Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

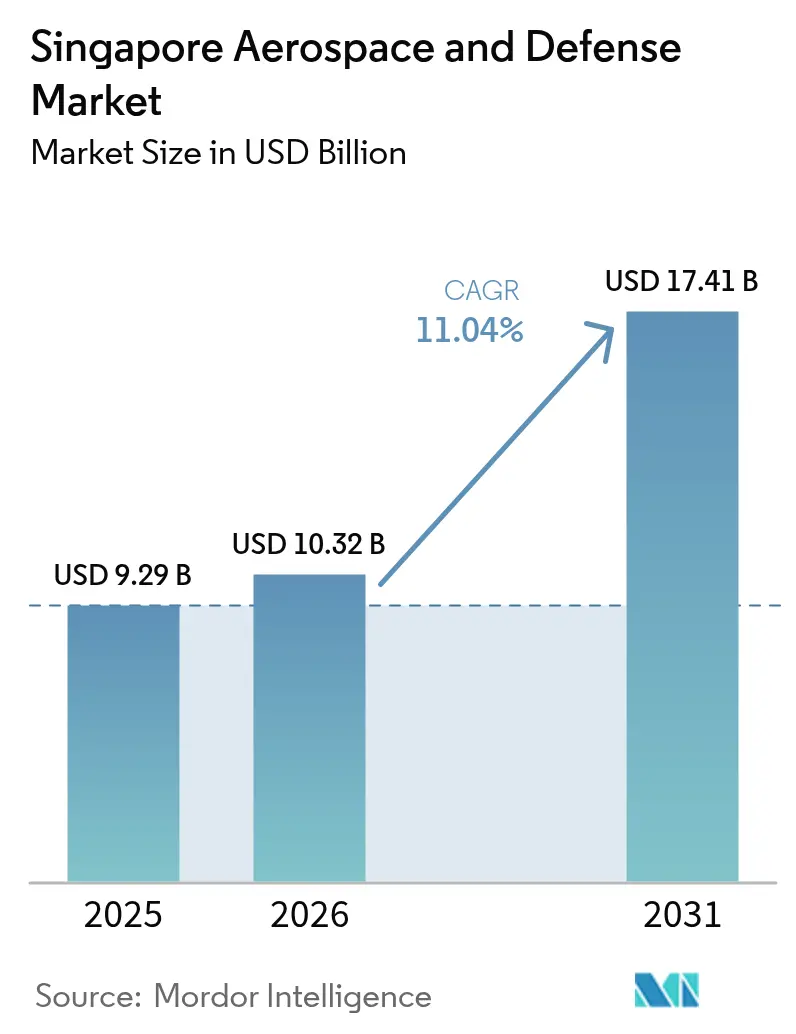

| Base Year Market Size (2025) | USD 9.29 Billion |

| Market Size (2026) | USD 10.32 Billion |

| Market Size (2031) | USD 17.41 Billion |

| Growth Rate (2026 - 2031) | 11.04% CAGR |

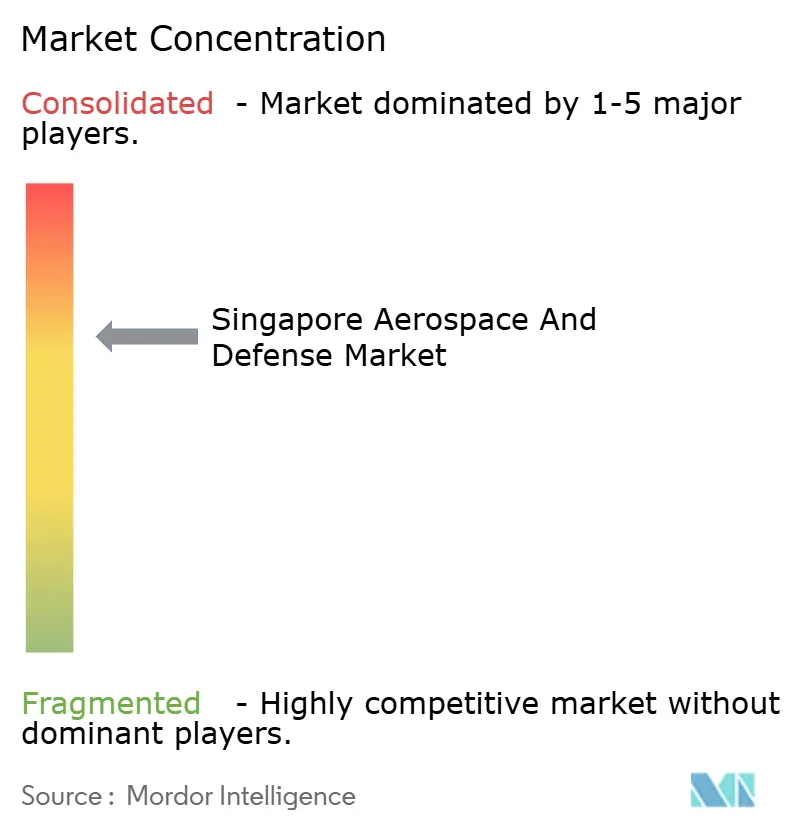

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Aerospace And Defense Market Analysis by Mordor Intelligence

The Singapore aerospace and defense market size is expected to grow from USD 9.29 billion in 2025 to USD 10.32 billion in 2026 and is forecast to reach USD 17.41 billion by 2031 at 11.04% CAGR over 2026-2031. This rapid trajectory rests on three pillars: steady defense‐budget expansion, the full revival of global maintenance-repair-overhaul (MRO) activity, and sustained foreign-direct-investment in advanced manufacturing. Singapore’s FY2025 defense allocation of SGD 23.4 billion anchors multi-year procurement pipelines and signals long-term demand visibility for local contractors.[1]Source: Ministry of Defence Singapore, “Defence Budget 2025,” mindef.gov.sg Parallel recovery in commercial air traffic is restoring MRO shop-visit volumes, while engine-original-equipment-manufacturers’ (OEMs) capacity additions deepen the nation’s supply chain. At the same time, R&D incentives under the “Manufacturing 2030” strategy accelerate the shift toward high-value design, engineering, and space-technology niches.[2]Source: Economic Development Board, “Manufacturing 2030 Incentive Factsheet,” edb.gov.sg

Key Report Takeaways

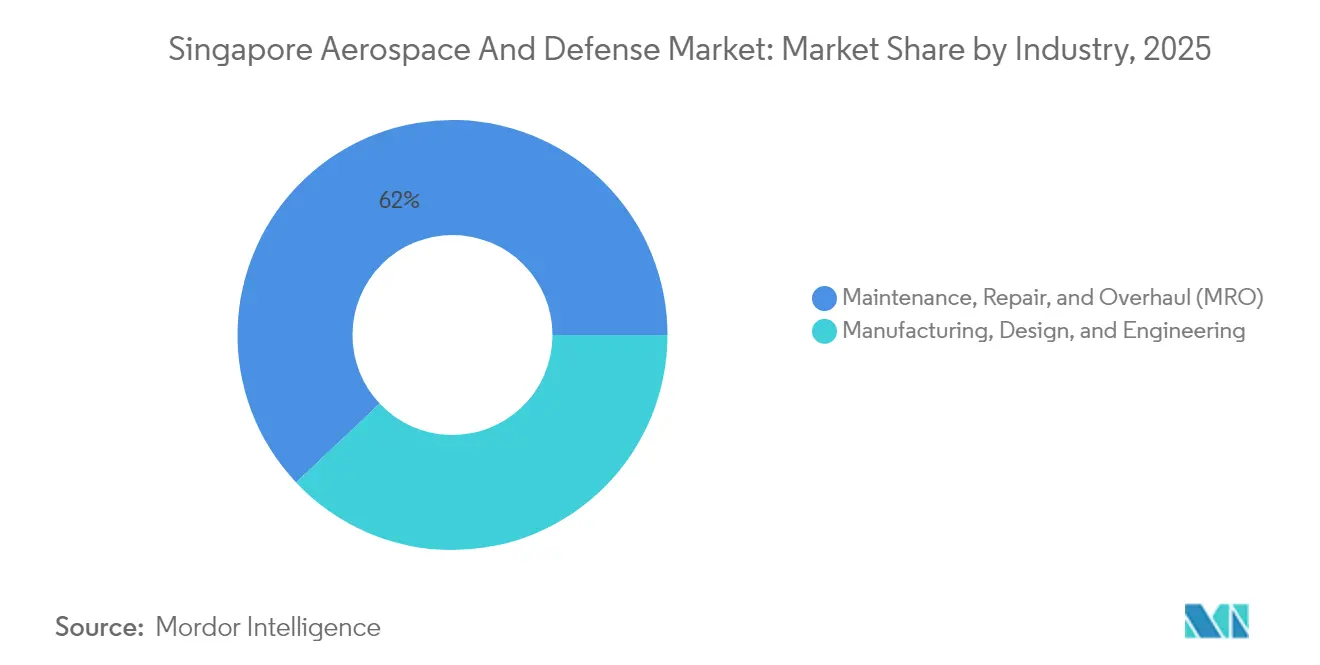

- By industry, MRO commanded 62.03% of the Singapore aerospace and defense market share in 2025, while the manufacturing, design, and engineering segment is projected to grow at a 14.41% CAGR to 2031.

- By type, the aerospace segment held 71.62% of revenue in 2025, while the defense segment recorded the fastest CAGR at 12.18% through 2031.

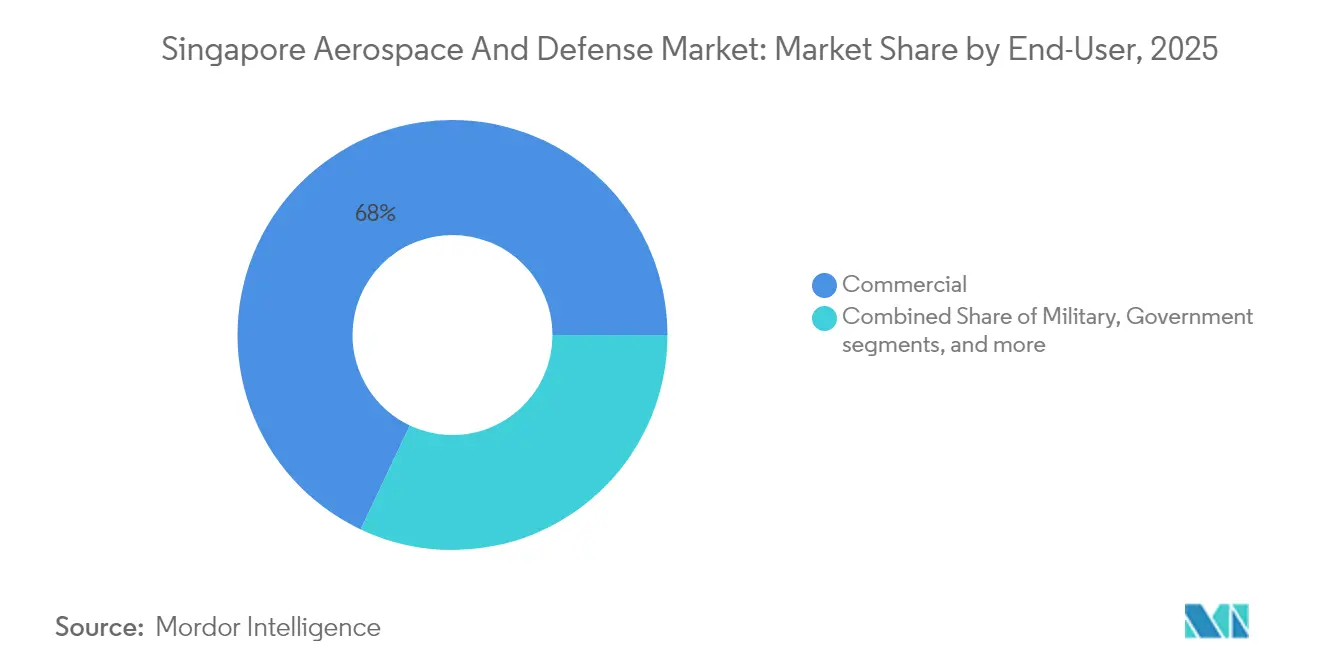

- By end user, commercial aviation captured 67.98% of the Singapore aerospace and defense market size in 2025; the military segment advances at a 12.44% CAGR to 2031.

- By platform, fixed-wing aircraft accounted for 49.12% of activity in 2025, whereas unmanned aerial vehicles led growth at a 15.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Singapore Aerospace And Defense Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust defense-budget growth through 2030 | +2.1% | National, with spillover to ASEAN | Long term (≥ 4 years) |

| Rebound of Singapore’s global-hub MRO business | +1.8% | Global, concentrated in Asia-Pacific | Medium term (2-4 years) |

| Dual-use R&D incentives under “Manufacturing 2030” | +1.3% | National, with technology export potential | Long term (≥ 4 years) |

| Engine-OEM capacity expansions deepening supply chain | +1.6% | Regional Asia-Pacific, global supply integration | Medium term (2-4 years) |

| Government-funded small-satellite and space-tech testbeds | +0.9% | National, with regional space services expansion | Long term (≥ 4 years) |

| SAF “Island-in-a-Box” autonomous training ranges | +0.7% | National, with defense export applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Robust Defense-Budget Growth Through 2030

Annual appropriations of roughly 3% of gross domestic product provide predictable long-cycle funding for fleet upgrades, smart training facilities, and base infrastructure. FY2025’s SGD 23.4 billion (USD 18.09 billion) line-item channels SGD 19.34 billion (USD 15.19 billion) into operations and maintenance, guaranteeing steady workloads for local aerospace-component repair shops. A separate development vote, up 43% since 2022, finances hangar automation and digital range instrumentation, reinforcing order visibility for advanced-manufacturing vendors.

Rebound of Singapore’s Global-Hub MRO Business

Shop-visit volumes have returned to pre-pandemic peaks as Changi Airport passenger flows normalise. SIA Engineering’s long-term services agreements with major carriers illustrate the stability of transaction-based MRO revenues, while workforce restoration to more than 95% of 2019 staffing underpins throughput recovery. Singapore Aero Engine Services’ latest expansion will add 500 skilled positions and bring next-generation engine-module competencies onshore, preserving the city-state’s double-digit share of worldwide MRO billings.[3]Source: Rolls-Royce, “Partners in Progress: Singapore,” rolls-royce.com

Dual-Use R&D Incentives Under “Manufacturing 2030”

Enhanced tax deductions of up to 300% and a refundable investment credit of as high as 50% lower the effective cost of prototyping autonomous systems, additive-manufactured engine parts, and small satellite payloads. The Singapore Aerospace Programme aggregates OEMs, local suppliers, and public research institutes into collaborative testbeds focused on sustainability and advanced-materials breakthroughs. Liquidity support in the form of a cash-conversion option widens participation by small and medium enterprises, accelerating technology diffusion across the ecosystem.

Engine-OEM Capacity Expansions Deepening the Supply Chain

GE Aerospace’s USD 11 million Smart Factory overhaul equips the world’s largest component-repair centre with robotics, advanced metrology, and data-driven process control, handling more than 60% of GE's global engine-repair volume. Rolls-Royce has consolidated the manufacturing of wide-chord fan blades in Singapore, signifying trust in the local talent pool and infrastructure resilience. Pratt & Whitney’s ongoing investment lifts geared-turbofan output by 45% and draws tier-one composites and sheet-metal suppliers into Seletar Aerospace Park.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Land-scarcity and ageing technician base | -1.4% | National, with regional talent competition | Medium term (2-4 years) |

| US-China export-control pressures on avionics and chips | -1.1% | Global, concentrated in high-tech segments | Short term (≤ 2 years) |

| High operating costs versus emerging SE-Asian hubs | -0.8% | Regional Southeast Asia competition | Long term (≥ 4 years) |

| Volatile regional tensions altering procurement timing | -0.6% | Regional Asia-Pacific, defense-specific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Land Scarcity and Ageing Technician Base

The closure of Paya Lebar Air Base by 2030 will release 800 hectares for urban redevelopment but compress aerospace operations into Changi and Tengah zones. New multi-story hangars and automated tool cranes partly offset the spatial squeeze yet raise capital intensity. Meanwhile, demographic shifts mean only 1,700 aerospace graduates enter the workforce yearly against demand for 2,500, prompting early-career outreach and mid-career conversion programmes sponsored by the Association of Aerospace Industries Singapore.

Export-Control Pressures on Avionics and Chips

As a critical node in global semiconductor value chains, Singapore must apply heightened scrutiny to shipments of dual-use items. Enhanced enforcement actions can elongate lead times for advanced avionics and AI-enabled mission computers, potentially delaying platform upgrades. At the same time, relocation of selected US equipment makers to Singapore opens supplier-diversification avenues for local integrators, partially mitigating the near-term drag.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Segment Analysis

The maintenance, repair, and overhaul (MRO) segment controlled 62.03% of the Singapore aerospace and defense market in 2025, reflecting three decades of accumulated know-how and an ecosystem of more than 130 service providers. That heft translates into a resilient baseline of engine-module, landing-gear, and avionics contracts covering 34 airports across eight countries. Segment revenue is reinforced by GE Aerospace’s Smart Factory, now the single-largest GE component-repair site worldwide, and by Singapore Aero Engine Services’ USD 180 million footprint enlargement that inaugurates composite fan-blade restoration capabilities.

Manufacturing, design, and engineering are growing at a 14.41% CAGR through 2031, propelled by Rolls-Royce’s decision to build every wide-chord fan blade outside Britain in Singapore and Pratt & Whitney lifting geared-turbofan component capacity. Additional lift comes from Bombardier’s 290,000-sq-ft service centre upgrade, underscoring the move toward high-value, OEM-branded support solutions. Close coupling between R&D testbeds and industrial lines means additive-manufactured parts validated in A*STAR’s joint labs often transition straight into production, compressing the innovation-to-market cycle.

By Type: Aerospace Leadership Amid Defense Acceleration

The aerospace segment contributed 71.62% of 2025 revenue, underpinned by Changi’s role as an intercontinental transfer hub and by Seletar Aerospace Park’s cluster of more than 70 OEM and tier-one tenants. Government grants worth SGD 210 million (USD 164.94 million) since 2022 support small-satellite payloads, ground-station analytics, and space-situational-awareness services, helping diversify beyond traditional civil aviation.

Defense revenues are expanding at a 12.18% CAGR through 2031 as the Republic of Singapore Air Force inducts 20 F-35 variants and the Navy grows to six Invincible-class submarines. These projects push requirements for composite-aerostructure repair, stealth-coating maintenance, and underwater acoustic systems, allowing MRO specialists to leverage existing civil capabilities for new military workloads.

By End User: Commercial Scale Meets Military Growth

Commercial aviation absorbed 67.98% of the Singapore aerospace and defense market size in 2025, fed by 7,200 weekly flights connecting 170 cities and the build-out of Changi Terminal 5, which will double passenger capacity to 135 million annually. Long-duration MRO agreements, such as SIA Engineering’s decade-long fleet-management pact with its flag-carrier parent, lock in stable shop inputs and underpin capital-investment decisions.

Military end-user demand is set to rise at 12.44% per year as force modernisation plans emphasise stealth aircraft, autonomous surface vessels, and sensor-rich urban training ranges. The SGD 900 million (USD 706.85 million) SAFTI City facility binds 11,000 combat-tracking sensors into instrumented rehearsal spaces, opening export paths for simulation software and live-fire telemetry hardware.

By Platform: Fixed-Wing Foundation Supports UAV Innovation

Fixed-wing aircraft retained 49.12% of 2025 revenue, anchored by wide-body MRO lines and the RSAF’s high-performance fighter fleet. Digital engine-health-management services now accompany most overhaul jobs, allowing predictive part-replacement strategies that raise fleet availability.

Unmanned aerial vehicles form the fastest-growing platform slice at a 15.12% CAGR. Early deployments of autonomous cargo drones at military bases and the port precinct are expanding into urban air mobility (UAM) trials for time-critical logistics. Investments in secure datalinks, detect-and-avoid algorithms, and lightweight composite airframes position Singapore firms to supply both government and private operators across Southeast Asia.

Geography Analysis

Singapore’s 728-square-kilometre landmass sits astride the Strait of Malacca, funnelling one-third of global trade and roughly 40% of Asia-bound airfreight. The nation’s 28 free-trade agreements and first-in-Asia 5G standalone network give aerospace producers near-frictionless market access and industry 4.0 connectivity. Purpose-built zones such as Seletar Aerospace Park integrate airside access, bonded-warehouse clusters, and talent-development centres, housing more than 6,000 professionals in a 320-hectare footprint.

Space constraints drive a hub-and-spoke strategy. High-value R&D and life-limited parts overhauls remain in-country, while labor-intensive airframe checks migrate to lower-cost joint-venture bases in Cambodia, the Philippines, and Vietnam. The model lets Singapore orchestrate regional supply nodes while preserving intellectual property-rich tasks locally. To maintain that edge, the government funds advanced automation retrofits that lift hangar labor productivity by up to 25%, compensating for wage differentials with neighbouring states.

Global neutrality and robust rule of law strengthen Singapore’s first-port-of-call status for multinationals seeking an Asian command centre. Stable bilateral ties with the United States and China give local firms diversified procurement channels. However, compliance with tightened export-control regimes is adding procedural layers for avionics and high-end chipsets. The overall calculus still favours Singapore as an integration and certification node because of its proven adherence to international standards and gold-plated intellectual property protections.

Regulatory Landscape

Singapore’s aerospace and defense activities operate under two related tracks: defense procurement governance and strategic-trade compliance. Defense suppliers contracting with the Ministry of Defence (MINDEF) work within public-sector procurement rules, including open sourcing, invitation-to-quote, and invitation-to-tender methods, alongside supplier registration and security undertakings handled across government. MINDEF’s Industry and Resources Policy Office (IRPO) also shapes defense capability management, technology security, and industry development policy, setting requirements for sensitive programs and sustainment work.

For cross-border movement of controlled hardware, software, and technical data, Singapore Customs administers controls under the Strategic Goods (Control) Act 2002. This is supported by a Strategic Goods Control List aligned to multilateral regimes (Australia Group, MTCR, Nuclear Suppliers Group, and Wassenaar Arrangement), with catch-all provisions covering proliferation-sensitive end uses. For aerospace-specific trade facilitation, the Inland Revenue Authority of Singapore (IRAS) runs the Approved Import GST Suspension Scheme (AISS) for qualifying aerospace players, reducing import-GST cash-flow friction for aircraft parts while requiring compliance with scheme conditions and record transparency.

Value Chain Analysis

Singapore’s value chain is anchored by high-value MRO and advanced manufacturing concentrated at Seletar Aerospace Park, where engine and systems primes and local champions execute OEM-licensed repair, component overhaul, and complex integration. Upstream inputs include aerospace-grade materials, avionics and electronics, and certified parts distributed through bonded logistics and regulated trade lanes, with strategic-goods screening acting as a gating step for dual-use items. Cluster effects are reinforced by multinational commitments such as Safran Electrical & Power’s production and maintenance facility in Seletar Aerospace Park (unveiled in December 2025) and long-horizon capability programs supported by Singapore’s industry agencies.

Midstream work on platform sustainment and modification is led by major local integrators and MRO providers, supported by government-linked capability development and OEM partnerships. Examples include the June 2025 DSTA-Airbus Helicopters agreement to explore crewed-uncrewed teaming using the H225M helicopter and Flexrotor UAS, and the December 2025 ST Engineering-Safran MOU expanding cooperation into defense-focused technology integration and lifecycle support. Downstream, delivery is executed through airline and defense operator contracts, with growing use of digital processes (automation, data-driven inspection, and traceability) to manage turnaround time and labor constraints. Capacity planning is also tied to long-cycle infrastructure such as Changi Airport Terminal 5, alongside its zoning for MRO, logistics, and aftermarket activities.

Competitive Landscape

Market leadership rests with two domestic champions: ST Engineering and SIA Engineering. They straddle OEM-licensed component repair, defense systems integration, and smart-training solutions. Their combined scale attracts engine primes—GE Aerospace, Rolls-Royce, and Pratt & Whitney—each now operating flagship sites within Seletar, which magnetises tier-one composites and sensor suppliers. New entrants concentrate on space-based analytics, additive-manufactured spares, and unmanned systems software, exploiting public-grant windows and the low-latency cloud infrastructure recently adopted by the Defence Science and Technology Agency.

Differentiation hinges on vertical integration and digital maturity. Rolls-Royce’s decision to localise fan-blade production establishes deep-technology moats that are hard to replicate elsewhere in Southeast Asia. In response, ST Engineering is deploying machine-learning-based inspection robots that cut turnaround time on wide-body checks by 20%. Meanwhile, SIA Engineering pilots blockchain-backed parts-traceability, positioning itself for the airworthiness-data economy.

Sustainability themes are rising in tenders. Engine primes commit to 50% recycled-material fan cases, and local researchers are developing power-to-liquid sustainable-aviation-fuel blends. Companies integrating these green credentials early are likely to win upcoming fleet-renewal packages from regional carriers seeking to meet International Civil Aviation Organization emission standards.

Singapore Aerospace And Defense Industry Leaders

SIA Engineering Company Limited

Rolls-Royce plc

RTX Corporation

General Electric Company

Singapore Technologies Engineering Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Time-bound capital commitments and capability programs are creating near-term whitespace across next-generation engine MRO, advanced manufacturing, and digital sustainment services. GE Aerospace’s announced US$300 million investment (2025-2029) to enhance engine repair capabilities in Singapore, RTX’s MOUs committing S$139 million in new investments via Collins Aerospace and Pratt & Whitney, and Bombardier’s June 2026 plan for a new 250,000 sq ft service facility at Seletar Aerospace Park (with construction starting in late 2026) collectively widen the scope for tooling, test equipment, precision machining, NDT, and repair-development services across the local supply base. SPAARC, established by CAAS, EDB, GE Aerospace, and the International Centre for Aviation Innovation, provides a structured pathway for suppliers and research teams to translate aviation and aerospace R&D into deployable capabilities across maintenance and manufacturing workflows.

Sustainability and defense modernization are also opening adjacent demand pockets beyond traditional airframe checks. The 2024 Singapore Sustainable Air Hub Blueprint sets a concrete 2026 SAF uplift target (1%), driving work across feedstock-to-fueling logistics, quality assurance, and aircraft-operational readiness for blended fuels. Separately, the Keppel and Aster agreement (January 2026) to assess a commercial-scale Ethanol-to-Jet SAF plant on Jurong Island points to ongoing industrial development around local SAF supply. On the defense side, MINDEF confirmed in September 2025 that the first of 20 F-35 aircraft is on track for delivery by end-2026, which raises requirements for secure sustainment ecosystems, specialized coatings and materials support, and compliant handling of controlled avionics and software, with Singapore-based MRO and systems firms able to extend civil aviation capabilities into higher-spec military support environments.

Recent Industry Developments

- June 2026: SIA Engineering Company Limited and Safran Aircraft Engines signed a joint venture agreement to establish a CFM LEAP engine MRO facility in Singapore, with Safran holding 51% and SIA Engineering 49%. The move consolidates LEAP quick-turn activity into a dedicated platform and expands Singapore’s role in next-generation engine sustainment work. It also strengthens the local ecosystem for specialized tooling, test capability, and LEAP repair-development support.

- May 2025: Singapore signed a contract with thyssenkrupp Marine Systems for two additional Invincible-class submarines, expanding the Republic of Singapore Navy fleet program to six units. The contract extends long-cycle demand for naval systems integration, maintenance planning, and local supply participation tied to DSTA-managed sustainment. It also reinforces Singapore’s emphasis on sovereign readiness through multi-year platform procurement.

- February 2024: ST Engineering signed agreements with Airbus to support the C295 and with Embraer to support the C-390, covering depot-level maintenance and turnkey solutions from existing facilities in Singapore. These OEM-linked support arrangements deepen Singapore’s military airlift sustainment footprint and raise certification and capability requirements for component repair and heavy maintenance. The partnerships also broaden throughput opportunities by positioning Singapore as a regional support node for C295 fleets.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of aerospace and defense activities carried out in Singapore, including engineering and design work, manufacturing output, and maintenance, repair, and overhaul services tied to aerospace and defense platforms and users.

Scope exclusions: We exclude purely civilian security services, general IT services not tied to defense platforms, and stand-alone airport ground handling that does not relate to aircraft MRO or defense support.

Segmentation Overview

- By Industry

- Manufacturing, Design, and Engineering

- Maintenance, Repair, and Overhaul (MRO)

- By Type

- Aerospace

- Aviation

- Space

- Defense

- Aerospace

- By End User

- Commercial

- Military

- Government (Non-military)

- Private and Business Aviation

- By Platform

- Fixed-Wing Aircraft

- Rotary-Wing Aircraft

- Unmanned Aerial Vehicles (UAVs)

- Land Systems

- Naval Systems

- Missiles and Precision Munitions

- Space Platforms and Launchers

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with public data that helps anchor Singapore activity levels, procurement intent, and industrial output trends. We relied on sources such as Singapore government budget documents and defense statements, Civil Aviation Authority updates, and national trade statistics for relevant aerospace and defense categories.

To keep assumptions grounded, we also reviewed industry association publications and reputable technical journals that discuss MRO capacity, engine shop activity, and fleet servicing patterns. Company annual reports, investor presentations, and major contract announcements were used to understand revenue exposure and timing effects. We then sense-checked key numbers using paid subscriptions for company financials and news, and aircraft and engine fleet databases where applicable. These examples are illustrative rather than exhaustive, and we also referred to other public sources for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on validating what portion of local activity is truly attributable to aerospace and defense value creation in Singapore, and how quickly demand flows through to revenues. We spoke with a mix of ecosystem participants, including MRO and manufacturing executives, procurement and program specialists, and operators and integrators. We then revisited gaps where desk inputs were not consistent with how work is actually planned and delivered.

Because this is a single-country market, outreach centered on Singapore-based decision makers and delivery teams, while still checking regional demand drivers that influence local MRO throughput and defense support work.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 12% | |

| Mid tier: 58% | Functional/Unit leaders: 31% | |

| Smaller Players: 15% | Managers: 57% |

Market-Sizing & Forecasting

The sizing model begins with a top-down reconstruction of Singapore demand and output signals. Defense budget and acquisition plans, installed fleet and servicing intensity, and MRO and manufacturing capacity cues were translated into value pools. We then corroborated those totals with selective bottom-up approximations, such as sampled revenue rollups from local aerospace and defense activity disclosures, channel checks on maintenance throughput, and sanity checks on average value per check and per shop visit. Where these inputs conflicted with macro signals, we adjusted the underlying assumptions.

The inputs that mattered most were aircraft fleet mix and utilization (because it drives shop visits), defense procurement timing and delivery schedules (because it shifts revenue recognition), MRO capacity additions and constraints, and exchange-rate timing for converting local contracts into USD. For forecasting, we used scenario analysis to stress-test base growth against slower fleet recovery, program slippage, or faster modernization cycles. The chosen path was aligned to expert views gathered in interviews. Where company disclosures were incomplete, we filled gaps using peer benchmarks and activity-based ratios, then re-checked those ratios with additional calls before finalizing the totals.

Data Validation & Update Cycle

Validation was done by checking whether modeled revenues align with independent signals, such as defense budget direction, known platform procurement milestones, and Singapore aerospace output and MRO activity indicators. Large variances were flagged, reviewed by another analyst, and then resolved through assumption resets or targeted re-contact with interviewees when the driver could not be explained by timing effects.

Reports are refreshed annually, with interim updates when material shifts occur, such as a major program award, a meaningful change in budgets, or a step-change in MRO capacity. Before delivery, we do a final update pass so clients receive the latest view and late-breaking events are reflected in the market numbers.

Mordor Intelligence's Singapore Aerospace and Defense Market Size Measured Against Other Published Estimates

Published market numbers for Singapore aerospace and defense can look far apart because the underlying scope is not always consistent, and the timing of currency conversion and contract recognition also varies. Differences also show up when one estimate relies more on defense budgets while another relies more on aerospace services output, which can move in different cycles.

The main gap comes from whether defense procurement budgets are treated as market value in the same year, or whether only executed in-country revenues are counted. This is handled explicitly by Mordor Intelligence by tying totals to Singapore-delivered engineering, manufacturing, and MRO activity, while excluding offshore work that is only linked to local buyers.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 10.32 B (2026) | |

| Government Trade Brief A | USD 6.00 B (2024) | Often presented as a sector snapshot with strong emphasis on MRO positioning and a near-term outlook, and it may not fully map engineering, manufacturing, and defense support revenues into one consistent value model. |

| Industry Association Note B | USD 13.20 B (2026) | Can reflect an expanded interpretation that blends defense procurement budgets and adjacent aviation services, and it may apply faster growth assumptions without checking capacity limits and revenue timing. |

Taken together, the spread is mainly explained by scope and timing choices, especially around whether budgets are treated as market value and how aerospace services are bundled. Using clear activity drivers like fleet servicing intensity, program delivery timing, and local execution share helps keep the estimate traceable and repeatable when the model is updated.

Key Questions Answered in the Report

What is the current size of the Singapore aerospace and defense industry market?

The market is valued at USD 10.32 billion in 2026 and is projected to hit USD 17.41 billion by 2031.

Which segment holds the largest share of the market today?

Maintenance, repair and overhaul (MRO) services dominate with 62.03% of 2025 revenue.

What is driving the strong growth outlook for the market?

Three key drivers are a rising defense budget, a full rebound in global MRO demand, and generous “Manufacturing 2030” R&D incentives.

Which platform type is growing the quickest?

Unmanned aerial vehicles (UAVs) are the fastest-expanding platform, logging a 15.12% CAGR through 2031.

What competitive advantage does Rolls-Royce’s fan-blade consolidation confer on Singapore’s wider ecosystem?

Rolls-Royce plc anchors a critical mass of advanced-composite expertise, attracting tier-one material suppliers and giving adjacent MRO shops privileged access to proprietary repair techniques.

How exposed are local integrators to US–China export-control shifts on avionics and semiconductors?

Lead times on high-end mission computers could lengthen, but parallel relocation of US chip-equipment makers to Singapore is creating substitute sourcing channels that soften the blow.

Page last updated on: