany underlines the region’s manufacturing relevance.

APAC Smart Insulin Pens Market

Asia-Pacific stands out with a forecast 13.18% CAGR, propelled by urbanization, rising disposable income, and an estimated 109 million undiagnosed diabetes cases. China already exhibits high pen penetration, yet affordability concerns persist, opening space for lower-priced disposable and attachment products. India, Japan, and Australia each show distinct regulatory and reimbursement trajectories, necessitating nuanced market-entry plans. Rapid adoption of mobile-health solutions favors integrated pen-CGM bundles that meet growing demand for remote monitoring across diverse healthcare infrastructures.

Competitive Landscape

The smart insulin pens industry reflects moderate consolidation driven by platform-level competition. Medtronic, Novo Nordisk, Tandem Diabetes Care, and Abbott link smart pens, CGMs, and dosing algorithms into closed ecosystems, deterring patients from piecemeal upgrades. These firms leverage established regulatory teams and cybersecurity frameworks, easing compliance with Section 524B rules. Partnership activity—exemplified by Abbott’s global alliance with Medtronic—expands addressable patient pools and speeds feature upgrades without full in-house development.

Emerging players focus on price disruption and user-centric design. Sequel Med Tech’s direct-to-consumer model lowers monthly costs, while CeQur channels new funding toward simplified wearable patch pens. Technology differentiation increasingly relies on AI-based dose-recommendation engines and multi-protocol connectivity. As payers migrate to outcome-based contracts, vendors that can provide longitudinal evidence of reduced adverse events will gain negotiation leverage.

Barriers to entry now hinge on combined evidence of clinical benefit, cybersecurity readiness, and interoperable architecture. Incumbents with diversified insulin portfolios can subsidize device margins through drug revenue, reinforcing their moat. Meanwhile, white-space remains in emerging markets where price points and distribution logistics challenge premium brands. Strategic local manufacturing and modular product lines could unlock those segments and widen overall smart insulin pens market reach.

Smart Insulin Pens Industry Leaders

Novo Nordisk A/S

Eli Lilly and Company

Medtronic plc

Abbott Laboratories

Ypsomed

- *Disclaimer: Major Players sorted in no particular order

Smart Insulin Pens Market Companies Covered in this Report

- Abbott Laboratories

- Bigfoot Biomedical Inc.

- Cambridge Consultants Ltd.

- Companion Medical (Medtronic InPen)

- DiabNext

- Digital Medics GmbH (Pendiq)

- Eli Lilly and Company

- Embecta Corp.

- Emperra GmbH

- Glytec LLC

- Jiangsu Delfu Medical Device Co.

- Medtronic

- Novo Nordisk

- Owen Mumford

- Patients Pending Ltd. (Timesulin)

- Roche

- Sanofi

- Smiths Group

- Ypsomed

Recent Industry Developments in Smart Insulin Pens Market

- June 2025: Tandem Diabetes Care and Abbott agreed to integrate future glucose-ketone sensor data with automated insulin delivery systems, targeting early diabetic ketoacidosis detection.

- April 2025: Biolinq raised USD 100 million Series C to commercialize multi-analyte wearable sensors relevant for pen-based dosing feedback.

- April 2025: Medtronic filed 510(k) submissions for MiniMed 780G as alternate controller and SmartGuard algorithm as interoperable glycemic controller

- March 2025: Vivani Medical posted positive preclinical data for once-yearly semaglutide implant NPM-139, highlighting new competition vectors in injectable therapy.

- March 2025: Sequel Med Tech commercially launched twiist pump with Abbott Libre 3 Plus integration at roughly USD 50 per month via savings programs.

Smart Insulin Pens Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the smart insulin pens market as connected, reusable or disposable insulin-delivery devices that record dose and timing, often glucose data too, and sync these details through Bluetooth or NFC with a companion app for people living with type 1 or type 2 diabetes. We track factory shipments and related device revenues worldwide and also capture retrofit caps that turn standard pens into connected ones.

Scope exclusion: Conventional non-connected pens and stand-alone insulin pumps sit outside our sizing.

Segments Covered in This Report

- By Indication

- Diabetes Type I

- Diabetes Type II

- By Product Type

- Reusable Smart Pens

- Disposable Smart Pens

- Smart Pen Attachments / Caps

- By Connectivity Technology

- Bluetooth

- Near-Field Communication (NFC)

- Multi-Protocol (Bluetooth + NFC / Cellular)

- By Insulin-Type Compatibility

- Rapid-Acting Analogs

- Long-Acting Analogs

- Premixed Formulations

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- E-Commerce

- By End User

- Home-Care Settings

- Hospitals & Clinics

- Ambulatory Surgical Centers

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Structured calls with endocrinologists, hospital-pharmacy buyers, device product managers, and digital-health payers across North America, Europe, and Asia validate penetration rates, real-world pricing, and replacement cycles, allowing us to fine-tune every secondary assumption.

Desk Research

We begin by screening tier-1 public sources such as the International Diabetes Federation, FDA 510(k) files, Eurostat trade sheets, and national health portals to size insulin users and import flows. Annual reports, 10-Ks, Questel patent pulls, peer-reviewed dosing studies, Volza customs logs, and news feeds in Dow Jones Factiva refine average selling prices and adoption curves. A second sweep reviews reimbursement lists, device-recall notices, and clinical-trial registries, letting our team detect early demand shifts. The titles named are illustrative only; many other publications were cross-checked by Mordor analysts.

Market-Sizing & Forecasting

We anchor 2025 with a top-down prevalence-to-treated build multiplied by smart-pen penetration and a globally weighted ASP. Selected supplier roll-ups and channel checks serve as bottom-up guardrails before totals are reconciled. Key inputs include diagnosed insulin population, pen replacement interval, Bluetooth-module cost erosion, reimbursement ratios, and dose-logging adherence. A multivariate regression, stress-tested by scenario analysis, projects values to 2030.

Data Validation & Update Cycle

Outputs pass two analyst reviews; flagged variances trigger re-checks. Models refresh each year, with interim updates for recalls, reimbursement shifts, or mergers before delivery to clients.

How Mordor Intelligence's Smart Insulin Pens Market Size Compares to Other Published Estimates

Published figures differ because firms vary scope, geography, and currency year.

Mordor Intelligence applies one consistent definition, dual-path validation, and an annual refresh, so inputs stay aligned and current.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.92 B (2025) | Mordor Intelligence | - |

| USD 0.90 B (2025) | Global Consultancy A | Mixes emerging and developed ASPs without currency-timing parity |

| USD 0.85 B (2024) | Industry Tracker B | Historic base year and no primary validation |

| USD 0.18 B (2025) | Trade Journal C | Excludes retrofit caps and NFC models |

This comparison shows that our disciplined variable selection and dual-path modeling give decision-makers a balanced, transparent baseline they can trust and repeat.

Key Questions Answered in the Report

What is the current value of the smart insulin pens market?

The market is valued at USD 1.03 billion in 2026 and is forecast to reach USD 1.85 billion by 2031, growing at a 12.32% CAGR over 2026-2031.

Which segment leads by indication?

Type 2 diabetes holds 68.12% revenue share, while Type 1 diabetes records the fastest 14.02% CAGR through 2031.

How large is North America’s regional share?

North America accounts for 38.10% of global revenue, supported by strong reimbursement and early technology adoption.

What connectivity technology is most common?

What connectivity technology is most common?

Why are multi-protocol pens gaining attention?

They improve data reliability and interoperability, satisfying regulatory and clinical demands for seamless ecosystem integration.

What are the main restraints on growth?

Premium device pricing and heightened cybersecurity compliance costs present the most significant headwinds, especially in emerging markets.

Page last updated on: