Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 13.49 Billion |

| Market Size (2026) | USD 14.20 Billion |

| Market Size (2031) | USD 17.84 Billion |

| Growth Rate (2026 - 2031) | 4.67% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Power EPC Market Analysis by Mordor Intelligence

The Saudi Arabia Power EPC Market size is expected to grow from USD 13.49 billion in 2025 to USD 14.20 billion in 2026 and is forecast to reach USD 17.84 billion by 2031 at 4.67% CAGR over 2026-2031.

This steady uptick is anchored by Vision 2030’s 100–130 gigawatt renewable-capacity goal, the accelerating build-out of grid links, and a sovereign wealth–backed procurement model that shields developers from commercial-lending stress.[1]PowerChina, “International Projects,” powerchina.cn Public and private sponsors alike rely on engineering-procurement-construction (EPC) firms to deliver an annual installation pace above 20 gigawatts from 2025, driving both generation and transmission awards. Contractors diversify by pairing large solar and wind farms with battery storage, while industrial off-takers commission captive microgrids that bypass permitting bottlenecks. Competition splits along technology lines: Korean and Chinese firms win price-driven bids, whereas European OEMs monetize long-term service contracts that guarantee stable cash flows.

Key Report Takeaways

- Saudi Arabia's power EPC market is segmented into power generation EPC and power transmission and distribution (T&D) EPC. Power generation EPC accounted for 51.96% of the market in 2025, and is projected to grow at a 4.82% CAGR through 2031.

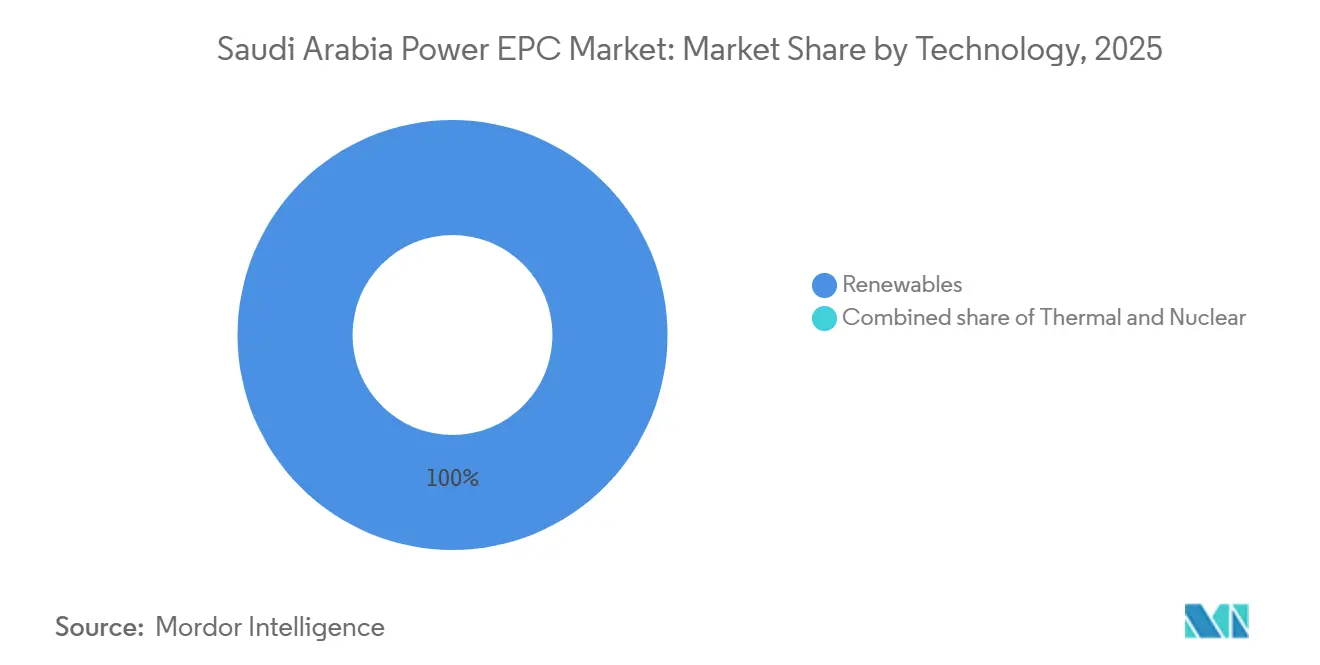

- By technology, renewables commanded the entire 2025 tender pipeline of Saudi Arabia's power generation EPC market and are projected to expand at a 4.8% CAGR to 2031.

- By capacity band, plants above 500 megawatts captured 61.5% of Saudi Arabia's power generation EPC market share in 2025.

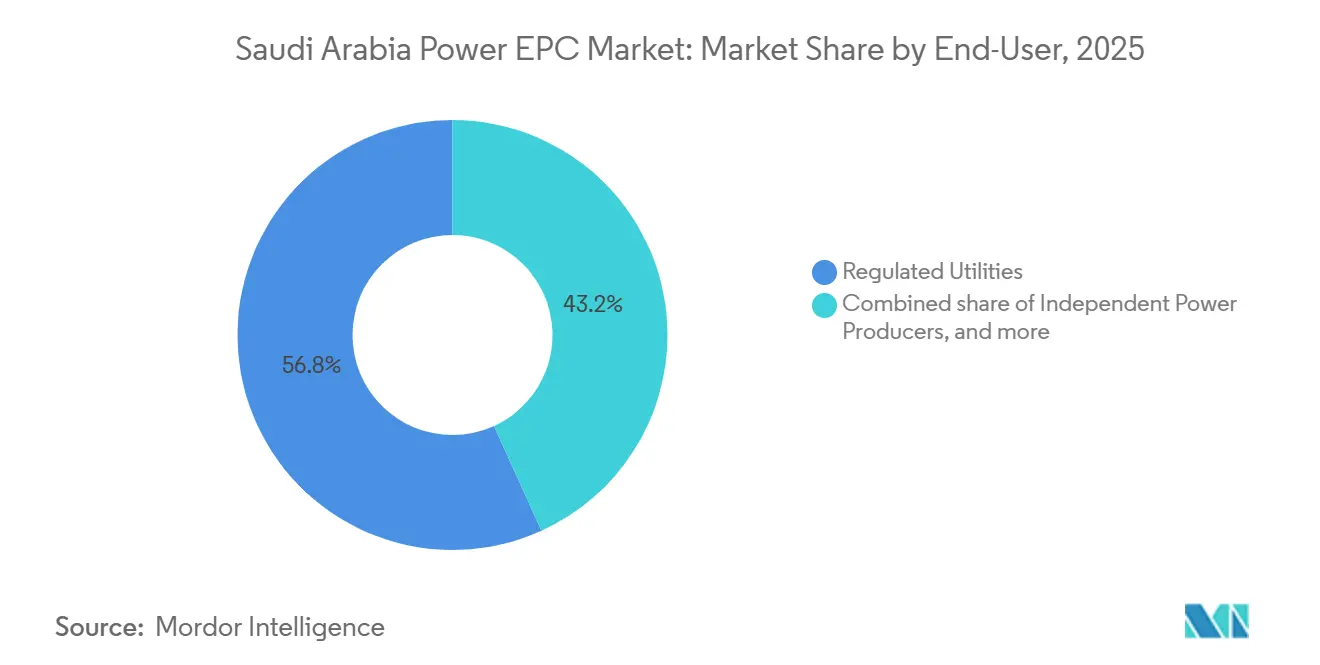

- By end-user, regulated utilities accounted for 56.8% of Saudi Arabia's power generation EPC market, while independent power producers are poised to grow at 5.7% annually to 2031, outpacing regulated utilities.

- By geography, the Northern Border–Tabuk solar corridor led with 40% of Saudi Arabia's power EPC market size in 2025.

- ACWA Power, PowerChina, and Doosan Enerbility together held a 35% Saudi Arabia power EPC market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Power EPC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 capacity-addition roadmap | +1.2% | Northern Border, Tabuk, Eastern Province | Long term (≥ 4 years) |

| National Renewable Energy Program pipeline | +1.0% | All regions | Medium term (2–4 years) |

| Rapid industrial-sector electricity demand | +0.8% | Jubail, Ras Al Khair, Jazan, Wa’ad Al Shamal | Medium term (2–4 years) |

| Grid modernisation & cross-border links | +0.6% | National backbone, Egypt and GCC interconnectors | Long term (≥ 4 years) |

| Local-content mandates for EPC contractors | +0.4% | Kingdom-wide through IKTVA | Short term (≤ 2 years) |

| Green-hydrogen mega-projects | +0.5% | NEOM, Ras Al Khair | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Capacity-Addition Roadmap

Saudi Arabia raised its renewable target to 100–130 gigawatts by 2030, a leap that requires more than 20 gigawatts of fresh capacity each year, a rate triple the cumulative 6.55 gigawatts installed before 2025. The Public Investment Fund–backed ACWA Power secured seven PPAs in July 2025 totaling 15 gigawatts, proving that sovereign balance sheets can absorb large awards without auction delays. Record solar bids of USD 0.0129 per kilowatt-hour at the 2-gigawatt Al-Sadawi plant illustrate continuing cost deflation. Yet with only 14.4 gigawatts tendered to date, policymakers must contract at least 70 gigawatts in five years to meet the low end of the target range, underscoring the urgency for streamlined permitting.

National Renewable Energy Program Pipeline

Round 5 of the National Renewable Energy Program pre-qualified 33 bidders for a 2-gigawatt battery-storage tender, bundling storage and solar into one EPC scope that favors integrated suppliers.[2]International Monetary Fund, “Saudi Arabia: 2024 Article IV Consultation,” imf.org PowerChina alone won 1.75 gigawatts of solar EPC in January 2025, while China Energy Engineering Corporation secured the 2-gigawatt Haden plant for USD 976 million in 2024, confirming Chinese dominance in price-competitive utility-scale projects.[3]ACWA Power, “Al-Sadawi Solar Bid,” acwapower.com The phased auction schedule mitigates execution risk, but parallel construction of multiple sites strains welders, electricians, and logistically critical crane operators.

Rapid Industrial-Sector Electricity Demand Growth

Mining, petrochemicals, and gas-processing expansions in Jubail, Ras Al Khair, and Yanbu push industrial loads beyond household demand. Ma’aden’s capital plan allocates up to SAR 9.55 billion (USD 2.55 billion) for growth projects in 2025, much of it for captive substations. Saudi Aramco’s Al Jafurah field adds compressor stations that require multi-megawatt onsite generation. These industrial clusters gravitate toward projects above 500 megawatts for scale economies while remote sites adopt sub-100 megawatt microgrids.

Grid-Modernisation & Inter-Connection Investments

The Saudi Electricity Company’s smart-grid roadmap rolls out automated substations, advanced meters, and high-voltage direct-current (HVDC) backbones. Hyundai E&C is building a 1,089-kilometer, 4,000-megawatt HVDC link between Kudmi and Riyadh for USD 725 million. Hitachi Energy began commissioning the 3-gigawatt Saudi–Egypt interconnector in January 2026, a precursor to an Arab Mashreq grid. Regionally, the GCC Interconnection Authority committed USD 3.5 billion to new links, further lifting transmission EPC demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy permitting & approval cycles | -0.5% | National, with bottlenecks in environmental and land-use clearances | Short term (≤ 2 years) |

| Shortage of specialised EPC labour & skills | -0.7% | National, acute in welding, high-voltage electrical, and commissioning trades | Medium term (2-4 years) |

| Volatile steel & equipment prices | -0.3% | National, with Eastern Province industrial clusters most exposed to input-cost fluctuations | Short term (≤ 2 years) |

| Cooling-water scarcity for thermal plants | -0.2% | Eastern Province coastal sites and inland CCGT plants requiring desalination integration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lengthy Permitting & Approval Cycles

Environmental assessments, land leases, and interconnection sign-offs can stretch 12–18 months. The 2025 Investment Law promises streamlined dispute resolution, but developers have yet to record faster approvals. While the Etimad e-procurement portal pays 83% of invoices within 15 days, licensing delays continue to slow multi-gigawatt auctions.

Shortage of Specialised EPC Labor & Skills

Sixty percent of global energy firms report hiring trouble, with electricians and welders hardest to source. Saudization targets set 75% local employment in energy, but rapid project scaling still forces contractors to import skilled workers from South Asia, risking compliance penalties. ABB’s 2026 training academy will help, but labor tightness could linger through 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Renewable Tenders Monopolize Competitive EPC

Renewables took 100% of new capacity awards in 2025, and the segment is forecast to rise at a 4.8% CAGR to 2031. This dominance stems from a policy that channels Saudi Power Procurement Company auctions solely to solar and wind, while thermal plants proceed under direct awards. ACWA Power alone commissioned 2.79 gigawatts of solar in 2025 across Al Kahfah, Ar Rass 2, and Saad 2. Although excluded from competitive tenders, combined-cycle gas turbine builds such as the 3.6-gigawatt Rumah 2 project ensure reserve margin stability. Siemens Energy booked USD 1.6 billion of orders for Rumah 2 and Nairiyah 2 in March 2025, bolstering the Saudi Arabia power EPC industry’s thermal backlog.[4]Saudi Electricity Company, “Corporate Information,” se.com.sa

Second-order effects include rising demand for grid-connected batteries, with Round 5 bundling 2 gigawatts of storage across four sites. Competitive tariffs below USD 0.013 per kilowatt-hour indicate that integrated solar-plus-storage EPC achieves economies that non-integrated vendors cannot match. If execution stays on schedule, renewables will continue to shape the Saudi Arabia power generation EPC market size over the forecast period.

By Capacity Band: Utility-Scale Dominates, Yet Microgrids Surge

Projects above 500 megawatts captured 61.5% of 2025 power generation EPC spending, led by ACWA Power’s 1.425-gigawatt Al Kahfah solar farm. High capacity factors and centralized procurement cut levelized costs, favoring mega-scale plants. The 100–499 megawatt bracket serves regional utilities and industrial clusters, often integrating 250-megawatt storage blocks.

The up-to-100 megawatt segment, though smaller in absolute value, is the fastest-growing at 6.1% through 2031. NEOM’s hydrogen facility uses modular sub-100 megawatt arrays aligned with electrolyzer ramps. The Red Sea Development Company operates a 400-megawatt microgrid with 1.3 gigawatt-hours of batteries, proving that distributed resources can power isolated assets. These projects confirm that microgrids will steadily enlarge their Saudi Arabia power generation EPC market share.

By End-User: IPPs Outpace Utilities as Liberalization Accelerates

Regulated utilities controlled 56.8% of 2025 spending, yet independent power producers (IPPs) are forecast to expand 5.7% annually to 2031. ACWA Power’s SAR 31 billion worth of PPAs in 2025 illustrate the IPP growth path, while Korea Electric Power Corporation’s joint ventures in combined-cycle gas projects show foreign utilities favor equity stakes over equipment sales. Industrial captive power also rises as Ma’aden invests SAR 7.55–9.55 billion in generation to secure tariff certainty.

Power Transmission and Distribution EPC: Smart Grids and Cross-Border Links

Transmission and distribution EPC represented USD 6.81 billion in 2026 and is poised to reach USD 8.49 billion in 2031. Hyundai E&C’s Kudmi–Riyadh HVDC line and Hitachi Energy’s Saudi–Egypt link exemplify the shift toward long-distance, high-capacity corridors. Regionally, the GCC Interconnection Authority’s USD 3.5 billion plan fosters a meshed Gulf grid. On the distribution side, Saudi Electricity Company aims for nationwide smart-meter coverage by 2028 to unlock demand-response tariffs.

Geography Analysis

Northern Border and Tabuk lead the renewable build-out thanks to the kingdom’s best solar irradiance and steady wind patterns. ACWA Power’s 1.425-gigawatt Al Kahfah project and the 400-megawatt Dumat Al Jandal wind farm deliver capacity factors 15–20% above national averages, entrenching the region as a cost-leader. Hyundai E&C’s 4,000-megawatt Kudmi–Riyadh HVDC line unlocks an added 10–15 gigawatts of stranded northern potential.

The Eastern Province anchors heavy-industry demand. Jubail, Ras Al Khair, and Dammam absorb over 30% of national electricity, spurring large gas-fired builds and captive substations. Siemens Energy’s Dammam plant rolled out the first Saudi-built H-class turbine in 2025, while the Saudi–Egypt interconnector terminates near Dammam, positioning the area as a future export hub.

NEOM and the Red Sea coast form an emerging green-hydrogen and tourism corridor. NEOM’s 4 gigawatts of captive renewables and the Red Sea Development Company’s 400-megawatt microgrid rely on distributed architectures suited to phased developments. Although eventual GCC links will integrate these coastal loads, present EPC work focuses on islanded systems that can be expanded module by module.

Competitive Landscape

The Saudi Arabia power EPC market shows moderate concentration, with the top five firms controlling roughly 45% of 2025 awards. PowerChina, China Energy Engineering Corporation, and Doosan Enerbility dominate price-sensitive solar, wind, and thermal packages, respectively, while Siemens Energy and GE Vernova anchor OEM-tied service contracts. Alfanar exploits local-content rules to win battery-storage integration, partnering with BYD and HiTHIUM for 4 gigawatt-hours of capacity. Sungrow’s 7.8-gigawatt-hour Najran-cluster system, switched on in December 2025, demonstrates Chinese suppliers’ scale advantage in lithium-iron-phosphate cells.

Financially robust consortia gain traction under the Private Sector Participation Law, which shifts construction and operational risk to contractors. Access to long-term Islamic finance and sovereign guarantees further tilts the field toward large incumbents. Smaller local firms thrive in substation fabrication and low-voltage works but rarely lead multi-gigawatt bids.

Saudi Arabia Power EPC Industry Leaders

ACWA Power

Saudi Electricity Co. – NCC

Larsen & Toubro

PowerChina

Doosan Enerbility

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Sungrow energized a 7.8-gigawatt-hour battery system across Najran, Khamis Mushait, and Madaya.

- October 2025: PowerChina and Energy China booked USD 4.3 billion of EPC for 3 gigawatts of wind and several solar sites.

- August 2025: ACWA Power, SEC, and KEPCO achieved financial close on the 3.6-gigawatt Rumah 1 and Nairiyah 1 CCGT projects.

- July 2025: ACWA Power signed seven PPAs totaling 15 gigawatts with SPPC.

- March 2025: Siemens Energy secured USD 1.6 billion in CCGT turbine orders for Rumah 2 and Nariyah 2.

Saudi Arabia Power EPC Market Report Scope

The power EPC market encompasses the global industry of companies that provide comprehensive execution of power generation, transmission, and distribution projects on a turnkey basis. EPC contractors handle engineering design, equipment procurement, construction, installation, testing, and commissioning of power infrastructure, ensuring project delivery aligns with agreed cost, time, and performance requirements.

The Saudi Arabia power EPC market is segmented into power generation EPC and power transmission and distribution EPC. By power generation EPC, the market is segmented into technology, capacity band, and end-user. These segments are further divided as technology- thermal, nuclear, and renewables; capacity band- Up to 100 MW, 100-499 MW, Above 500 MW; end-user- regulated utilities, IPPs, industrial captive power, and public sector/SOE. For each segment, the market sizing and forecasts have been done based on revenue (USD Billion) for all the above segments.

Power Generation EPC

| By Technology | Thermal |

| Nuclear | |

| Renewables | |

| By Capacity Band | Up to 100 MW (DER, micro-grid) |

| 100 to 499 MW | |

| Above 500 MW | |

| By End-User | Regulated Utilities |

| Independent Power Producers | |

| Industrial Captive Power | |

| Public Sector and SOE |

| Power Generation EPC | By Technology | Thermal |

| Nuclear | ||

| Renewables | ||

| By Capacity Band | Up to 100 MW (DER, micro-grid) | |

| 100 to 499 MW | ||

| Above 500 MW | ||

| By End-User | Regulated Utilities | |

| Independent Power Producers | ||

| Industrial Captive Power | ||

| Public Sector and SOE | ||

Key Questions Answered in the Report

What is the current Saudi Arabia power EPC market size?

The Saudi Arabia power EPC market size stood at USD 14.20 billion in 2026 and is projected to reach USD 17.84 billion by 2031.

How fast is the Saudi Arabia power EPC market expected to grow?

Market value is forecast to rise at a 4.67% CAGR during 2026-2031, driven by Vision 2030 renewables and grid upgrades.

Which segment is expanding the quickest?

Distributed resources under 100 megawatts show the fastest growth at 6.1% through 2031, thanks to microgrids for hydrogen and tourism projects.

Who are the leading EPC contractors in Saudi Arabia?

Key players include ACWA Power, PowerChina, Doosan Enerbility, Siemens Energy, GE Vernova, and Alfanar, together holding roughly 45% of 2025 awards.

What role do battery systems play in new projects?

Over 5 gigawatts of storage tenders are live, with the 7.8 gigawatt-hour Najran project highlighting the scale and importance of batteries for grid stability.

How do local-content rules affect foreign contractors?

The IKTVA program compels international EPC firms to source locally or form joint ventures, influencing plant-equipment choices and job creation.

Page last updated on: