Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

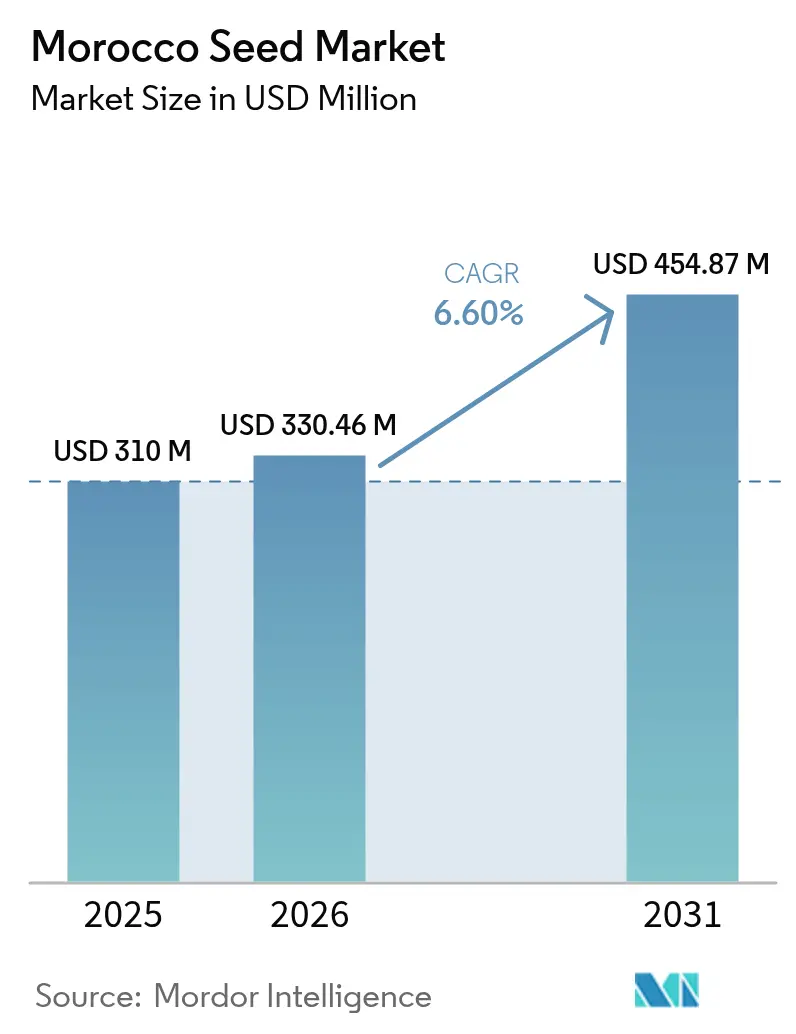

| Base Year Market Size (2025) | USD 310 Million |

| Market Size (2026) | USD 330.46 Million |

| Market Size (2031) | USD 454.87 Million |

| Growth Rate (2026 - 2031) | 6.60% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Morocco Seed Market Analysis by Mordor Intelligence

The Morocco seed market size was valued at USD 310 million in 2025 and estimated to grow from USD 330.46 million in 2026 to reach USD 454.87 million by 2031, at a CAGR of 6.6% during the forecast period (2026-2031). State subsidies for certified seeds, expanding export horticulture, and rising demand for hybrid feed grains help maintain steady momentum, even in a climate marked by erratic rainfall. Premium vegetable hybrids for Europe-bound tomatoes and peppers, drought-tolerant wheat lines, and high-yield maize all contribute to a rapid shift away from farm-saved seed. Larger growers in the Souss-Massa and Gharb plains are adopting disease-resistant and climate-resilient genetics to meet stringent European residue standards, while poultry integrators near Casablanca prioritize hybrid cereals that improve feed conversion ratios. Digital agri-markets, localized seed-coating research, and a USD 250 million climate-smart agriculture program, financed by the World Bank, provide further structural support. Together, these dynamics reinforce the growth path of the Morocco seed market despite short-term acreage swings linked to drought.

Key Report Takeaways

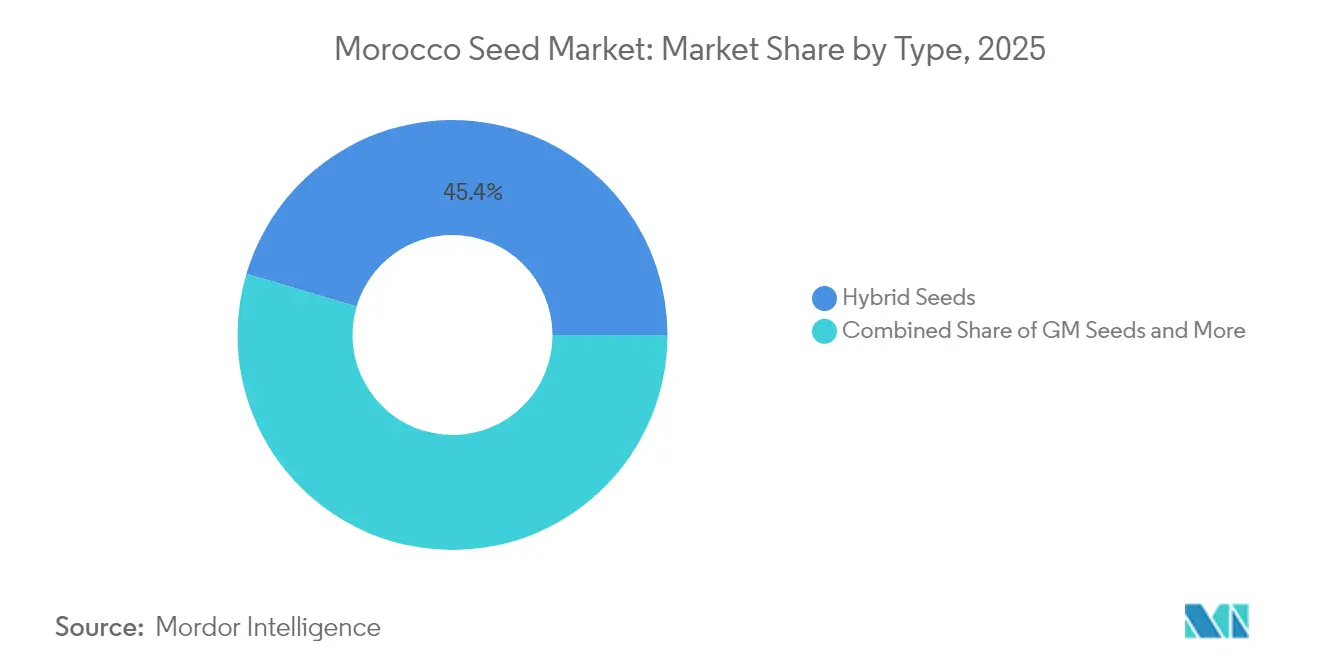

- By type, hybrid seeds captured 45.40% share of the Morocco seed market size in 2025, while GM seeds recorded the fastest 10.9% CAGR through 2031.

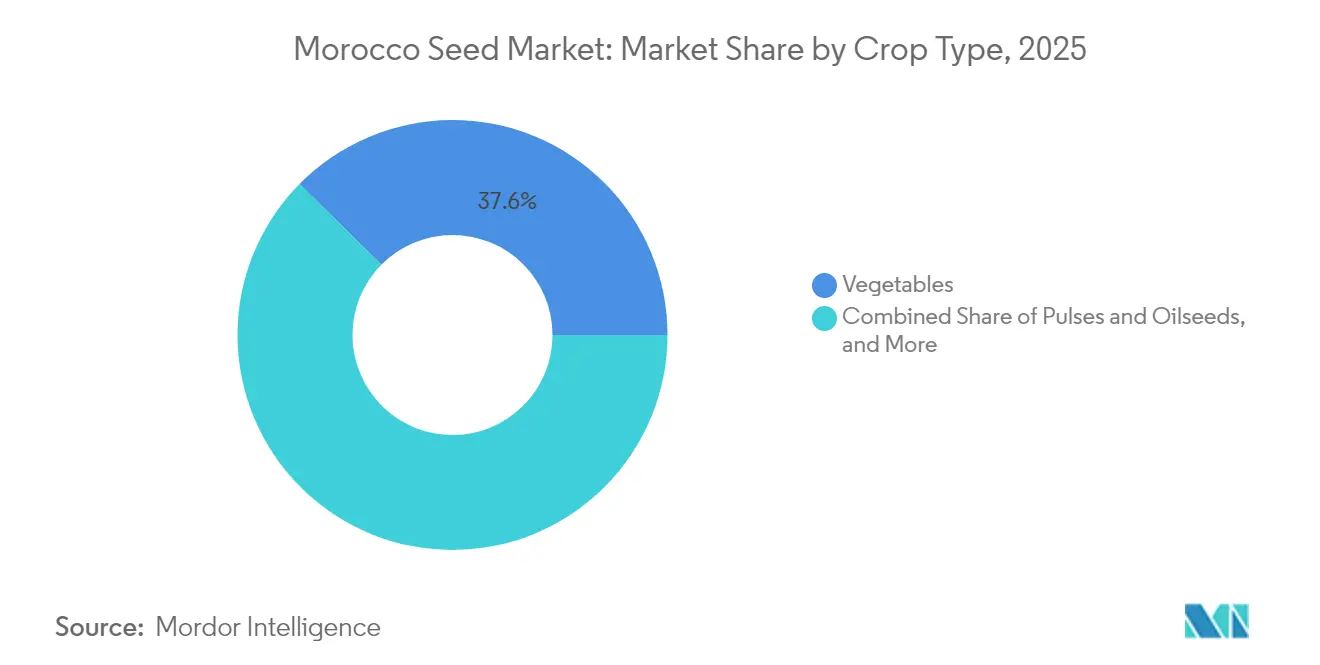

- By crop type, vegetables led the Morocco seed market with a 37.60% share in 2025, whereas pulses and oilseeds are projected to advance at a 9.3% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Morocco Seed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government subsidies for certified seeds | +1.2% | Gharb, Saïss, and Doukkala plains | Short term (≤ 2 years) |

| Rising demand for high-yield hybrid cereals | +1.5% | Poultry belts near Casablanca and Rabat | Medium term (2-4 years) |

| Expansion of export-oriented horticulture | +1.8% | Souss-Massa, Gharb, and other coastal zones | Medium term (2-4 years) |

| Accelerated adoption of drought-tolerant varieties | +1.3% | Rain-fed cereal belts of Fès-Meknès and Marrakech-Safi | Short term (≤ 2 years) |

| Emergence of digital agri-marketplaces for seed ordering | +0.6% | Urban-adjacent areas around Casablanca and Agadir | Long term (≥ 4 years) |

| Phosphate-based seed-coating R&D leveraging local fertilizer industry | +0.8% | Pilot zones near Khouribga and Jorf Lasfar | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Subsidies for Certified Seeds

Morocco's 2024 to 2025 certified-seed subsidy program reduced wheat prices by 5% and barley by 3%, distributing 1.1 million quintals at subsidized rates of USD 21 per quintal for soft wheat and barley, and USD 29 per quintal for durum wheat [1]Source: Morocco Ministry of Agriculture, “Certified Seed Subsidy Program,” agriculture.gov.ma. This intervention directly lowers the entry cost for smallholders, who would otherwise allocate up to 12% of their seasonal budgets to seed procurement, and accelerates replacement rates in the Gharb and Saïss plains, where cereal monoculture dominates. The subsidy structure favors certified over farm-saved seed by narrowing the price gap to less than 20%, a threshold at which adoption curves steepen according to agronomic studies in semi-arid zones. The program's short-term impact peaks within 2 years as inventory cycles turn over, but sustained funding remains contingent on fiscal space and donor co-financing, introducing execution risk if commodity-price shocks divert budget allocations.

Rising Demand for High-Yield Hybrid Cereals

Morocco imported 2.2 million metric tons of corn during the 2022-2023 season to meet poultry-sector feed requirements, a volume that highlights the structural deficit in domestic coarse-grain production. The recovery of the poultry industry post-pandemic and rising per-capita meat consumption are driving feed-grain demand upward, creating a pull effect for high-yield hybrid maize and wheat seeds that can help close the gap between domestic supply and processing needs. The concentration of poultry operations around Casablanca and Rabat amplifies this demand in irrigated perimeters where water access supports intensive cropping. Bayer's 2024 commitment to launch 400 to 500 new seed hybrids and varieties annually, with active pipelines in wheat and vegetables for the Europe, Middle East, and Africa region, positions multinational breeders to capture this segment.

Expansion of Export-Oriented Horticulture

Morocco shipped 133,319 metric tons of small citrus to the European Union between October 2024 and April 2025, maintaining its role as a counter-seasonal supplier to northern markets. Tomato exports, the kingdom's flagship horticultural product, reached 740,000 metric tons valued at USD 1,030 million in 2022, cementing Morocco as the leading non-European source and creating sustained demand for disease-resistant, high-brix vegetable seed. Export contracts impose stringent phytosanitary and residue standards, prompting growers to adopt certified hybrid seed with documented resistance to tomato brown rugose fruit virus and other pathogens that can lead to border rejections. The medium-term impact persists through 2028 as Europe import quotas expand and Moroccan growers invest in greenhouse infrastructure, though currency volatility and freight-cost inflation introduce margin pressures that can dampen seed-budget flexibility.

Accelerated Adoption of Drought-Tolerant Varieties

The 2024 cereal harvest declined to 31.2 million quintals, a 43% year-on-year decrease, as the cultivated area decreased from 3.7 million hectares to 2.5 million hectares due to severe drought conditions. This shock accelerated farmer interest in drought-tolerant germplasm, particularly INRA-endorsed varieties such as Jawahir wheat, released in 2023, and 6 additional lines approved for commercialization following multi-location trials at Sidi Al-Aidi. The short-term impact peaks within 2 years as memory of the 2022 to 2024 drought remains vivid, and government extension services prioritize these varieties in subsidy allocations, though adoption rates will plateau if above-average rainfall returns and erodes perceived risk.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Erratic rainfall and water scarcity | -1.5% | Rain-fed cereal zones of Fès-Meknès and Marrakech-Safi | Short term (≤ 2 years) |

| Smallholder purchasing-power constraints | -0.9% | Farms below 5 hectares nationwide | Medium term (2-4 years) |

| Regulatory bottlenecks for GMO approvals | -0.7% | All crop-trait combinations | Long term (≥ 4 years) |

| Persistent informal seed-saving culture limiting varietal turnover | -1.1% | Traditional cereal regions nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Erratic Rainfall and Water Scarcity

Recurrent droughts cut seed demand by forcing acreage reductions, as evidenced by the 2024 season, when cultivated area fell from 3.7 million hectares to 2.5 million hectares, a 32% contraction that directly translated into lower seed purchases. Rain-fed cereal zones in Fès-Meknès and Marrakech-Safi bear the brunt of this volatility, where farmers delay planting decisions until late-season rainfall confirms soil moisture, often missing optimal sowing windows and opting to save cash rather than invest in seed. The World Bank's USD 250 million climate-smart agriculture program, approved in December 2024, aims to expand irrigation infrastructure and promote water-efficient varieties. However, implementation timelines stretch over five years and face execution risks tied to land-tenure complexity and competing fiscal priorities [2]Source: World Bank, “Climate-Smart Agriculture for Morocco,” worldbank.org .

Smallholder Purchasing-Power Constraints

High-quality seed can equal 12% of a smallholder's seasonal cash outlay, a burden that becomes prohibitive when grain prices fall or input costs for fertilizer and fuel spike. Farms below 5 hectares, which dominate Morocco's agrarian structure, operate on thin margins and prioritize liquidity for immediate household needs over investments with payback periods of 4 to 6 months. This constraint is most binding in the absence of subsidy support, as demonstrated by the 2024 to 2025 government program, which saw a rise in certified-seed uptake when prices dropped by 3% to 5%. The medium-term impact extends through 2028 as inflation pressures persist and global commodity cycles remain volatile, though targeted subsidy expansions or bundled input-credit schemes could partially offset the restraint.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Hybrids Anchor Value While GM Traits Await Regulatory Clarity

Hybrid seeds captured 45.40% of the Morocco seed market size in 2025. Hybrid seeds deliver heterosis effects that lift yields 20% to 40% above open-pollinated lines, a premium that justifies the 50% to 70% price differential in export-oriented horticulture and intensive cereal systems. Vegetable hybrids, particularly those of Solanaceae and cucurbits, command the highest margins due to their disease-resistance traits and fruit-quality attributes that European buyers demand. Cereal hybrids, led by maize, are expanding in irrigated perimeters where poultry-sector feed demand pulls adoption rates upward.

GM seeds recorded the fastest 10.9% CAGR through 2031, but face regulatory bottlenecks that delay field-trial approvals and commercialization, limiting current penetration to negligible levels. Varietal and open-pollinated seeds retain a foothold in rain-fed zones where smallholders prioritize low upfront costs and seed-saving flexibility over maximum yield potential. Enza Zaden Morocco, based in Agadir, focuses on tomato, pepper, cucumber, melon, and courgette hybrids, working closely with its Spanish subsidiary to adapt European germplasm to North African growing conditions.

By Crop Type: Vegetable Exports and Feed Deficits Shape Demand

Vegetables led the Morocco seed market with a 37.60% share in 2025, underpinned by Morocco's status as the European Union's leading non-European Union tomato supplier, which shipped a 740,000 metric tons valued at USD 1,030 million in 2022 . Cucurbits, including cucumbers, melons, and watermelons, serve both domestic and export markets, with Rijk Zwaan Maroc and Enza Zaden Morocco leading the development of varietals. Roots and bulbs, primarily onions and carrots, occupy niche segments with lower seed costs per hectare but stable demand from the processing industries. Brassicas, such as cabbage and cauliflower, face competition from European imports during the winter months, constraining local production incentives.

Pulses and oilseeds are projected to advance at a 9.3% CAGR to 2031, driven by a national plan to scale rapeseed and sunflower acreage to 70,000 to 80,000 hectares by 2030 and reduce vegetable-oil import dependency from the current 1.3% self-sufficiency level. This initiative requires state support exceeding USD 200 million and leverages the Europe-funded Olajino Oilseed Programme to distribute certified seed and provide agronomic training. Grains and cereals, encompassing maize, wheat, sorghum, and rice, remain the largest crop-type segment by volume but face demand volatility tied to erratic rainfall, as the 2024 harvest collapsed 43% year-on-year to 31.2 million quintals.

Geography Analysis

Morocco's seed market operates within a single-country geography, yet internal regional heterogeneity creates distinct demand profiles shaped by climate, irrigation access, and export orientation. The Souss-Massa region, centered on Agadir, dominates vegetable seed consumption due to its concentration of greenhouse and open-field horticulture, which supplies European markets with tomatoes, peppers, cucumbers, and melons. Enza Zaden Morocco and Rijk Zwaan Maroc maintain breeding stations and commercial operations in Agadir, reflecting the zone's strategic importance for varietal adaptation and demonstration trials. The Greenport Morocco Centre of Excellence, completed in June 2024, reinforces Agadir's role as a hub for technology adoption, showcasing protected cultivation techniques and water-efficient irrigation that enhance yields and extend harvest windows.

Coastal zones, including Gharb and Loukkos, combine export horticulture with irrigated cereals, creating dual demand for vegetable hybrids and high-yield maize seed. The Gharb plain benefits from the Sebou River irrigation scheme, supporting intensive cropping systems where hybrid penetration exceeds 50% of the maize area. Rain-fed cereal belts in Fès-Meknès and Marrakech-Safi exhibit lower seed-replacement rates, with approximately 42% of the acreage relying on farm-saved seed, as erratic rainfall and smallholder liquidity constraints hinder the adoption of commercial seed. The 2024 drought, which shrank cultivated area from 3.7 million hectares to 2.5 million hectares and cut cereal production to 31.2 million quintals, hit these regions hardest, compressing seed demand by 30% to 40% year-on-year.

The World Bank's USD 250 million climate-smart agriculture program, approved in December 2024, targets 1.36 million beneficiaries across rain-fed zones, prioritizing irrigation expansion and drought-tolerant germplasm to stabilize seed demand. Peri-urban zones around Casablanca and Rabat, where poultry operations concentrate, drive feed-grain demand and pull hybrid maize adoption rates above national averages, creating localized seed markets with higher price tolerance and faster varietal turnover.

Competitive Landscape

The Morocco seed market exhibits moderate concentration, with the top five players, including Rijk Zwaan Maroc SARL, Syngenta Group Co., Ltd., BASF SE, Agrosem SARL, and East-West Seed International Ltd., capturing a significant portion of the 2024 revenue, leaving a fragmented space for niche entrants targeting trait-specific segments and underserved crops. Strategic patterns emphasize vertical integration, as evidenced by OCP Group's October 2024 partnership with Université Mohammed VI Polytechnique, Intercéréales-France, and Arvalis to develop phosphate-based seed coatings and cereal innovations, creating a localized value chain that bypasses import costs.

Opportunities persist in pulses and oilseeds, where the national plan to scale rapeseed and sunflower acreage to 70,000 to 80,000 hectares by 2030 creates demand for certified seed that current suppliers underserve. Technology deployment centers on digital agronomy and precision phenotyping. Bayer's November 2024 collaboration with Orbia Netafim integrates Climate FieldView with irrigation management, enabling seed recommendations tailored to water availability and local microclimate conditions. ICARDA's SpectraVOCS project, funded by OCP Foundation, applies volatile-organic-compound profiling to accelerate faba bean breeding for stem borer resistance, shortening trait-development cycles from 10 to 12 years to 6 to 8 years.

Emerging disruptors include genome-editing platforms that deliver drought tolerance and disease resistance outside Morocco's GMO regulatory scope, potentially accelerating trait deployment by 2 to 3 years relative to transgenic pathways. Regulatory compliance under National Office for Food Safety (Office National de Sécurité Sanitaire des Produits Alimentaires) (ONSSA) seed-certification standards and phytosanitary protocols for export horticulture favors established players with local trial networks and quality-assurance infrastructure, raising barriers for new entrants lacking institutional relationships.

Morocco Seed Industry Leaders

Rijk Zwaan Maroc SARL

Syngenta Group Co., Ltd.

BASF SE

Agrosem SARL

East-West Seed International Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: The World Bank approved a USD 250 million climate-smart agriculture program for Morocco, targeting 1.36 million beneficiaries with irrigation expansion, drought-tolerant germplasm, and water-efficient practices. The program prioritizes rain-fed cereal zones in Fès-Meknès and Marrakech-Safi, where the 2024 drought cut production by 43%, and aims to stabilize seed demand by reducing climate-driven acreage volatility.

- March 2023: The International Center for Agricultural Research in the Dry Areas (ICARDA) and its partners have developed six promising new drought-tolerant varieties of durum wheat and barley. These new varieties aim to increase production, resilience, and nutritional quality for farmers. They possess climate-smart traits and enhanced food quality characteristics, including resistance to heat, drought, and pests.

- February 2023: BASF introduced tomato seed varieties resistant to the Tomato Brown Rugose Fruit Virus (ToBRFV) in Morocco through its Nunhems brand.

Morocco Seed Market Report Scope

The seed is one of the most basic and important agricultural inputs, and it forms the third-largest input market globally, after agrochemicals and farm machinery. The Morocco Seed Market Report is Segmented by Type (Hybrid Seeds, Conventional Seeds, and Varietal Seeds) and by Crop Type (Grains and Cereals, Pulses and Oilseeds, and More). The Market Forecasts are Provided in Terms of Value (USD).

By Type

| Hybrid Seeds |

| GM Seeds |

| Open-Pollinated Seeds |

By Crop Type

| Grains and Cereals | Maize |

| Rice | |

| Wheat | |

| Sorghum | |

| Other Grains and Cereals | |

| Pulses and Oilseeds | Soybean |

| Sunflower | |

| Canola | |

| Pulses | |

| Other Oilseeds | |

| Vegetables | Solanaceae |

| Cucurbits | |

| Roots and Bulbs | |

| Brassicas | |

| Other Vegetables | |

| Other Crops |

| By Type | Hybrid Seeds | |

| GM Seeds | ||

| Open-Pollinated Seeds | ||

| By Crop Type | Grains and Cereals | Maize |

| Rice | ||

| Wheat | ||

| Sorghum | ||

| Other Grains and Cereals | ||

| Pulses and Oilseeds | Soybean | |

| Sunflower | ||

| Canola | ||

| Pulses | ||

| Other Oilseeds | ||

| Vegetables | Solanaceae | |

| Cucurbits | ||

| Roots and Bulbs | ||

| Brassicas | ||

| Other Vegetables | ||

| Other Crops | ||

Key Questions Answered in the Report

What is the current value of the Morocco seed market?

The Morocco seed market size stands at USD 330.46 million in 2026 and is projected to reach USD 454.87 million by 2031.

Which segment grows fastest through 2031?

GM seed shows the highest 10.9% CAGR, although actual sales remain modest until regulatory clarity improves.

How important are vegetables to overall seed demand?

Vegetables accounted for 37.60% of the revenue share in 2025, driven by tomato exports to the European Union.

Why is drought-tolerant seed critical for Moroccan farmers?

The 2024 drought cut cereal output 43%, so varieties that stabilize yields in water-stressed fields reduce income risk.

Page last updated on: