Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

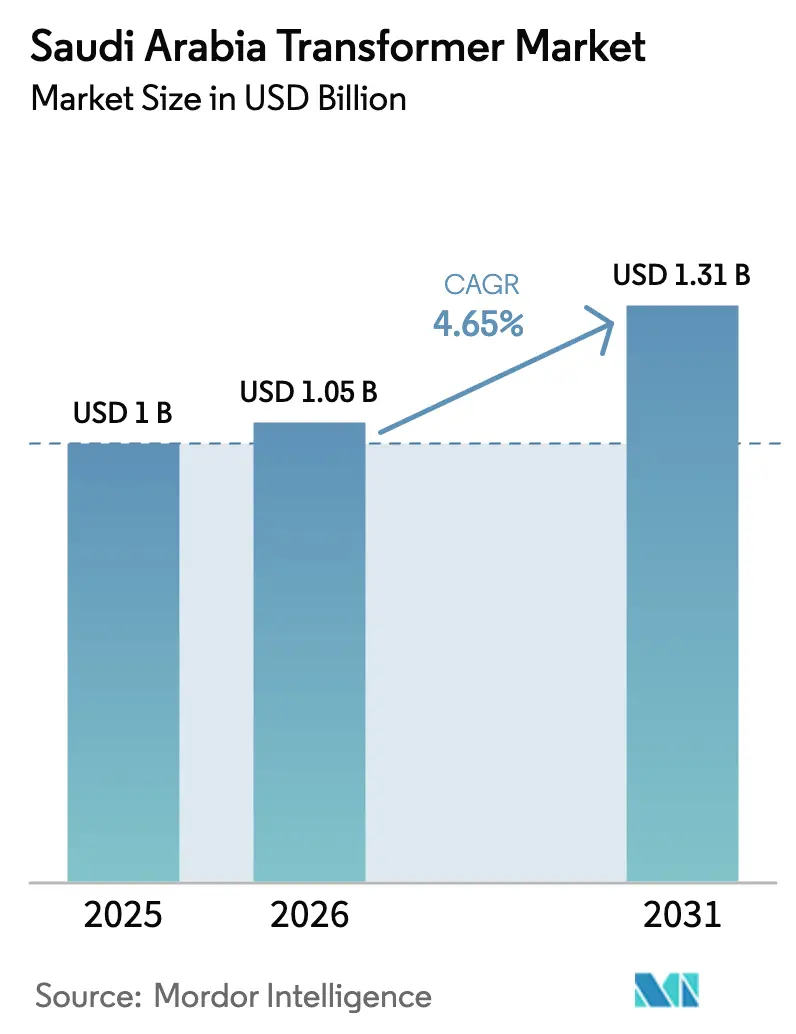

| Base Year Market Size (2025) | USD 1 Billion |

| Market Size (2026) | USD 1.05 Billion |

| Market Size (2031) | USD 1.31 Billion |

| Growth Rate (2026 - 2031) | 4.65% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Transformer Market Analysis by Mordor Intelligence

The Saudi Arabia Transformer Market size was valued at USD 1 billion in 2025 and estimated to grow from USD 1.05 billion in 2026 to reach USD 1.31 billion by 2031, at a CAGR of 4.65% during the forecast period (2026-2031).

Sustained transmission expansion by Saudi Electricity Company (SEC), which is expected to connect 6.7 GW of renewable capacity by Q1 2025, underpins equipment demand as the utility targets an additional 34.4 GW by 2027. Medium-rated units (10-100 MVA) currently anchor volumes, but large transformers (>100 MVA) are leading the growth curve, thanks to high-voltage DC (HVDC) links and utility-scale solar and wind farms. Oil-cooled technology remains prevalent; however, sealed air-cooled alternatives are gaining momentum in desert environments, as they simplify maintenance and mitigate contamination risks. Local-content rules, combined with public-sector capital expenditure (capex) equal to roughly 5% of GDP, are attracting new investment from global majors and spurring capacity additions by domestic manufacturers.

Key Report Takeaways

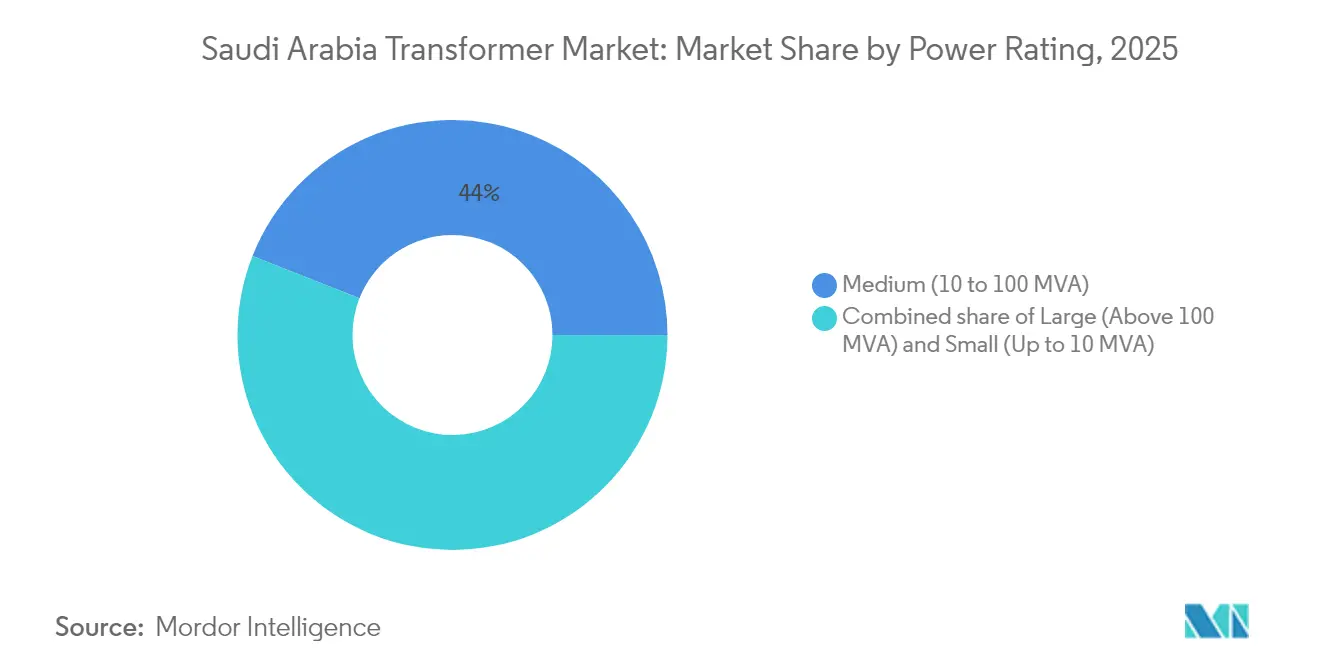

- By power rating, medium-rated transformers held 44.02% of the Saudi Arabia transformer market share in 2025, while large units are projected to advance at a 6.38% CAGR through 2031.

- By cooling type, oil-cooled systems accounted for 69.75% of the Saudi Arabia transformer market size in 2025; air-cooled designs are expected to post a 6.11% CAGR to 2031.

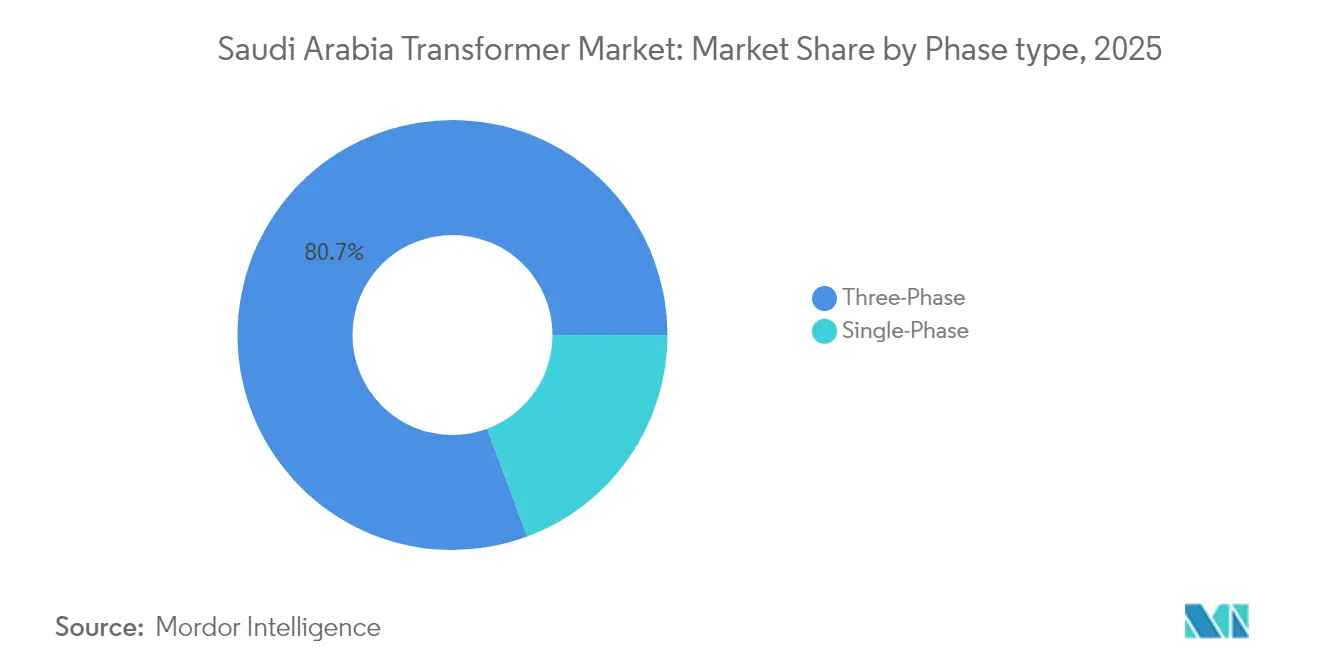

- By phase, three-phase designs captured an 80.65% share of the Saudi Arabia transformer market size in 2025 and are expected to grow at a 4.92% CAGR during 2026-2031.

- By transformer type, distribution units commanded a 59.85% share of the Saudi Arabia transformer market size in 2025, expanding at a 5.12% CAGR through 2031.

- By end-user, power utilities led with 49.35% of the Saudi Arabia transformer market share in 2025; the commercial segment is forecast to accelerate at a 6.65% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Transformer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 infrastructure build-out | +1.20% | Riyadh, Eastern Province, NEOM | Long term (≥ 4 years) |

| 50% renewables-by-2030 target | +0.90% | Northern Borders, Tabuk, Al Jouf | Medium term (2-4 years) |

| Rapid peak-load growth | +0.70% | Urban centers, industrial cities | Short term (≤ 2 years) |

| Local-content mandates | +0.50% | National manufacturing hubs (Eastern Province) | Medium term (2-4 years) |

| Mega sports & entertainment projects | +0.30% | Riyadh, Jeddah, NEOM, Al-Ula | Short term (≤ 2 years) |

| Hydrogen & green-ammonia mega-projects | +0.40% | NEOM, Yanbu, Eastern Province | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Infrastructure Build-out Fuels Grid & Sub-station Additions

The SEC raised its transmission network above 100,700 circuit kilometers in Q1 2025, following a string of quarterly 4% expansions. New substations that accompany these lines incorporate digitally enabled transformers, 37.5% of which already feature remote monitoring capability. Projects such as the USD 5.33 billion 7 GW HVDC converter-station award to Alfanar illustrate the scale of individual contracts that require specialized 7 GW-class converter transformers for bulk power transfer. An additional 60,300 customers joined the grid in Q1 2025, bringing the total number of connections to 11.37 million and triggering increased demand for parallel distribution transformers. Public-sector spending—roughly 5% of GDP—remains protected under the latest fiscal plan, insulating the Saudi Arabia transformer market from cyclical capex pauses. Each new substation typically installs multiple high-voltage and medium-voltage units, establishing reliable multi-year volume visibility for suppliers.

50% Renewables-by-2030 Target Drives Step-up Transformers for PV & Wind

Renewable capacity must increase from 2.8 GW in 2024 to 130 GW by 2030, corresponding to near-term annual additions of 20 GW. Step-up transformers sit at the center of this build-out because they raise the outputs of solar and wind farms to grid voltage. ACWA Power’s commitment to deliver roughly 70% of planned capacity promotes standardized transformer specifications, which speed up procurement while reducing costs.(1)ACWA Power, “Capacity Expansion Strategy 2025,” acwapower.com Interconnection projects—such as the 1 GW Iraq-Saudi link now live and a planned 3 GW Egypt-Saudi tie scheduled for 2026—need high-capacity autotransformers and frequency-conversion equipment. Solar inverter harmonics are prompting requests for enhanced voltage-regulation features and harmonic filtering within transformer designs. As variable renewables penetrate deeper, older units without bidirectional capability face accelerated replacement cycles.

Rapid Peak-load Growth from Population & Industrialization

Ma’aden’s H1 2024 net profit jumped 160.4% and foreign direct investment stocks climbed 6.1% year-on-year to USD 217.88 billion, underscoring a sustained industrial upswing. Data-center build-outs—USD 1 billion from Equinix, plus a 1.5 GW facility at NEOM—create concentrated, round-the-clock power demand that dwarfs traditional commercial loads. EV charging roll-outs could approach 160,000 public points by 2035 to support a targeted 31% passenger-car EV share in 2030, each fast-charge hub relying on dedicated distribution transformers. Tourism arrivals surged 73% in the first seven months of 2024, compelling hospitality upgrades that also lift distribution-level demand. Rising summer air-conditioning loads, layered onto industrial and commercial growth, create compound peaks that stress existing units and prompt accelerated procurement of medium-rated models.

Local-content Mandates Boost Domestic Transformer Manufacturing

December 2024 regulations added 122 transformer-related items to the mandatory local-content list. Aramco’s iktva program, channeling over USD 28 billion in annual spend, rewards vendors that exceed localization thresholds, reshaping bid evaluations in favor of Saudi-based manufacturers. United Transformers Electric Company (UTEC) is expanding tailored distribution-unit production through its joint venture with Wilson Transformer Company to meet the SEC’s specification library. Emerson inaugurated a 13,000 m² hub at King Salman Energy Park in October 2024, capturing automation assemblies that pair with transformer installations. While localization stimulates technology transfer and job creation, initial ramp-up costs and capacity constraints can lengthen delivery schedules and lift short-term pricing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital intensity & lengthy tenders | -0.80% | National | Medium term (2-4 years) |

| Volatile copper & steel prices | -0.60% | Global supply chains → Saudi projects | Short term (≤ 2 years) |

| Grid-code harmonization delays | -0.40% | National | Short term (≤ 2 years) |

| Desert heat & sand raise O&M costs | -0.30% | Central & Eastern regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Intensity & Lengthy Tender Cycles

Government bids route through the Etimad platform, where payment terms range from 60 to 70 days, producing working-capital strains for mid-tier vendors. Compliance with the 2019 Tenders and Procurement Law, while elevating transparency, introduces extra documentation and surety-bond requirements that can extend evaluations well past planned award dates. The SEC’s SAR 6.73 billion utility-scale battery project illustrates the magnitude of single tenders, each requiring robust balance sheets and past-performance proofs for eligibility. Manufacturers holding costly core steel or windings inventory must finance their stock during months-long evaluations, which dissuades smaller entrants. The EXPRO agency, established in 2021, continues to streamline procedures but has not yet fully resolved the time-to-award issues that hinder urgent replacement orders.

Volatile Copper & Steel Prices Squeeze Project Budgets

Copper and steel account for roughly 60-70% of transformer build cost, and sharp rallies have squeezed fixed-price supply contracts. Econometric work from 1998 to 2024 shows that supply-chain shocks added 0.038 percentage points to national inflation, highlighting macroeconomic sensitivity to raw-material costs.(2)Fiscal Studies & Statistics Center, “Commodity-Price Shocks and Saudi Inflation,” fsksa.org Although Saudi mills expand capacity, world pricing still sets the domestic baseline. Red Sea shipping disruptions reduced regional volumes by 40%, leading to increased freight surcharges that are then passed on to delivered unit costs. Suppliers without hedging mechanisms face margin erosion or must raise bid prices, both of which weigh on short-term order intake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Rating: Large Units Accelerate Transmission Upgrades

Large transformers above 100 MVA are expected to post a 6.38% CAGR to 2031 as the Saudi Arabia transformer market expands to include HVDC lines, 380 kV autotransformers, and massive renewable intertie equipment. Medium-rated models account for 44.02% of the Saudi Arabia transformer market share in 2025, primarily serving petrochemical complexes in Jubail and Yanbu, as well as expanding urban feeders in Riyadh. Small units under 10 MVA see steady but slower gains tied to residential extensions. Hyundai Electric’s USD 51 million NEOM substation award underscores the premium commanded by units weighing≥ 200 tons, which can cost USD 8.9 million each. Engineering complexity and lengthy 120-210-week lead times shield the high-capacity niche from low-cost entrants, concentrating orders among proven OEMs.

Large-unit demand rises in lockstep with mega-project timelines: the 4 GW NEOM Green Hydrogen Complex and the ±500 kV Riyadh-Kudmi HVDC link both specify converter transformers exceeding 300 MVA. IEC-aligned monitoring functions—such as fiber-optic winding temperature probes and gas-in-oil sensors—now appear standard on every high-rating tender. While medium-rated sales remain the volume workhorse, grid planners increasingly re-evaluate 132 kV corridors for upgrade to 275 kV and 380 kV, bumping medium units into higher classes over the forecast horizon.

By Cooling Type: Air-cooled Gains in Harsh Desert Sites

Oil-cooled systems accounted for 69.75% of 2025 revenue, owing to their superior power density and established SEC type tests. Yet air-cooled variants, advancing at 6.11% CAGR, provide sealed-tank simplicity that avoids routine oil sampling and mitigates sand ingress in remote PV fields. Studies on 230 kV polymer insulator performance confirm accelerated aging in coastal salt-spray zones, pushing asset managers to consider sealed systems for lifecycle savings.Predictive-maintenance analytics cut O&M costs up to 40% when applied to oil-cooled fleets, partially offsetting their service burden.

Lifecycle economics tend to favor air-cooled units in smaller ratings, where power density gaps are less critical. Urban fire-safety rules are another tailwind: Riyadh municipalities increasingly specify air-insulated units for indoor substations. Nonetheless, large bulk-power and converter transformers will remain oil-cooled through 2031 because forced-oil-forced-air (FOFA) configurations manage extreme thermal loads that dry-type cores cannot yet accommodate at scale.

By Phase: Three-Phase Standard Remains Unchallenged

Three-phase equipment captured 80.65% of the Saudi Arabia transformer market size in 2025 with a 4.92% CAGR outlook. Industrial motors, high-voltage feeders, and data-center UPS systems all depend on three-phase supply, preserving a dominant share. Single-phase units persist in residential laterals but rarely exceed 50 kVA, keeping total value modest. SEC’s distribution circuit length climbed to 816,000 km in Q1 2025; the majority are three-phase feeders to industrial estates and evolving smart-grid loops.

Transformer OEMs design three-phase cores using miter-cut, grain-oriented steel, which generates higher material yields but also imposes tighter fabrication tolerances that deter small workshops. Cross-border connections with Egypt and Iraq share a three-phase architecture, reinforcing standardization across Gulf Cooperation Council (GCC) grids. Even emerging fast-charging corridors rely on balanced three-phase input to mitigate harmonic distortion from 350 kW DC chargers.

By Transformer Type: Distribution Units Dominate Installed Base

Distribution transformers held 59.85% of the Saudi Arabia transformer market size in 2025 and are expected to expand at a 5.12% CAGR to 2031 as SEC onboards new consumers and smart meters. Each Q1 2025 grid connection triggers a demand chain for low-loss 250 kVA-to-2.5 MVA pole-mount or pad-mount units calibrated to SEC’s loss-evaluation formula SEC.COM.SA. Power transformers, although fewer in number, generate high revenue per unit, particularly for≥33 kV step-ups in generation plants and ≥380 kV interties.

United Transformers Electric Company customizes distribution units according to the SEC Rev-18 specification, prioritizing low excitation loss and aluminum windings for cost efficiency. Power-class orders show lumpiness tied to mega-projects; for example, the ±500 kV HVDC scheme installed purpose-built 1,100 MVA converters in 2025. Hybrid grids with bidirectional flows prompt new specifications, where distribution units integrate on-load tap changers once reserved for power classes, blurring historic distinctions.

By End-User: Commercial Segment Outpaces Utilities

Utilities retained 49.35% of 2025 revenue through bulk procurement but the commercial category is scheduled to grow 6.65% CAGR, the fastest among all segments. Data-center capacity, which hit 71.17 MW IT load after stc’s Phase 4 expansion, concentrates 15-20 MVA per campus, each requiring fault-current-rated sub-station transformers. Hospitality venues in King Salman Park, plus stadium retrofits for the 2034 FIFA World Cup, order low-loss cast-resin units for indoor spaces with tight fire codes.

Industrial buyers remain stable as petrochemical and steel plants roll through multi-year debottleneck programs, while EV assembly sites such as Lucid’s Jeddah plant slot into the commercial-industrial hybrid. Residential growth trails but still adds steady volumes on the back of 73% tourism-driven population influx spikes that inflate rental stock. The line between commercial and utility procurement narrows when independent power producers supply embedded generation behind commercial meters, requiring utility-spec power transformers in private facilities.

Geography Analysis

The Eastern Province commands the single largest cluster of transformer demand due to the presence of petrochemical giants in Jubail and the King Salman Energy Park in Dammam, both of which rely on 132 kV-to-380 kV step-downs for process power. Riyadh, the political and financial capital, is closely followed by metro rail extensions, King Salman Park's 21.6 km² entertainment hub, and a growing data center corridor that stretches toward Diriyah. Western Province demand rises on the back of the Red Sea Project's hospitality assets and Jeddah's port-centric logistics growth; here, 110 kV cast-resin units are gaining traction for indoor substations serving hotel clusters.

NEOM redefines the northern landscape: the 4 GW hydrogen complex and a 1.5 GW hyperscale data center zone together drive orders for step-up and converter-transformer equipment that surpass those of earlier greenfield builds in Tabuk. Cross-border interties shape border demand as the operational 1 GW Iraq link and the future 3 GW Egypt tie necessitate specialized phase-shifting transformers to manage differing grid codes. Climate variation influences designs: coastal areas specify C4-grade corrosion-proof tanks, while central-desert substations add forced-oil cooling to counter 55 °C ambient peaks. Logistics considerations favor Eastern Province ports after Red Sea volatility led to a 40% reduction in shipping volume to Jeddah. The result: more OEMs schedule final winding and test operations near Dammam to reduce the risk of over-the-road haulage for heavyweight cores. As Vision 2030 economic zones mature, spatial transformer demand becomes multi-centered, distributing procurement influence beyond the historic Eastern-Riyadh axis.

Competitive Landscape

Global majors—ABB, Siemens Energy, GE Vernova, Hitachi Energy, and Schneider Electric—share the high-rating, technology-intensive tier. Each maintains a Saudi manufacturing or service footprint to satisfy localization thresholds; GE Vernova has earmarked up to USD 14.2 billion for Saudi ventures, covering turbines, synchronous condensers, and transformer-related balance-of-plant. Hitachi Energy will invest an additional USD 250 million worldwide to alleviate component bottlenecks that currently extend Saudi delivery lead times.

Domestic champions, notably UTEC and Saudi Power Transformer Company, leverage local-content credits, quick service response, and familiarity with SEC specifications to defend their distribution-unit turf. HD Hyundai Electric’s USD 274 million capacity lift across Korea and the U.S. ensures supply resilience for its NEOM contracts and positions the firm for follow-on large-unit tenders. Market share battles are shifting from pure hardware to digitally enabled lifecycle packages: OEMs now bundle online dissolved-gas analysis, fiber-optic winding sensors, and AI-based failure prediction models to lock in service revenue.

White-space opportunities revolve around converter transformers for hydrogen electrolyzer farms, traction-grade transformers for urban rail, and smart distribution units that integrate automatic voltage regulation and real-time telemetry. Bidders who can combine hardware with analytics platforms gain an edge in public tenders that are scored on total cost of ownership. Despite an intensifying rivalry, barriers tied to IEC-type testing, SEC qualification, and localization still restrict the total field to under 30 active suppliers across all ratings.

Saudi Arabia Transformer Industry Leaders

Siemens AG

ABB Ltd

General Electric Company

Mitsubishi Electric Corporation

Schneider Electric

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: GE Vernova unveiled Saudi initiatives worth up to USD 14.2 billion, spanning gas turbines, synchronous condensers, and grid-stability packages that necessitate complementary transformer procurement.

- April 2025: The SEC launched a SAR 6.73 billion, 2,500 MWh battery-storage program across five sites, each requiring bespoke grid-connection transformers.

- March 2025: Hitachi Energy has committed USD 250 million to expand its global component output, thereby alleviating shortages of bushings and tap changers that affect Saudi deliveries.

- March 2025: The Saudi Electricity Company (SEC) has officially energized the ±500 kV Riyadh–Kudmi HVDC transmission line, marking a major milestone in Saudi Arabia’s grid modernization efforts. This ±500 kV HVDC line features a 3–4 GW transmission capacity, enabling long-distance, high-efficiency power transfer.

- January 2025: HD Hyundai Electric announced a USD 274 million capacity upgrade; its Saudi backlog includes a USD 51 million NEOM substation package.

Saudi Arabia Transformer Market Report Scope

By Power Rating

| Large (Above 100 MVA) |

| Medium (10 to 100 MVA) |

| Small (Up to 10 MVA) |

By Cooling Type

| Air-cooled |

| Oil-cooled |

By Phase

| Single-Phase |

| Three-Phase |

By Transformer Type

| Power |

| Distribution |

By End-User

| Power Utilities (includes, Renewables, Non-renewables, and T&D) |

| Industrial |

| Commercial |

| Residential |

| By Power Rating | Large (Above 100 MVA) |

| Medium (10 to 100 MVA) | |

| Small (Up to 10 MVA) | |

| By Cooling Type | Air-cooled |

| Oil-cooled | |

| By Phase | Single-Phase |

| Three-Phase | |

| By Transformer Type | Power |

| Distribution | |

| By End-User | Power Utilities (includes, Renewables, Non-renewables, and T&D) |

| Industrial | |

| Commercial | |

| Residential |

Key Questions Answered in the Report

What is the current value of the Saudi Arabia transformer market?

The Saudi Arabia transformer market size was USD 1.05 billion in 2026 and is projected to reach USD 1.31 billion by 2031.

Which transformer rating category is growing fastest in Saudi Arabia?

Units above 100 MVA are forecast to expand at a 6.38% CAGR between 2026 and 2031 thanks to HVDC projects and renewable interconnections.

How are local-content rules affecting transformer suppliers?

Mandatory localization lists and Aramco’s iktva incentives are steering awards toward manufacturers with Saudi production footprints or partnerships, reshaping bid strategies.

What cooling technology trend is emerging in desert installations?

Air-cooled, sealed transformers are gaining ground at a 6.11% CAGR because they cut maintenance and handle sand-laden environments better than oil-filled equivalents.

Which end-user segment will outpace others through 2031?

Commercial facilities—driven by data-center and hospitality investments—will expand at a 6.65% CAGR, the fastest among all end-users.

What recent mega-project is influencing large-transformer demand?

The ±500 kV Riyadh-Kudmi HVDC link, energized in March 2025, required high-capacity converter transformers and signals further utility demand for similar equipment.

Page last updated on: