Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

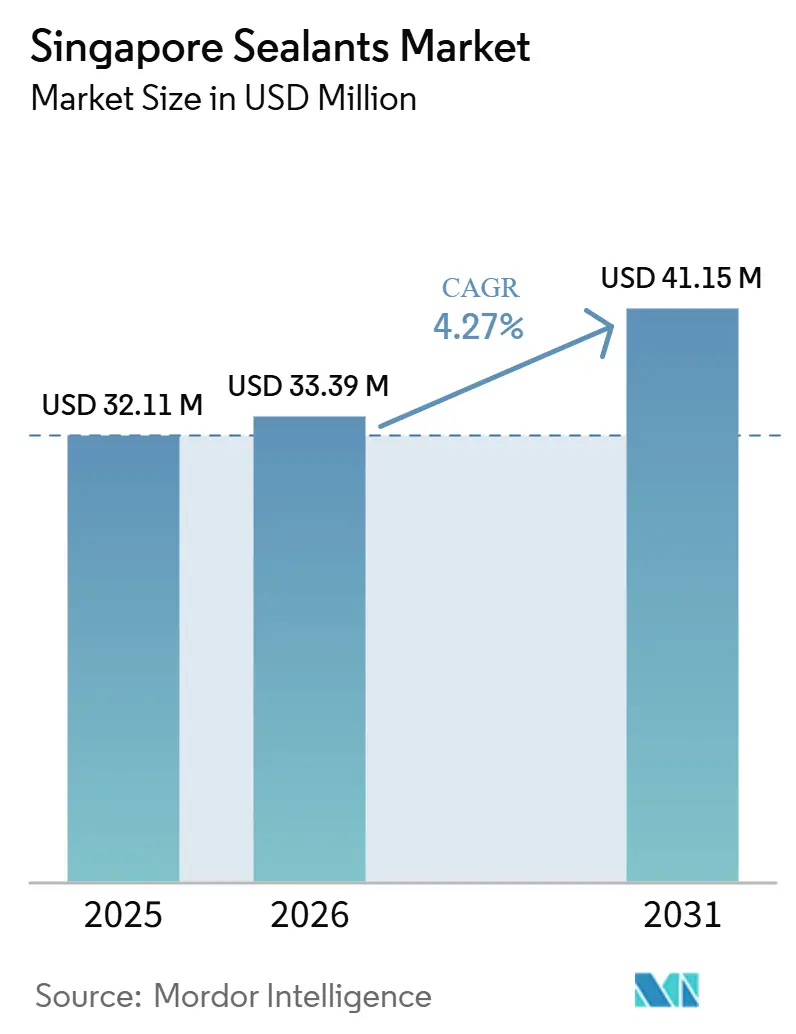

| Base Year Market Size (2025) | USD 32.11 Million |

| Market Size (2026) | USD 33.39 Million |

| Market Size (2031) | USD 41.15 Million |

| Growth Rate (2026 - 2031) | 4.27% CAGR |

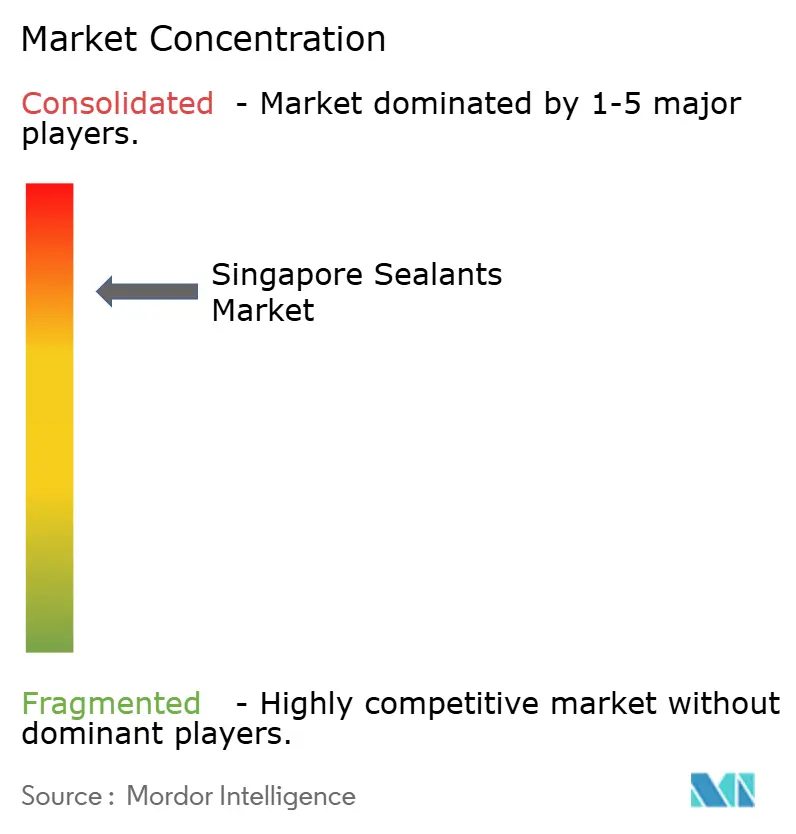

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Sealants Market Analysis by Mordor Intelligence

The Singapore Sealants Market size is expected to grow from USD 32.11 million in 2025 to USD 33.39 million in 2026 and is forecast to reach USD 41.15 million by 2031 at 4.27% CAGR over 2026-2031. Public-sector rail extensions, pandemic-backlog housing completions, and semiconductor clean-room upgrades collectively reinforce a steady contracting pipeline that keeps procurement volumes resilient even as project mix shifts toward higher technical specifications. On the supply side, silicone feedstock price swings linked to Chinese environmental curbs compress margins and accelerate resin substitution toward polyurethane and hybrid polymers. Migrant-labor quotas and higher work-permit levies raise on-site application costs, encouraging Design for Manufacturing and Assembly adoption that moves sealant work upstream into factories and rewards distributors able to provide training and batch traceability. Amid these dynamics, multinational formulators leverage laboratory investments and vertical acquisitions to lock in specification advantages, while nimble local distributors carve service-led niches with just-in-time inventory and small-batch customization.

Key Report Takeaways

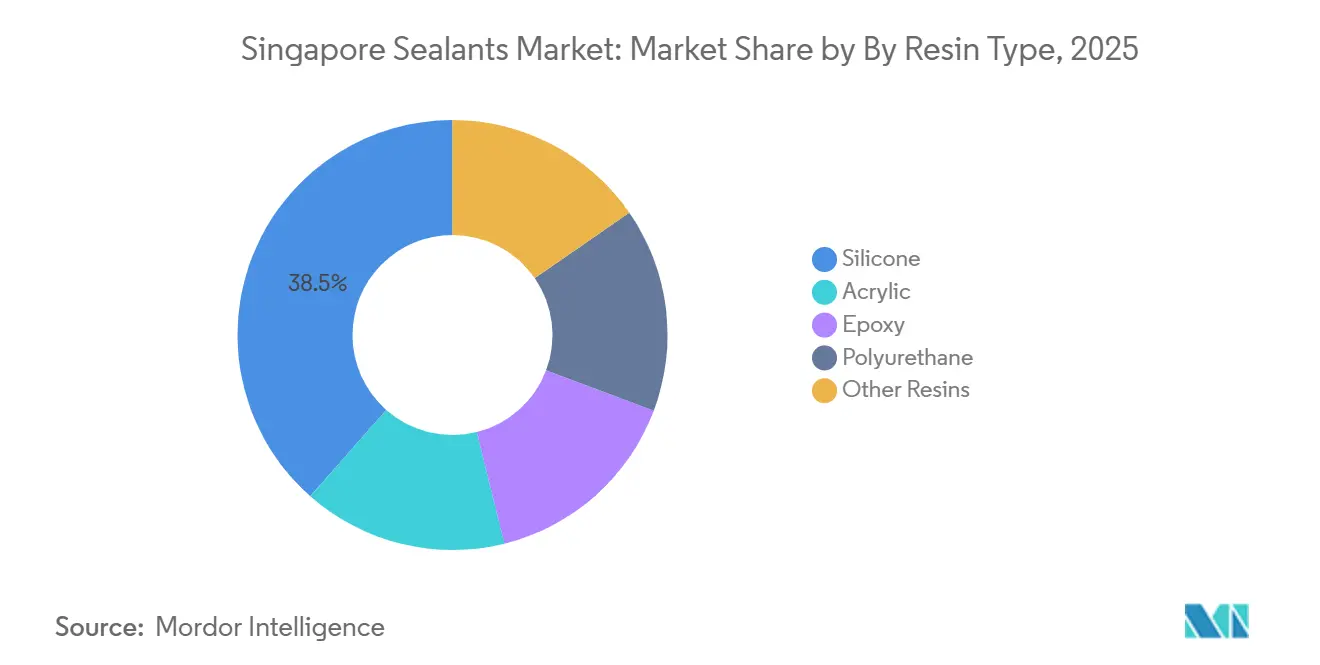

- By resin type, silicone commanded 38.50% of Singapore sealants market share in 2025, whereas polyurethane is projected to expand at a 6.21% CAGR from 2026 to 2031.

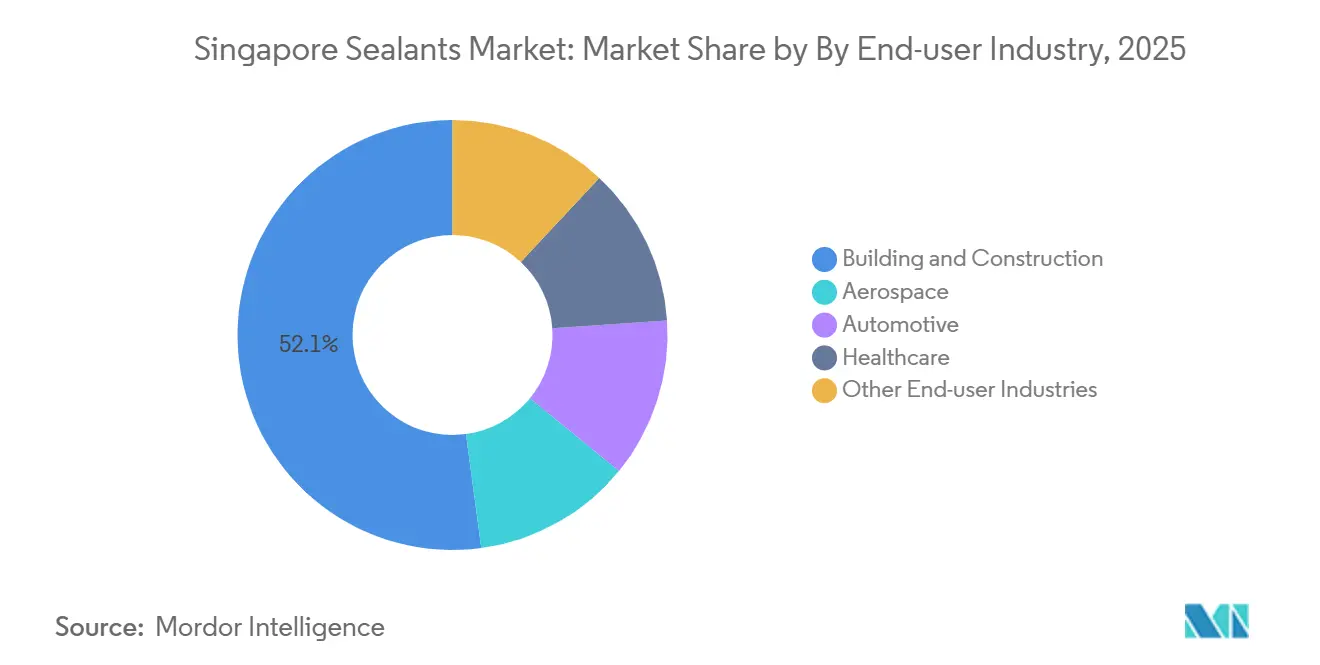

- By end-user industry, building and construction led with 52.14% revenue share in 2025, while aerospace is forecast to register the fastest growth at a 6.43% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Singapore Sealants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated public-sector infrastructure pipeline | +1.20% | National | Medium term (2-4 years) |

| Transition to green-certified building envelopes | +0.90% | National | Long term (≥ 4 years) |

| Semiconductor clean-room expansion | +0.80% | National | Medium term (2-4 years) |

| Growing aircraft MRO hub status at Seletar and Changi | +0.60% | National | Long term (≥ 4 years) |

| Government incentives for low-VOC materials | +0.40% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Public-Sector Infrastructure Pipeline

Five concurrent rail packages, the Jurong Region Line, Cross Island Line Stage 1, Circle Line Stage 6, Thomson-East Coast Line Stage 5, and Downtown Line Stage 3 East, will introduce dozens of stations that require fire-rated tunnel, platform, and concourse joints, sustaining annual demand for fast-cure, low-shrink silicone, polyurethane, and polysulfide grades[1]Land Transport Authority, “Rail Projects,” lta.gov.sg. The Urban Redevelopment Authority’s Master Plan pledges more than 80,000 new residential units, while Housing and Development Board data lists 127 active projects in early 2026, collectively locking in multi-year sealant volumes. CONQUAS 2025 now ties functional-test results to Temporary Occupation Permit issuance, elevating the premium on products that achieve leak-free glazing and ponding compliance in a single pass. Contractors, therefore, favor formulations with primer-less adhesion and extended movement capability that shorten remediation cycles. Distributors that supply site training and accelerated-cure mock-ups strengthen specification pull-through and repeat orders.

Transition to Green-Certified Building Envelopes

Singapore's Green Mark guidelines emphasize reducing life-cycle carbon footprints and encourage the use of low-emission sealants. These sealants must hold certifications such as GEV EMICODE EC1 PLUS, the Singapore Green Label, or equivalent. Sika's products, Sikaflex Purform and SikaTop-540 Seal, comply with various indoor-air-quality standards, supporting developers in obtaining Leadership in Energy and Environmental Design (LEED) credits. Additionally, these products help developers qualify for Green Mark incentives, including gross floor area benefits. Henkel’s new Geneo Science Park lab accelerates perfluoroalkyl-substance-free research and development ahead of anticipated National Environment Agency solvent limits, keeping the firm positioned for early compliance bids. Moisture-cure polyurethanes and hybrid silyl-terminated polymers, which emit negligible isocyanates or aromatics, gain share as workplace exposure limits tighten. Developers increasingly specify two-component epoxy-polyurethane hybrids for below-grade waterproofing because they deliver zero shrinkage and prevent delamination in high water-table sites along reclaimed coasts.

Semiconductor Clean-Room Expansion

GlobalFoundries is undertaking a significant wafer-fab upgrade, which requires ISO Class 5 clean rooms. This requirement is driving up the demand for ultra-low-outgassing silicones and epoxies that meet the stringent SEMI F21 and IEST-RP-CC012 tests. Specialty grades like Chemlink M-1 Clean Room not only meet the trace total-organic-carbon thresholds but also resist siloxane outgassing. Furthermore, batch traceability and ISO 9001 warehousing are becoming crucial factors in securing contract awards. Local distributors without controlled-environment storage struggle to participate, concentrating their share with multinationals that host aerospace and electronics divisions under one roof. The Economic Development Board’s advanced-packaging push diversifies opportunities to high-margin assembly adhesives that require far tighter ionic contamination and thermal-outgassing controls than commodity construction sealants.

Growing aircraft Maintenance, Repair, and Overhaul (MRO) hub status

ST Engineering, GE Aerospace, and WingsOverAsia collectively add shop-visit capacity that consumes polysulfide sealants certified to MIL-PRF-81733 and Airbus AIMS 09-00-002 standards. Applications range from fuel-tank fillets to faying surfaces and windshield beds, demanding materials that survive -65 °F to 250 °F duty cycles. Just-in-time delivery and frozen pre-mixed cartridges minimize waste and downtime, offering suppliers attractive service premiums over volume-driven construction grades. Civil Aviation Authority initiatives that brand Singapore as a regional MRO nexus entrench this high-specification demand pattern, with multiyear contracts shielding formulators from commodity cyclicality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile silicone polymer import prices tied to China supply | -0.90% | National | Short term (≤ 2 years) |

| Shrinking public-housing backlog post-HDB 2025 handover peak | -0.50% | National | Medium term (2-4 years) |

| Tight migrant-labor quotas raising on-site application costs | -0.40% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Silicone Polymer Import Prices Tied to China Supply

Spot premiums for dimethyl carbonate increased, and lead times between Asia and Europe lengthened significantly, driven by China's environmental restrictions on silicon-metal smelters[2]Semitech, “Dimethyl Carbonate Price Analysis Q1 2026,” semitech.com. Singapore, fully import-dependent, saw distributors absorb cost spikes because fixed-price public tenders prevented pass-through. Some shifted to acrylic or hybrid polymers, but substitution risks warranty breaches where high movement or ultraviolet (UV) durability is mandatory. Multinationals with multi-regional sourcing diversified feedstock exposure, while smaller players relied on higher inventory holdings, straining working capital.

Shrinking Public-Housing Backlog Post-Handover Peak

The Housing and Development Board delivered all pandemic-delayed flats by March 2025, normalizing new-build volumes and tilting the mix toward renovation and smaller parcels. Although 19,600 Build-To-Order units will still hand over in 2026, future launches will disperse geographically, diluting bulk delivery efficiencies. Retail hardware chains pick up a greater share as homeowners drive patch-and-paint refurbishments. Suppliers focused on industrial cartridge formats face erosion in average order size, intensifying competition and compressing margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Polyurethane Gains on Facade Movement Demands

Silicone retained 38.50% of the Singapore sealants market share in 2025, owing to superior UV resistance and -40 °C to 100 °C service capability. However, polyurethane’s 6.21% CAGR from 2026 to 2031 outpaces the overall Singapore sealants market size as architects specify low-modulus, high-movement products for glass facades and precast concrete joints. SikaHyflex 250 Facade is designed to accommodate significant movement, allowing contractors to widen joints without requiring bond-breaker tape. In humid conditions, where pure silicones often face challenges, hybrid MS-polymers like PENOSIL Facade Joint Hybrid 25LM are highly effective. These polymers adhere well to damp substrates and achieve high emissions standards. Meanwhile, acrylic and butyl mastics continue to be preferred for interior trim and vapor-barrier details, particularly in applications where cost sensitivity is critical, and movement is limited.

The transition from solvent-borne polysulfides to moisture-cure chemistries accelerates under South Coast Air Quality Management District (AQMD) Rule 1124, which bans para-chlorobenzotrifluoride in aerospace sealants by 2028, signaling global supply rationalization that will ripple into Singapore specifications. Producers responding with Product-Weighted Maximum Incremental Reactivity-compliant catalysts highlight a regulatory trend that structurally favors polyurethane and hybrid platforms over legacy polysulfides.

By End-User Industry: Aerospace Outpaces Construction on Maintenance, Repair, and Overhaul (MRO) Investments

Building and construction captured 52.14% of the Singapore sealants market share in 2025, yet aerospace is projected to post the fastest 6.43% CAGR from 2026 to 2031 as ST Engineering doubles engine overhaul bays and GE Aerospace injects multi-year capital into Changi shops. WingsOverAsia's new Seletar hangar, opened in February 2026, adds narrowbody slots that pull polysulfide fuel-tank grades like PPG PR-1776M. Semiconductor clean-rooms, housed under “Other” or healthcare categories, record high-margin growth but off a low base, fueled by GlobalFoundries’ expansion and Micron’s packaging lines.

Automotive uptake remains niche but strategic, as 3M SZ1000 silicone-based cure-in-place gaskets support electric-vehicle battery enclosures assembled in contract factories serving ASEAN markets. Healthcare draws on ISO 22196 antimicrobial silicones for operating-theater walls and cyanoacrylate adhesives for catheter bonding supplied by H.B. Fuller. The divergent trajectories illustrate a maturing residential segment counterbalanced by technologically demanding aerospace and electronics applications that lift average selling prices and require deep application engineering.

Geography Analysis

Singapore’s compact 728 square kilometer (km²) footprint concentrates all demand, yet sub-regional specialization creates four distinct micro-markets. The Marina Bay and downtown core generate continuous curtain-wall demand as developers chase Green Mark Platinum and Leadership in Energy and Environmental Design (LEED) Gold credits requiring low-VOC structural silicones. Northern estates such as Woodlands and Yishun, together with western Jurong, host Housing & Development Board Build-To-Order clusters that consume bulk polyurethane weather-seals. Changi and Seletar precincts anchor MRO activity, driving polysulfide and epoxy throughput. Finally, the Tuas–Jurong Island corridor sustains clean-room and petrochemical sealing uses with ultra-low-outgassing and chemical-resistant grades.

Land Transport Authority projects skew toward western and northern sectors, injecting tunnel-grade silicone and fire-stop formulations from 2026 to 2031. Regulatory mirroring of European Union Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH) propels rapid solvent substitutions; Henkel’s new laboratory in Geneo Science Park positions early to formulate compliant electronic-adhesive alternatives. CONQUAS 2025 banding publicizes developer quality rankings, pushing premium sealant demand in districts where resale premiums matter. Sika’s Elmich buyout bundles membranes, drainage plates, and perimeter seals, simplifying tender compliance for green roofs and podium landscapes prevalent in city-core mixed-use projects.

Import dependence remains a structural vulnerability. Dimethyl carbonate shipment lead times ballooned to 12 weeks early in 2026, incentivizing higher local warehousing and multi-regional sourcing. The Economic Development Board’s semiconductor agenda cements long-run appetite for clean-room formulations, securing a technology-driven buffer against construction cycle dips.

Competitive Landscape

The Singapore Sealants Market is consolidated. Hybrid polymer platforms that merge silicone weather-resistance with polyurethane adhesion open a white-space. Products such as Soudal SMX 506 and Tremco Illmod 600 enjoy CONQUAS-driven pull, where hollow-tile defects and fenestration leaks attract penalties. Sika’s minority stake in Giatec Scientific in 2025 signals the convergence of sealants with sensor-enabled concrete monitoring, hinting at data-layer differentiation rather than chemistry alone.

Singapore Sealants Industry Leaders

3M

Dow

Henkel AG & Co. KGaA

Sika AG

Tremco Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: WEVO-CHEMIE GmbH has established a new production facility in Singapore. This strategic initiative enables the company to meet the increasing demand for polyurethane-based sealants and other products, solidifying its position as a regional manufacturer for the Asia-Pacific market. Production is expected to begin in the third quarter of 2026.

- January 2026: Henkel relocated its Singapore operations to Geneo at Singapore Science Park, establishing a hub that enhances research and development, technical services, and regional supply efficiency, driving Singapore's sealants market growth.

Singapore Sealants Market Report Scope

A sealant is a flexible substance applied to surfaces, joints, or openings to block the passage of fluids, air, dust, and contaminants. Unlike rigid adhesives, sealants remain elastic after curing, allowing them to withstand movement and temperature changes. Common types include silicone and polyurethane, used in construction, automotive, and industrial applications to provide waterproofing, insulation, and durable environmental protection.

The Singapore Sealants Market is segmented by resin type and end-user industry. By resin type, the market is segmented into acrylic, epoxy, polyurethane, silicone, and other resins. By end-user industry, the market is segmented into aerospace, automotive, building and construction, healthcare, and other end-user industries. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Resin Type

| Acrylic |

| Epoxy |

| Polyurethane |

| Silicone |

| Other Resins |

By End-user Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Healthcare |

| Other End-user Industries |

| By Resin Type | Acrylic |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| Other Resins | |

| By End-user Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Healthcare | |

| Other End-user Industries |

Market Definition

- End-user Industry - Building & Construction, Automotive, Aerospace, Healthcare, and Others are the end-user industries considered under the sealants market.

- Product - All sealant products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Silicone, and Others are considered

- Technology - For the purpose of this study, One component and Two component sealant technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms