Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

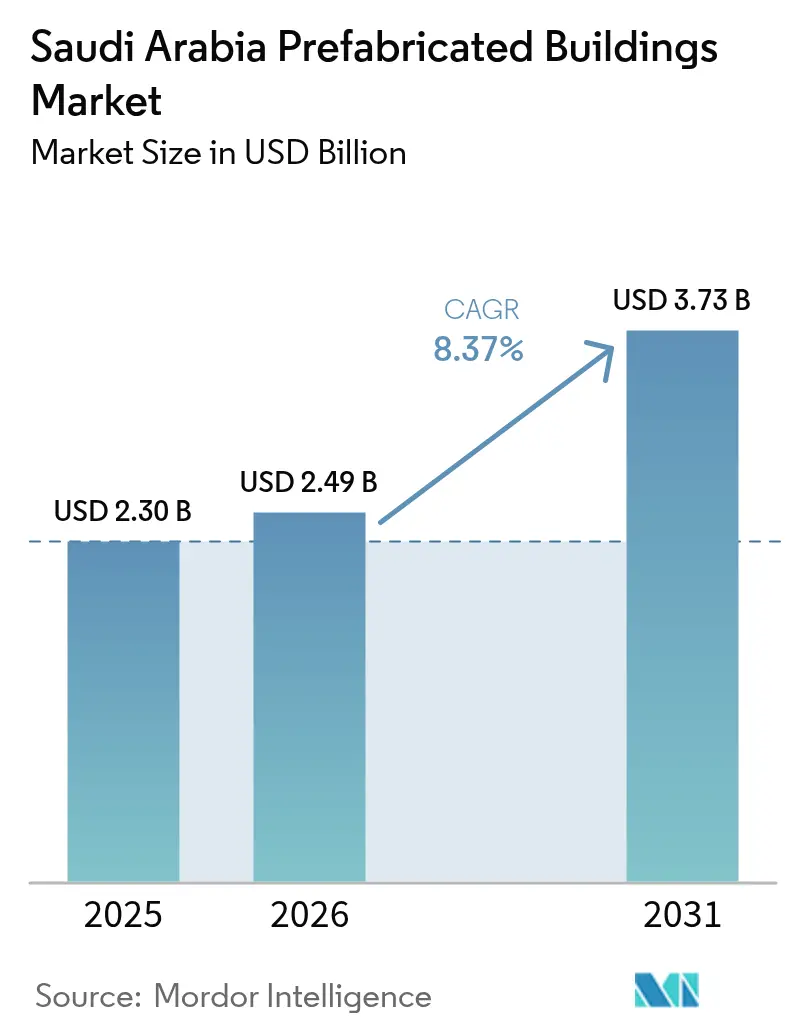

| Base Year Market Size (2025) | USD 2.30 Billion |

| Market Size (2026) | USD 2.49 Billion |

| Market Size (2031) | USD 3.73 Billion |

| Growth Rate (2026 - 2031) | 8.37% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Prefabricated Buildings Market Analysis by Mordor Intelligence

Saudi Arabia prefabricated buildings market size in 2026 is estimated at USD 2.49 billion, growing from 2025 value of USD 2.30 billion with 2031 projections showing USD 3.73 billion, growing at 8.37% CAGR over 2026-2031. This brisk expansion reflects Vision 2030 deadlines that favor rapid, industrialized construction, sovereign-wealth-fund capital channels, and an expanding pipeline of hotel capacity required for rising Hajj and Umrah visitation. Public Investment Fund (PIF) allocations of USD 19.4 billion to 91 green projects—including USD 372 million for eight prefabricated green-building developments—signal government preference for factory-built envelopes that meet Mostadam and SBC 2018 energy-efficiency thresholds. NEOM’s construction workforce has doubled to more than 140,000, and its USD 1.3 billion robotics joint venture with Samsung C&T is institutionalizing off-site assembly as the default delivery model for giga projects[1]NEOM and Samsung C&T formed a SAR 1.3 billion construction-robotics JV to automate rebar cage assembly, targeting 40% cost savings. Modular hotel programs anchored to religious-tourism targets of 36 million pilgrims by 2030 are accelerating demand for standardized, climate-controlled accommodation around Makkah and Madinah. Meanwhile, SBC 2018 enforcement is narrowing the field to operators with advanced quality-management systems, reinforcing a flight-to-scale dynamic that rewards large, technology-enabled fabricators.

Key Report Takeaways

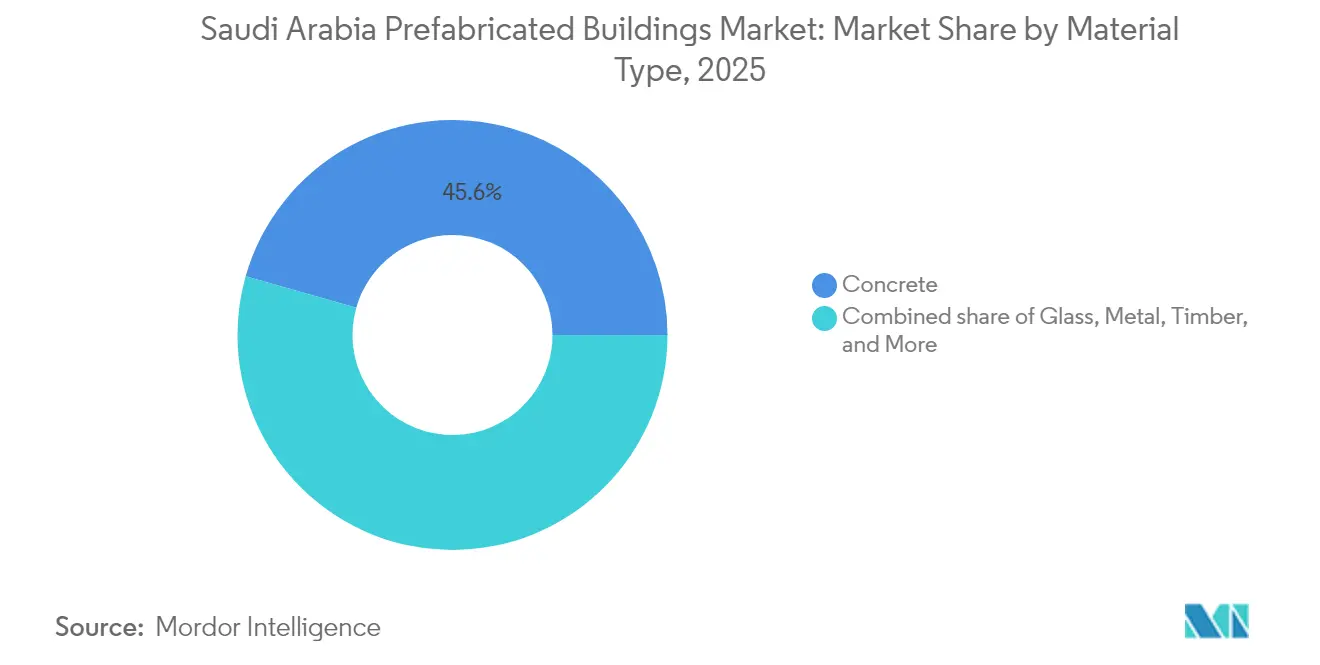

- By material type, concrete captured 45.60% of Saudi Arabia prefabricated buildings market share in 2025; timber is forecast to expand at a 9.49% CAGR through 2031.

- By application, the residential segment accounted for a 37.40% share of the Saudi Arabia prefabricated buildings market size in 2025, while commercial buildings are advancing at a 9.07% CAGR through 2031.

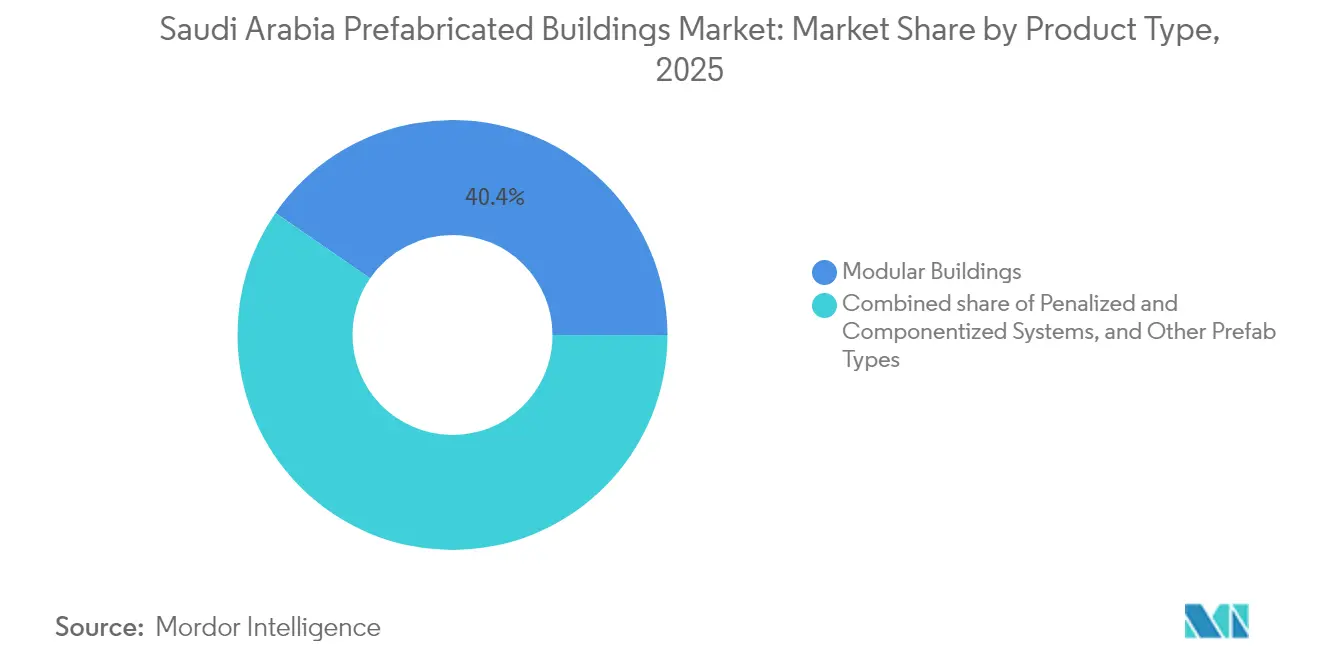

- By product type, modular buildings held a 40.40% share of the Saudi Arabia prefabricated buildings market in 2025 and are projected to grow at a 9.35% CAGR between 2026 and 2031.

- By city, Riyadh led with a 34.60% share of the Saudi Arabia prefabricated buildings market in 2025; Jeddah is recording the fastest trajectory at a 9.66% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Prefabricated Buildings Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 megaproject deadlines accelerating off-site adoption | +2.1% | National, with concentration in NEOM, Red Sea, Qiddiya | Medium term (2-4 years) |

| Public-sector housing PPPs demanding rapid delivery | +1.8% | National, with early gains in Riyadh, Jeddah, Eastern Province | Short term (≤ 2 years) |

| Rising Hajj/Umrah visitor volumes boosting modular hotel demand | +1.4% | Makkah, Madinah regions with spillover to transport corridors | Long term (≥ 4 years) |

| Mandatory green-building code favouring energy-efficient prefab envelopes | +1.2% | National implementation with stricter enforcement in major cities | Medium term (2-4 years) |

| Sovereign-wealth-fund backed industrialized-construction JV funding | +1.7% | Concentrated in giga-project zones, expanding to secondary cities | Long term (≥ 4 years) |

| AI-driven mass-customisation factories in King Salman Energy Park | +0.8% | Eastern Province with technology transfer to other industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Megaproject Deadlines Accelerating Off-Site Adoption

The USD 1.5 trillion Vision 2030 portfolio has reset construction schedules, prompting developers to embed prefabrication into project baselines to meet fixed completion dates. Samsung C&T’s rebar automation program at NEOM reduces manual steel-fixing labor by up to 80%, compressing structural cycles and improving safety compliance. The Red Sea Project mandates “unprecedented levels of prefabrication,” ensuring its 50 resorts and 8,000 rooms achieve carbon-neutral operations while staying on-schedule. Dedicated logistics corridors, including the expanding Port of NEOM, streamline oversized-module throughput, further embedding factory-built methods into giga-project delivery. The resulting economies of scale are closing the historical cost premium of off-site solutions, positioning the Saudi Arabia prefabricated buildings market as a primary beneficiary of Vision 2030 capital flows.

Public-Sector Housing PPPs Demanding Rapid Delivery

Saudi Arabia’s Housing Program enabled more than 1 million households to secure homes by 2024, lifting national ownership to 63.74% and underscoring the urgency for rapid-delivery construction. PPP frameworks stewarded by the National Center for Privatization involve 200 projects across 17 sectors, with housing, schools, and staff accommodations prioritized for modular deployment. Saudi Aramco’s USD 229 million staff-housing PPP on Abu Ali Island leverages factory-finished modules to meet a 28-month schedule for 500 residents. ROSHN’s Sedra community applies modular shells to accelerate a 30,000-unit roll-out east of Riyadh, signaling mainstream acceptance of prefabrication for mass housing.

Rising Hajj / Umrah Visitor Volumes Boosting Modular Hotel Demand

Umrah pilgrim arrivals jumped 58% year-on-year to 13.5 million in 2023, and the government targets 36 million by 2030, driving the need for 320,000–362,000 new hotel rooms valued at USD 110 billion[2]Hospitality Net, “Saudi Arabia set to deliver 362,000 new hotel rooms by 2030,” hospitalitynet.org. The USD 27 billion Masar mixed-use spine in Makkah and the USD 7 billion Thakher Makkah district both specify modular hotels that can flex capacity around peak pilgrimage periods. Prefabricated guestrooms deliver consistent finishes within compressed site windows, while factory-integrated MEP systems reduce commissioning time and ensure Mostadam compliance. Major operators such as Marriott and Accor are specifying premium modules to safeguard brand standards, reinforcing modular hotels as the default supply strategy for religious-tourism growth corridors.

Mandatory Green-Building Code Favoring Energy-Efficient Prefab Envelopes

SBC 2018 and its green-building addendum (SBC 1001-CR) oblige new buildings to meet strict U-value and airtightness thresholds, tilting the market toward factory-controlled envelopes that consistently achieve those metrics. The Mostadam rating encourages prefabricated projects to pre-install PV conduits, high-performance insulation, and smart HVAC systems, reducing on-site waste and rework. Academic modelling shows that correct insulation selection can cut operational energy by 2–14% across climate zones. PIF-owned HQ buildings are already reporting 20% energy savings through prefab facades, validating the regulatory push and supporting market expansion.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited domestic CLT/LVL supply raising import dependence | -1.3% | National, with acute impact on timber-intensive projects | Medium term (2-4 years) |

| Harsh-climate logistics for oversize modules in western desert corridors | -0.9% | Western regions, NEOM, Red Sea Project areas | Short term (≤ 2 years) |

| Fragmented municipal permitting outside Riyadh metro | -0.7% | Secondary cities, rural development zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Domestic CLT / LVL Supply Raising Import Dependence

Saudi projects specifying engineered timber currently import slabs from Europe and Australia, exposing budgets to currency swings and freight volatility. NEOM’s first 1,500 timber modules used Australian hardwood, illustrating lead-time risk for large timber interiors. Vision 2030 localization goals add pressure to cultivate domestic glulam, CLT, and LVL mills, yet capital intensity and feedstock constraints postpone meaningful capacity until late-decade. Until then, high-end timber towers remain vulnerable to shipment delays and spot-price surges that can derail project schedules and dampen Saudi Arabia prefabricated buildings market momentum.

Harsh-Climate Logistics for Oversize Modules in Western Desert Corridors

Moving 14-meter hotel modules from Gulf coast yards to Red Sea resorts entails 1,000-kilometer hauls across dune terrain where ambient temperatures reach 50 °C. Thermal expansion risks panel delamination, dictating specialized low-velocity convoys and costly climactic controls. Contractors such as Besix cite logistics as the single biggest hurdle on west-coast megaprojects, eclipsing even engineering complexity. Although Port of NEOM upgrades and Red Sea Global’s dedicated causeways alleviate some choke points, final-mile routes still restrict payload size, compelling multi-drop deliveries that erode prefab time-savings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Concrete Resilience and Timber Momentum

Concrete held a commanding 45.60% share of Saudi Arabia prefabricated buildings market in 2025, buttressed by widespread precast yards integrated with local cement and rebar supply chains. Durability under extreme heat and wind-blown sand preserves lifecycle value, maintaining concrete’s status as the default structural choice across housing, hotel, and industrial assets. Engineered timber, however, is projected to log a 9.49% CAGR, pivoting on sustainability codes and high-end aesthetics demanded by luxury segments of NEOM and Red Sea resorts. Saudi Arabia's prefabricated buildings market size for engineered timber is still marginal today, yet net-zero targets are stimulating policy interest in localized CLT plants, which could pivot share gains decisively after 2028. Composite and hybrid skins combining aluminum frames with insulated panels are also scaling as developers pursue lighter foundations for coastal reclamations.

Concrete’s cost stability and on-site familiarity keep it dominant among public-sector schools and hospitals, but innovation within admixtures and precast connection systems is creating weight and time advantages previously associated only with steel. Timber’s status as the fastest-growing material is amplified by Mostadam point incentives for sequestered carbon, a factor that offsets import premiums in prestige projects. R&D initiatives exploring basalt-fiber reinforcement and rammed-earth interior walls reflect a broader experimentation trend as Vision 2030 architects seek culturally resonant, climate-appropriate assemblies.

By Application: Residential Scale Faces Commercial Surge

Residential builds retained 37.40% share of Saudi Arabia prefabricated buildings market size in 2025, tethered to government homeownership milestones and multizone communities such as ROSHN Sedra. Permanent modular construction reduces the average villa handover cycle from 14 months to fewer than 8 months, allowing public agencies to track quarterly keys-in-hand targets. Commercial stock is forecast to pace the market at 9.07% CAGR through 2031, mirroring hospitality demand curves tied to pilgrimage peaks and office pipeline expansions linked to Riyadh’s global financial-center ambitions. Saudi Arabia prefabricated buildings market share within commerce is also driven by data-center shells in Oxagon and SPARK, which favor pre-wired steel pods for rapid commissioning.

Beyond core segments, the “Others” bucket—spanning healthcare, education, and industrial—absorbs PPP deals for 4,000 schools and multiple field hospitals. Pre-assembled operating theaters shorten fit-out schedules while supporting infection-control standards, demonstrating prefabrication’s value beyond speed alone. Compliance with SBC 2018 pushes residential and commercial developers alike toward consistent thermal envelopes achievable only in controlled factory environments.

By Product Type: Modular Buildings Dominate and Innovate

Modular buildings captured 40.40% of Saudi Arabia prefabricated buildings market share in 2025 and will maintain momentum at a 9.35% CAGR through 2031. Red Sea International’s 770,000 m² annual capacity underscores the industrial scale that has emerged to serve giga-project demand. Robotics-enabled finishing lines allow eight-story modules to roll out at five-day takt times, while AI-driven quality-inspection cameras reduce defect rates. Panelized and componentized systems retain niches where irregular footprints complicate volumetric approaches, such as museum atriums and airport canopies. Saudi Arabia prefabricated buildings market size for panelized systems is set to grow more modestly but will benefit from hybrid integration into volumetric cores.

Additive-manufactured elements, highlighted by the world’s first 3D-printed mosque completed in 2024, signal an innovation frontier that may compress bespoke façades into single-day prints. NEOM’s robotics unit blurs conventional boundaries by combining panelization with fully serviced pods, hinting at a convergent ecosystem where product-type distinctions dissolve under unified digital fabrication platforms.

Geography Analysis

Riyadh generated 34.60% of Saudi Arabia's prefabricated buildings market value in 2025, leveraging centralized permitting and anchor projects such as the USD 50 billion Mukaab mixed-use cube now under construction. Capital-centric budgets, coupled with a robust industrial base—44.3% of national factories are sited here—create continuous demand for volumetric housing and Class-A office shells. Jeddah posts the steepest growth curve at 9.66% CAGR, energized by Red Sea resort modules and the MARAFY canal-front redevelopment that prioritizes prefab micro-units and hospitality suites.

DMA’s proximity to SPARK and petrochemical complexes stabilizes industrial order flow, while the Rest-of-Kingdom category, spanning NEOM’s desert plateau to Tabuk’s coastal inlet, commands huge absolute volumes owing to giga-project site build-outs.

Logistics disparities remain; Riyadh enjoys complete grade-separated ring roads, whereas west-coast corridors still grapple with oversize-load curfews. Regulatory fragmentation outside the capital elongates approval timelines, yet the Future Projects Forum lists more than SAR 1 trillion in upcoming contracts beyond the three major metros, guaranteeing that geographic diversification will continue shaping Saudi Arabia prefabricated buildings market dynamics.

Competitive Landscape

The Saudi Arabia prefabricated buildings market is moderately fragmented, with industry leaders setting themselves apart through scale, automation, and strict compliance. Red Sea International, leveraging its hubs in Jubail and Dubai, boasts an impressive annual throughput of 770,000 m², allowing it to concurrently deliver both housing and hospitality solutions.

Spacemaker KSA completes up to 1,000 m² of pods per day using conveyorized welding gantries and robot-assisted paint booths, setting a productivity bar that smaller regional yards struggle to match. NEOM’s robotics partnership sets new process benchmarks—machine-assembled rebar cages guarantee positional tolerance and shave two days per floor plate, reshaping client expectations.

Capitalized entrants backed by PIF and Aramco venture arms are pursuing disruptive technologies. Mighty Buildings—fresh off a USD 52 million funding round—intends to introduce printed composite shells that halve embodied carbon against traditional concrete, positioning itself for villa portfolios in climate-sensitive coastal zones. Simultaneously, legacy steel firms are retrofitting beam lines to manufacture volumetric frames, capturing Mostadam opportunities while preserving asset bases.

Regulatory screening now extends to ESG reporting and SCA licensing, triggering consolidation as under-capitalized shops exit or merge. Those retaining ISO 9001 and Mostadam pre-approvals gain preferred-bidder status on PPP rosters, reinforcing a virtuous cycle of scale and compliance. International attention is rising: the Chinese engineering giant CEEC recently secured a 2 GW EPC contract that complements prefab substation enclosures, indicating cross-border competition is set to intensify[4]MEED, “CEEC to undertake EPC works for 2 GW Saudi project,” meed.com.

Saudi Arabia Prefabricated Buildings Industry Leaders

Red Sea Housing Services

Zamil Steel (Pre-Engineered Buildings)

Saudi Building Systems Mfg. Co. (SBS)

Nesma & Partners – Modular Division

Al-Jazira Prefab Houses

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: NEOM and DataVolt announced a USD 5 billion net-zero AI factory in Oxagon, operational by 2028, to underpin automated component manufacturing. The plant adds localized capacity for high-precision panels and MEP skids, supporting supply-chain resilience and lowering import dependence for future modular contracts.

- December 2024: NEOM and Samsung C&T formed a SAR 1.3 billion construction-robotics JV to automate rebar cage assembly, targeting 40% cost savings. Automated steel fabrication will compress structural cycles, enabling higher factory throughput and reducing module lead times across the Saudi Arabia prefabricated buildings market.

- November 2024: ROSHN Group rebranded and launched the MARAFY canal project in Jeddah, expanding its mandate to mixed-use prefab assets. The project elevates demand for premium volumetric units and underscores prefab’s role in high-density coastal developments.

- November 2024: MODON inked USD 533 million contracts with Albaddad Holding to erect industrial complexes in Makkah and Al-Kharj centered on prefab halls. These complexes expand end-use adoption of prefab shells in light-industrial real estate, creating a steady pipeline for steel-frame fabricators.

Saudi Arabia Prefabricated Buildings Market Report Scope

Prefabricated buildings, often referred to as prefab homes, are primarily manufactured in advance off-site, then delivered and assembled on-site. This report covers market insights, such as market dynamics, drivers, restraints, opportunities, technological innovations and their impact, Porter's five forces analysis, and the impact of COVID-19. Additionally, the report provides company profiles of leading market players to help understand the competitive landscape.

The Saudi Arabian prefabricated buildings market is segmented by application (residential, commercial, and other applications (industrial, institutional, and infrastructure)) and material type (concrete, glass, metal, timber, and other material types). The report offers market sizes and forecasts in value terms (USD) for all the above segments.

By Material Type

| Concrete |

| Glass |

| Metal |

| Timber |

| Other Materials |

By Application

| Residential |

| Commercial |

| Others |

By Product Type

| Modular Buildings |

| Panelized & Componentized Systems |

| Other Prefab Types |

By Region (Saudi Arabia)

| Riyadh |

| Jeddah |

| DMA (Dammam Metropolitan Area) |

| Rest of Saudi Arabia |

| By Material Type | Concrete |

| Glass | |

| Metal | |

| Timber | |

| Other Materials | |

| By Application | Residential |

| Commercial | |

| Others | |

| By Product Type | Modular Buildings |

| Panelized & Componentized Systems | |

| Other Prefab Types | |

| By Region (Saudi Arabia) | Riyadh |

| Jeddah | |

| DMA (Dammam Metropolitan Area) | |

| Rest of Saudi Arabia |

Key Questions Answered in the Report

What is the current value of Saudi Arabia prefabricated buildings market?

The market stands at USD 2.49 billion in 2026 and is projected to reach USD 3.73 billion by 2031.

How fast is the sector growing?

It is advancing at a 8.37% CAGR, propelled by Vision 2030 megaproject timelines and a surge in modular hotel demand.

Which material leads the market?

Precast concrete retains 45.60% share, while engineered timber is the fastest-growing material at a 9.49% CAGR.

Why are modular hotels gaining traction?

Rising Hajj and Umrah pilgrim numbers require rapid accommodation delivery; factory-built rooms compress schedules and ensure consistent quality.

How does SBC 2018 impact prefab adoption?

Mandatory energy-efficiency and green-building clauses favor factory-controlled envelopes, accelerating prefab penetration across segments.

Who are the prominent players?

Red Sea International, Spacemaker KSA, and technology-driven entrants backed by PIF and Aramco ventures dominate output capacity and automation investment.

Page last updated on: