Shelf-Life, Stability And Challenge Testing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

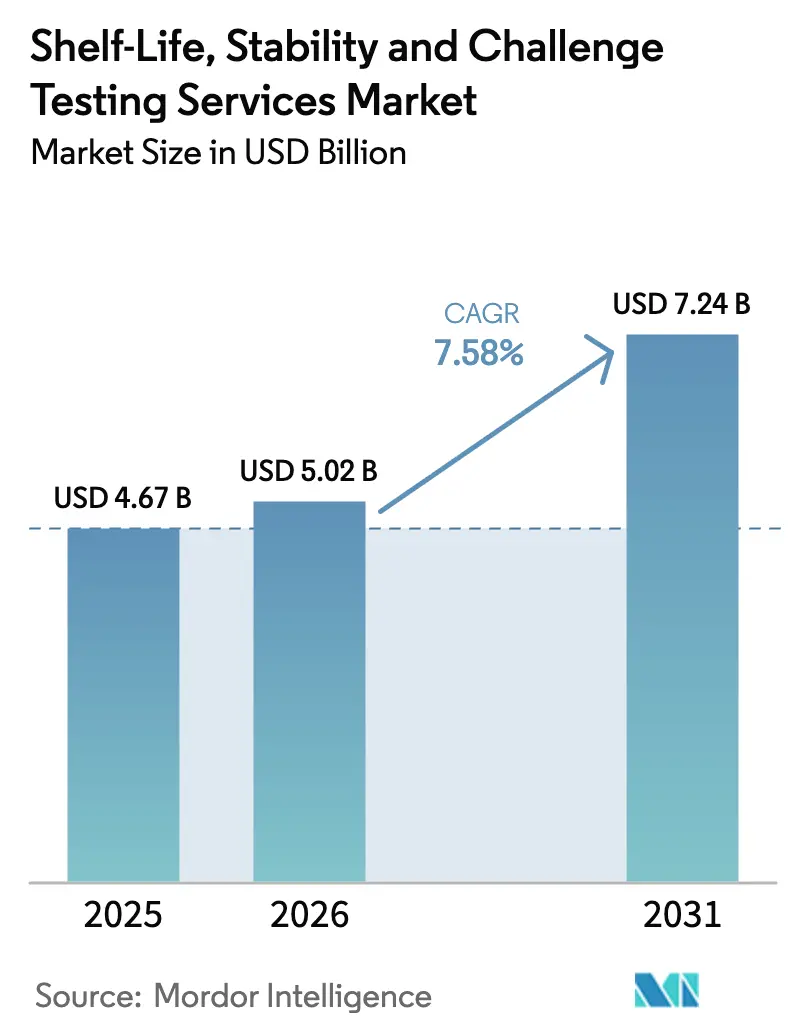

| Market Size (2026) | USD 5.02 Billion |

| Market Size (2031) | USD 7.24 Billion |

| Growth Rate (2026 - 2031) | 7.58% CAGR |

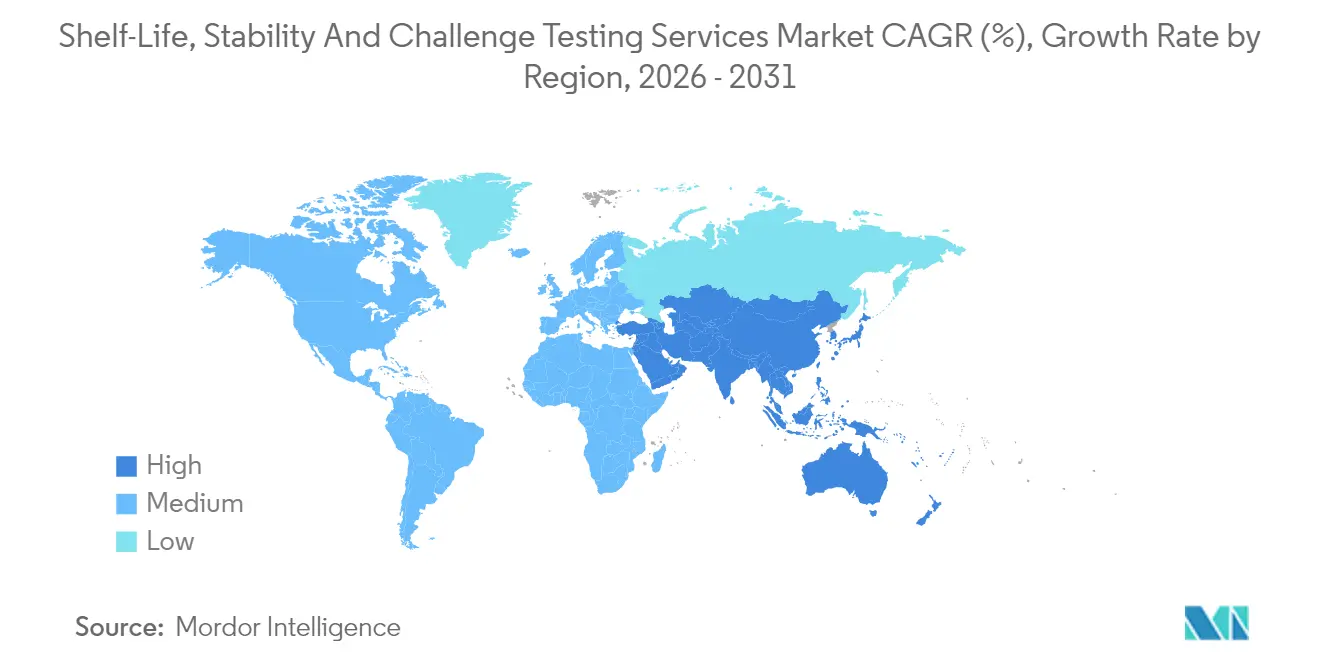

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Shelf-Life, Stability And Challenge Testing Services Market Analysis by Mordor Intelligence

Shelf-life, stability and challenge testing services market size in 2026 is estimated at USD 5.02 billion, growing from 2025 value of USD 4.67 billion with 2031 projections showing USD 7.24 billion, growing at 7.58% CAGR over 2026-2031. Adoption is lifted by unified global stability guidelines, rapid digital transformation in laboratories, and the migration of pharmaceutical and food production to outsourced testing hubs. Real-time studies remain the dominant service because regulators still insist on longitudinal data for high-risk products, whereas predictive and accelerated protocols record the quickest gains as AI platforms shorten project timelines. Microbiological assays anchor the test method mix, yet data-rich analytics and IoT monitoring create new revenue pools for advanced providers. Regionally, North America retains leadership through FDA oversight and strong biologics pipelines, but Asia-Pacific delivers the fastest expansion as manufacturing footprints and harmonized rules broaden the demand base.

Key Report Takeaways

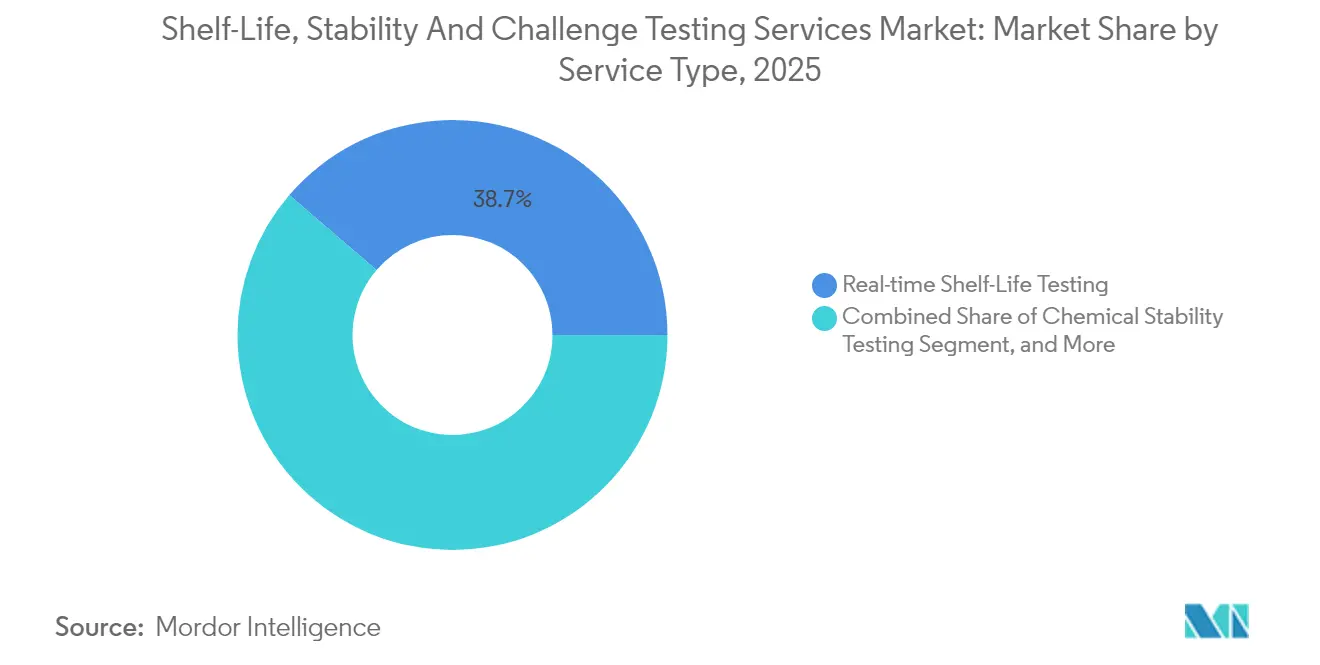

- By service type, real-time shelf-life testing captured 38.72% of the Shelf-life, Stability, and Challenge Testing Services Market share in 2025.

- By testing method, Shelf-life, Stability, and Challenge Testing Services Market size for data modeling and AI analytics is projected to grow at a 9.24% CAGR between 2026–2031.

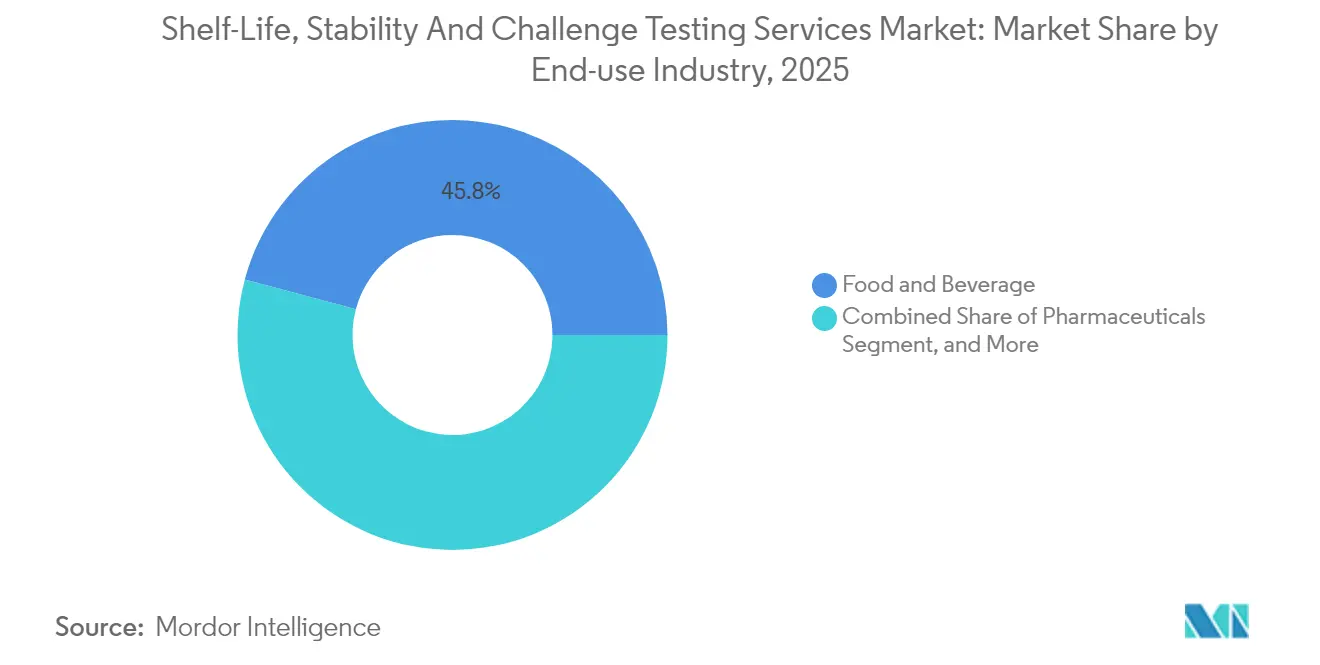

- By end-use industry, food and beverage captured 45.84% of the Shelf-life, Stability, and Challenge Testing Services Market share in 2025.

- By geography, Shelf-life, Stability, and Challenge Testing Services Market size in Asia-Pacific is projected to grow at 9.31% CAGR between 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Shelf-Life, Stability And Challenge Testing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory tightening across food and pharma supply chains | +2.1% | Global, early gains in North America and Europe | Medium term (2-4 years) |

| Proliferation of biologics and cold-chain products | +1.8% | Global, concentrated in North America, Europe and Asia-Pacific | Long term (≥ 4 years) |

| Rise of AI-enabled predictive shelf-life modeling | +1.4% | North America and EU, spill-over to core Asia-Pacific | Short term (≤ 2 years) |

| Growth in e-commerce and globalized distribution networks | +1.2% | Global, early gains in North America and Asia-Pacific | Medium term (2-4 years) |

| Sustainability-driven packaging innovations demanding re-validation | +0.9% | Europe and North America, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Expansion of outsourced testing among SMEs and emerging markets | +0.7% | Asia-Pacific, South America and Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Tightening Across Food and Pharma Supply Chains

Global oversight has intensified since 2025, when ICH issued a revised Q1 stability framework that synchronizes protocols for climatic zones, storage intervals, and data integrity. The updated guideline obliges real-time studies for high-risk formulations and mandates electronic records that withstand audit trails. Complementing this, EFSA has embedded stricter shelf-life validation into its 2025-2030 strategy for novel food ingredients, resulting in increased test volumes across Europe.[1]European Food Safety Authority, “EFSA Strategy 2025-2030,” efsa.europa.eu In the United States, the FDA draft on data fidelity for stability files tightens Part 11 expectations, pushing smaller manufacturers toward external laboratories equipped with validated systems. Collectively, the new requirements lengthen study matrices, increase documentation workloads, and shift demand toward large, accredited providers capable of meeting multiregional compliance requirements.

Proliferation of Biologics and Cold-Chain Products

Biologic drugs, vaccines, and cell therapies expanded production capacity by 23% in 2025, driving unique testing challenges that extend beyond classical small-molecule profiles. Cell-based formulations require continuous monitoring at temperatures ranging from -80 °C to -20 °C and benefit from real-time data logging to anticipate potential excursion risks. Recent ICH Q5C updates introduce special stability brackets for gene therapies, including potency drift metrics under simulated transport. Manufacturers in China, India, and South Korea are advancing these modalities for regional and global markets, triggering a surge in outsourced, cold-chain-ready chambers equipped with redundant power and 21 CFR Part 11 controls. WHO prequalification now references those standards, reinforcing the compliance premium and strengthening the momentum for outsourcing.

Rise of AI-Enabled Predictive Shelf-Life Modeling

Machine-learning engines have become integral to routine stability strategy design. They ingest historical degradation curves, environmental readings, and packaging data to predict the failure point earlier than conventional Arrhenius projections, trimming test durations by up to 40% without eroding statistical confidence. FDA’s Model-Informed Drug Development pilot opened a regulatory on-ramp for algorithm-generated evidence in New Drug Applications, provided firms validate models against real-time data. European regulators followed with similar pilots under EMA’s adaptive pathways. Service providers responded by embedding AI modules into laboratory information management systems, creating hybrid offerings that merge wet-lab analytics with cloud-based predictions. This capability differentiates suppliers and shortens commercialization cycles for complex biologics and functional foods.

Growth in E-Commerce and Globalized Distribution Networks

Online retail exceeded USD 6.2 trillion in 2025, introducing more touchpoints where temperature, vibration, and humidity can erode product integrity. Shippers now request custom stability panels replicating multiple transit modes and last-mile drop-offs. Europe’s Packaging and Packaging Waste Regulation, effective June 2025, obliges verification that sustainable materials preserve function during cross-border journeys. U.S. brands align with similar ESG goals, mandating recyclable or compostable packs that often alter moisture or oxygen ingress rates. These variables increase the volume and complexity of stability dossiers, opening opportunities for laboratories equipped to simulate multi-zone distribution pathways in controlled chambers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and operating costs for advanced analytical labs | -1.3% | Global, acute in emerging markets | Long term (≥ 4 years) |

| Shortage of skilled microbiologists and stability scientists | -1.1% | Global, severe in North America and Europe | Medium term (2-4 years) |

| Data-integrity and cyber-security compliance burdens | -0.8% | Global, stringent in North America and Europe | Short term (≤ 2 years) |

| Limited harmonization of global testing standards | -0.6% | Global, fragmented across regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital and Operating Costs for Advanced Analytical Labs

Qualification of walk-in stability chambers, redundant HVAC systems, validated LIMS, and GMP documentation drives multi-million-dollar expenditures. Operating expenses include twenty-four-hour monitoring, calibration, and periodic re-qualification, which rise with each new regulatory layer. Emerging-market labs face steeper hurdles as access to imported instrumentation and spare parts is restricted by customs duties or supply bottlenecks. Return on investment spans many years, prompting small players to either cap their test scope or exit, while multinational networks spread costs across diverse accounts.

Shortage of Skilled Microbiologists and Stability Scientists

Demand for professionals trained in predictive modeling, aseptic technique, and data integrity surpasses supply across North America and Europe. Universities graduate fewer specialists than laboratory expansions require, and immigration policies tighten candidate pools. The talent gap inflates labor costs, elongates project queues, and limits the speed at which providers can add capacity. Companies woo scarce experts with signing bonuses and flexible schedules, yet turnover remains high, prompting investment in automation and AI to offset shortages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Real-Time Testing Dominates Amid Predictive Growth

The real-time modality accounted for 38.72% of the shelf-life, stability, and challenge testing services market in 2025. It persists because regulators insist on proof across the entire claimed shelf life under the intended storage conditions. However, accelerated and predictive studies are projected to register a 8.78% CAGR through 2031, as AI tools simulate degradation pathways much faster. Providers add hybrid protocols that blend brief high-temperature exposure with algorithmic extrapolation to keep filings on track. Industry adoption expanded in 2025 when the ICH clarified how modeling data could support dosage form changes, thereby reducing the need for duplicative studies. Small and mid-sized enterprises now outsource predictive packages to shave months from product launches. The shelf-life, stability, and challenge testing services market size for predictive workflows is expected to close much of the gap with real-time programs beyond 2028. Consulting add-ons that guide protocol design have transitioned from a niche to a mainstream service, particularly where clients lack in-house regulatory affairs teams.

The regulatory push for sustainable packaging further boosts demand for transport and in-use tests. E-commerce sellers run temperature cycling, vibration, and compression panels to validate corrugated or bio-polymer materials. This dynamic broadens service menus that traditionally focused on pharmaceuticals, making multi-sector laboratories more resilient to cyclical funding. Laboratories that invested early in large-scale climatic chambers and automated sample pull systems report capacity utilization nearing 85%, a level that supports premium pricing. Competitive bids increasingly hinge on turnaround speed rather than basic per-sample rates, cementing the technology advantage for firms with integrated data management and predictive modules.

By Testing Method: Microbiological Methods Lead While AI Analytics Accelerate

Microbiological assays contributed 34.41% of the revenue in 2025, thanks to stringent sterility demands for injectables, ready-to-eat foods, and cosmetics that are prone to fungal contamination. Pathogen challenge tests remain non-negotiable, especially as cold-chain excursions can trigger rapid microbial growth. Nonetheless, data modeling and AI analytics demonstrate a 9.24% CAGR, the fastest among all methodologies. The trend gained momentum after the FDA accepted model-informed submissions that integrate historical laboratory datasets, climatic curves, and spectroscopic fingerprints. As a result, the shelf-life, stability, and challenge testing services market share for analytical software bundles continues to widen, particularly in North America and Western Europe.

Physical and mechanical testing expands in tandem with sustainability programs, since compostable or recycled polymers often shift barrier performance. Chemical profiling is growing steadily on the back of small-molecule generics, while sensor-based IoT monitoring is entering distribution studies, where real-time alerts can intercept quality drift. Providers invest in high-resolution mass spectrometry, automated microbial enumeration, and cloud analytics to differentiate offerings. ISO 17025 accreditation remains a gatekeeper, and audits now assess cybersecurity as closely as assay repeatability, cementing the need for robust IT controls.

By End-use Industry: Food Sector Leadership Challenged by Pharmaceutical Acceleration

Food and beverage maintained 45.84% of the shelf-life, stability, and challenge testing services market size in 2025, driven by global safety rules and brand protection imperatives. However, the pharmaceutical sector is expected to exhibit a 9.62% CAGR through 2031, reflecting surging biologics pipelines, mRNA vaccine programs, and intensifying audits across emerging manufacturing hubs. The growth trajectory is reinforced by digital twins, which allow for tweaking of dose forms without restarting full stability plans. Nutraceuticals also climb as consumers gravitate toward immunity and wellness products, many of which employ plant-based actives sensitive to oxygen and light.

Cosmetics and personal care maintain steady momentum through innovation in preservative-free formulations that demand microbial challenge tests. Chemical and materials players look to shelf-life data to validate biodegradable resins in industrial applications. Cross-sector collaboration increases when packaging changes span multiple product categories, distributing validation budgets across business units. This integrated view positions diversified testing providers to secure enterprise-wide agreements that lock in multi-year revenue streams.

Geography Analysis

North America accounted for 32.21% of global revenue in 2025, driven by entrenched pharmaceutical manufacturing, robust R&D pipelines, and the FDA's enforcement of data integrity. Providers located near major biotech clusters in Massachusetts, California, and Ontario offer rapid turnaround and flexible chamber volumes. Uptake of predictive platforms is particularly high because sponsors seek to compress clinical timelines and secure expedited pathways.

Asia-Pacific posts the fastest 9.31% CAGR due to production migration and regulatory convergence. China’s continued 23% escalation in biologics capacity in 2025 demanded sophisticated stability regimens under NMPA guidance. [2]Nature Biotechnology, “Biologics Manufacturing Capacity Expansion,” nature.com India leverages a robust generics industry and cost-effective talent to attract outsourced dossiers aimed at the FDA and EMA markets. Japan and South Korea, both advanced biologics innovators, require ultra-cold studies backed by granular documentation, which boosts demand for local ISO 17025 labs equipped with redundancy against seismic risk. Europe maintains significant scale through the European Union’s Packaging and Packaging Waste Regulation and EFSA oversight. Germany and France lead the adoption of AI-enhanced protocols, and the United Kingdom’s post-Brexit alignment creates parallel filings that double certain study sets. Elsewhere, South America and the Middle East and Africa register mid-single-digit CAGR as multinationals extend supply chains into growth markets and must qualify zone-specific transport conditions.

Competitive Landscape

Eurofins Scientific, SGS, Intertek, ALS Limited, and Bureau Veritas collectively hold approximately 35-40% of the industry's revenue. Their scale supports investment in robotic sample handling, blockchain audit trails, and predictive analytics suites. Consolidation intensified when SGS and Bureau Veritas entered merger talks valued at nearly EUR 32-33 billion (USD 34.2-35.3 billion), a move that would forge the largest lab network with a 140-country reach.[3]Reuters, “SGS and Bureau Veritas Merger Discussions,” reuters.com Such a scale promises volume leverage on consumables and easier compliance with diverging cybersecurity mandates.

Mid-tier specialists focus on high-margin niches, such as live-biotherapeutic products or reusable bioreactors. They compete by offering customized protocols, rapid onboarding, and consultative guidance through complex regulatory submissions. Talent scarcity remains a bottleneck; many firms sponsor academic programs and offer apprenticeships to attract and retain fresh graduates.

Price competition centers on bundled solutions rather than per-assay tariffs. Clients favor suppliers who can cover stability, packaging validation, and regulatory dossier preparation under a single contract. This one-stop approach lowers project management overhead and aligns accountability. Consequently, laboratories lacking end-to-end capabilities risk relegation to overflow work. Market entry barriers climb as regulators heighten cyber-security scrutiny, further advantaging incumbents with mature IT governance frameworks.

Shelf-Life, Stability And Challenge Testing Services Industry Leaders

Eurofins Scientific SE

SGS SA

Intertek Group plc

ALS Limited

Bureau Veritas SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: SGS and Bureau Veritas advanced merger discussions valued at EUR 32-33 billion (USD 34.2-35.3 billion), aiming to create a global testing leader.

- September 2025: Eurofins Scientific completed EUR 180 million (USD 192.6 million) expansion adding 12 stability laboratories across North America and Asia-Pacific.

- August 2025: Charles River Laboratories introduced an integrated stability testing platform that merges real-time monitoring with predictive analytics to cut study timelines by up to 35%.

- July 2025: The International Council for Harmonisation issued a comprehensive revision to ICH Q1 that formalized AI-based evidence and stricter data integrity clauses.

Global Shelf-Life, Stability And Challenge Testing Services Market Report Scope

| Real-time Shelf-Life Testing |

| Accelerated/Predictive Shelf-Life Testing |

| Microbial Challenge Testing |

| Chemical Stability Testing |

| Physical and Packaging Integrity Testing |

| In-use and Transport Stability Studies |

| Consulting and Modelling Services |

| Microbiological Methods |

| Chemical/Analytical Methods |

| Physical/Mechanical Methods |

| Sensor and IoT-Based Monitoring |

| Data Modelling and AI Predictive Analytics |

| Food and Beverage |

| Pharmaceuticals |

| Cosmetics and Personal Care |

| Nutraceuticals and Functional Ingredients |

| Other End-use Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Real-time Shelf-Life Testing | ||

| Accelerated/Predictive Shelf-Life Testing | |||

| Microbial Challenge Testing | |||

| Chemical Stability Testing | |||

| Physical and Packaging Integrity Testing | |||

| In-use and Transport Stability Studies | |||

| Consulting and Modelling Services | |||

| By Testing Method | Microbiological Methods | ||

| Chemical/Analytical Methods | |||

| Physical/Mechanical Methods | |||

| Sensor and IoT-Based Monitoring | |||

| Data Modelling and AI Predictive Analytics | |||

| By End-use Industry | Food and Beverage | ||

| Pharmaceuticals | |||

| Cosmetics and Personal Care | |||

| Nutraceuticals and Functional Ingredients | |||

| Other End-use Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the shelf-life, stability and challenge testing services market?

It reached USD 5.02 billion in 2026.

What is the market's expected growth rate by 2031?

The forecast CAGR is 7.58%.

Which service segment is expanding the quickest?

Accelerated and predictive shelf-life testing is advancing at a 8.78% CAGR.

Which region is posting the highest growth rate?

Asia-Pacific is projected to rise at a 9.31% CAGR.

Who are the leading companies considering a merger?

SGS and Bureau Veritas are in negotiations for a potential combination worth up to USD 35.3 billion.

Which end-use sector will likely outpace others?

Pharmaceuticals are projected to register a 9.62% CAGR to 2031.

Page last updated on: