Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

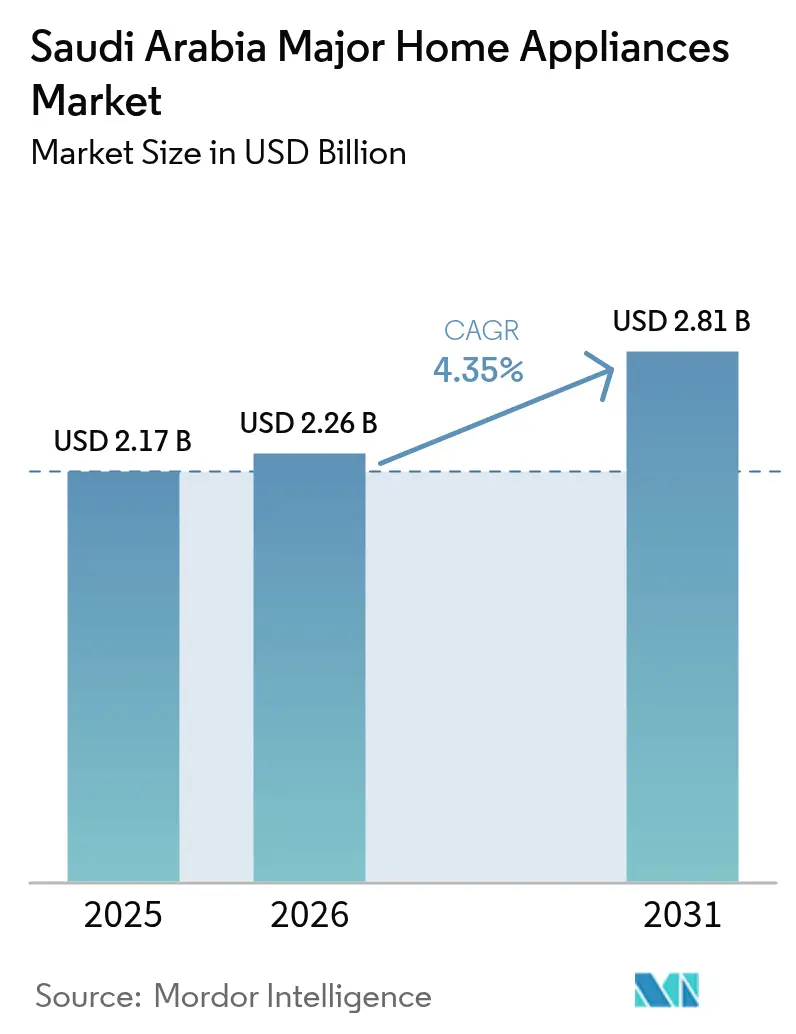

| Base Year Market Size (2025) | USD 2.17 Billion |

| Market Size (2026) | USD 2.26 Billion |

| Market Size (2031) | USD 2.81 Billion |

| Growth Rate (2026 - 2031) | 4.35% CAGR |

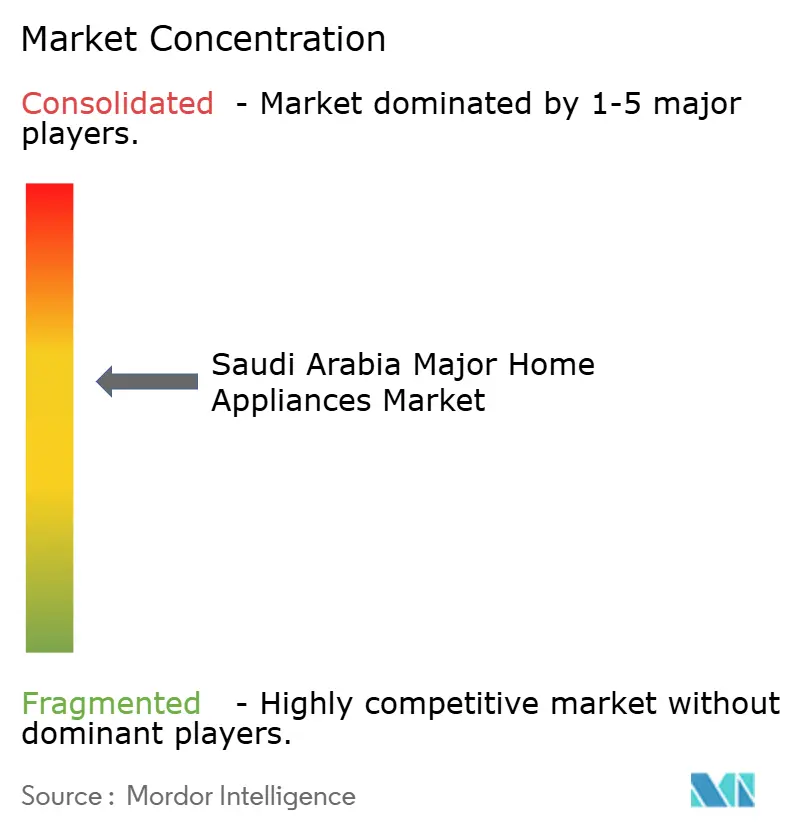

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Major Home Appliances Market Analysis by Mordor Intelligence

The Saudi Arabia major home appliances market size is expected to grow from USD 2.17 billion in 2025 to USD 2.26 billion in 2026 and is forecast to reach USD 2.81 billion by 2031 at 4.35% CAGR over 2026-2031. This market size outlook aligns with the Kingdom’s Vision 2030 economic program, which accelerates residential construction, incentivizes smart-home adoption, and expands domestic manufacturing capacity. Refrigerators and air conditioners already dominate unit sales because extreme summer temperatures push households to upgrade to more efficient cooling equipment, and government energy-label regulations accelerate replacement cycles. Rapid e-commerce growth, a youth-driven rise in disposable income, and strong housing demand in Riyadh, Jeddah, and emerging megaproject zones reinforce the sales momentum. At the same time, import-tariff reforms that raise duties to 15% on select electrical items provide cost advantages to local assembly operations and encourage foreign brands to partner with Saudi producers for tariff mitigation.

Key Report Takeaways

- By product type, air conditioners and refrigerators jointly commanded 29.05% of the Saudi Arabia major home appliances market share in 2025, while smart refrigerators are projected to advance at a 12.83% CAGR through 2031.

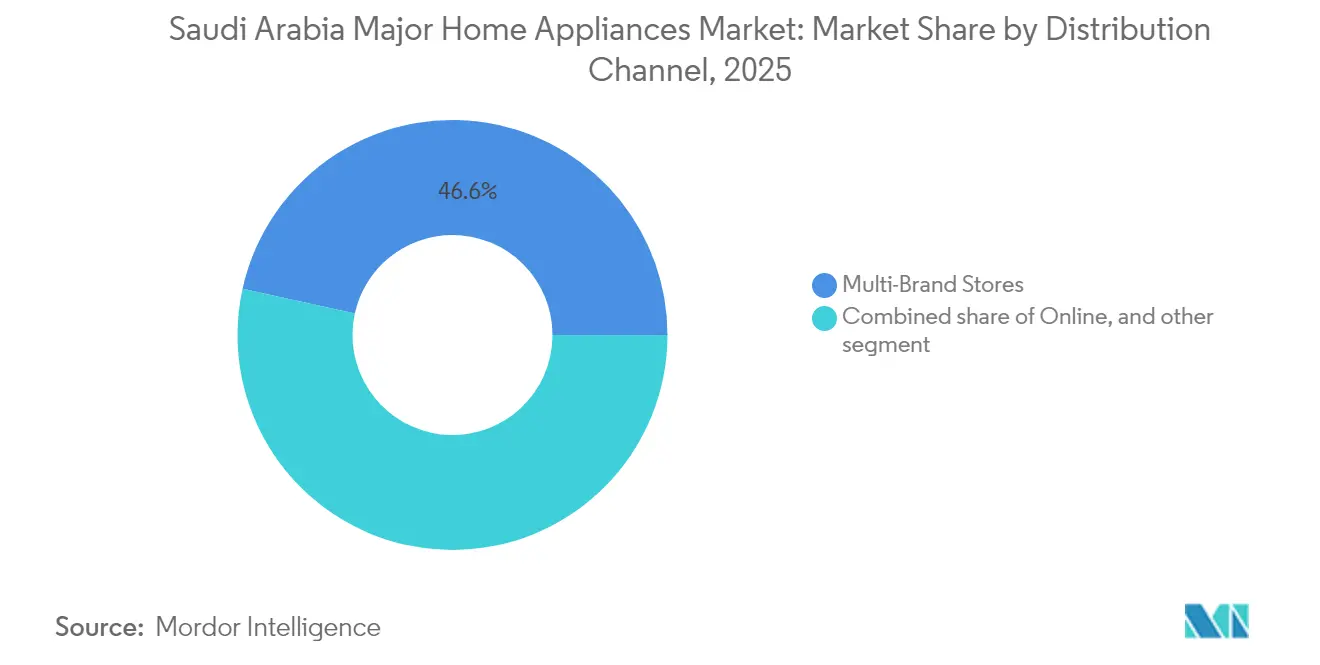

- By distribution channel, multi-brand stores held 46.55% of the Saudi Arabia major home appliances market in 2025, whereas online platforms are poised to expand at a 18.5% CAGR during the same period.

- By technology, conventional units represented 78.45% of the Saudi Arabia major home appliances market size in 2025, yet smart connected models are expected to progress at an 17.6% CAGR to 2031.

- By region, Central & Western region holds the dominating share 32.90% of the Saudi Arabia major home appliances market size in 2025, Western region led growth with a 8.95% CAGR in 2025 and remains the fastest-rising geography through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Major Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-efficiency labeling & SEEC enforcement | +1.2% | National, strongest in Riyadh, Jeddah, Dammam | Medium term (2-4 years) |

| Rapid expansion of e-commerce logistics networks | +0.8% | National, concentrated in major urban centers | Short term (≤ 2 years) |

| Rising disposable incomes among Saudi youth | +0.7% | National, higher in Central and Western regions | Long term (≥ 4 years) |

| Government housing programs (Sakani) boosting demand | +0.9% | National, priority in Riyadh, Makkah, Eastern Province | Medium term (2-4 years) |

| Surge in smart-home adoption under Vision 2030 | +0.6% | Urban centers, early adoption in NEOM, Qiddiya | Long term (≥ 4 years) |

| Cooling requirement for giga-projects (NEOM, Qiddiya) | +0.4% | Western and Northern regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Energy-Efficiency Labeling & SEEC Enforcement

Mandatory energy labels introduced by the Saudi Energy Efficiency Center have reshaped purchasing behavior, achieving a 91% compliance rate in 2024 [1]Saudi Energy Efficiency Center, “SEEC Compliance Dashboard 2024,” seec.gov.sa. . More than 50,000 non-compliant air conditioners have been removed from retail channels since enforcement intensified, highlighting robust oversight of the Saudi Arabia major home appliances market. The switch from EER to SEER measurement obliges consumers to retire older units sooner, while a SAR 1,000 incentive supports households that adopt high-efficiency split systems. Given that air conditioning consumes 70% of household electricity, inverter technology and smart-grid-ready compressors now headline marketing campaigns aimed at reducing peak-load demand. Accredited lab testing and SABER registration add a compliance gate that limits low-grade imports, compelling OEMs to enhance performance before market entry. The combined effect is a progressive shift toward advanced cooling appliances that satisfy both comfort expectations and tightening power-use regulations.

Government Housing Programs (Sakani) Boosting Demand

The Sakani platform issued more than 800,000 housing contracts by 2024 and lifted Saudi homeownership to 63.74% [2]Ministry of Municipal and Rural Affairs and Housing, “Annual Report of the Housing Program 2023,” momah.gov.sa. . Plans to build 115,000 homes a year until 2030 ensure a continual flow of first-time buyers needing complete appliance suites [3]Arab News, “Saudi E-Commerce Sales Using Mada Cards Hit USD 53bn in 2024,” arabnews.com. . VAT exemptions, low down payments, and subsidized mortgages remove financial barriers for middle-income families, stimulating bulk purchases of refrigerators, ranges, and washing machines. Mortgage securitization through the Saudi Real Estate Refinance Company enlarges lending capacity and underpins long-term demand visibility. Developers cluster near Riyadh, Makkah, and the Eastern Province, positioning appliance distributors close to the highest volume of new keys. Mandatory SASO certification guarantees product quality, so retailers focus on value-added services such as installation and extended warranty bundles to secure loyalty in this expanding customer base.

Surge in Smart-Home Adoption under Vision 2030

Vision 2030 emphasizes digital transformation, and 99% internet coverage, combined with 78% 5G availability, provides the connectivity backbone for smart appliances. The local IoT market is growing at 12.8% a year and is anticipated to reach USD 2.9 billion by 2025. Consumers increasingly expect Wi-Fi functionality in major devices, prompting LG and Samsung to embed remote diagnostics and energy-management dashboards into mainstream models. Government grants that promote data-driven energy savings nudge households toward connected refrigerators and AC units that synchronize with smart meters. NEOM and Qiddiya act as pilot zones where apartment blocks standardize on interoperable home-hub platforms, giving suppliers a showcase for nationwide marketing. As a result, smart SKUs are outpacing conventional lines, gradually eroding the 79.13% base that traditional appliances still occupy in the Saudi Arabia major home appliances market.

Rising Disposable Incomes Among Saudi Youth

Unemployment fell to 7.7% in 2024, female workforce participation surged, and non-oil GDP is advancing at 4.3% in 2025. Household budgets consequently allocate more resources to premium refrigerators, washer-dryer combos, and IoT-enabled ovens, with urban millennials showing the highest readiness to trade up. Retail credit remains plentiful due to retail-loan expansion by Saudi banks and benign interest rates that lower installment costs. Two-earner young families prefer feature-rich appliances that reduce household chores, and brand loyalty intensifies around manufacturers that offer after-sales apps. Private-sector job creation under Vision 2030 stimulates continuous income growth, which lifts discretionary spending despite periodic oil-price swings. Collectively, these factors inject durable purchasing power into the Saudi Arabia major home appliances market well beyond basic replacement demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High import tariffs on certain categories | -0.9% | National, all import-dependent segments | Short term (≤ 2 years) |

| Persistent grey-market influx of low-cost Asian brands | -0.6% | Border regions, price-sensitive urban areas | Medium term (2-4 years) |

| Limited local manufacturing ecosystem | -0.5% | National, especially outside industrial hubs | Medium term (2-4 years) |

| Water and energy efficiency mandates increasing compliance costs | -0.4% | National, with emphasis on air conditioners and washing machines | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Import Tariffs on Certain Categories

The July 2024 customs overhaul lifted duties on many electrical items to 15%, raising landed costs for imported refrigerators, freezers, and components [4]Saudi Press Agency, “Saudi Arabia Records 54% Surge in Industrial Investments After Expat Fees Waived,” spa.gov.sa. . Foreign brands must now recalibrate pricing or shift partial assembly to Saudi plants to stay competitive. Higher sticker prices can suppress volume growth in the near term, particularly in cost-sensitive mid-range segments. Yet these tariffs also bolster domestic manufacturing ambitions by narrowing the cost gap versus imports, aligning with the Vision 2030 goal of enlarging non-oil industrial GDP. Suppliers that establish knock-down kit factories inside the Kingdom gain duty exemptions and potentially faster customs clearance. The policy therefore penalizes purely import-based models while stimulating local value addition, reshaping supply chains in the Saudi Arabia major home appliances market.

Persistent Grey-Market Influx of Low-Cost Asian Brands

Uncertified appliances still reach Saudi consumers through unofficial distributors that bypass SASO documentation. Price gaps of 10–20% tempt buyers in border cities and discounted urban bazaars, undermining official channel sales. New rules requiring Product Certificates of Conformity and shipment-by-shipment approvals should curb this leakage, but enforcement hurdles persist at secondary entry points. Legitimate retailers respond by emphasizing factory warranties, maintenance networks, and guaranteed energy ratings that grey-market sellers cannot match. Greater public awareness campaigns and targeted customs raids are gradually shielding brand equity, yet the issue continues to subtract 0.6% from the Saudi Arabia major home appliances market CAGR outlook until full compliance is achieved.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cooling Dominates amid Smart Innovation

Air conditioners and refrigerators jointly held 29.05% of the Saudi Arabia major home appliances market share in 2025, driven by high ambient temperatures and SEEC-mandated energy upgrades. Smart refrigerators, supported by IoT sensors and mobile dashboards, are set to record a 12.83% CAGR, the fastest among all categories. The Saudi Arabia major home appliances market size for cooling appliances expands further as households switch from window to split systems to qualify for the SAR 1,000 incentive. LG’s Inverter Ducted Split models with antimicrobial filters and Samsung’s dual-sensor technology illustrate brand competition that prioritizes both comfort and lower utility bills. Washing machines remain resilient thanks to enhanced water-efficiency standards, while dishwashers gain traction in metropolitan kitchens where space and labor savings matter. Freezers remain essential for bulk food storage, reflecting Saudi bulk-buying habits and extended family living patterns. Premium oven and built-in appliance sales rise in tandem with upscale housing developments in Riyadh and Jeddah, presenting scope for smart cooking platforms that integrate recipe libraries and AI cooking assistance.

Transition toward intelligent cooling continues as inverter compressors and variable-speed fans migrate into mid-priced units, eroding the cost premium once associated with advanced HVAC. Manufacturers embed Wi-Fi modules that push firmware updates and allow remote fault diagnostics, curtailing service downtimes for end users. Retailers use in-store energy-savings calculators to demonstrate payback periods, which resonate with bill-conscious consumers following successive electricity-tariff adjustments. High-efficiency units also align with government peak-load reduction programs that may soon introduce dynamic tariffs, further bolstering demand for adaptive cooling technologies. This feedback loop supports sustained revenue growth for smart categories while ensuring conventional models still serve price-sensitive shoppers looking for entry-level reliability. As a result, every brand refines a tiered product ladder to capture each income cohort without neglecting the expanding tech-savvy segment.

By Distribution Channel: Multi-Brand Stores Lead Digital Transition

Multi-brand retailers retained 46.55% of transaction value in 2025 because Saudi consumers still prefer in-person demonstrations of large appliances before checking out online. Chain operators such as eXtra leverage vast floor space to showcase connected ecosystems, yet final payment often occurs via the company’s mobile app after home measurement confirmation. The Saudi Arabia major home appliances market size funneled through the online channel is set to rise at a 18.5% CAGR as logistics investments shorten delivery windows to under 48 hours nationwide. Pure-play e-commerce sites benefit from low overheads and targeted marketing but must solve reverse-logistics challenges for high-value returns. Brand-exclusive boutiques remain viable for premium lineups that need curated displays, while neighborhood dealers cater to immediate replacement needs with same-day delivery promises. Payment-tech progress, including Mada contactless and Google Pay adoption, supports frictionless checkout irrespective of channel.

Traditional chains double as service hubs for warranty repairs, reinforcing customer confidence that online-only rivals cannot easily replicate. “Bricks-and-clicks” hybrids capture impulse-purchase upsells such as extended warranties or accessory bundles during showroom visits. Retailers also integrate VR tools so shoppers can visualize appliances in custom kitchen layouts, marrying physical touchpoints with digital inspiration. Meanwhile, government initiatives encouraging SMEs to sell online expand rural coverage for essential appliances, bringing fringe provinces into the mainstream retail network. These developments collectively steer market share toward platforms that merge experiential retail with fast fulfillment, all while maintaining the high-trust environment that Saudi buyers expect for big-ticket items.

By Technology: Conventional Base Shifts toward Smart Integration

Conventional machines still accounted for 78.45% share in 2025 because many households replace like-for-like units on a budgetyet smart appliances are gaining ground at an 17.6% CAGR through 2031. The Saudi Arabia major home appliances market, therefore, accommodates two parallel value propositions: affordable reliability for mass households and data-driven convenience for digitally engaged consumers. Smart-device rollout gains momentum because 78% 5G coverage enables seamless firmware downloads and real-time diagnostics without home Wi-Fi dead zones. Power utilities encourage connected equipment that cooperates with demand-response signals, and utilities’ mobile apps now integrate appliance dashboards, making consumption more transparent to users. SASO regulations increasingly reward devices that display real-time energy data, nudging shoppers toward smart SKUs that satisfy both efficiency goals and lifestyle aspirations. Artificial intelligence features—such as LG’s Copilot integration for predictive maintenance—begin to migrate from flagship refrigerators and washers into mid-tier lines, accelerating feature trickle-down. Manufacturers capitalize on this transition by bundling smart modules as optional add-ons, allowing buyers to upgrade when household budgets allow.

Meanwhile, conventional models do not disappear; instead, they evolve with incremental technology such as brushless DC motors that save power without adding connectivity. Lower upfront cost remains crucial for first-time homeowners under Sakani’s affordable-housing schemes, ensuring a broad installed base for basic machines. Suppliers streamline production lines by designing a common chassis that can host either conventional or smart control boards, enhancing manufacturing flexibility. Aftermarket retrofit kits emerge that convert legacy models into semi-smart units capable of basic monitoring, prolonging useful life while easing the shift toward connected homes. The coexistence of both modes supports inclusive growth, positioning the Saudi Arabia major home appliances market as a dynamic arena where every income bracket finds a timely upgrade path.

Geography Analysis

The Central and Western regions combined captured 32.90% of Saudi Arabia major home appliances market in 2025, and the Western corridor now advances at a 8.95% CAGR thanks to NEOM, the Red Sea Project, and Qiddiya. The Saudi Arabia major home appliances market size expands most rapidly in these job-creating zones, where new housing, hospitality, and retail spaces demand comprehensive appliance packages. NEOM’s net-zero mandate incentivizes procurement of solar-ready refrigerators and ultra-efficient HVAC that align with strict carbon budgets. Jeddah’s thriving tourism and expatriate communities add steady replacement demand for versatile kitchen appliances and laundry equipment capable of multi-language interface support. The Eastern region posts solid gains through industrial hiring in Dammam and Al-Khobar, where employee housing contracts specify durable, mid-range appliances that balance cost with SASO compliance. Northern and Southern provinces remain smaller sales territories but receive increased logistical attention as e-commerce penetration lowers delivery barriers, gradually broadening the national market footprint.

Megaproject developers execute phased construction, so appliance orders surface in waves: initial worker accommodations need rugged, bulk-buy models, while luxury villas built later require bespoke, Wi-Fi-enabled bundles. Retailers expand satellite outlets near construction zones and partner with logistics providers to stage inventory in portable warehouses, minimizing lead times. Customized SKUs featuring Arabic-language smart-home integration appeal to the growing domestic middle class and migrant executives alike, reinforcing brand presence. Government incentives for domestic manufacturing encourage OEMs to locate assembly lines near Western free-trade zones, shortening supply chains and offering faster customization. These region-specific dynamics ensure that geographical sales patterns will stay diversified, with growth pockets shifting in concert with the Kingdom’s evolving urbanization map.

Competitive Landscape

The Saudi Arabia major home appliances market shows moderate concentration, with the top companies accounting for a significant share of 2024 revenue. LG holds the leading position, driven by strong air-conditioning and laundry product lines, supported by local assembly in partnership with the Shaker Group. Samsung secures a prominent position in the market, leveraging its Bespoke AI product lineup and widespread online presence to drive consumer engagement and sales. Haier also maintains a notable presence, thanks to competitively priced, multi-brand offerings sold under the GE and Candy labels. Tariff escalation to 15% on imported units presses global firms to deepen Saudi partnerships; LG already produces split-system casings domestically, while Samsung explores joint-ventures under the new Alat industrial umbrella. Chinese entrants emphasize cost-effective smart refrigerators, expanding direct-to-consumer models that bypass conventional retail mark-ups but must still clear SASO compliance hurdles.

Technology partnerships stand out as prime differentiators. LG’s alliance with Microsoft integrates Copilot for predictive maintenance across 2025 smart lines, whereas Samsung’s entry in the Home Connectivity Alliance ensures interoperability for multi-brand smart ecosystems. Manufacturers also race to meet SEER thresholds ahead of regulatory deadlines, upgrading R-32 refrigerants and variable-speed drives to stave off efficiency-related obsolescence. Authorized channel operators bolster loyalty by extending five-year full warranties, a compelling value proposition against grey-market imports lacking service infrastructure. Local content mandates under Vision 2030 stimulate build-operate-transfer agreements that incrementally lift in-country component fabrication, promising shorter lead times and tailored SKUs. Overall rivalry remains intense yet structured, with players balancing innovation pacing, after-sales reach, and tariff-driven cost management to retain share in the Saudi Arabia major home appliances market.

Saudi Arabia Major Home Appliances Industry Leaders

LG Electronics

Samsung Electronics

Haier Group (incl. Candy & GE Appliances)

Whirlpool Corp.

Midea Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: LG Electronics partnered with Microsoft to embed Copilot AI agents into 2025 smart TVs and home appliances, enhancing device autonomy and energy optimization.

- October 2024: The Communications, Space and Technology Commission and SASO mandated USB Type-C charging ports for phones by Jan 2025 and laptops by Apr 2026, aiming to cut electronic waste and save consumers SAR 170 million annually.

- September 2024: BinDawood committed USD 390 million to new delivery hubs that strengthen last-mile logistics for large-format products, including major appliances.

- May 2024: United Electronics Company (eXtra) opened its 50th branch and reported Q1 profit of SAR 93.9 (USD 25.03) million, marking 11% growth and signaling its intent to claim 25% national market share.

Saudi Arabia Major Home Appliances Market Report Scope

A home appliance, also referred to as a domestic appliance, an electric appliance, or a household appliance, is a machine that assists in household functions such as cooking, cleaning, and food preservation. A complete background analysis of the major home appliances market, which includes an assessment of the national accounts, economy, and emerging market trends by segments, significant changes in the market dynamics, and the market overview, is covered in the report. The Market is Segmented By Product (Refrigerators, Freezers, Dish Washing Machines, Ovens, Air Conditioners, and Other Major Appliances) and By Distribution Channel (Multi-Branded Stores, Specialty Stores, Online, and Other Distribution Channels). The report offers the market size and forecasts in value (USD Billion) for the above segments.

By Product Type (Value)

| Refrigerators |

| Freezers |

| Dishwashing Machines |

| Washing Machines |

| Ovens |

| Air Conditioners |

| Other Major Home Appliances |

By Distribution Channel

| Multi-Brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

By Technology

| Smart Connected Major Appliances |

| Conventional Major Appliances |

By Region

| Central Region |

| Western Region |

| Eastern Region |

| Northern Region |

| Southern Region |

| By Product Type (Value) | Refrigerators |

| Freezers | |

| Dishwashing Machines | |

| Washing Machines | |

| Ovens | |

| Air Conditioners | |

| Other Major Home Appliances | |

| By Distribution Channel | Multi-Brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| By Technology | Smart Connected Major Appliances |

| Conventional Major Appliances | |

| By Region | Central Region |

| Western Region | |

| Eastern Region | |

| Northern Region | |

| Southern Region |

Key Questions Answered in the Report

What is the current value of the Saudi Arabia major home appliances market?

What is the current value of the Saudi Arabia major home appliances market?

Which product category leads sales?

Air conditioners and refrigerators together represented 29.05% of 2025 revenue, reflecting the country’s hot climate and energy-efficiency push.

How fast are smart appliances growing?

How fast are smart appliances growing?

What impact do higher import tariffs have?

The 15% duty on many electrical items increases costs for import-heavy brands but encourages local assembly partnerships that bypass these fees.

Which sales channel grows the quickest?

Online platforms are forecast to expand at a 18.5% CAGR, driven by improving logistics and contactless-payment adoption.

Why is the Western region important?

NEOM, the Red Sea Project, and Qiddiya fuel a 8.95% CAGR in that region, demanding high-efficiency cooling and smart-home solutions.

Page last updated on: