Senior Living Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

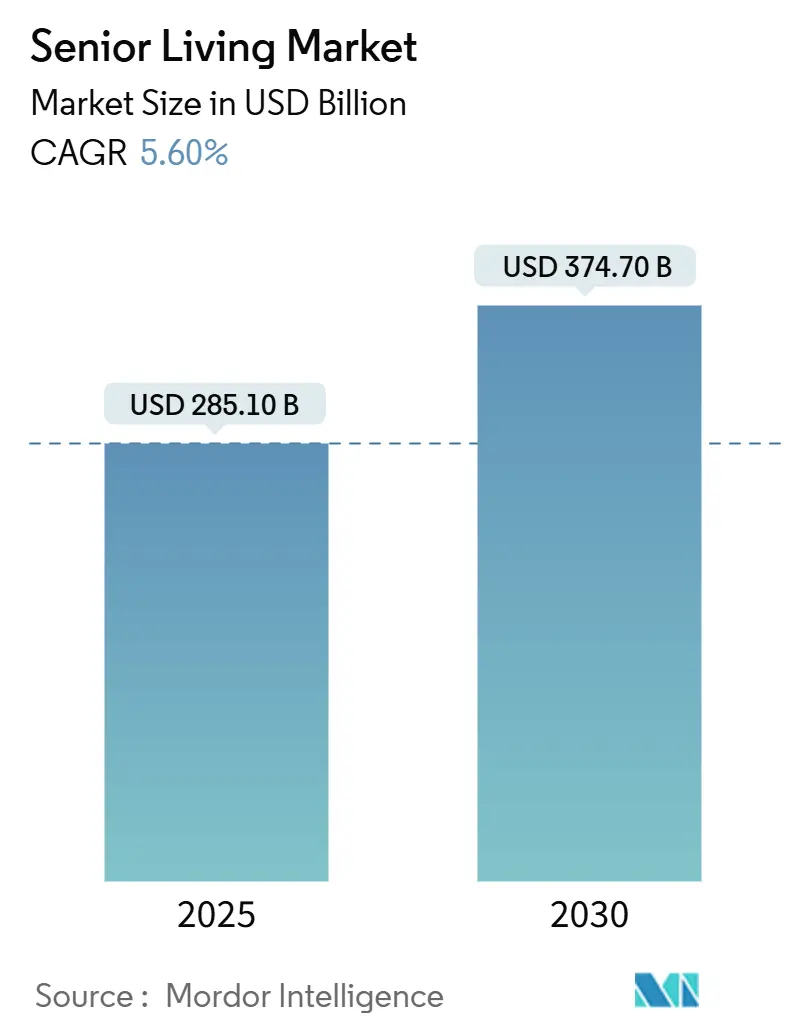

| Market Size (2025) | USD 285.10 Billion |

| Market Size (2030) | USD 374.70 Billion |

| Growth Rate (2025 - 2030) | 5.60% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

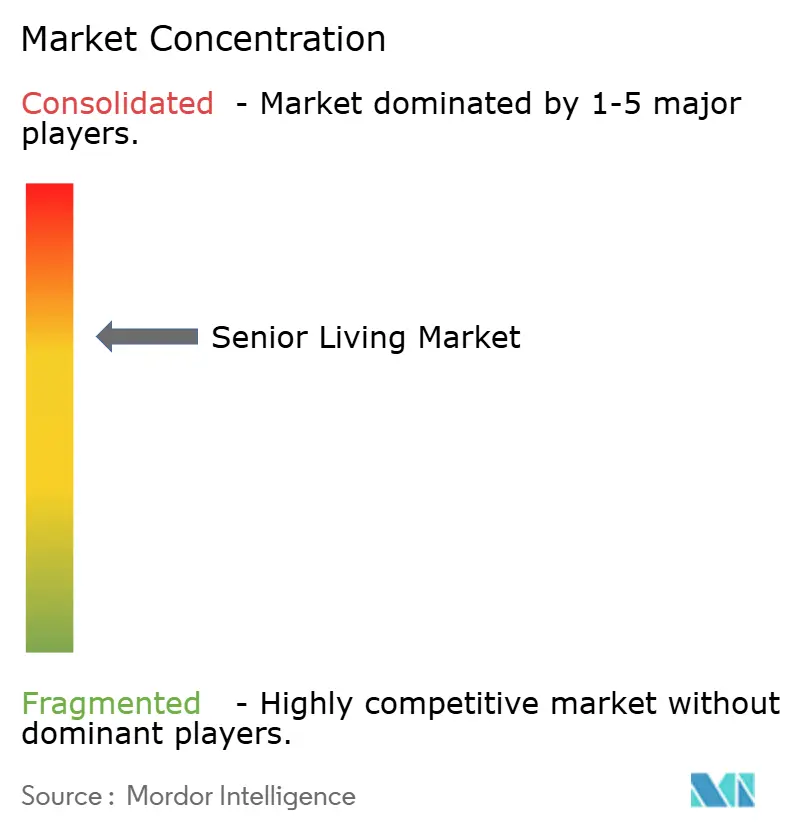

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Senior Living Market Analysis by Mordor Intelligence

The Senior Living Market size is estimated at USD 285.10 billion in 2025, and is expected to reach USD 374.70 billion by 2030, at a CAGR of 5.60% during the forecast period (2025-2030).

Accelerating demand stems from the global population of 80-plus individuals rising by roughly 500,000 people each year, prompting developers to add purpose-built communities despite the capital-intensive construction costs. Institutional investors now direct more than USD 2 billion annually into the senior housing market, drawn by stable yields and inflation-hedging rent escalators. On the supply side, groundbreakings fell to only 1,287 units in Q1 2025, the lowest quarterly total on record, which lifted RevPAR by 4.9% across prime metros. Operators gain further pricing leverage by integrating predictive analytics platforms that lower avoidable hospitalizations and enhance resident outcomes.

Key Report Takeaways

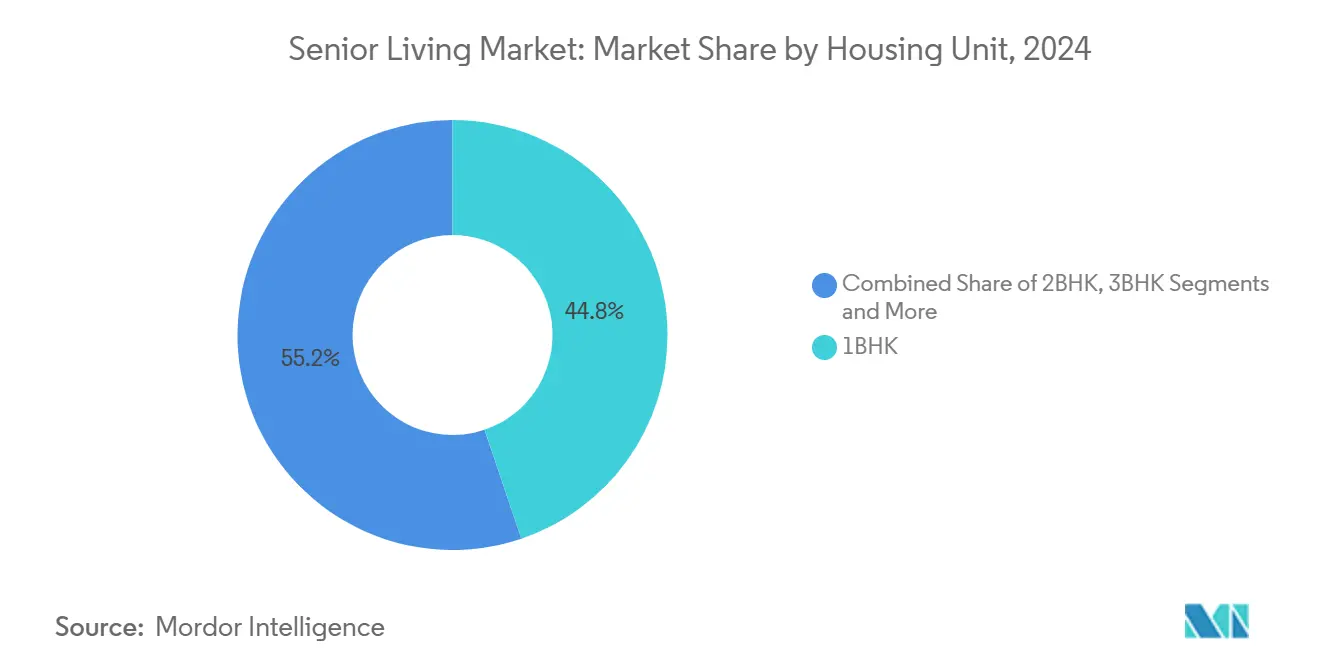

- By housing unit configuration, 1BHK apartments captured 44.8% of the senior housing market size in 2024; Independent Villas are poised to grow at a 9.2% CAGR to 2030.

- By level of care, Lifestyle/Minimal Assistance residences represented 41.6% of 2024 revenue, while Memory Care is advancing at a 10.7% CAGR.

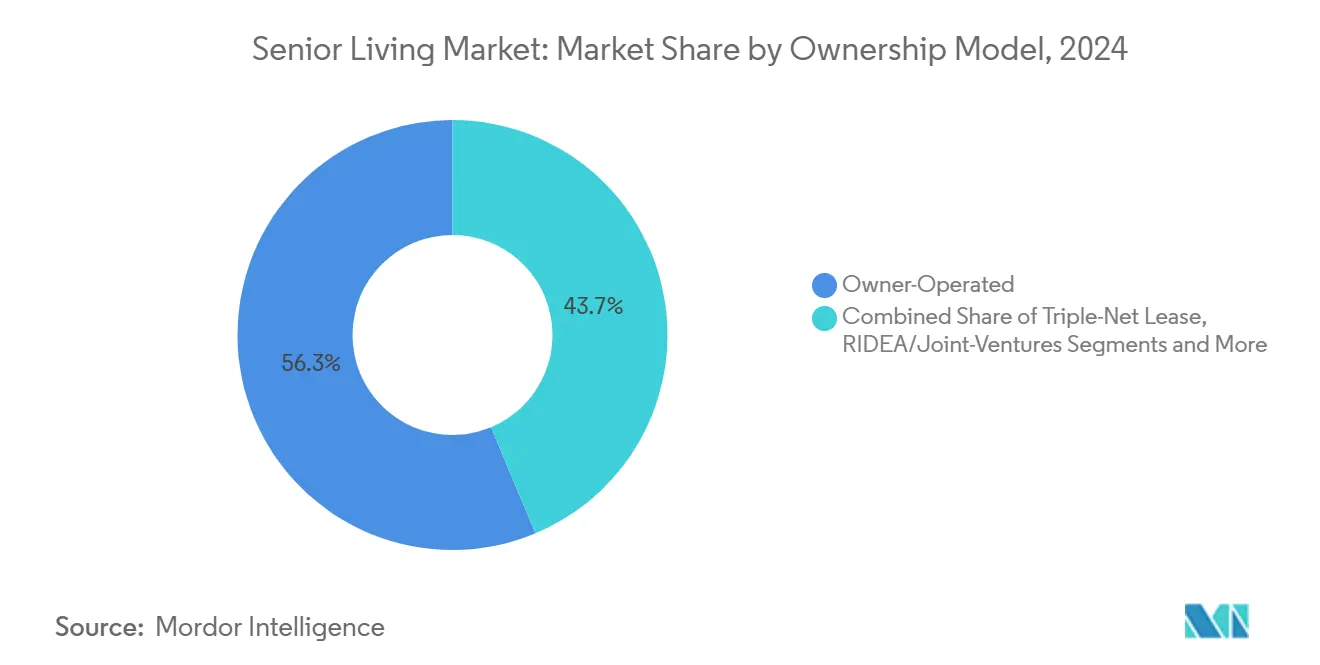

- By ownership model, Owner-Operated facilities controlled 56.3% of 2024 inventory; RIDEA/Joint-Ventures exhibit a 9.1% CAGR to 2030.

- By funding, Private Pay residents accounted for 72.8% of spend in 2024, yet Long-Term Care Insurance premiums are scaling at a 10.8% CAGR.

- By geography, North America led with 37.9% of senior housing market share in 2024, whereas Asia Pacific is projected to log the fastest 8.6% CAGR through 2030.

Global Senior Living Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population expansion | +1.80% | Global; highest in North America & Europe | Long term (≥ 4 years) |

| Rising prevalence of dementia & comorbidities | +1.20% | Global; strongest in developed markets | Medium term (2-4 years) |

| Institutional capital inflow to alternative assets | +0.90% | North America & Europe; emerging in Asia Pacific | Short term (≤ 2 years) |

| Longevity technology ecosystem partnerships | +0.70% | Core markets in North America & Asia Pacific | Medium term (2-4 years) |

| Climate-resilient, wellness-certified community design | +0.40% | North America & Europe, especially climate-exposed regions | Long term (≥ 4 years) |

| Reverse-mortgage and equity-release uptake | +0.30% | North America; spreading to Australia & United Kingdom | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Population Expansion

Demographic momentum anchors the senior housing market. Baby boomers collectively hold nearly USD 14 trillion in home equity, capital that can be unlocked via reverse-mortgage offerings such as PHH Mortgage’s EquityIQ, which now extends loans up to USD 4 million. Premium communities channel this wealth into bundled hospitality and care services that command higher margins. China’s policy planners anticipate seniors will constitute 30% of the population by 2035, underpinning a USD 4.1 trillion opportunity that is already attracting foreign operators.[1]Asia Bureau, “China’s Silver Economy,” Nikkei Asia, nikkei.com Wealth concentration also intensifies a supply gap at the affordable end, where land costs and regulatory hurdles curtail new stock.

Rising Prevalence of Dementia & Comorbidities

Memory Care, growing 10.7% annually, benefits from state regulations that enforce staff-training standards and secure layouts. Facilities now incorporate biophilic design and music-therapy spaces to slow cognitive decline. AI motion sensors alert staff to fall risk, lowering liability and extending the average length of stay. Higher acuity embeds premium daily rates that lift overall senior housing market size while raising barriers against operators unable to meet compliance thresholds.

Institutional Capital Inflow to Alternative Assets

Family offices and private-equity funds view senior housing market cash flows as defensive during periods of macroeconomic volatility. Morgan Stanley’s purchase of eight Brightview campuses illustrates institutional appetite for large, stabilized portfolios. Development yields remain 200-300 basis points above stabilized capitalization rates, spurring new builds in supply-constrained metropolitan areas. The RIDEA model aligns real-estate owners with operating partners, allowing both to share upside and accelerating a 9.1% CAGR for RIDEA-structured assets.[2]Press Center, “Brightview Portfolio Acquisition,” Morgan Stanley, morganstanley.com

Longevity Technology Ecosystem Partnerships

Tech convergence is reshaping competitive strategy. CarePredict’s AI wearables track subtle changes in gait or sleep days before clinical episodes, reducing hospital transfers and supporting risk-sharing contracts with Medicare Advantage plans. Operators bundle telepharmacy, remote vital monitoring, and virtual behavioral therapy to enhance resident satisfaction while diversifying revenue. Data-driven staffing algorithms, meanwhile, mitigate workforce shortages and lift profit margins.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-labor shortages & wage inflation | -1.40% | Global; most acute in North America | Short term (≤ 2 years) |

| Complex, fragmented regulatory compliance | -0.80% | North America & Europe | Medium term (2-4 years) |

| Escalating property-insurance premiums in climate zones | -0.60% | U.S. Gulf Coast; Australia | Short term (≤ 2 years) |

| Community opposition & restrictive zoning (“NIMBY”) | -0.40% | Suburban North America; select EU cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled-Labor Shortages & Wage Inflation

Ninety-nine percent of U.S. skilled nursing providers report unfilled clinical positions, driving an increased reliance on agency staff and elevating wage bills. Compensation for certified nursing assistants has outpaced cost-of-living adjustments since 2024. Operators respond with scholarship, mentorship, and career-ladder programs that improve retention, supplemented by AI scheduling tools that stretch limited headcount across multiple care wings.

Complex, Fragmented Regulatory Compliance

Licensing statutes differ markedly by state and country, forcing operators to adapt building codes, staffing ratios, and admission protocols. While compliance raises cost structures, it also protects incumbents that amortize legal overhead across large portfolios. Digital platforms now auto-track policy updates and incident reporting, lowering administrative burden and curbing citation risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Housing Unit: Independent Villas Accelerate Upscale Demand

Independent Villas underpin a 9.2% CAGR, capitalizing on retirees’ desire for privacy inside gated, amenity-rich campuses. Developers incorporate smart-home systems and voice-activated controls that facilitate aging in place. Although Villas carry higher build costs, premium rents and ancillary technology fees drive superior margins. This mix strengthens the senior housing market by attracting residents earlier in the aging curve and retaining them through progressive care tiers.

1BHK suites retain 44.8% of the senior housing market share due to cost efficiency and standardized construction templates. Two-bedroom units satisfy couples and serve as flexible layouts for visiting family, helping reduce churn. Three-bedroom options remain limited but meet multi-generational demand in parts of the Asia Pacific.

By Level of Care Intensity: Memory Care Commands Premium Growth

Lifestyle/Minimal Assistance residences generated 41.6% of 2024 revenue by servicing healthier seniors who seek maintenance-free living and social programming. However, Memory Care advances at 10.7% per year as dementia prevalence climbs. Secure wings utilize circadian lighting, therapeutic gardens, and smaller resident “households,” resulting in measurable declines in behavioral episodes. Operators price these specialized services at a premium, thereby increasing the segment's contribution to the overall senior housing market size.

Activities of Daily Living support functions as a transitional layer where residents move from independent status toward higher acuity. Skilled Nursing and Rehabilitation continues to serve complex clinical needs, often subsidized by Medicare or equivalent payors, but faces cap-rate compression and increasing compliance costs.

By Ownership Model: RIDEA Partnerships Gain Traction

Owner-Operators still manage 56.3% of inventory, but the RIDEA/Joint Venture pathway is scaling fastest, as REITs such as Welltower co-participate in NOI gains. These structures unlock cheaper capital for modernization and tech upgrades. Triple-Net leases remain popular for investors seeking stable income, though they forgo upside from operational efficiencies. Condominium or resident-owned models flourish in Nordic markets, offering seniors deeded ownership and governance rights.

By Funding Source: Insurance-Backed Residents Expand

Private Pay still dominates at 72.8%, yet hybrid long-term-care policies are growing 10.8% annually, broadening access for middle-income households. Insurers pre-package stay durations and acuity upgrades, smoothing cash flow for operators. Government-subsidized beds remain vital in Europe and Asia, tying reimbursement to quality-of-life scores and energy-efficiency metrics. Medicaid and Medicare funding underpins U.S. post-acute stays but demands rigorous documentation that smaller providers struggle to maintain.

Geography Analysis

North America generated 37.9% of 2024 revenue, anchored by the United States’ deep private-pay market and Canada’s expanding REIT footprint. Welltower’s CAD 4.6 billion (USD 3.4 billion) acquisition of Amica Senior Living highlights continued consolidation in premium Canadian metros. Climate-driven insurance spikes—Florida premiums climbed 125% in five years—force older properties to retrofit roofs and window systems, pushing some operators to exit hazard-prone zones. Mexico’s coastal enclaves offer U.S. retirees lower living costs and medical tourism arrangements, prompting experimental cross-border partnerships.

The Asia Pacific region records the fastest 8.6% CAGR, led by China’s deregulation of foreign ownership restrictions and the implementation of large-scale eldercare subsidies. South Korea’s luxury condo towers capture affluent seniors who demand wellness spas, rooftop gardens, and concierge medicine.[3]Features Desk, “Luxury Retirement Towers in Korea,” The Japan Times, japantimes.co.jp Australia benefits from strong superannuation inflows that bankroll state-of-the-art campuses in Sydney and Melbourne, frequently co-located with acute-care hospitals for continuum-of-care advantages.

Europe posts steady growth as private operators supplement robust public safety nets. Germany leads development volume; the United Kingdom draws foreign capital despite Brexit-related regulatory shifts. Southern Europe offers a latent opportunity, buoyed by improving macro conditions and government incentives for age-friendly infrastructure. EU taxonomy rules favor green-certified assets, prompting widespread retrofits and photovoltaic installations that cut operating costs and align with residents’ wellness priorities.

Competitive Landscape

The senior housing market remains fragmented, with no single operator controlling more than 5% of the occupied inventory, creating abundant room for consolidation. Brookdale Senior Living expanded its footprint by purchasing 41 formerly leased communities for USD 610 million, enhancing control over capital expenditures. Atria and Sunrise expand through management contracts with mixed-use developers seeking experiential retail anchors. Technology adoption separates leaders: 12 Oaks Senior Living transitioned to a value-based reimbursement model by standardizing electronic health records across its portfolio. Environmental resilience is another differentiator; operators with hurricane-rated windows and redundant power systems negotiate better insurance terms.

Healthcare systems are entering the senior housing market to capture post-acute revenue and manage readmission penalties. Hospitality brands are piloting membership clubs that let older adults reserve stays at multiple campuses worldwide. International investors, particularly those from Singapore and Japan, are introducing robotics-assisted care models that enhance staffing flexibility. As the roll-up thesis matures, synergies center on centralized procurement, cross-campus staffing pools, and unified marketing platforms.

Senior Living Industry Leaders

Brookdale Senior Living

Atria Senior Living

Ventas Inc.

Korian

Paranjape Athashri

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Jonathan Rose Companies acquired a Southern California community for USD 83 million, expanding its green-building portfolio.

- April 2025: Welltower completed USD 2.8 billion of acquisitions, including 38 ultra-luxury properties across Canada.

- April 2025: PHH Mortgage introduced EquityIQ, a reverse mortgage product targeting homeowners aged 55 and older.

- March 2025: Spring Arbor merged with Allegro, creating a 53-community platform in the U.S. Southeast.

Global Senior Living Market Report Scope

| 1BHK |

| 2BHK |

| 3BHK |

| Independent Villas |

| Lifestyle / Minimal Assistance |

| Activities-of-Daily-Living (ADL) Support |

| Specialized Memory Care |

| Skilled Nursing & Rehabilitation |

| Owner-Operated |

| Triple-Net Lease |

| RIDEA / Joint-Ventures |

| Condominium / Resident-Owned |

| Private Pay |

| Public Subsidized |

| Long-Term Care Insurance |

| Medicaid / Medicare |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa |

| By Housing Unit | 1BHK | |

| 2BHK | ||

| 3BHK | ||

| Independent Villas | ||

| By Level of Care Intensity | Lifestyle / Minimal Assistance | |

| Activities-of-Daily-Living (ADL) Support | ||

| Specialized Memory Care | ||

| Skilled Nursing & Rehabilitation | ||

| By Ownership Model | Owner-Operated | |

| Triple-Net Lease | ||

| RIDEA / Joint-Ventures | ||

| Condominium / Resident-Owned | ||

| By Funding Source | Private Pay | |

| Public Subsidized | ||

| Long-Term Care Insurance | ||

| Medicaid / Medicare | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the forecast growth of the senior housing market?

The market is projected to rise from USD 285.1 billion in 2025 to USD 374.7 billion by 2030, reflecting a 5.6% CAGR.

Which region grows fastest in senior housing?

Asia Pacific leads with an anticipated 8.6% CAGR through 2030, supported by Chinese policy shifts and rising wealth in South Korea and Australia.

Why are Independent Villas important?

They grow at a 9.2% CAGR by offering privacy, smart-home technology, and concierge services that appeal to affluent retirees.

How severe is the labor shortage?

Nearly all North American operators report vacancies, driving wage inflation and pushing operators to invest in AI scheduling and retention incentives.

What funding models are emerging?

Hybrid long-term-care insurance policies are expanding at 10.8% annually, supplementing the private-pay dominant revenue mix.

How fragmented is the competitive landscape?

No single operator controls more than 5% of capacity, creating opportunities for roll-ups and operational efficiency gains across the sector.

Page last updated on: