Saudi Arabia Switchgear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.52 Billion |

| Market Size (2026) | USD 2.67 Billion |

| Market Size (2031) | USD 3.56 Billion |

| Growth Rate (2026 - 2031) | 5.94% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Switchgear Market Analysis by Mordor Intelligence

The Saudi Arabia Switchgear Market size was valued at USD 2.52 billion in 2025 and estimated to grow from USD 2.67 billion in 2026 to reach USD 3.56 billion by 2031, at a CAGR of 5.94% during the forecast period (2026-2031).

Momentum stems from Vision 2030’s grid modernization drive, utility-scale renewable rollouts, giga-project electrification, and steady construction activity that elevates procurement across all voltage classes. Government guidance on localized manufacturing is widening participation for domestic suppliers even as global OEMs introduce digital, SF₆-free, and cybersecurity-ready equipment that commands premium pricing. Simultaneously, utilities are standardizing 132 kV-380 kV backbones to integrate new solar and wind generation, while rising industrial power demand by 8.3% in 2024 underscores the medium-voltage opportunity in petrochemical, mining, and data-center clusters. Commodity cost volatility and lengthy public-utility approval cycles temper near-term margins, but the policy focus on supply-chain resilience continues to anchor long-run investment appetite within the Saudi Arabia switchgear market.

Key Report Takeaways

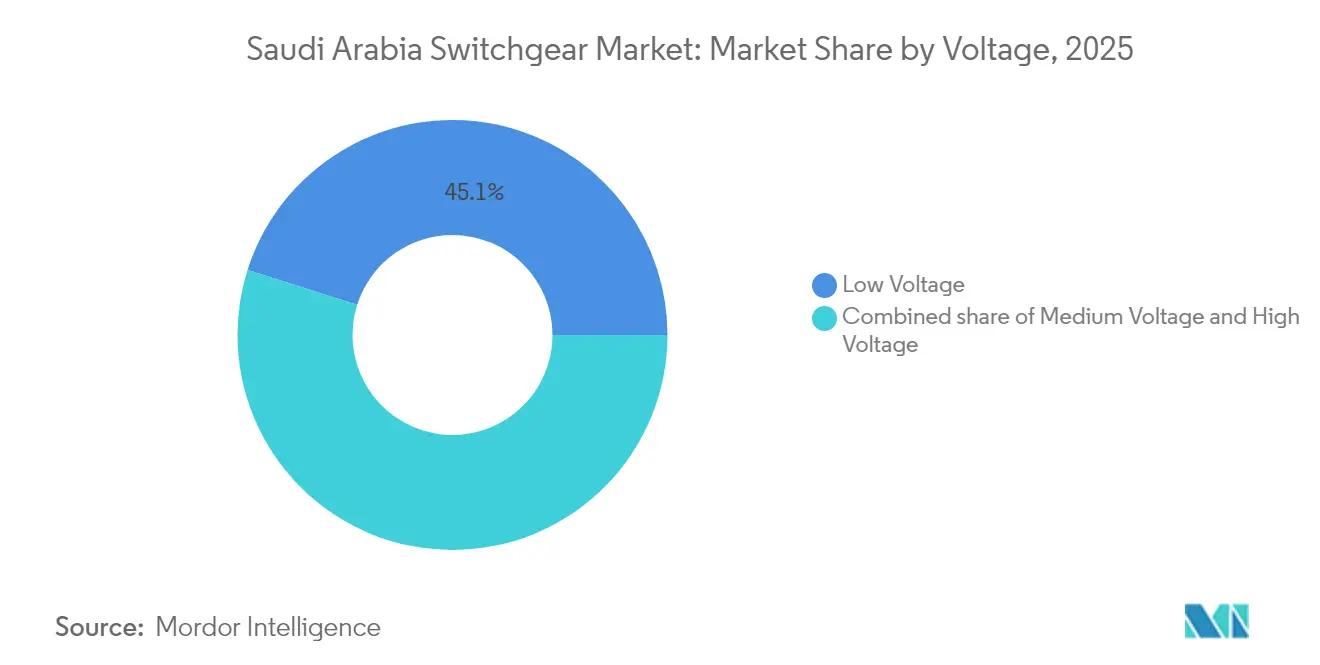

- By voltage, low-voltage switchgear led the market with a 45.12% share in Saudi Arabia in 2025, while high-voltage equipment is poised for the fastest growth, with a 7.74% CAGR through 2031.

- By insulation type, air-insulated units accounted for a 64.71% share of the Saudi Arabia switchgear market size in 2025; the "Others" category, centered on SF₆-free designs, is expected to expand at a 13.95% CAGR by 2031.

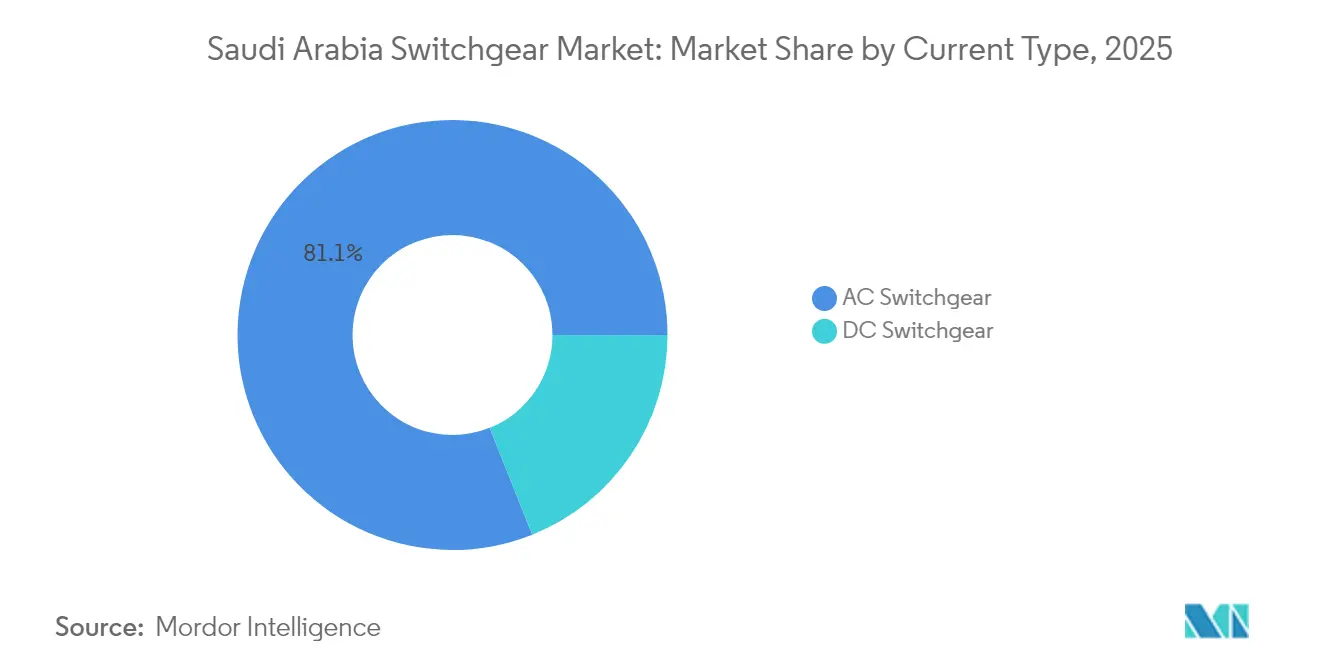

- By current type, AC assemblies dominated the Saudi Arabia switchgear market, with an 81.05% share in 2025. Meanwhile, DC configurations are expected to progress at a 6.83% CAGR through 2031.

- By installation, indoor systems captured 75.62% of Saudi Arabia's switchgear market size in 2025, and outdoor systems are projected to advance at an 8.5% CAGR through 2031.

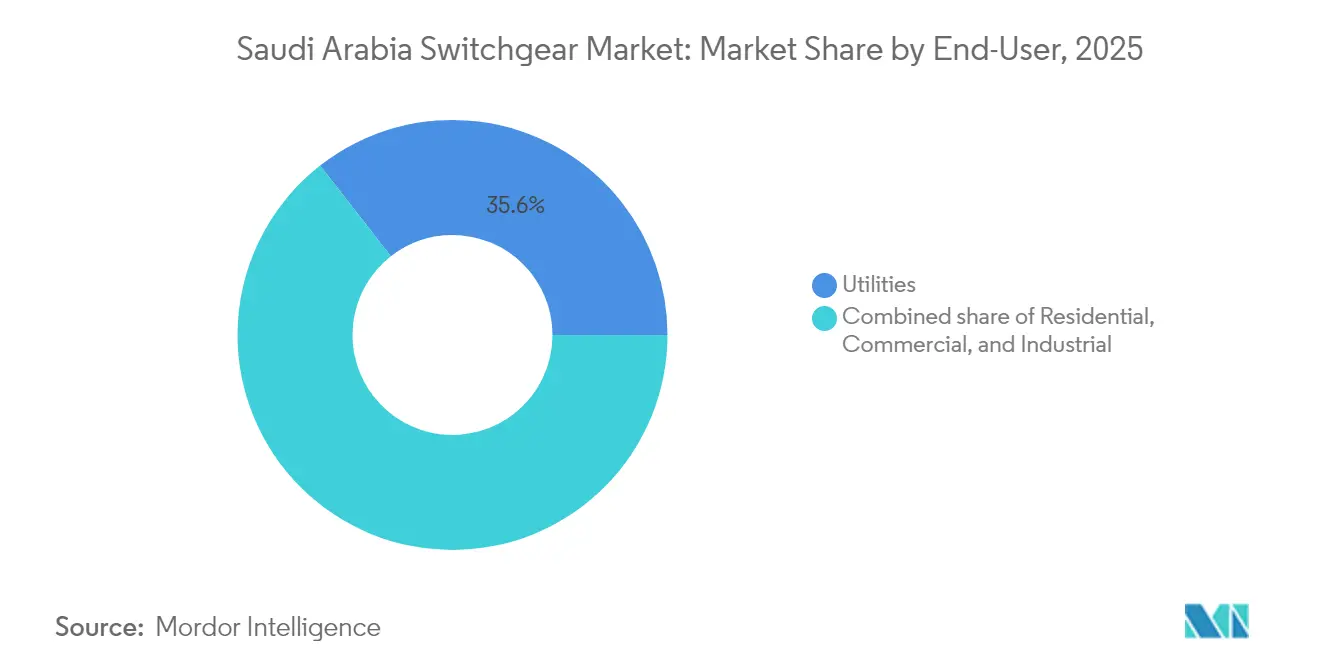

- By end-user, utilities represented 35.56% of Saudi Arabia's switchgear market share in 2025 and also headline growth at a 6.44% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Switchgear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of utility-scale renewables under Vision 2030 | +1.8% | National, with early gains in NEOM, Tabuk, Al Jouf | Medium term (2-4 years) |

| Growing power demand from industrial & commercial sectors | +1.2% | National, concentrated in Eastern Province, Riyadh, Jeddah | Short term (≤ 2 years) |

| Grid-modernisation investments by SEC & National Grid SA | +1.1% | National grid infrastructure, priority on 132kV-380kV networks | Medium term (2-4 years) |

| Government-backed T&D upgrades across 69 kV-380 kV network | +0.9% | National, focusing on interconnection between regions | Long term (≥ 4 years) |

| Electrification of giga-projects (NEOM, Red Sea, Qiddiya) | +0.7% | NEOM (Tabuk), Red Sea (Makkah), Qiddiya (Riyadh) | Long term (≥ 4 years) |

| Shift toward eco-efficient SF₆-free switchgear | +0.4% | Global, with early adoption in industrial zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Utility-Scale Renewables Under Vision 2030

Saudi Arabia targets 58.7 GW of renewables by 2030, triggering concentrated demand for 380 kV gas-insulated bays at bulk-supply substations serving remote desert solar and wind sites. Each new 380 kV facility needs three to five GIS bays, favoring compact footprints where land is scarce and ambient temperatures exceed 50 °C. Renewables also prompt utilities to adopt IEC 61850-enabled digital protection, which manages bidirectional flows and voltage fluctuations, as illustrated by ABB’s UniSec Digital launch, tailored for variable generation.[1]ABB Ltd., “UniSec Digital Switchgear Datasheet,” abb.com These factors collectively increase the complexity of high-voltage switchgear specifications and accelerate procurement within the Saudi Arabia switchgear market.

Growing Power Demand from Industrial & Commercial Sectors

Industrial electricity usage rose 8.3% in 2024, outpacing residential loads and concentrating switchgear demand in petrochemical hubs, mining districts, and emergent data-center corridors. Manufacturing localization under NIDLP has given rise to clusters around Riyadh and Jeddah that feature redundant medium-voltage gear with higher short-circuit ratings. EV-battery and semiconductor plants introduce harmonic-rich profiles mandating advanced filtering and rapid fault clearing. Commercial smart-city projects now require intelligent low-voltage boards that integrate energy management for LEED certification, expanding the low-voltage share of the Saudi Arabia switchgear market.

Government-Backed T&D Upgrades Across 69 kV-380 kV Network

Standardizing distribution at 132 kV will eliminate aging 69 kV lines and necessitate more than 200 substation retrofits between 2025-2030. Each retrofit includes smart-grid-ready switchgear capable of automated fault localization, cutting outage duration by 60%. Voltage optimization aligns with Vision 2030 milestones, creating predictable tender cycles that allow manufacturers to streamline local production inside the Saudi Arabia switchgear market.

Grid-Modernization Investments by SEC & National Grid SA

The Saudi Electricity Company has earmarked SAR 60 billion for upgrades, allocating 40% of the funds to automation and switchgear replacement across its 132 kV-220 kV assets. Compact GIS units cut substation footprints by up to 70%, enabling capacity growth in urban centers. National Grid SA plans to construct 12 new 380 kV stations by 2027 to reinforce inter-regional corridors. Cybersecurity mandates now require IEC 62351 compliance, prompting premium demand for switchgear with embedded security as utilities safeguard their critical infrastructure, thereby strengthening the Saudi Arabia switchgear market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent environmental & safety regulations | -0.8% | National, with stricter enforcement in industrial zones | Short term (≤ 2 years) |

| Volatile copper & steel prices | -0.6% | Global supply chain impact, affecting all regions | Short term (≤ 2 years) |

| Lengthy approval cycles within state-owned utilities | -0.4% | National, particularly affecting SEC and National Grid SA projects | Medium term (2-4 years) |

| Dependence on expatriate technical workforce | -0.3% | National, with higher impact in specialized HV installations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Environmental & Safety Regulations

Saudi Arabia adopted RoHS-aligned rules in 2024, obligating SF₆ leak detection and quarterly monitoring above 72.5 kV, which adds 12-15% to the lifecycle cost of GIS assets.[2]Saudi Standards, Metrology and Quality Organization, “RoHS Implementation Guidelines 2024,” saso.gov.sa Industrial zone audits by the Royal Commission for Jubail and Yanbu can delay approvals by up to six months if the documentation falls short. Firms offering vacuum or fluoronitrile alternatives gain an edge but face higher upfront costs that strain budgets across the Saudi Arabia switchgear market.

Volatile Copper & Steel Prices

Copper and steel price swings of 35% and 28% respectively, in 2024 disrupted switchgear cost baselines and lengthened delivery by as much as eight weeks. Domestic steel capacity cushions local producers, yet imported copper keeps high-voltage gear exposed to global shocks. Utilities now incorporate price-adjustment clauses into contracts, complicating tender comparisons and squeezing smaller vendors within the Saudi Arabia switchgear industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Voltage: Transmission Builds Propel High-Voltage Gains

High-voltage equipment is expected to grow at a 7.74% CAGR, as SEC’s tenders indicate that 60% of 2024 specifications will be at 132 kV or higher. Low-voltage retains its leadership at a 45.12% share due to construction, but growth tapers as centralized distribution models become more widespread. Digital relaying via IEC 61850 is now compulsory for new high-voltage bays, while medium-voltage lines serve industrial users demanding 30 kA interruption capability. Taken together, the segment composition underscores how transmission reinforcement shapes procurement within the Saudi Arabia switchgear market.

Grid hardening relocates desert solar output to load centers, prompting utilities to favor gas-insulated breakers rated at 380 kV that can withstand dust storms without derating. In parallel, commercial construction sustains low-voltage panel demand, but building-code evolution toward ring-main configurations flattens volume growth. Medium-voltage packages bridge both, supplying newly licensed factories under NIDLP mandates. These intertwined dynamics illustrate a balanced yet transmission-tilted opportunity pool in the Saudi Arabia switchgear market.

By Insulation: SF₆-Free Designs Accelerate

Air-insulated assemblies held a 64.71% share in 2025, primarily due to lower capital expenditures and operator familiarity. Yet “Others,” including vacuum, solid, and fluoronitrile mixtures, advance at 13.95% CAGR as utilities seek greenhouse-gas reductions that align with Saudi Green Initiative targets. Hitachi Energy’s pilot GIS with a fluoronitrile blend logged its first commercial orders in 2025, offering 80% footprint savings compared to AIS while eliminating SF₆ emissions. Vacuum interrupters now achieve 30,000 mechanical cycles, reducing maintenance calls by one-third and enhancing total life-cycle cost competitiveness in the Saudi Arabia switchgear market.

Eaton’s solid-insulated switchgear penetrates data center halls where fire safety codes prohibit gas installations, providing a non-flammable, arc-resistant option. Utilities weigh higher upfront costs against regulatory clarity and potential carbon fees, tilting the long-term preference toward SF₆-free systems. Consequently, the choice of insulation is evolving from a purely economic consideration to a strategic carbon-management consideration across the Saudi Arabia switchgear market.

By Current Type: DC Momentum Builds Under AC Dominance

AC maintains an 81.05% share due to its grid architecture, yet DC units clock a 6.83% CAGR as battery-energy-storage contracts require low-voltage DC breakers with rapid cut-off times of less than 5 ms. SEC’s 1,000 MW Tabuk and Hail BESS procurements require modular DC switchboards rated 1,500 V for containerized battery racks. High-power EV charging stations at 800 V also create a nascent urban DC segment. Suppliers are now adapting vacuum interrupter technology for 25 kA DC ratings, positioning themselves for the next investment wave in the Saudi Arabia switchgear market.

Industrial estates pilot DC microgrids to reduce conversion losses, but adoption remains in its early stages. Long-distance HVDC lines are under feasibility review to transport western solar output eastward; should the projects proceed, demand may surge for 500 kV DC breakers, which are currently in limited global supply. AC’s dominance will remain for the decade, yet line-item DC growth elevates diversification prospects for specialized vendors within the Saudi Arabia switchgear industry.

By Installation: Outdoor Assemblies Gain Traction

Indoor switchgear captured 75.62% of the 2025 revenue due to its reliability in climate-controlled rooms. Outdoor gear, however, experiences an 8.5% CAGR as remote solar plants, wind farms, and backbone transmission corridors opt for prefabricated skid-mounted units, which reduce civil works by 30%. Composite-insulator and polymer-housed designs withstand sandstorms and 50°C heat, thereby reducing derating risks. Cost-sensitive public tenders often favor outdoor units, influencing capital allocations within the Saudi Arabia switchgear market.

Urban planners still favor indoor GIS for aesthetic and noise control purposes. Yet, suburban distribution nodes increasingly deploy compact outdoor RMUs that halve installation time. Manufacturers refine ingress-protection seals and anti-corrosion coatings to extend the mean time between failures beyond 35 years, thereby enhancing total asset value. The contrasting requirements foster parallel demand channels that sustain healthy growth in the Saudi Arabia switchgear market.

By End-User: Utilities Drive Both Volume and Innovation

Utilities controlled 35.56% of the 2025 spend and are expected to expand by a 6.44% CAGR as the SEC upgrades 150 substations under its ongoing capital expenditure plan. Tender documents now stipulate local-content quotas, encouraging joint ventures between global OEMs and domestic firms such as Electrical Industries Company, which signed SAR 785.5 million contracts in September 2025. Industrial consumers hold the next-largest slice; petrochemical plants in Jubail specify arc-resistant medium-voltage gear to protect personnel and maintain uptime. Residential and commercial builders maintain steady low-voltage orders, while smart-building mandates shift attention to intelligent metering and predictive maintenance interfaces.

Giga-project developers, such as NEOM and Qiddiya, represent a hybrid buyer profile: they source high-voltage backbone equipment as utilities, while demanding building-level low-voltage panels for mixed-use zones. Independent Power Producers, newly empowered by PPA frameworks, tender switchgear that meets stringent availability guarantees. Collectively, these segments form a diversified book of demand sustaining innovation cycles in the Saudi Arabia switchgear market.

Geography Analysis

Regional demand patterns mirror Saudi Arabia’s economic map. The Eastern Province dominates industrial orders, leveraging petrochemical, LNG, and steel complexes that specify medium- and high-voltage gear capable of interrupting 40 kA faults. Saline air and petrochemical fumes necessitate corrosion-resistant enclosures, which add 10% cost premiums yet ensure reliability over 35 years of service. The region’s proximity to domestic steel mills partially shields manufacturers from global commodity shocks, stabilizing pricing inputs in the Saudi Arabia switchgear market.

Riyadh’s Central Region shapes commercial and government demand. Mega-projects such as New Murabba and King Salman Park generate thousands of low-voltage feeders and ring-main units. Space constraints in high-rise zones favor compact gas-insulated switchboards, despite the elevated capital expenditure. Simultaneously, the region’s industrial suburbs are pursuing medium-voltage installations for EV manufacturing and food-processing plants, thereby widening the voltage mix procured within the Saudi Arabia switchgear market size.

The Western Province blends tourism-centric Red Sea resorts with urban densities in Jeddah. Coastal humidity drives the preference for stainless-steel enclosures, and premium land values justify the adoption of GIS in 33 kV distribution. The NEOM development in Tabuk extends the western footprint northward, specifying more than 200 digital substations that integrate 380 kV-rated backbone lines with 11 kV smart-city feeders. Northern territories, which have long been underserved, are now investing in high-voltage GIS for wind corridors, elevating their regional share from low single digits to a mid-teens contribution by 2030. These shifts distribute growth more evenly nationwide and moderate historical over-reliance on the Eastern Province within the Saudi Arabia switchgear market.

Competitive Landscape

The market exhibits moderate concentration, with the top five players accounting for approximately 55% of revenue, striking a balance between proprietary technology and localization incentives. ABB, Siemens, and Schneider Electric dominate the digital and high-voltage niches, often partnering locally; Schneider inaugurated an LV/MV assembly line at King Salman Energy Park in 2025. Alfanar and Electrical Industries Company utilize domestic fabrication and preferential procurement clauses to bid on medium-voltage tenders. Hitachi Energy’s JV with PIF and SEC to produce SF₆-free GIS underscores the policy-backed drive to embed advanced technology in Saudi supply chains.

Strategically, vendors differentiate through compliance with IEC 61850, cybersecurity certifications, and SF₆-free roadmaps. Service portfolios now bundle condition-monitoring and digital twins, locking in post-sale revenue streams. Commodity volatility forces quarterly price negotiations; firms with hedged supply contracts maintain margin stability. White-space opportunities persist in DC-rated switchgear, distributed BESS integration, and arc-flash mitigation, where local portfolios remain thin, leaving room for new entrants. Overall, rivalry pivots on simultaneous localization and technology leadership, defining value capture within the Saudi Arabia switchgear market.

Saudi Arabia Switchgear Industry Leaders

ABB Ltd.

Siemens AG

Eaton Corporation Plc.

Hitachi Energy Ltd.

Schneider Electric SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Electrical Industries Company subsidiaries WESCOSA and Saudi Transformers Company have signed a SAR 785.5 million supply agreement with the Saudi Electricity Company for distribution substations over a 19-month period.

- March 2025: Energy Capital Group’s ECG2.0-Fund2 acquired Dar Al Balad Contracting, enhancing electrical and instrumentation capabilities ahead of a planned Tadawul IPO.

- March 2025: Saudi Power Transformers Company secured a SAR 129.3 million transformer supply contract for the Ras Tanura Development.

- February 2025: Elsewedy Electric won a 110/13.8 kV substation contract in Jeddah, reinforcing urban grid capacity.

Saudi Arabia Switchgear Market Report Scope

Switchgear is a piece of equipment that is used to protect circuits from fault currents and control the way power is sent to larger areas. Voltage, insulation, and end-user are the key market segments for switchgear in Saudi Arabia. The Saudi Arabia Switchgear Market is segmented by Voltage (Low-Voltage, Medium-Voltage, High Voltage), Insulation (Gas-Insulated Switchgear, Air-Insulated Switchgear), and End-User Industry (Commercial, Residential, and Industrial). The report offers the market size and forecasts for the switchgear market in terms of revenue (USD) for all the above segments.

| Low Voltage |

| Medium Voltage |

| High Voltage |

| Gas Insulated Switchgear (GIS) |

| Air Insulated Switchgear (AIS) |

| Others |

| AC Switchgear |

| DC Switchgear |

| Indoor |

| Outdoor |

| Utilities |

| Residential |

| Commercial |

| Industrial |

| By Voltage | Low Voltage |

| Medium Voltage | |

| High Voltage | |

| By Insulation | Gas Insulated Switchgear (GIS) |

| Air Insulated Switchgear (AIS) | |

| Others | |

| By Current Type | AC Switchgear |

| DC Switchgear | |

| By Installation | Indoor |

| Outdoor | |

| By End-User | Utilities |

| Residential | |

| Commercial | |

| Industrial |

Key Questions Answered in the Report

How large is the Saudi Arabia switchgear market in 2026?

The market is valued at USD 2.67 billion in 2026 with a projected 5.94% CAGR to 2031.

Which voltage class is expanding fastest?

High-voltage switchgear rated 132 kV-380 kV is advancing at a 7.74% CAGR due to transmission backbone upgrades.

What insulation technology is gaining traction?

SF₆-free alternatives such as vacuum and fluoronitrile GIS are set for a 13.95% CAGR amid tighter environmental rules.

Who are the leading players?

ABB, Siemens, Schneider Electric, Alfanar, and Electrical Industries Company together command about 55% of revenue.

Which end-user segment drives demand?

Utilities lead with a 35.56% share and will grow at 6.44% CAGR as SEC modernizes 150 substations.

What is the main restraint affecting pricing?

Volatility in copper and steel prices, with swings up to 35% in 2024, strains budgeting and delivery timelines.

Page last updated on: