Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

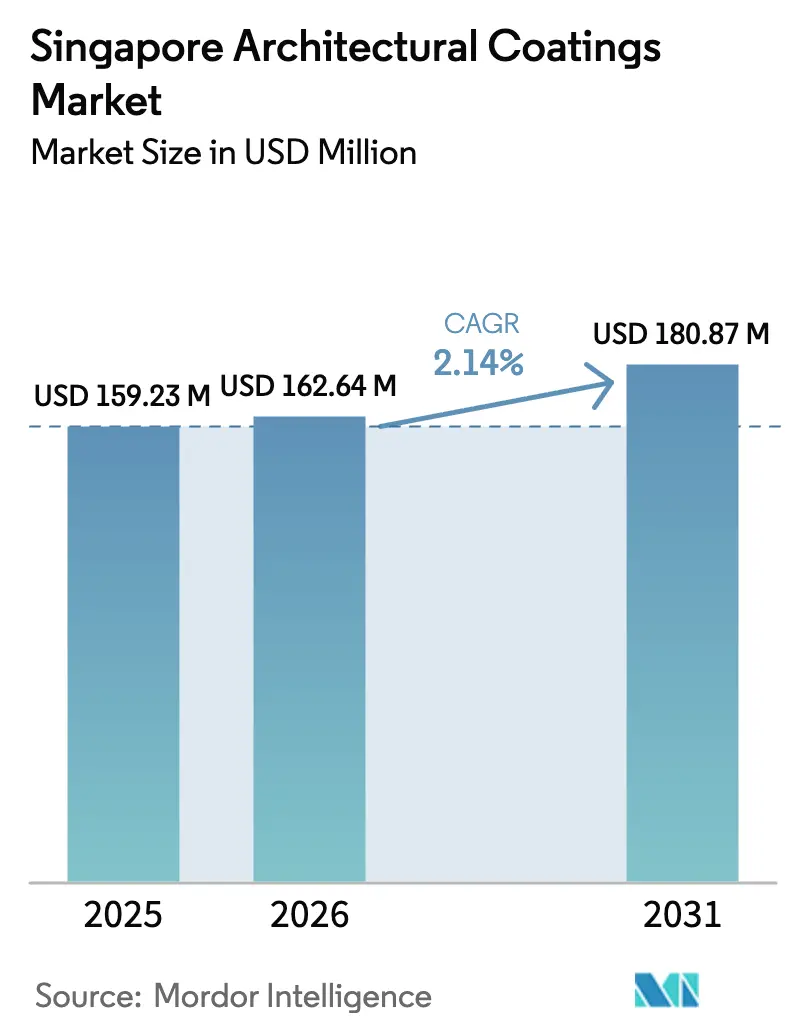

| Base Year Market Size (2025) | USD 159.23 Million |

| Market Size (2026) | USD 162.64 Million |

| Market Size (2031) | USD 180.87 Million |

| Growth Rate (2026 - 2031) | 2.14% CAGR |

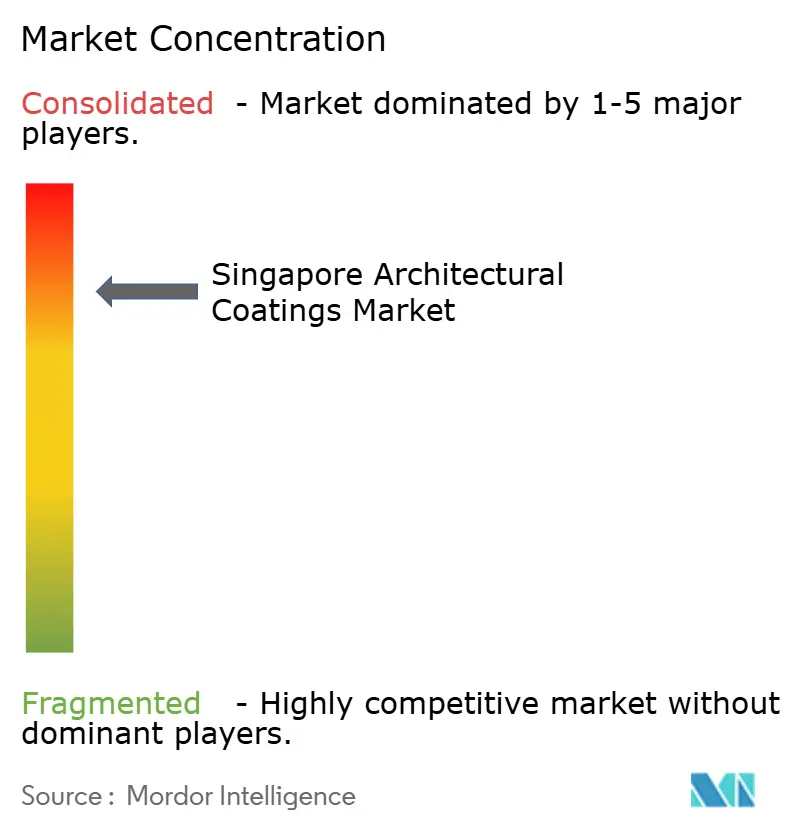

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Architectural Coatings Market Analysis by Mordor Intelligence

The Singapore Architectural Coatings Market size was valued at USD 159.23 million in 2025 and estimated to grow from USD 162.64 million in 2026 to reach USD 180.87 million by 2031, at a CAGR of 2.14% during the forecast period (2026-2031). Steady public-sector repainting programs, stricter green-building codes and selective commercial upgrades sustain incremental demand in this mature construction setting. Expanding low-VOC regulations guide product substitution toward water-borne chemistries, while corporate net-zero targets spur the uptake of cool-roof and heat-reflective solutions. Large public-housing repaint cycles underpin baseline volumes, and ongoing healthcare expansion propels antimicrobial interior formulations. Competitive dynamics favor incumbents that can navigate Green Mark certification, comply with Singapore Green Labelling Scheme limits and supply technically differentiated products.

Key Report Takeaways

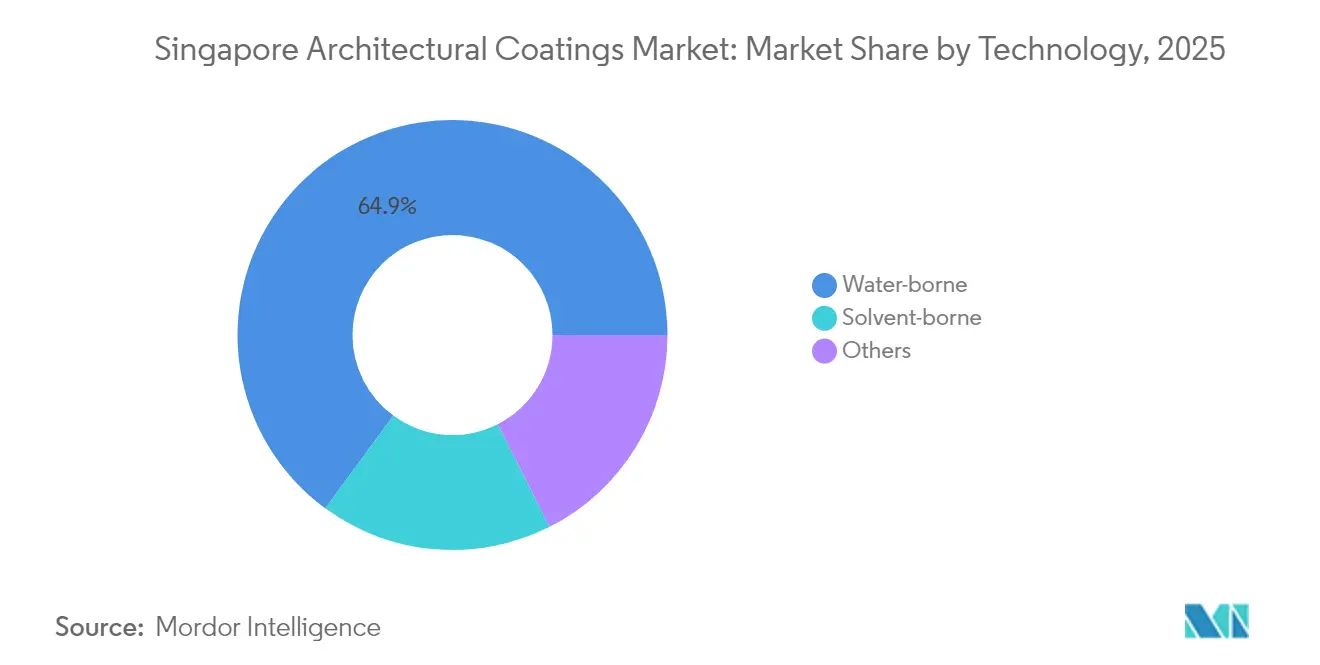

- By technology, water-borne coatings captured 64.92% revenue share in 2025 and remain the fastest-growing segment at a 2.62% CAGR to 2031.

- By resin type, acrylic formulations led with 43.68% share of the Singapore architectural coatings market size in 2025, whereas polyurethane is on track to expand at a 2.38% CAGR through 2031.

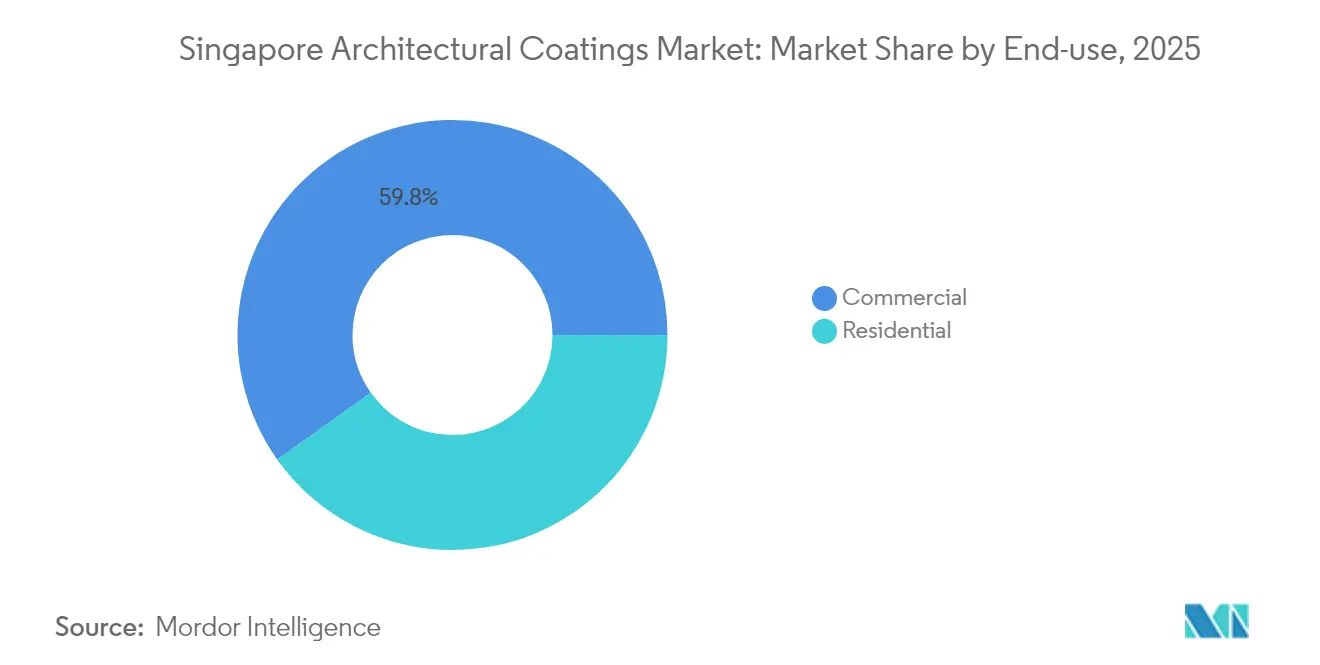

- By end use, commercial construction accounted for 59.82% of the Singapore architectural coatings market share in 2025, but residential demand is forecast to rise at a 2.51% CAGR through 2031, buoyed by Housing Development Board repaint programs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Singapore Architectural Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Green Mark incentives for low-VOC paints | +0.8% | National; new builds and retrofits | Medium term (2-4 years) |

| Repainting of ageing HDB stock | +0.6% | Mature estates island-wide | Long term (≥ 4 years) |

| Corporate net-zero pledges and cool roofs | +0.4% | CBD and industrial zones | Medium term (2-4 years) |

| Antimicrobial paint demand in healthcare | +0.3% | Existing and new medical facilities | Short term (≤ 2 years) |

| Smart tintable coatings pilots | +0.2% | Grade A office developments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Green Mark Incentives Drive Low-VOC Paint Adoption

Elevated Green Mark baselines now oblige every new building to meet certified status, with up-to-3% gross-floor-area bonuses for Platinum Super-Low-Energy ratings[1]Building and Construction Authority, “Green Building Masterplan,” bca.gov.sg. Singapore Green Labelling Scheme rules cap interior paint VOCs at 50 g/L, effectively sidelining most solvent-borne options. A SGD 63 million incentive fund through Q1 2027 subsidizes compliant retrofits, letting developers recoup premium material costs quickly. Owners increasingly specify Green-Mark-ready coatings in advance to avoid future retrofit penalties. These measures channel demand toward high-margin water-borne and bio-based technologies and reinforce Singapore’s role as a proving ground for next-generation sustainable finishes.

HDB Heat-Reflective Paint Rollout Creates Predictable Demand Cycles

The Housing Development Board is applying heat-reflective coatings across roughly 1 million flats by 2030, the largest single coatings initiative ever undertaken locally[2]Singapore Green Building Council, “Green Mark Incentives,” sgbc.sg . Pilot blocks in Tampines logged 2 °C ambient reductions, prompting phased island-wide implementation within the standard 5-7-year repaint schedule. Guaranteed volumes enable manufacturers to fine-tune production and build localized supply chains, aligning product development with Singapore’s high humidity and solar-load realities. The program stabilizes residential offtake even when private construction moderates.

Corporate Net-Zero Commitments Accelerate Cool-Roof Technology Adoption

Developers such as CapitaLand and City Developments Limited now align portfolios with 2050 net-zero trajectories, prioritizing envelope solutions that lower cooling loads. BCA’s Green Buildings Innovation Cluster 2.0 co-funds retrofit pilots, often choosing high-albedo roof coatings for rapid, measurable energy savings. Tenants weigh operational efficiency in lease negotiations, nudging landlords toward reflective products. The expanding ESG disclosure regime renders these upgrades strategic rather than elective, intensifying demand for durable, high-solar-reflectance systems.

Healthcare Sector Drives Antimicrobial Coating Innovation

Woodlands Health Campus, Eastern General Hospital and other expansions embed antimicrobial interiors into baseline specifications. Singapore Standard SS 705 clarifies performance benchmarks, giving facility managers confidence to mandate such coatings during both new builds and routine maintenance. The result is an addressable market that extends beyond new clinical space to include existing ward refurbishments, pushing premium antimicrobial lines from niche to mainstream.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight foreign-labor quotas | −0.5% | Nation-wide repaint projects | Short term (≤ 2 years) |

| Volatile titanium-dioxide prices | −0.3% | All coatings manufacturers | Medium term (2-4 years) |

| Costly waste-paint take-back regulations | −0.2% | Large commercial and public-sector jobs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Foreign-Worker Quotas Constrain Application Capacity

Dependency-ratio ceilings limit overseas labor to 83% of construction workforce, shrinking the pool of skilled painters. Contractors face higher wage bills and stretched schedules, occasionally pushing HDB repaints 6-12 months behind plan. Large applicators trial robotic sprayers on high-rise façades, tripling productivity where geometry suits, but up-front CAPEX and training restrict rapid scaling. Until automation matures, labor scarcity will temper otherwise steady maintenance volumes.

Limited Landfill Capacity Drives Costly Waste-Paint Take-Back

Singapore’s Semakau Landfill reaches design capacity in 2035, prompting NEA to tighten extended-producer-responsibility rules for leftover paint. Contractors must manifest disposal or channel returns through manufacturer take-back schemes, adding logistical overhead. High-volume projects already bake these costs into bids, but smaller applicators struggle, discouraging full-specification purchases and nudging users toward thin-film touch-ups over complete recoats.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Regulatory Pull Cements Water-Borne Leadership

Water-borne products dominated the Singapore architectural coatings market with a 64.92% slice in 2025, and their 2.62% CAGR through 2031 outpaces every rival. This position reflects synchrony with Green Mark VOC ceilings and contractors’ familiarity with current application equipment. Solvent-borne coatings persist only in legacy industrial areas and small-batch specialty finishes. Powder and nascent bio-based alternatives collectively occupy single-digit shares but draw disproportionate researchh and development funding as suppliers seek environmental branding advantages.

Water-borne chemistries now rival solvent-borne in adhesion and weatherability thanks to advances in polymer design and coalescent selection. Rapid drying at high humidity shortens project timelines, a crucial advantage amid labor constraints. The Singapore architectural coatings market continues to test bio-based binders within water-borne matrices, positioning the city-state as a staging ground for region-wide adoption once cost parity is reached.

By Resin Type: Acrylic Holds Sway while Polyurethane Gains Traction

Acrylic systems controlled 43.68% of 2025 value, anchoring bread-and-butter interior finishes and facade topcoats. The segment’s maturity stems from broad color range, UV durability and ease of Green Mark compliance. Polyurethane, however, posts the fastest 2.38% CAGR as specifiers chase longer lifecycle and abrasion resistance on premium commercial towers. Alkyd usage fades under VOC scrutiny, while epoxy and polyester maintain niche roles in floor and metal applications.

Building owners increasingly weigh total maintenance cost, tilting specifications toward higher upfront polyurethane. Coupled with HDB’s interest in service-interval extension, the resin shift pushes formulators to blend acrylic flexibility with polyurethane toughness, spawning hybrid systems that fit within VOC caps and retain familiar application profiles. These trends solidify polyurethane’s ascent without abruptly displacing incumbents, allowing orderly substitution cycles.

By End Use: Commercial Heft Masks Maturing Residential Opportunity

Commercial projects generated 59.82% of 2025 turnover, anchored by continuous Grade A office supply and retail refurbishments. Specifications favor premium multilayer systems, lifting value per square meter even as floor-plate growth tapers. The residential records a healthier 2.51% CAGR, propelled by scheduled HDB heat-reflective deployments. Public housing’s regimented cycles create secure multi-year off-take, insulating the Singapore architectural coatings market against private-sector pauses.

The distinctions between segments are narrowing. Green-building codes bind both commercial and residential structures to similar VOC and performance standards, encouraging manufacturers to leverage common platforms with tailored add-ons. This harmonization streamlines production and distribution in an urban market where storage footprints and logistics windows are constrained.

Geography Analysis

Operating within just 720 km², the Singapore architectural coatings market benefits from unrivaled logistical simplicity. Local plants deliver same-day shipments across the island, lowering inventory requirements and enabling just-in-time servicing of rapid-cycle projects. Centralized BCA regulation ensures uniform technical criteria, eliminating provincial compliance costs seen in larger nations. Mature neighborhoods like Toa Payoh and Ang Mo Kio undergo cyclical repaints, while emerging towns like Punggol provide first-coat opportunities, balancing workload across applicators.

Jurong Island and Tuas house petrochemical and heavy-industry plants that demand specialized high-build protective systems. These clusters also serve as test beds for low-carbon industrial coatings under the Sustainable Jurong Island initiative, opening export pathways once formulations prove out. Port proximity streamlines raw-material inflow and outbound shipments to ASEAN, letting Singapore suppliers serve regional demand without extensive overseas warehousing. Uniform tropical weather simplifies product portfolios, one climatic challenge rather than many, allowing deep optimization for humidity, UV and salt exposure.

Competitive Landscape

The Singapore architectural coatings market exhibits consolidtion. Global multinationals AkzoNobel, PPG and Sherwin-Williams maintain regional hubs, leveraging technology pipelines to compete on niche innovations such as antimicrobial and self-cleaning finishes. Local challengers including Raffles Paint and Seamaster Paint focus on relationship-driven project supply, carving space in mid-tier residential and SME refurbishments. Entry barriers are material. Newcomers must bankroll local testing labs, secure Singapore Green Labelling Scheme seals and build logistics footprints in a dense urban environment where warehouse space commands premium rents. The result is a steady market where leadership tends to reinforce itself, though white-space opportunities persist in specialty coatings aligned with national sustainability targets.

Singapore Architectural Coatings Industry Leaders

Jotun

Kansai Paint Co.,Ltd.

Nippon Paint Holdings Co., Ltd.

AkzoNobel N.V.

Seamaster Paint (Singapore) Pte Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Dulux Professional unveiled low-carbon paints and color-science tools at the Singapore International Green Building Conference 2025 to support next-generation sustainable buildings.

- March 2024: The National Environment Agency declared that, effective 1 Jan 2026, all interior paints retailed in Singapore must contain below 0.01% formaldehyde, reinforcing indoor-air-quality safeguards.

Singapore Architectural Coatings Market Report Scope

Commercial, Residential are covered as segments by Sub End User. Solventborne, Waterborne are covered as segments by Technology. Acrylic, Alkyd, Epoxy, Polyester, Polyurethane are covered as segments by Resin.By Technology

| Water-borne |

| Solvent-borne |

| Others |

By Resin Type

| Acrylic |

| Alkyd |

| Epoxy |

| Polyester |

| Polyurethane |

| Other Resin Types |

By End-Use

| Residential |

| Commercial |

| By Technology | Water-borne |

| Solvent-borne | |

| Others | |

| By Resin Type | Acrylic |

| Alkyd | |

| Epoxy | |

| Polyester | |

| Polyurethane | |

| Other Resin Types | |

| By End-Use | Residential |

| Commercial |

Market Definition

- COMMERCIAL - The Commercial Sector includes the paints and coatings used for hotels, hospitals, educational institutions, government institutions and malls among others. The scope does not include paints and coatings used for infrastructure applications.

- RESIDENTIAL - This section includes interior and exterior paints and coatings used on residential buildings.

- FLOOR AREA - The total floor area comprises of both existing and new floor area for the sub end users considered in the study.

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific end-user segment and country are selected from a group of relevant variables & factors based on the desk research & literature review; along with primary expert inputs.

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms