Home and Property Improvement

9th JuneA Leading Sanitaryware Company’s Journey in Saudi Arabia

4 Min Read

The Saudi Arabia Microwave Ovens Market Report is Segmented by Product (Solo, Grill, and More), Structure (Countertop, Built-In, and More), Control Feature (Button Controls, and Dial Controls), Capacity (Up To 19 Litres, 20 To 24 Litres, and More), Application (Residential, and Commercial), Distribution Channel (B2C, and B2B), Geography (Western, Central, and More). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

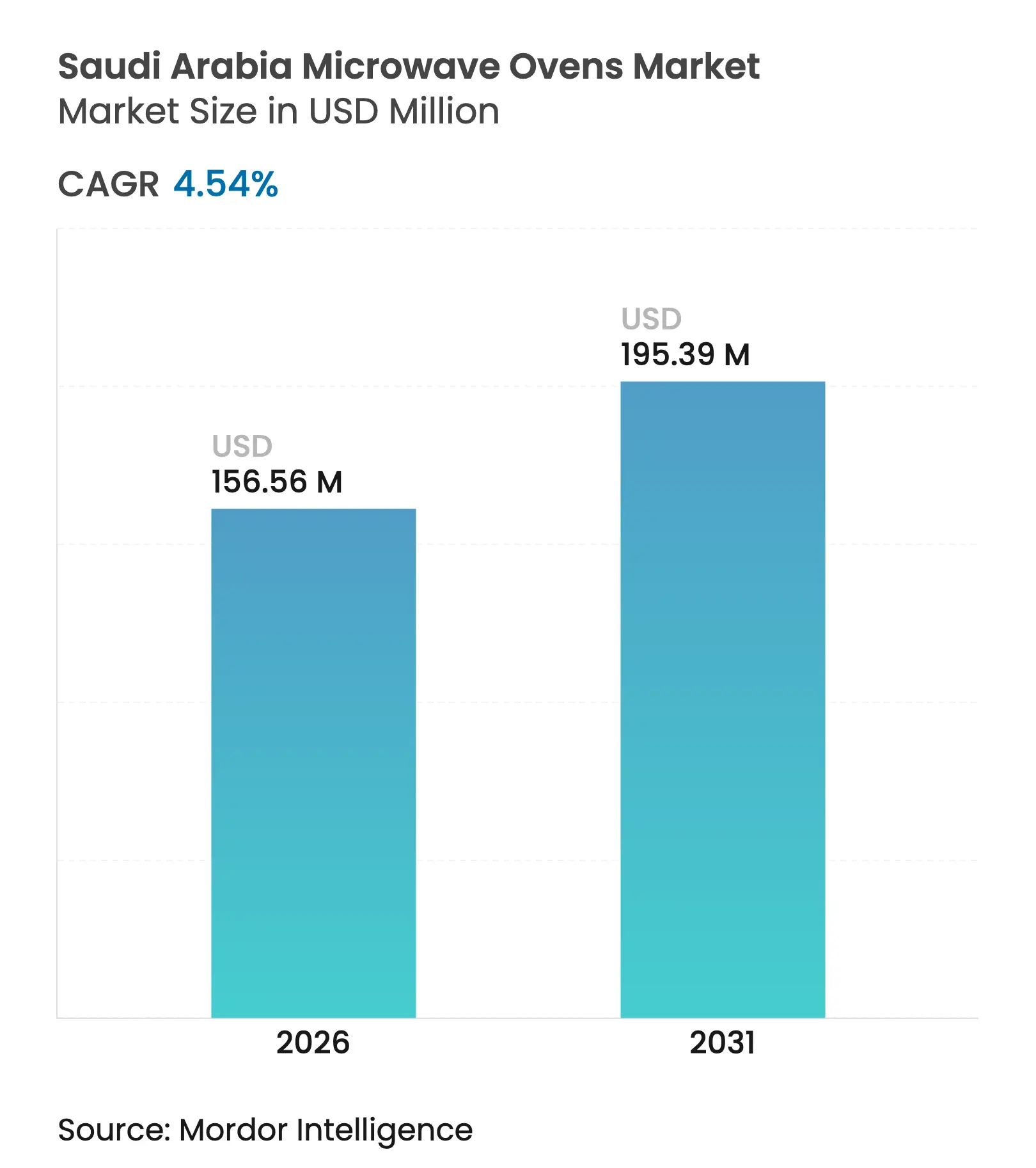

| Market Size (2026) | USD 156.56 Million |

| Market Size (2031) | USD 195.39 Million |

| Growth Rate (2026 - 2031) | 4.54 % CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Saudi Arabia microwave ovens market size was valued at USD 149.76 million in 2025 and estimated to grow from USD 156.56 million in 2026 to reach USD 195.39 million by 2031, at a CAGR of 4.54% during the forecast period (2026-2031). The market growth is expected from the Vision 2030 reforms that lift disposable incomes, accelerate residential building approvals, and incentivize digital payment adoption. Convection units lead product demand as households embrace appliances that blend traditional cooking with fast-paced lifestyles. Countertop formats remain dominant, yet built-in models gain momentum in premium housing developments where space optimization and aesthetics matter. Supply chain localization efforts such as the Public Investment Fund-backed Alat initiative may gradually curb import reliance and reshape pricing as local production scales.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising dual-income nuclear households seeking convenience

cooking

Rising dual-income nuclear households seeking convenience

cooking

| +0.8% | National; highest in Central & Western regions | Medium term (2–4 years) |

(~) % Impact on CAGR Forecast

:

+0.8%

|

Geographic Relevance

:

National; highest in Central & Western regions

|

Impact Timeline

:

Medium term (2–4 years)

|

Government-backed housing initiatives under Vision 2030

Government-backed housing initiatives under Vision 2030

| +0.7% | National; early gains in Riyadh, Jeddah, NEOM | Long term (≥ 4 years) | |||

Rapid expansion of QSR & cloud kitchens boosting

commercial demand

Rapid expansion of QSR & cloud kitchens boosting

commercial demand

| +0.6% | Urban hubs, mainly Central & Western | Short term (≤ 2 years) | |||

Growing popularity of built-in kitchen concepts in premium

homes

Growing popularity of built-in kitchen concepts in premium

homes

| +0.5% | Central & Western high-income districts | Medium term (2–4 years) | |||

Innovation in energy-efficient inverter/air-fry models

Innovation in energy-efficient inverter/air-fry models

| +0.4% | National; premium uptake in major cities | Medium term (2–4 years) | |||

Surge in e-commerce flash-sales events

Surge in e-commerce flash-sales events

| +0.3% | National; urban skew | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Dual-Income Nuclear Households Seeking Convenience Cooking

Female labor participation gains under Vision 2030 shift household routines and elevate demand for quick-use appliances. These consumers prioritize energy-efficient models that align with Saudi Energy Efficiency Center guidelines cutting residential consumption by up to 70%.[1]Source: Saudi Energy Efficiency Center, “Building Code Guidelines,” seec.gov.sa Inverter platforms and air-fry functionality satisfy both healthy-eating goals and traditional recipe needs. Demand spreads fastest across Riyadh and Jeddah, where professional employment opportunities for women have risen sharply since 2024. Marketers underscore reliability and warranty coverage to attract families who seek durable solutions amid rising utility tariffs. As dual-income homes grow, repeat replacement cycles shorten, enlarging the Saudi Arabia microwave ovens market.

Government-Backed Housing Initiatives Under Vision 2030

Programs such as Wafi (off-plan sales) and Etmam (licensing streamlining) fast-track construction starts and feed appliance uptake at handover. Developers increasingly specify built-in kitchens, prompting consistent orders for integrated microwave ovens. The White Land program widens residential land supply, supporting appliance sales beyond premium neighborhoods. Policies that favor energy-efficient fittings dovetail with consumer interest in inverter technology, anchoring long-term growth for the Saudi Arabia microwave ovens market.

Rapid Expansion of QSR & Cloud Kitchens Boosting Commercial Demand

Quick service restaurant networks and cloud kitchens scale aggressively in major cities, propelling high-capacity ovens for rapid reheating. Payment ecosystems dominated by digital wallets and Buy Now Pay Later options streamline B2B procurement. Cloud operators favor compact yet powerful units that fit shared facilities while meeting volume surges tied to delivery platforms. Food-tech incumbents leverage IoT diagnostics to minimize downtime, reinforcing preference for globally recognized brands with established Saudi service partners. Commercial demand therefore adds momentum to the Saudi Arabia microwave ovens market through 2030.

Innovation in Energy-Efficient Inverter/Air-Fry Models

Lead brands cascade inverter engines across mid-range lines to trim power draw in a climate where cooling already dominates electricity bills. Samsung’s Bespoke AI range debuted deeper food-specific algorithms in 2025, promising precise heating cycles.[2]Source: Samsung Electronics, “KBIS 2025 Product Highlights,” news.samsung.com Air-fry features resonate with health-conscious millennials looking to cut oil yet retain familiar flavors. Multifunction adds value in smaller urban kitchens, encouraging replacement of older single-mode units. Sustained R&D investment by multinational OEMs ensures a steady rollout of energy-saving upgrades, reinforcing growth in the Saudi Arabia microwave ovens market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High import tariffs & SASO certification delays

High import tariffs & SASO certification delays

| -0.9% | Nationwide; price-sensitive tiers | Long term (≥ 4 years) |

(~) % Impact on CAGR Forecast

:

-0.9%

|

Geographic Relevance

:

Nationwide; price-sensitive tiers

|

Impact Timeline

:

Long term (≥ 4 years)

|

Volatility in global freight costs inflating retail prices

Volatility in global freight costs inflating retail prices

| -0.6% | Nationwide; import-heavy SKUs | Short term (≤ 2 years) | |||

Limited after-sales service network in tier-2 cities

Limited after-sales service network in tier-2 cities

| -0.4% | Tier-2 urban areas | Medium term (2–4 years) | |||

| Source: Mordor Intelligence | ||||||

High Import Tariffs & SASO Certification Delays

Microwave ovens shipped from outside the GCC attract 5% customs duty plus 15% VAT. Extra levies and port surcharges can lift shelf prices 20-25% above neighboring markets.[3]Source: U.S. International Trade Administration, “Saudi Arabia – Import Tariffs,” trade.gov The SABER portal requires every model to secure a conformity certificate, adding lead times of up to six months and raising compliance costs. Periodic tariff revisions—some lines rose to 25% in 2024—tighten margins for midsize importers. Smaller foreign brands struggle to absorb these expenses, deterring new entrants and tempering competitive pressure in the Saudi Arabia microwave ovens market.

Volatility in Global Freight Costs Inflating Retail Prices

Container rates on Asia–Red Sea lanes swung 40-60% in 2024. Importers faced higher working capital and hedging needs as spot pricing spiked after Suez disruptions. UPS emphasizes landed-cost contracts to cushion variance, but not all distributors secure similar terms. Price-sensitive shoppers defer upgrades when sticker shock exceeds budgets, particularly in mid-range segments. Retailers run leaner inventories to mitigate risk, reducing the breadth of on-hand SKUs and constraining choice across the Saudi Arabia microwave ovens market.

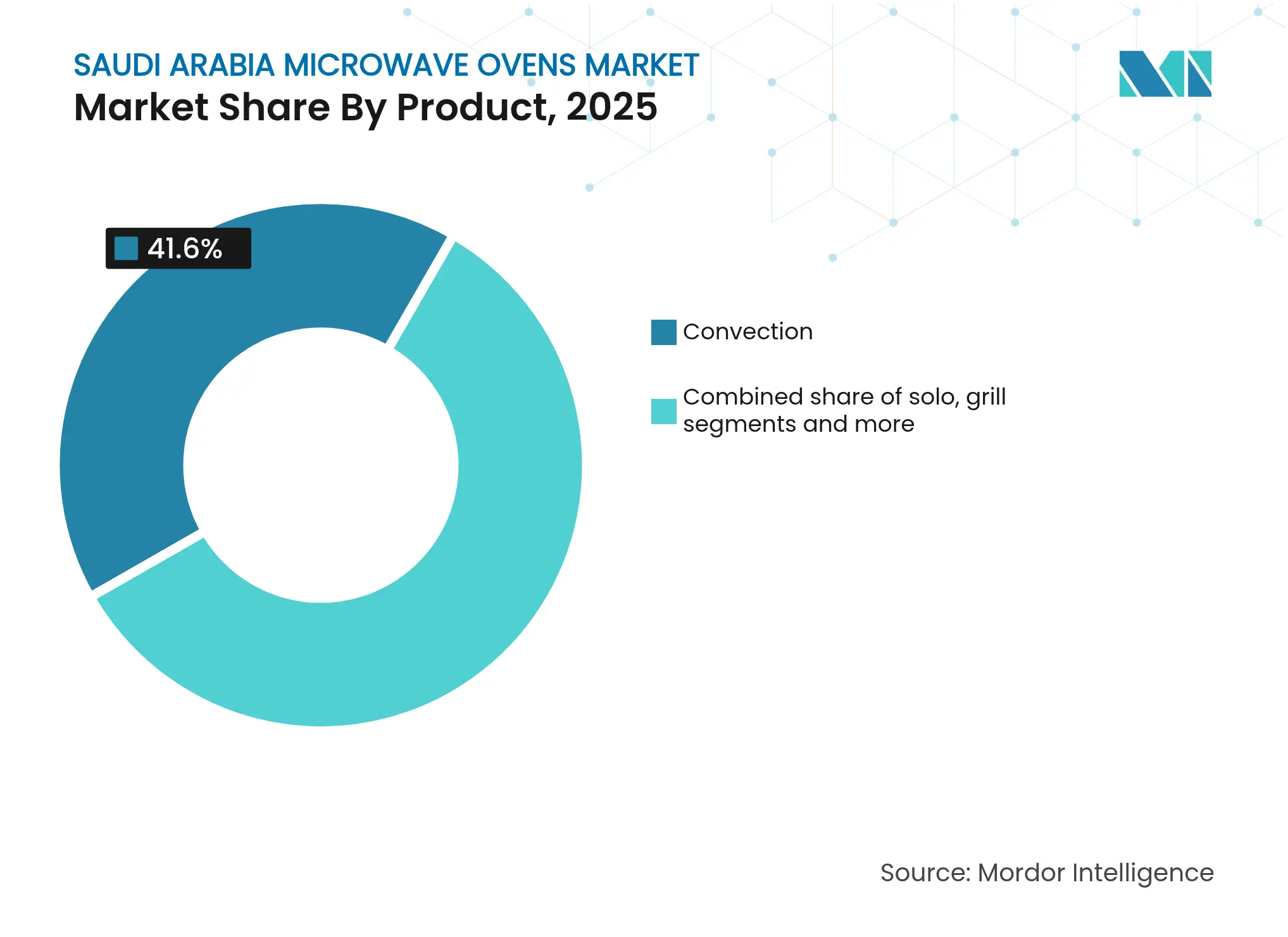

By Product: Convection Models Drive Market Leadership

Convection units accounted for 41.60% of 2025 revenue, cementing them as the keystone of the Saudi Arabia microwave ovens market. Multifunction heating meets local culinary routines ranging from reheating kabsa to baking desserts. Grill models, encouraged by healthy-eating campaigns, register a 4.83% CAGR and erode solo oven share. Consumers assessing value increasingly weigh air-fry integration and inverter energy savings before purchasing. Manufacturers spread these features to solo lines to protect entry-level relevance. Meanwhile, Samsung’s AI-ready ecosystem points to rising appetite for connected cooking, suggesting future segmentation may shift toward software capability tiers within the Saudi Arabia microwave ovens market.

Note: Segment shares of all individual segments available upon report purchase

By Structure: Countertop Dominance Faces Built-In Challenge

Countertop appliances captured 59.10% of 2025 unit sales due to straightforward setup and competitive pricing. Rental households and students favor portability and low upfront costs. Built-in units claim a 4.49% CAGR through 2031 as upscale developers incorporate seamless cabinetry. The average kitchen size in new Riyadh villas is falling, prompting homeowners to hide appliances behind flush panels. Local carpenters install standardized niches that speed replacement cycles and normalize built-in sizes, improving part commonality. As a result, the Saudi Arabia microwave ovens market sees ASP lift despite flat raw-material cost trends.

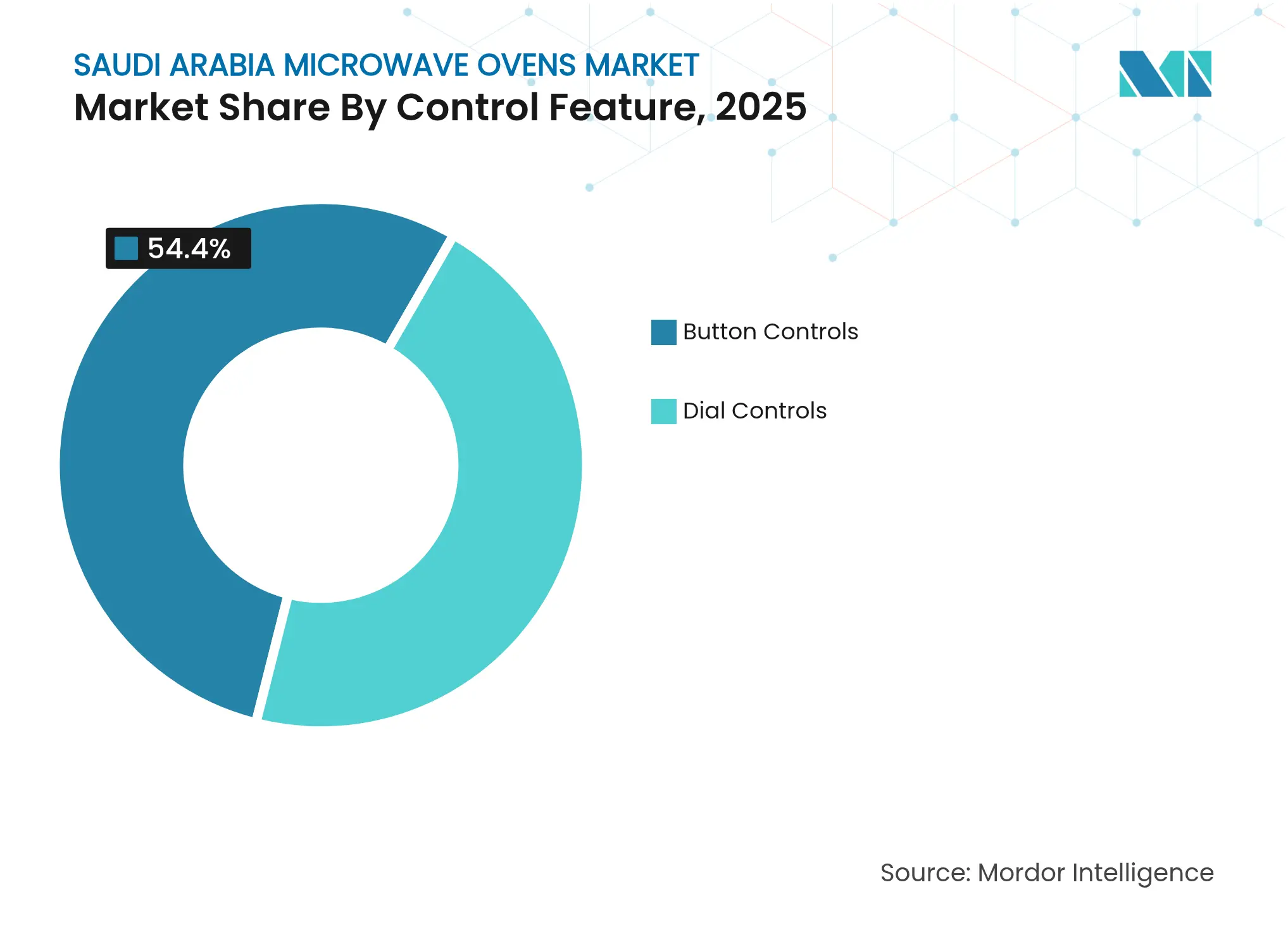

By Control Feature: Button Controls Maintain User Preference

Button panels held 54.40% share in 2025, preferred for tactile clarity and ease of cleaning. Multi-generational households welcome large physical keys over glass touchpads susceptible to fingerprints. Dial variants endure among senior consumers, but OEMs gradually phase them from premium lines to allow OTA firmware updates on button-plus-display hybrids. Samsung’s 2025 launch of 7-inch AI Home touchscreens could catalyze a slow interface migration once prices decline, but today reliability and familiarity sustain button dominance within the Saudi Arabia microwave ovens market.

Note: Segment shares of all individual segments available upon report purchase

By Capacity: Mid-Range Sizes Dominate Consumer Choice

The 20-24 liter class seized 39.30% share in 2025 as it suits typical Saudi family portions while fitting standard counter depth. 30 litres & above models pace growth at 4.73% CAGR, fueled by cloud kitchens and big families in the Eastern region. Compact ≤ 19-liter units serve dormitories and offices yet suffer from limited dish clearance, curbing broad appeal. Mid-range sizes see feature proliferation—sensor defrost, steam add-ons—enhancing value and reinforcing their anchor status in the Saudi Arabia microwave ovens market.

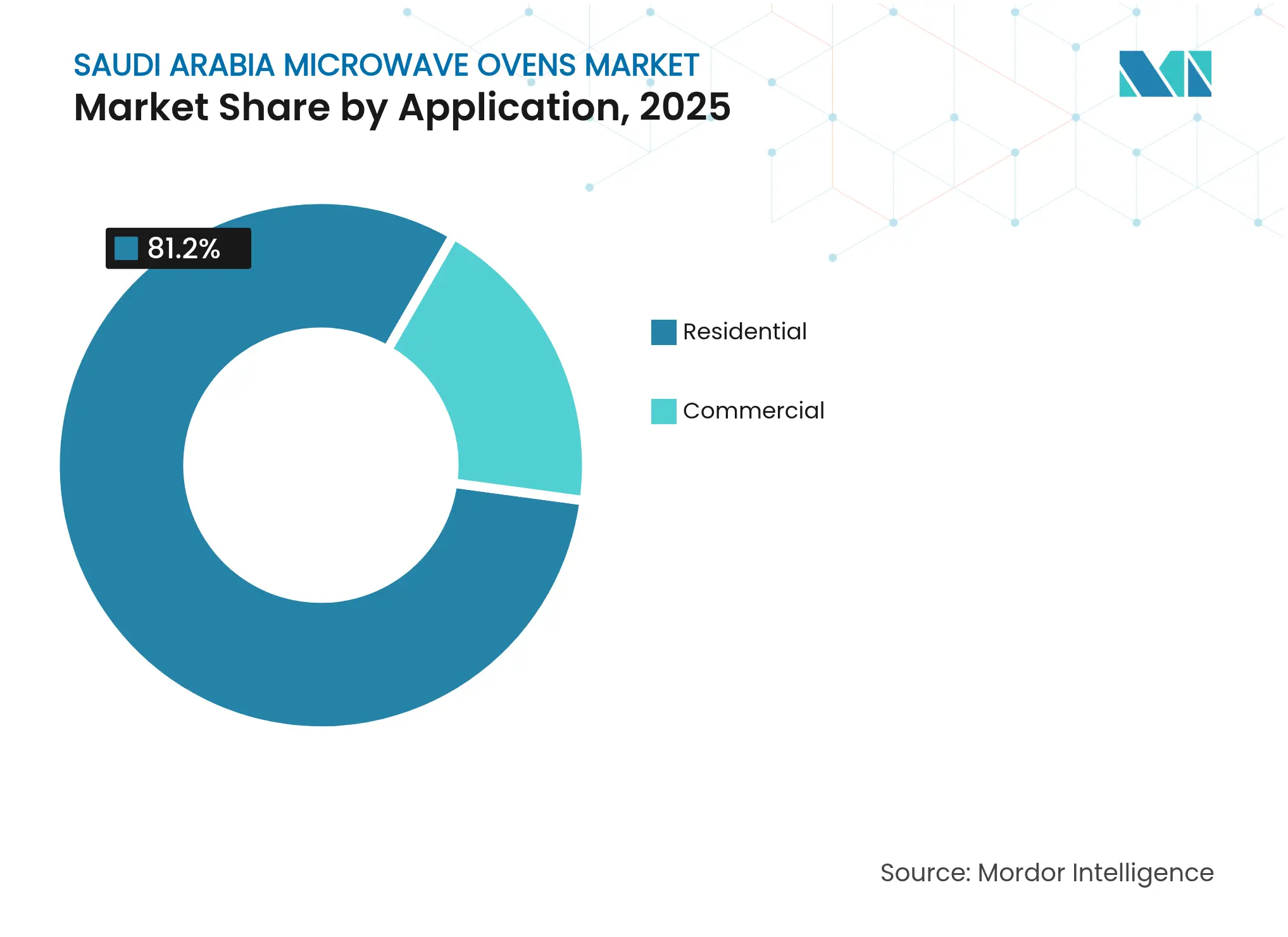

By Application: Residential Dominance with Commercial Acceleration

Households represented 81.20% of 2025 value, underpinning steady baseline demand via replacement and new-home fit-outs. Commercial kitchens, however, expand at 5.13% CAGR as QSR chains localize menus and ramp ghost-kitchen footprints. Commercial buyers stipulate stainless shells and 1,000-hour duty cycles, pushing vendors toward rugged models with field-swappable magnetrons. The cross-pollination of specs elevates overall quality expectations across the Saudi Arabia microwave ovens market.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Multi-Brand Stores Lead Amid Online Surge

Multi-brand electronics chains secured 44.20% of 2025 sales, offering in-person demos and same-day carryout convenience. Online marketplaces mount a 5.62% CAGR, boosted by frictionless checkout integrations and aggressive last-mile subsidies. Exclusive brand boutiques in luxury malls nurture high-margin lines and drive experiential marketing. Retailers now deploy click-and-collect points and AR product visualizers to merge channels, sustaining store footfalls while capturing the rising digital share of the Saudi Arabia microwave ovens market.

Central anchored 34.70% of the 2025 demand through concentrated dual-income households and government-backed mortgage programs. Jeddah and Mecca form the high-growth Western corridor at 4.34% CAGR, energized by tourism infrastructure. Western region buyers increasingly acquire commercial-grade units for hospitality suites serving religious tourists. Central households spend heavily on appliance upgrades, aided by mortgage rate incentives and mandatory building-code insulation that highlights energy-efficient microwave benefits. Eastern province consumers exhibit the highest average ticket due to expatriate demand for premium imported lines. In tier-2 Northern towns, outreach programs train local technicians, easing warranty concerns. Southern agricultural centers observe rising appliance ownership as farm families diversify income. Overall, regional convergence narrows but persists, requiring tailored channel strategies to maximize reach across the Saudi Arabia microwave ovens market.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

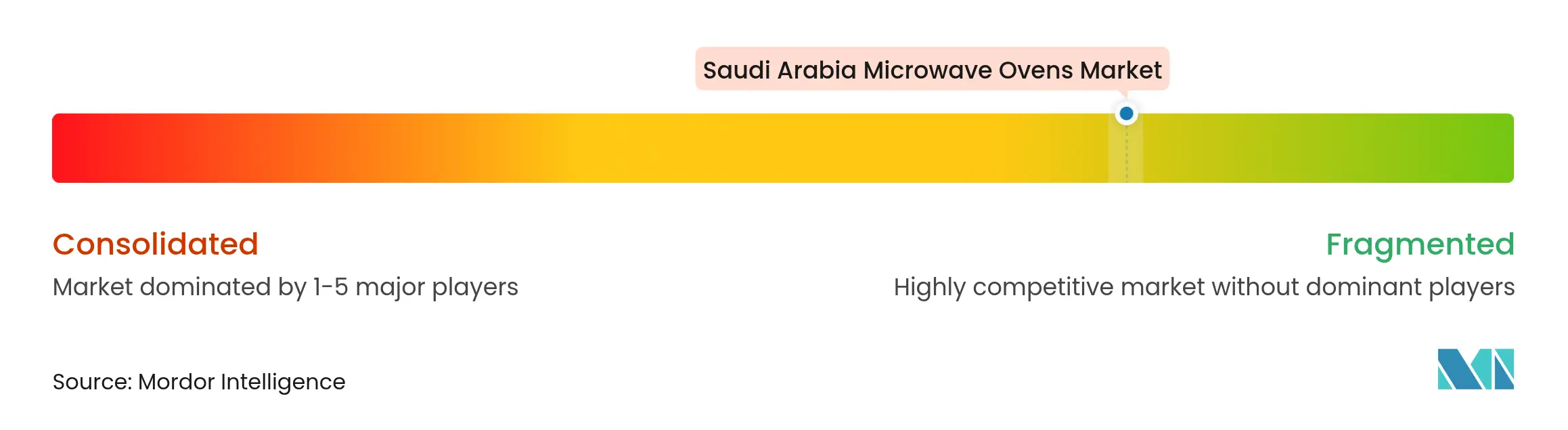

Market Concentration

The Saudi Arabia microwave ovens market shows fragmentation. LG and Samsung leverage global R&D pipelines to introduce inverter technology ahead of rivals. Whirlpool and Midea emphasize cost-effective countertop models to secure price-sensitive households.

Players race to comply with SASO’s evolving efficiency thresholds, investing in local testing labs to shorten certification cycles. Partnerships with distributors like eXtra enable extended warranty packages and in-store digital kiosks demonstrating AI features. Samsung’s 2025 Bespoke showcase underscored a pivot toward connected cooking suites, presaging higher attach rates for SmartThings subscriptions.

Domestic manufacturing prospects improve following the launch of Alat, which plans multi-category appliance facilities. Brands assessing joint-venture assembly explore tariff mitigation and faster replenishment. Service network expansion in Hail and Tabuk becomes a differentiator, as consumers value reliable after-sales care almost as much as headline features in the Saudi Arabia microwave ovens market.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size & Growth Forecasts (Value)

6. Competitive Landscape

7. Market Opportunities & Future Outlook

Market Definitions and Key Coverage

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

Desk Research

Market-Sizing & Forecasting

Data Validation & Update Cycle

Why Our Saudi Arabia Microwave Ovens Baseline Commands Confidence

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 149.76 million (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 146.2 million (2024) | Global Consultancy A | Omits built-in units; uses constant 2020 prices. | ||

USD 295.0 million (2023) | Global Consultancy B | Bundles ovens and microwaves; applies tax-inclusive retail mark-ups. | ||

USD 39.0 million (2024) | Trade Statistics Source C | Captures CIF import value only, excludes domestic mark-ups and replacement demand. |

A Leading Sanitaryware Company’s Journey in Saudi Arabia

4 Min Read

Strategic Expansion in the Russia Laundry Appliances Market

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.