Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

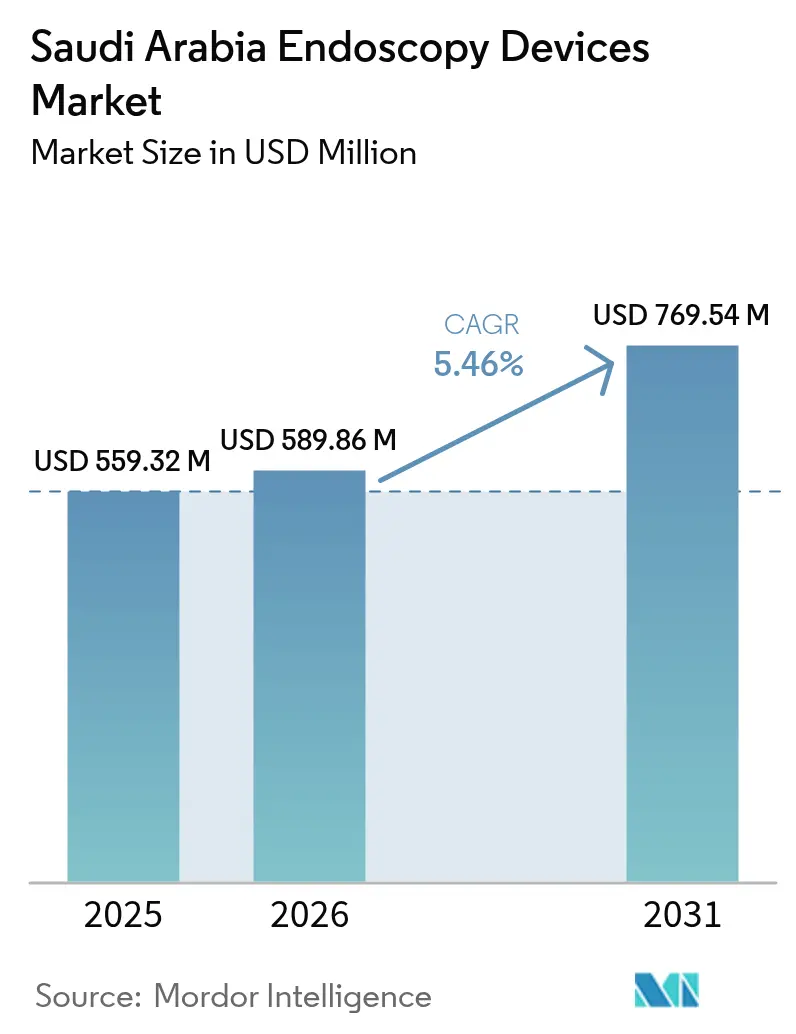

| Base Year Market Size (2025) | USD 559.32 Million |

| Market Size (2026) | USD 589.86 Million |

| Market Size (2031) | USD 769.54 Million |

| Growth Rate (2026 - 2031) | 5.46% CAGR |

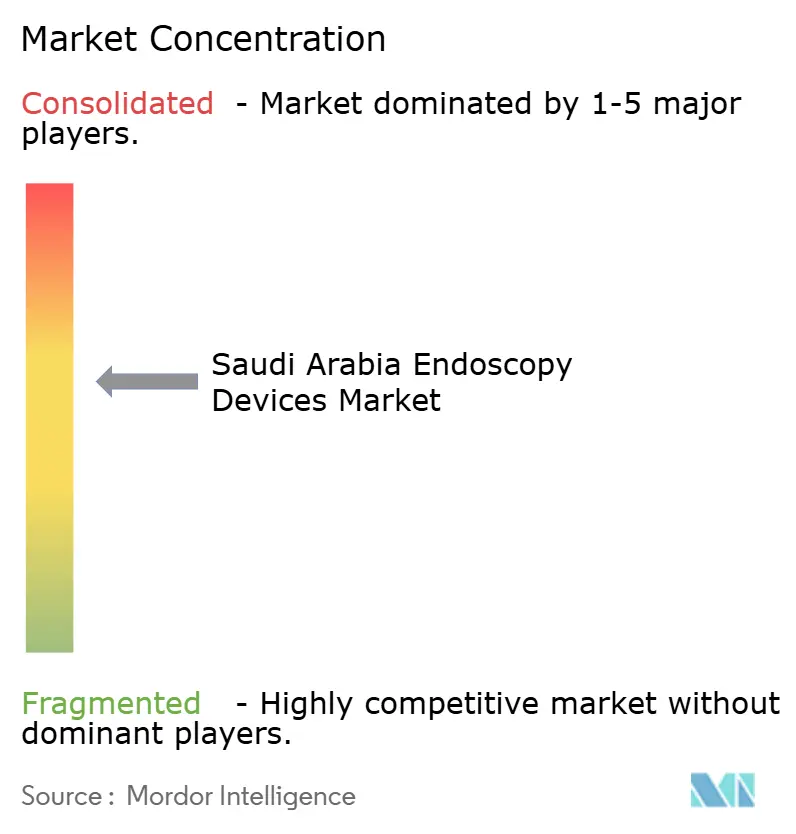

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Endoscopy Devices Market Analysis by Mordor Intelligence

The Saudi Arabia endoscopy devices market size was valued at USD 559.32 million in 2025 and estimated to grow from USD 589.86 million in 2026 to reach USD 769.54 million by 2031, at a CAGR of 5.46% during the forecast period (2026-2031). The solid trajectory reflects Vision 2030-led healthcare modernization, large-scale procurement of minimally invasive technologies, and the country’s push to localize complex procedures. Demand spikes during Hajj and Umrah seasons, rising gastrointestinal (GI) disease incidence, and the rapid spread of AI-enabled visualization systems all reinforce growth. Hospital groups continue to centralize purchasing, yet private operators and ambulatory surgery centers are accelerating orders as reimbursement pathways improve. International vendors extend local training centers and technology-transfer deals to protect share, while emerging Saudi distributors target niche product gaps.

Key Report Takeaways

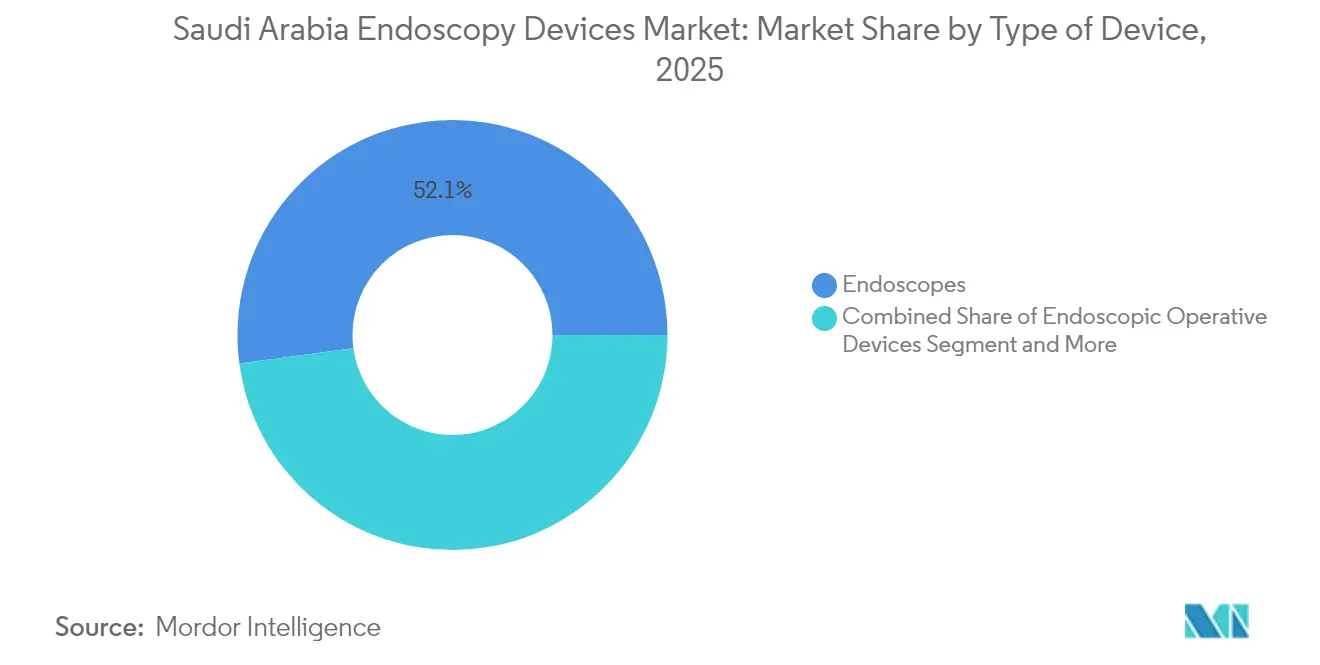

- By device type, endoscopes held 52.12% of the Saudi Arabia endoscopy devices market share in 2025, whereas visualization equipment is forecast to expand at a 9.78% CAGR through 2031.

- By application, gastroenterology accounted for 39.06% of the Saudi Arabia endoscopy devices market size in 2025 and neurology is projected to advance at an 11.24% CAGR to 2031.

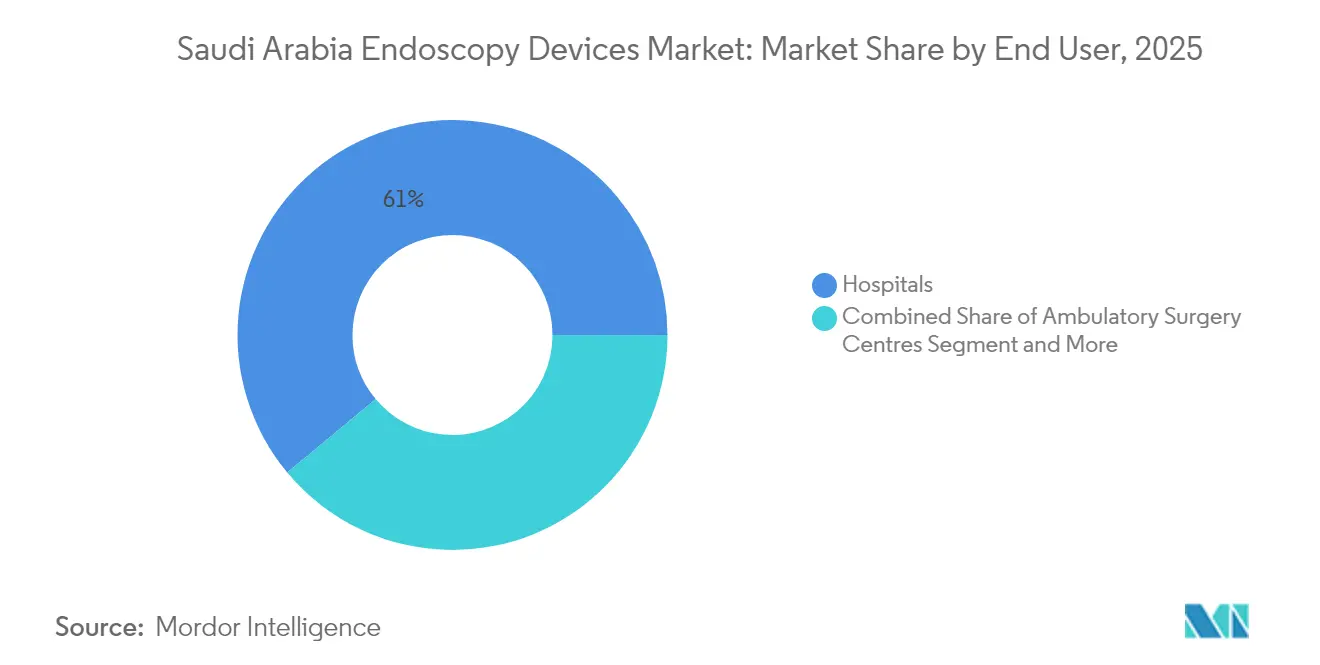

- By end user, hospitals commanded 61.05% of the Saudi Arabia endoscopy devices market size in 2025, while ambulatory surgery centers are set to record the fastest 11.63% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Endoscopy Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Preference for Minimally-Invasive Surgeries | +1.2% | Global, with early gains in Riyadh, Jeddah, Eastern Province | Medium term (2-4 years) |

| Rising Prevalence of GI Disorders in Saudi Arabia | +0.9% | National, concentrated in urban centers | Long term (≥ 4 years) |

| Expanding Healthcare Infrastructure & Private Hospital Investment | +1.5% | National, with priority in NEOM, Red Sea Project regions | Medium term (2-4 years) |

| Favourable Vision-2030 Healthcare Initiatives | +1.1% | National implementation with regional variations | Long term (≥ 4 years) |

| Pilgrimage-Related Surge in Emergency Endoscopy Demand | +0.4% | Mecca, Medina regions with spillover to Jeddah | Short term (≤ 2 years) |

| AI-Enabled Capsule Endoscopy Adoption by Tele-Health Start-Ups | +0.6% | Urban centers, expanding to remote regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Preference for Minimally-Invasive Surgeries

Hospitals and private centers in Riyadh and Jeddah increasingly favor minimally invasive procedures because they shorten intensive-care stays and lower total treatment costs. Robotic heart programs at King Faisal Specialist Hospital cut average ICU time from 26 days to four, which convinces administrators to redirect capital toward upgraded endoscopic suites[1]King Faisal Specialist Hospital & Research Centre, “KFSH&RC Leads the Global Healthcare Revolution with AI and Robotics,” kfshrc.edu.sa. The August 2025 installation of a da Vinci system at Johns Hopkins Aramco Healthcare signals broader regional adoption. Vendors must comply with Saudi FDA registration rules and ISO 13485 requirements before shipping systems. As clinical teams gain hands-on training at new vendor-run academies, procedure volumes for robotic and flexible endoscopy rise, anchoring steady equipment reorder cycles.

Rising Prevalence of GI Disorders in Saudi Arabia

Recent national studies document climbing rates of inflammatory bowel disease, colorectal cancer, and gastroesophageal reflux among Saudi adults, trends tied to dietary shifts and sedentary lifestyles[2]Saudi Ministry of Health, “National Colorectal Screening Initiative,” moh.gov.sa. These conditions drive earlier and more frequent screening using colonoscopes and capsule endoscopes. Vision 2030 preventive-care mandates push public hospitals to expand surveillance programs, raising annual procurement of flexible endoscopes and 4K visualization towers. Private gastroenterology clinics respond by adding same-day diagnostic services, intensifying demand for high-volume reprocessing equipment. Compliance with international colorectal screening guidelines and Saudi FDA software-as-a-medical device rules shape product selection for AI polyp-detection tools.

Expanding Healthcare Infrastructure & Private Hospital Investment

More than ten flagship private hospitals are under construction across NEOM and the Red Sea corridor, each budgeting for full endoscopy suites and integrated sterile reprocessing lines. Becton Dickinson’s simulation center in Riyadh, opened in May 2025, illustrates how global manufacturers co-locate training with new builds to accelerate uptake. The National Unified Procurement Company bundles large public orders, while private groups negotiate direct supply contracts with service-level guarantees. Contractors must meet Saudi Building Code standards that require negative-pressure endoscopy rooms and redundant water filtration, factors that boost accessory sales such as insufflators and suction pumps.

Favorable Vision 2030 Healthcare Initiatives

Government programs link clinical training, digital health, and local manufacturing incentives, forming a policy flywheel that benefits the Saudi Arabia endoscopy devices market. The Human Capability Development Program funds scholarships for GI fellows to train in AI-enabled colonoscopy. Sanabil Investments partnered with Redesign Health in January 2025 to create a venture studio expected to launch 20 new healthcare companies that could design single-use endoscopes or smart biopsy tools. Accelerated Saudi FDA review pathways shorten device-approval timelines to under six months for technologies already cleared by the U.S. FDA or CE marked. Intellectual-property reforms help multinationals justify local assembly operations, further easing supply bottlenecks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infection & Cross-Contamination Risks | -0.8% | National, particularly in high-volume centers | Short term (≤ 2 years) |

| High Cost & Limited Reimbursement for Advanced Systems | -1.1% | National, affecting both public and private sectors | Medium term (2-4 years) |

| Shortage of Trained Female Endoscopists | -0.6% | National, with acute impact in conservative regions | Long term (≥ 4 years) |

| Import-Dependency & Geo-Political Supply Delays | -0.7% | National, with strategic buffer planning in major cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Infection & Cross-Contamination Risks

Reusable endoscope reprocessing remains complex, and several Saudi hospitals have reported sporadic contamination alerts that slowed elective case throughput. Administrators now weigh premium single-use scopes against higher consumable bills. Automated endoscope washers with real-time tracking sensors mitigate some risk but raise capital budgets and maintenance costs. The Ministry of Health audits sterilization workflows under updated infection-control guidelines modeled on WHO protocols. Vendors offering built-in leak testing, RFID-based scope tracking, and validated cleaning cycles gain preference, yet smaller centers struggle with staff certification and costs.

High Cost & Limited Reimbursement for Advanced Systems

AI-ready 4K towers, robotic flexible endoscopes, and smart biopsy forceps can triple upfront spending versus legacy units. Although Vision 2030 expands private insurance penetration, tariff schedules still lag behind actual equipment depreciation. Smaller private clinics defer purchases or lease devices, which elongates sales cycles. Currency fluctuations and a 5% customs duty add further pressure. Manufacturers must submit cost-effectiveness studies to the Saudi Health Technology Assessment Committee before premium systems enter public tenders, another barrier that slows unit growth in lower-volume facilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Device: Advanced Visualization Drives Technology Adoption

Flexible endoscopes captured 52.12% of the Saudi Arabia endoscopy devices market share in 2025, underlining their indispensability for upper and lower GI procedures. The Saudi Arabia endoscopy devices market size for endoscopes is projected to climb alongside higher colorectal screening volumes and the uptake of capsule formats in remote monitoring programs. Hospitals increasingly bundle flexible scopes with automated reprocessors to meet new infection-control benchmarks, deepening vendor lock-in.

Visualization equipment enjoys the fastest 9.78% CAGR because 4K towers and AI polyp-detection software improve diagnostic accuracy and shorten procedure times. King Faisal Specialist Hospital adopted ultra-high-definition imaging in 2024 and reported an 18% rise in adenoma-detection rates, which spurred peer institutions to follow. Vendors highlight plug-and-play upgrades that retrofit existing towers, bridging budget gaps for public centers. Single-use visualization components, particularly in bronchoscopy, gain acceptance in ICUs that lack full reprocessing rooms.

By Application: Gastroenterology Leadership with Neurology Expansion

Gastroenterology held 39.06% of the Saudi Arabia endoscopy devices market size in 2025 through sustained colorectal cancer screening and routine upper-GI diagnostics. Vision 2030’s prevention focus increases colonoscopy subsidies, driving regular turnover of colonoscope fleets and accessory biopsy forceps. Capsule endoscopy supports rural outreach programs, transmitting images to urban reading centers through telehealth platforms.

Neurology shows the most rapid 11.24% CAGR as tertiary hospitals introduce ventricular neuroendoscopy for hydrocephalus and tumor excision. Robotic stereotactic systems combined with flexible neuro-endoscopes lower surgical morbidity, making them attractive for centers seeking international accreditation. ENT and urology maintain steady growth by adding office-based endoscopy that shifts low-complexity work from congested hospitals to outpatient suites.

By End User: Hospital Dominance with ASC Growth Trajectory

Hospitals controlled 61.05% of the Saudi Arabia endoscopy devices market share in 2025 because tertiary centers concentrate advanced imaging towers and high-throughput reprocessing rooms. National Unified Procurement Company negotiations lock in multiyear vendor contracts that cover maintenance, training, and consumables, reinforcing market leadership among established brands.

Ambulatory surgery centers post a 11.63% CAGR as Vision 2030 incentives encourage day-case surgery expansion. Private operators in Riyadh and Dammam deploy slim colonoscopes and portable towers aimed at rapid turnover. Office-based clinics adopt single-use gastroscopes for helicobacter screening, giving vendors entry to a previously under-equipped niche.

Geography Analysis

Central Region hospitals anchored by Riyadh account for the largest share of the Saudi Arabia endoscopy devices market due to dense tertiary infrastructure, policy makers, and distributor headquarters. King Faisal Specialist Hospital’s 1,127 robotic procedures in 2024 underscore the region’s appetite for cutting-edge platforms. Procurement frameworks here often serve as templates for other provinces.

Western Region hubs Jeddah, Mecca, and Medina collectively generate the second-largest portion of demand. Seasonal pilgrimage inflows require flexible capacity, prompting facilities to maintain portable endoscopy towers that can be redeployed after Hajj. Private hospitals in Jeddah cater to a growing expatriate population that expects international-standard GI screening.

Eastern Region posts the fastest 2026-2031 growth rate as NEOM and Red Sea resorts come online with integrated medical campuses. King Fahd University Hospital’s robotic orthopedic milestones in 2025 illustrate the region’s expanding skill set. Northern and Southern regions still trail but attract Vision 2030 funding for new general hospitals equipped with modular endoscopy rooms.

Competitive Landscape

The Saudi Arabia endoscopy devices market is moderately fragmented. Olympus, Boston Scientific, Medtronic, and Karl Storz lead based on broad portfolios and long-standing distributor networks. They deepen presence through local training academies that shorten learning curves and reinforce loyalty. Becton Dickinson’s 2025 Riyadh center trains 1,000 clinicians annually on advanced visualization and sterility workflows[3]Becton Dickinson, “BD Simulation Center Riyadh Opens,” bd.com.

Local distributors such as ProMedEx and Almana leverage strong government ties to win regional tenders, often bundling consumables and service in price-competitive deals. Opportunities lie in AI-powered software, single-use scopes, and digitized reprocessing modules that align with Vision 2030 digitization targets. Hospitals give preference to vendors that prove measurable outcome gains—King Faisal Specialist Hospital achieved 98% survival in robotic cardiac cases, a benchmark that shapes procurement scoring models.

Market entrants must navigate Saudi FDA registration, cost-effectiveness dossiers, and post-market vigilance reporting. Manufacturers investing in partial local assembly could secure tariff exemptions and preferential tender scoring, providing a pathway to offset currency volatility and supply-chain disruptions.

Saudi Arabia Endoscopy Devices Industry Leaders

Fujifilm Holdings Corporation

Karl Storz SE & Co. KG

Olympus Corporation

Boston Scientific Corp.

Medtronic PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Becton Dickinson opened a training center in Riyadh to educate Saudi clinicians on advanced endoscopy and visualization technologies.

- February 2024: Waycen and MegaMind signed an AI-endoscopy supply agreement covering Middle East distribution, giving Saudi facilities early access to algorithm-driven diagnosis.

Saudi Arabia Endoscopy Devices Market Report Scope

As per the scope of this report, endoscopy devices are minimally invasive and can be inserted into natural openings of the human body, in order to observe an internal organ or a tissue in detail. Endoscopic surgeries are performed for imaging procedures and minor surgeries.

By Type of Device

| Endoscopes | Rigid Endoscope |

| Flexible Endoscope | |

| Capsule Endoscope | |

| Robot-assisted Endoscope | |

| Endoscopic Operative Devices | Irrigation / Suction System |

| Access Device | |

| Wound Protector | |

| Insufflation Device | |

| Operative Manual Instrument | |

| Visualization Equipment |

By Application

| Gastroenterology |

| Orthopedic Surgery |

| Cardiology |

| ENT Surgery |

| Gynecology |

| Neurology |

| Urology |

| Others |

By End User

| Hospitals |

| Ambulatory Surgery Centres |

| Office-based / Out-patient Clinics |

| By Type of Device | Endoscopes | Rigid Endoscope |

| Flexible Endoscope | ||

| Capsule Endoscope | ||

| Robot-assisted Endoscope | ||

| Endoscopic Operative Devices | Irrigation / Suction System | |

| Access Device | ||

| Wound Protector | ||

| Insufflation Device | ||

| Operative Manual Instrument | ||

| Visualization Equipment | ||

| By Application | Gastroenterology | |

| Orthopedic Surgery | ||

| Cardiology | ||

| ENT Surgery | ||

| Gynecology | ||

| Neurology | ||

| Urology | ||

| Others | ||

| By End User | Hospitals | |

| Ambulatory Surgery Centres | ||

| Office-based / Out-patient Clinics | ||

Key Questions Answered in the Report

What is the current value of the Saudi Arabia endoscopy devices market?

The market is valued at USD 589.86 million in 2026.

Which device category shows the fastest growth through 2031?

Visualization equipment leads with a projected 9.78% CAGR.

How large is the hospital segment within national demand?

Hospitals account for 61.05% of total 2025 sales.

Why is neurology gaining share in the Saudi endoscopy space?

Tertiary centers are adopting neuroendoscopic techniques that offer minimally invasive brain surgery with quicker recovery times.

How do Vision 2030 policies influence endoscopy procurement?

Vision 2030 incentivizes local training, digital health integration, and private investment, all of which accelerate endoscopy suite expansion.

What regional market shows the highest future growth?

The Eastern Region is forecast to grow fastest due to new medical campuses tied to NEOM and Red Sea projects.

Page last updated on: