Small Modular Reactor (SMR) Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

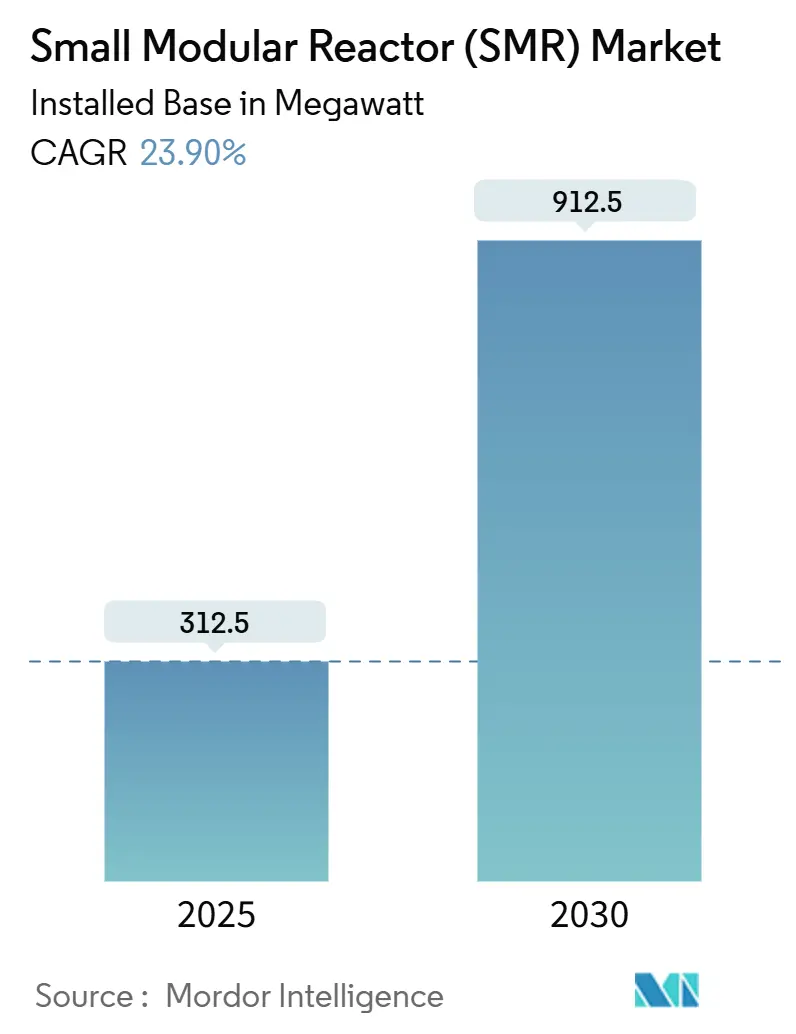

| Market Volume (2025) | 312.5 megawatt |

| Market Volume (2030) | 912.5 megawatt |

| Growth Rate (2025 - 2030) | 23.90% CAGR |

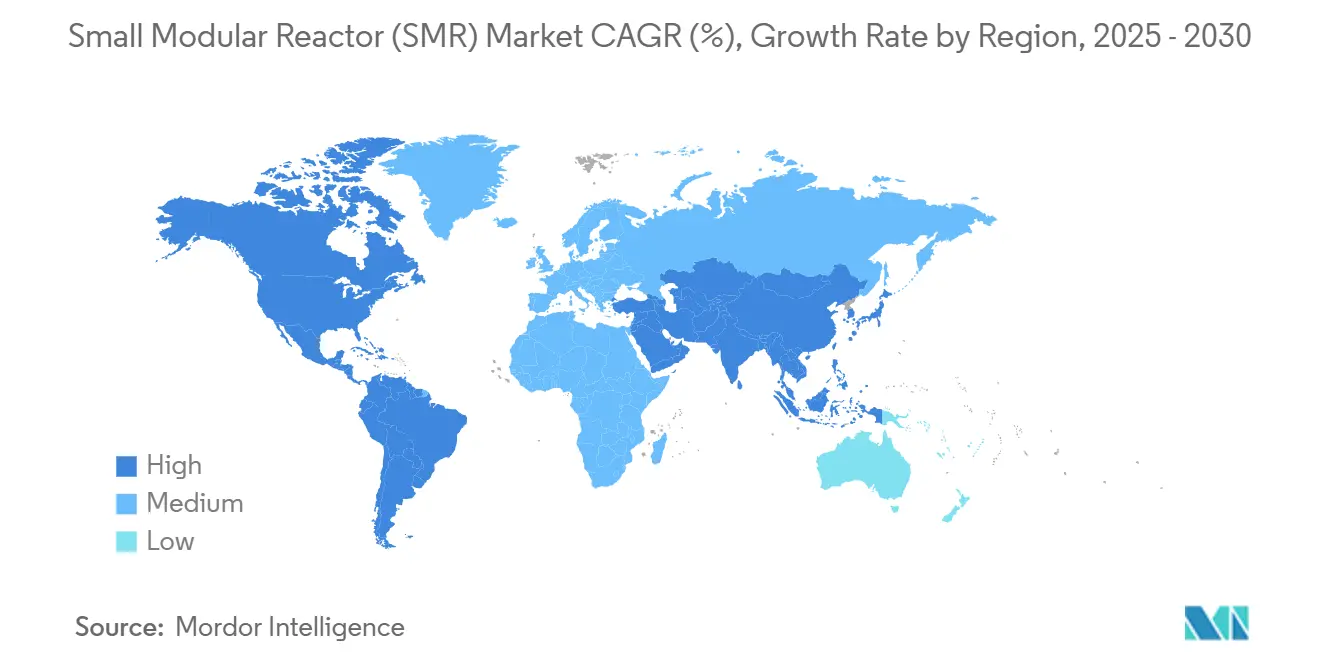

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

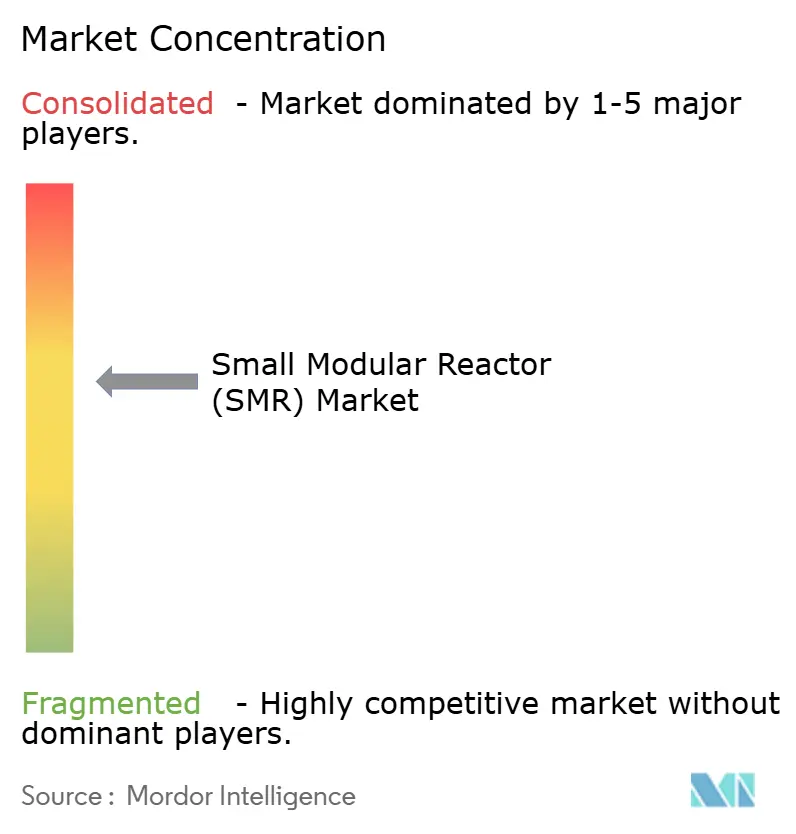

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Small Modular Reactor (SMR) Market Analysis by Mordor Intelligence

The Small Modular Reactor Market size in terms of installed base is expected to grow from 312.5 megawatt in 2025 to 912.5 megawatt by 2030, at a CAGR of 23.90% during the forecast period (2025-2030).

Capacity additions are tracking a clear pivot toward factory-built reactors, which shorten construction schedules and lower upfront capital outlays. Accelerated decarbonization timelines, intensified energy-security legislation, and rising confidence in modular manufacturing all converge to unlock a new wave of nuclear investment. Governments treat SMRs as flexible, low-carbon baseload that complements intermittent renewables, while industrial buyers view them as a single-asset route to deep process-heat decarbonization. Vendors that can secure multi-jurisdictional permits and establish repeatable supply chains benefit first. However, the small modular reactor market will continue to absorb execution risks tied to first-of-a-kind (FOAK) cost overruns, licensing delays, and nuclear-grade fabrication bottlenecks.

Key Report Takeaways

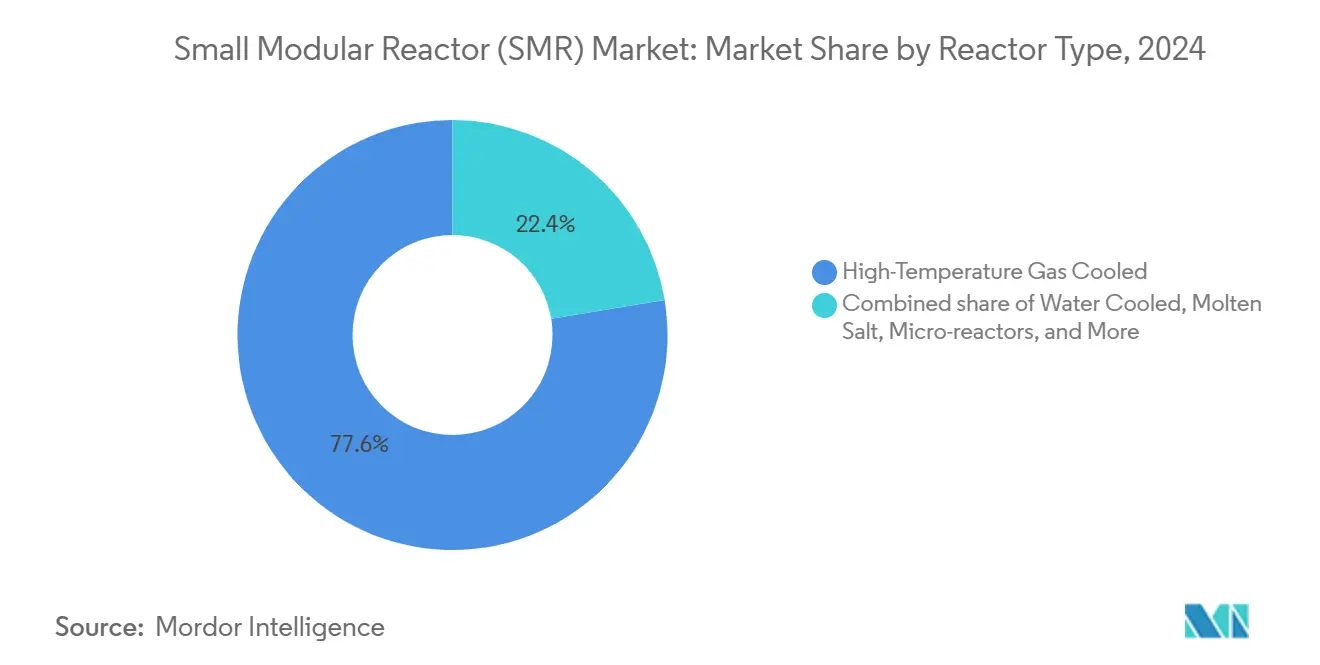

- By reactor type, high-temperature gas-cooled designs led the small modular reactor market with 77.6% of the market share in 2024; water-cooled designs are projected to expand at a 26.3% CAGR through 2030.

- By application, grid-connected power accounted for 76.8% of the small modular reactor market size in 2024, while industrial process heat and steam is projected to advance at a 50.5% CAGR through 2030.

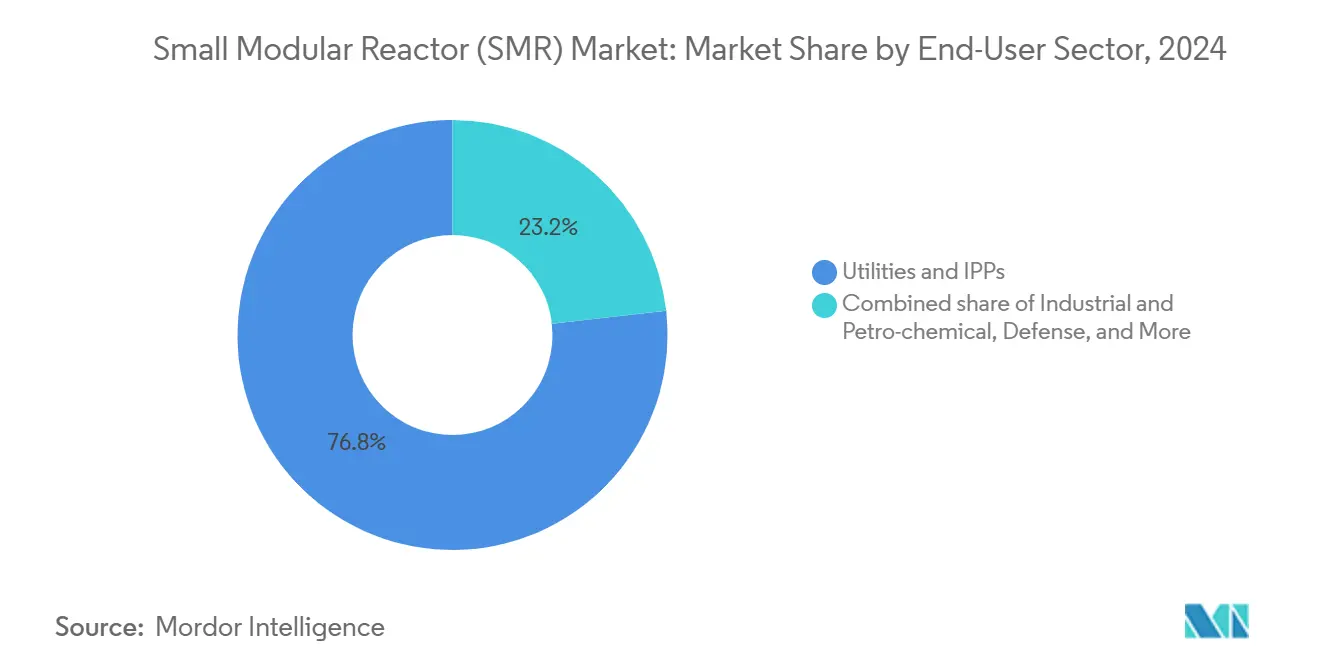

- By end-user, utilities and independent power producers held a 76.8% revenue share in the small modular reactor market for 2024; industrial and petrochemical companies are projected to record the highest CAGR of 42.6% from 2024 to 2030.

- By geography, Asia-Pacific controlled 77.6% of 2024 capacity in the small modular reactor market, whereas Europe is on track for a 39.5% CAGR during the outlook period.

Market Trends and Insights

Drivers Impact Analysis of Small Modular Reactor (SMR) Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid decarbonization mandates | +4.2% | Global (EU, North America lead) | Medium term (2–4 years) |

| Energy-security policies post-2025 | +3.8% | Europe, Asia-Pacific | Short term (≤ 2 years) |

| Modular factory fabrication lowers CAPEX | +3.1% | North America, EU hubs | Long term (≥ 4 years) |

| Rising demand for off-grid industrial heat | +2.9% | Global, mining regions | Medium term (2–4 years) |

| Uranium HALEU fuel-cycle localization | +2.4% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| National SMR export-credit programs | +1.8% | United States, Canada, United Kingdom | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Decarbonization Mandates

Corporate net-zero targets accelerate procurement of dedicated nuclear baseload as clean-energy portfolios mature. The COP28 pledge to triple global nuclear capacity by 2050 is already yielding firm contracts in the small modular reactor market. The technology sector's demand is evident in a 500 MW agreement between Google and Kairos Power, illustrating a direct vendor-customer model that bypasses traditional utility procurement.[1]GE Vernova, “Google Signs 500 MW Advanced Nuclear Collaboration,” gevernova.com Industrial groups value the combined heat-and-power functionality, utilizing SMRs to decarbonize steam and high-temperature processes that renewables cannot simultaneously serve. As 2030 interim climate milestones approach, buyers favor reactors that can be manufactured in controlled factory settings and delivered on compressed schedules, driving momentum in the small modular reactor market.

Energy-Security Policies Post-2025

Geopolitical supply disruptions reposition energy as a national-security priority. The European Union’s REPowerEU scheme enshrines SMRs in its sovereignty toolbox, while the U.S. Export-Import Bank approved a USD 275 million facility for Romania’s NuScale deployment, underscoring how nations leverage credit agencies to seed domestic reactor exports[2]Export-Import Bank of the United States, “Board Approves Financing for Romanian SMR,” exim.gov. Export controls increasingly channel contracts toward allied technology, privileging suppliers from NATO and key Indo-Pacific partners. Cost competitiveness temporarily takes a back seat to the security of supply, thereby enlarging the addressable demand for the small modular reactor market in regions previously reluctant to adopt nuclear solutions.

Modular Factory Fabrication Lowers CAPEX

Shifting construction activity from jobsite to factory floor addresses the cost overruns that plagued gigawatt-scale builds. BWXT’s expansion in Ontario and GE Vernova’s USD 600 million investment in dedicated SMR production lines demonstrate how suppliers seek volume-driven economies of scale. Parallel fabrication and site civil works compress delivery schedules and lower interest during construction, improving overall project LCOE. Vendors shipping sub-modules across borders encounter tension between global cost arbitrage and domestic-content rules spurred by security agendas, yet the underlying industrial logic remains a cornerstone driver for the small modular reactor market.

Rising Demand for Off-Grid Industrial Heat

Process industries tackling Scope 1 emissions tend to gravitate toward reactors capable of delivering 950 °C steam and electricity from a single asset. Dow Chemical’s evaluation of SMR integration into petrochemical complexes typifies this trend. Mining operations in remote regions likewise prioritize transportable nuclear heat and power to replace diesel generation. Premium heat contracts offer margin headroom that compensates suppliers for higher nuclear-specific costs, widening revenue diversity inside the small modular reactor market.

Restraints Impact Analysis of Small Modular Reactor (SMR) Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy multi-jurisdiction licensing | -3.6% | Global (acute in new nuclear countries) | Long term (≥ 4 years) |

| High first-of-a-kind cost overruns | -2.8% | North America, Europe | Medium term (2–4 years) |

| Skilled nuclear-grade manufacturing gap | -2.1% | Global fabrication hubs | Medium term (2–4 years) |

| Public ESG-fund exclusion pressures | -1.4% | Europe, North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lengthy Multi-Jurisdiction Licensing

Design reviews span 5–7 years even for light-water SMRs, and the UK Generic Design Assessment illustrates how comprehensive regulation lengthens commercialization pathways [3]Office for Nuclear Regulation, “Generic Design Assessment Guidance,” onr.gov.uk. Efforts by the IAEA SMR Regulators’ Forum to streamline mutual acceptance progress have been slow because nuclear oversight remains an expression of national sovereignty. Vendors that obtain early approvals secure durable competitive leads inside the small modular reactor market, but diverse technology concepts still require discrete dossiers, amplifying the bureaucracy burden for innovators.

High First-of-a-Kind Cost Overruns

Initial deployments often exceed early capital estimates due to limited supply chain maturity and broad project-specific contingencies. Ontario’s Darlington SMR cluster is budgeted at CAD 20.9 billion (USD 15 billion), reflecting risk premiums embedded in a quartet of 300 MW reactors. Smaller plant scale curtails natural economies of scale, so financial performance hinges on serial production after FOAK completion. Persistent overruns would imperil investor confidence and threaten policy momentum, placing pressure on vendors to deliver visibly on cost discipline across the small modular reactor market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Small Modular Reactor (SMR) Market Segment Analysis

By Reactor Type:

Deployment Speed Favors Water-Cooled DesignsHigh-temperature gas-cooled reactors captured 77.6% of 2024 capacity, equating to the largest slice of the small modular reactor market share. The segment’s appeal rests on its intrinsic safety and outlet temperatures of up to 950 °C for heavy industrial heat. Yet water-cooled reactors will outpace all rivals, logging a 26.3% CAGR through 2030. Regulators are comfortable with pressurized and boiling-water platforms adapted from gigawatt heritage, which cuts certification cycles and opens up near-term sales. As a result, water-cooled technologies represent the vanguard of construction pipelines across Canada, the United States, and select EU states. The small modular reactor market size attributable to water-cooled variants is therefore poised to expand much faster than the enduring but slower-moving HTGR installed base. Over the forecast period, vendors positioned with both reactor classes hedge market uncertainties and capture mutually reinforcing revenue streams.

While molten-salt and fast-spectrum concepts remain in the demonstration phase, they address strategic gaps in fuel utilization and waste minimization. Micro-reactors below 50 MW create an adjacent lane for defense, mining, and arctic communities where transportability and rapid commissioning trump efficiency. Although their absolute contribution to the small modular reactor market size is modest, their double-digit growth introduces technology diversity that keeps competitive pressure on mainstream suppliers.

By Application:

Industrial Heat Reconfigures SMR DemandGrid-connected use dominated in 2024, accounting for 76.8% of installed capacity, reflecting utility familiarity and ease of route-to-market. Nonetheless, industrial process heat is forecast to expand at a 50.5% annual rate as manufacturers decarbonize steam crackers, mineral processing, and ammonia synthesis. The segment's rapid ascent signals that electricity-centric metrics understate total addressable revenue in the small modular reactor market. Off-grid mining and islanded microgrids value continuous baseload and independence from volatile diesel supply chains. Desalination and district-heating pilots in the Middle East and Northern Europe further stretch SMR applicability, although they remain in early commercial testing. Defense contracts, such as the U.S. Department of Defense's Project Pele, increase demand for micro-reactors and demonstrate the military's appetite for resilient power. As the application breadth widens, suppliers must tailor their licensing strategies and business models to match the technical and financial idiosyncrasies across different customer verticals in the small modular reactor industry.

By End-User Sector:

Industry Gains ShareUtilities and independent power producers owned 76.8% of the 2024 capacity, yet industrial and petrochemical buyers are projected to post a 42.6% CAGR to 2030. Direct procurement by data-center operators, specialty chemicals firms, and metals producers compresses deal cycles and de-risks financing via fixed off-take agreements. Mining groups are evaluating SMR integration to reduce diesel dependency in remote pits, potentially generating new long-term service revenue for reactor vendors. Government and defense entities occupy a smaller but stable niche within the small modular reactor market, leveraging sovereign budgets and streamlined approval processes. End-user diversification softens exposure to policy swings in any single sector, though it increases commercial complexity and accentuates the need for configurable reactor-service packages.

Geography Analysis

APAC Small Modular Reactor (SMR) Market

Asia-Pacific anchored 77.6% of 2024 capacity after China connected its ACP100 at Changjiang and South Korea earmarked USD 1.8 billion through 2034 for maritime and land-based SMRs. Streamlined permitting frameworks, state-directed financing, and industrial-policy integration underpin the region’s outsized contribution to the small modular reactor market. Japan’s consortium deals with U.S. suppliers aim to rejuvenate domestic nuclear supply chains and reinforce strategic alliances.

Europe Small Modular Reactor (SMR) Market

Europe emerges as the fastest-expanding theater, with a projected 39.5% CAGR to 2030 underpinned by the European Commission’s February 2024 SMR Alliance. France-Italy cooperation and Czech capital infusions into Rolls-Royce SMR illustrate a collaborative architecture that pools engineering capacity and spreads financial risk within the small modular reactor market.[4] Poland, Estonia, and Finland have all gravitated toward the BWRX-300, signaling a convergence of technology that could expedite permitting across multiple jurisdictions.

The Americas and MEA Small Modular Reactor (SMR) Market

North America maintains a stable but slower growth profile. The U.S. NRC green-lit NuScale’s uprated 77 MWe design, while Ontario granted the first construction license inside a G7 economy. Yet, higher labor costs and complex federal-state regulatory overlays temper the overall advancement of the small modular reactor market. South America and the Middle East & Africa remain nascent, requiring external financing and capacity-building support before meaningful deployments materialize.

Competitive Landscape

The small modular reactor market exhibits moderate concentration, as legacy nuclear conglomerates leverage their deep regulatory pedigrees, while venture-backed startups introduce disruptive reactor physics and digitalize manufacturing. GE Hitachi, Westinghouse, and Rolls-Royce command early utility contracts through evolutionary light-water platforms. In parallel, X-Energy, Kairos Power, and TerraPower champion high-temperature, molten-salt, and fast-spectrum innovations. The International Atomic Energy Agency tracks 98 active SMR concepts, yet only a subset has cleared formal licensing milestones.[5]International Atomic Energy Agency, “SMR Development Status,” iaea.org Strategic battle lines increasingly form around supply-chain localization, serial factory output, and exclusive offtake agreements with industrial heavyweights. Vendor alliances with engineering, procurement, and construction specialists—exemplified by the Tennessee Valley Authority’s Clinch River consortium—fortify execution credibility. Overall, first-mover certifications and manufacturability remain the decisive competitive filters that shape long-term positioning in the small modular reactor market.

Small Modular Reactor (SMR) Industry Leaders

NuScale Power

Rosatom (OKBM)

China National Nuclear Corp.

Rolls-Royce SMR

TerraPower

- *Disclaimer: Major Players sorted in no particular order

Small Modular Reactor (SMR) Market Companies Covered in this Report

- NuScale Power

- Rolls-Royce SMR

- TerraPower

- Rosatom & JSC OKBM

- X-energy

- GE Hitachi Nuclear Energy

- Holtec International

- BWX Technologies

- Mitsubishi Heavy Industries

- China National Nuclear Corp. (CNNC)

- Korea Atomic Energy Research Institute (KAERI)

- EDF-NUWARD

- Ontario Power Generation

- Candu Energy (SNC-Lavalin)

- Ultra Safe Nuclear Corp.

- Westinghouse eVinci

- Fluor Corp.

- AtkinsRealis (formerly SNC-Lavalin)

- Ansaldo Nucleare

- KEPCO E&C

Recent Industry Developments in Small Modular Reactor (SMR) Market

- April 2025: Ontario Power Generation secured a construction license for a BWRX-300 unit at Darlington, inaugurating the first SMR build in a G7 nation.

- March 2025: X-Energy filed a construction permit application for an Xe-100 plant in Texas, marking a significant step in the U.S. commercialization of high-temperature gas-cooled technology.

- March 2025: Canada committed CAD 304 million to AtkinsRéalis for the engineering of next-generation CANDU reactors, thereby strengthening domestic nuclear supply resilience.

- January 2025: Tennessee Valley Authority appointed Bechtel, Sargent & Lundy, and GE Hitachi as prime contractors for the Clinch River SMR, backed by USD 800 million in DOE funding.

Global Small Modular Reactor (SMR) Market Report Scope

Segmentation Overview

| Water Cooled (Land- and Marine-based) |

| High-Temperature Gas Cooled |

| Molten Salt |

| Fast Neutron Spectrum |

| Micro-reactors |

| Grid-Connected Power |

| Off-grid/Remote Electrification |

| Industrial Process Heat and Steam |

| Desalination and District Heating |

| Defense and Military Bases |

| Utilities and IPPs |

| Industrial and Petro-chemical |

| Mining and Remote Operations |

| Government/Defense |

| Research Institutions |

| North America | United States |

| Canada | |

| Europe | United Kingdom |

| France | |

| Italy | |

| Sweden | |

| Denmark | |

| Switzerland | |

| Poland | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Argentina |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Reactor Type | Water Cooled (Land- and Marine-based) | |

| High-Temperature Gas Cooled | ||

| Molten Salt | ||

| Fast Neutron Spectrum | ||

| Micro-reactors | ||

| By Application | Grid-Connected Power | |

| Off-grid/Remote Electrification | ||

| Industrial Process Heat and Steam | ||

| Desalination and District Heating | ||

| Defense and Military Bases | ||

| By End-User Sector | Utilities and IPPs | |

| Industrial and Petro-chemical | ||

| Mining and Remote Operations | ||

| Government/Defense | ||

| Research Institutions | ||

| By Geography | North America | United States |

| Canada | ||

| Europe | United Kingdom | |

| France | ||

| Italy | ||

| Sweden | ||

| Denmark | ||

| Switzerland | ||

| Poland | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Argentina | |

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What capacity additions are projected for the small modular reactor market by 2030?

Total installed capacity is expected to rise from 312.5 MW in 2025 to 912.5 MW by 2030, supported by a 23.9% CAGR.

Which region is growing fastest in small modular reactor market deployment?

Europe shows the highest growth trajectory, with a 39.5% CAGR driven by the European Commissions coordinated SMR Alliance initiatives.

Which reactor type will capture the most incremental demand through 2030 in the small modular reactor market?

Water-cooled SMRs, such as the BWRX-300 and NuScale designs, are forecast to expand at 26.3% CAGR due to regulatory familiarity and near-term build pipelines.

Why are industrial companies investing directly in the small modular reactor market?

Industrial buyers seek dedicated baseload electricity and high-temperature steam to decarbonize operations, and project timelines align with 2030 net-zero milestones.

How do factory-built modules improve project economics for small modular reactor market?

Modular fabrication shifts critical work to controlled environments, enhancing quality, compressing schedules, and reducing interest during construction - all of which lower levelized costs over the plant lifecycle.

Page last updated on: