Market Overview

| Study Period | 2023 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

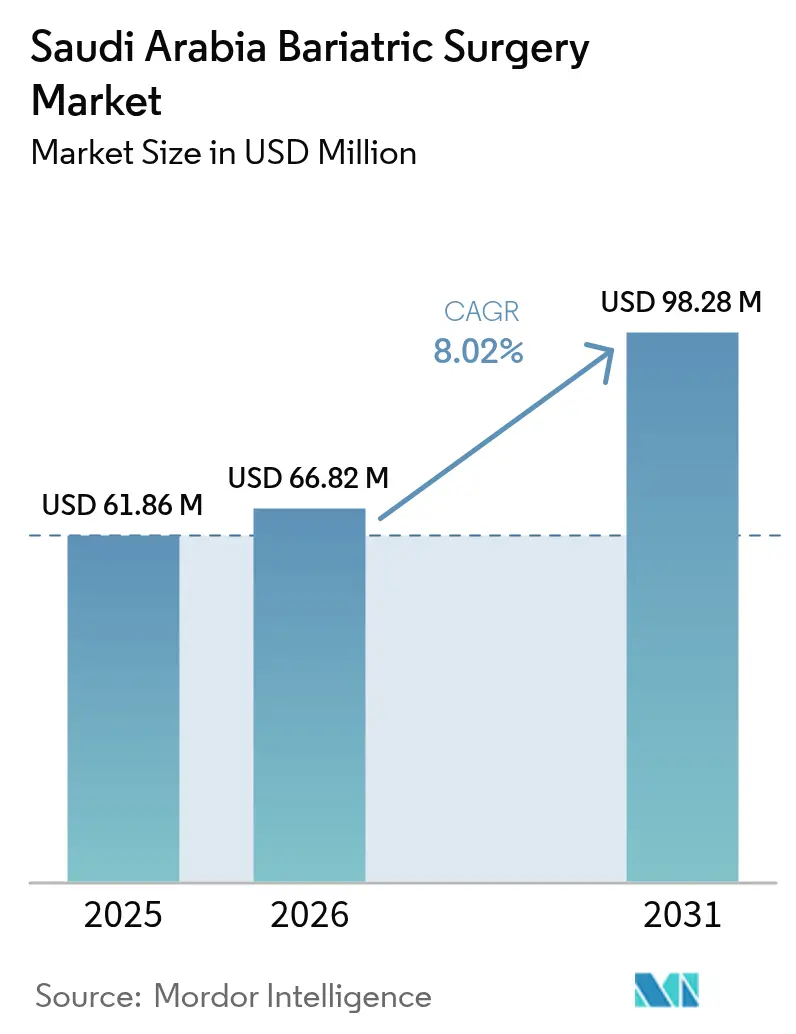

| Base Year Market Size (2025) | USD 61.86 Million |

| Market Size (2026) | USD 66.82 Million |

| Market Size (2031) | USD 98.28 Million |

| Growth Rate (2026 - 2031) | 8.02% CAGR |

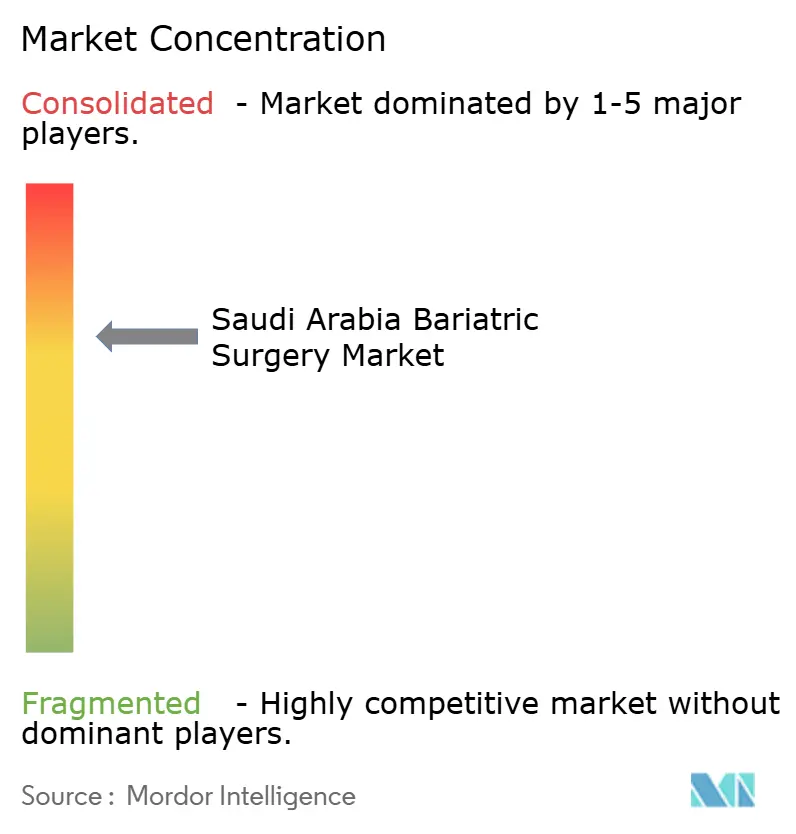

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Bariatric Surgery Market Analysis by Mordor Intelligence

The Saudi Arabia Bariatric Surgery market size was valued at USD 61.86 million in 2025 and estimated to grow from USD 66.82 million in 2026 to reach USD 98.28 million by 2031, at a CAGR of 8.02% during the forecast period (2026-2031). Rising adult obesity, sustained healthcare capital spending, and widening insurance coverage anchor this growth. Private operators collaborate with public hospitals to open dedicated centers, and global device makers deepen local distribution to capture procedure volume. Hospitals accelerate robotic and laparoscopic programs that shorten inpatient stays, while ambulatory surgery centers pursue cost-based differentiation. Workforce training initiatives and outcome registries strengthen clinical quality, positioning the Saudi Arabia Bariatric Surgery market for steady procedure expansion across all provinces.

Key Report Takeaways

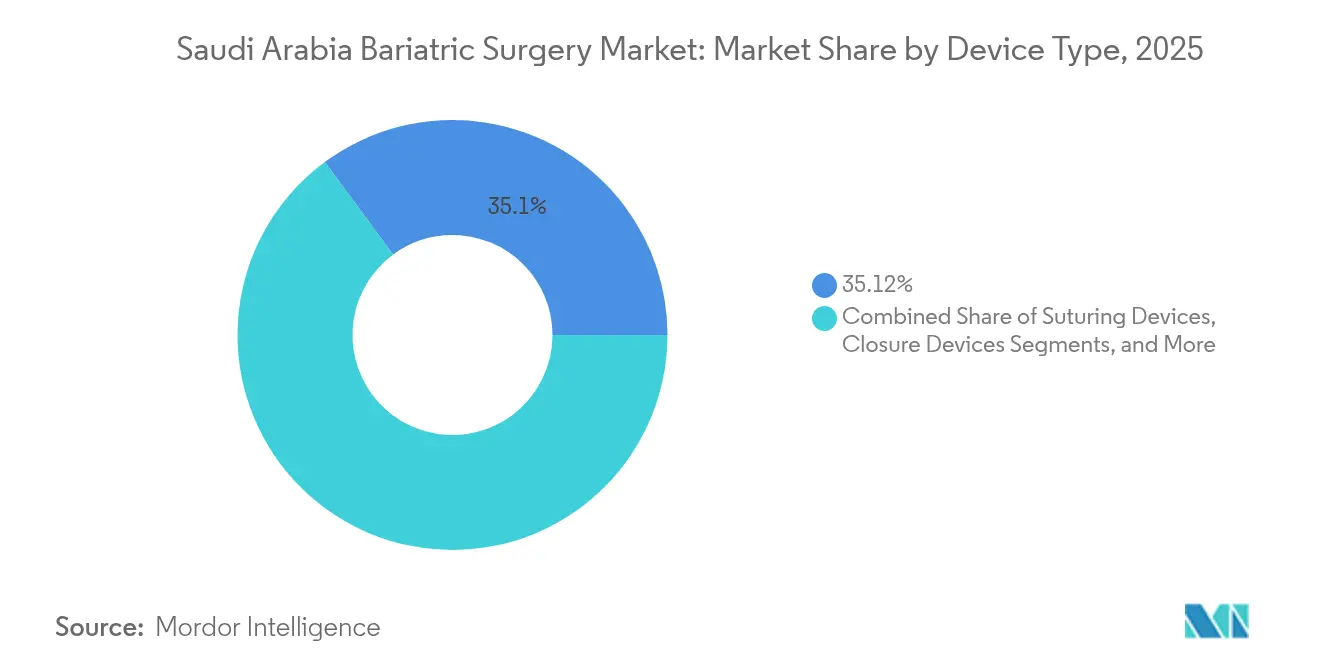

- By device type, Stapling Devices led with 35.12% of Saudi Arabia Bariatric Surgery market share in 2025.

- By device type, Gastric Balloons are projected to record the fastest 9.31% CAGR through 2031.

- By procedure, Sleeve Gastrectomy commanded 78.12% of the Saudi Arabia Bariatric Surgery market size in 2025.

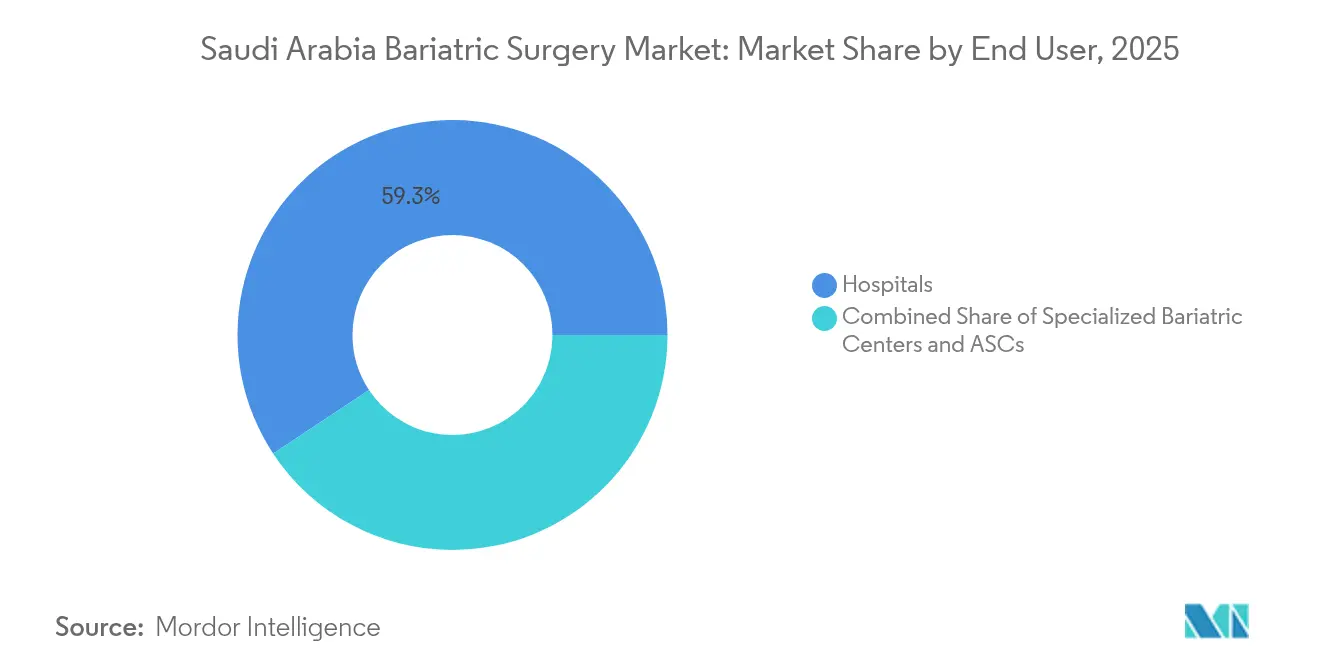

- By end user, Hospitals captured 59.28% revenue share in 2025, while Ambulatory Surgical Centres are set to expand at a 9.09% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Bariatric Surgery Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising obesity prevalence | +1.8% | Urban centers nationwide | Long term (≥ 4 years) |

| Higher type-2 diabetes and CVD burden | +1.5% | Concentrated in Eastern Province | Medium term (2-4 years) |

| Vision 2030 investment in centers & PPPs | +2.1% | Riyadh, Jeddah, Dammam | Medium term (2-4 years) |

| Early ERAS pathway adoption | +0.9% | Major tertiary hospitals | Short term (≤ 2 years) |

| National insurance inclusion from 2027 | +1.2% | All regions | Medium term (2-4 years) |

| Growing GCC medical-tourism inflow | +0.8% | Jeddah, Makkah, Riyadh | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Obesity Drives Surgical Demand

Adult obesity exceeded 40.6% in 2025, translating to more than 1.9 million candidates for metabolic procedures. Saudi clinical guidelines place surgery as first-line therapy for BMI ≥ 40 kg/m² or BMI ≥ 35 kg/m² with comorbidities, so procedure volumes climb faster than population growth. Urban dietary shifts and sedentary employment amplify prevalence in working-age cohorts, sustaining patient flow into high-volume centers. Obesity-related healthcare spending reached USD 110.6 billion in 2022, and cost-utility models show bariatric surgery at USD 31,909 per QALY, well within accepted thresholds, reinforcing payer willingness to reimburse[1]“Global Obesity Outlook 2025,” Dove Press, dovepress.com.

Vision 2030 Healthcare Infrastructure Investments Accelerate Market Growth

The government allocated SAR 65 billion (USD 17.3 billion) to expand surgical capacity through 2030. Projects such as Saudi German Hospital Makkah add 300 beds and dedicated operating suites, while plans to privatize 290 hospitals and 2,300 primary centers widen private sector roles. Digital initiatives like Seha Virtual Hospital enable remote pre-operative screening and follow-up, supporting the Saudi Arabia Bariatric Surgery market across underserved regions. These investments underpin long-run procedure growth beyond demographic effects.

Enhanced Recovery After Surgery Protocols Transform Operational Efficiency

ERAS adoption trims the average length of stay from two nights to a single night in 82% of robotic sleeve cases versus 32% for conventional laparoscopy. King Faisal Specialist Hospital leveraged AI patient-flow tools to cut bed wait from 32 to 6 hours, which lifted throughput and informed broader hospital network benchmarking. Consumable cost savings reached USD 355 per robotic case and, coupled with 93% patient-satisfaction scores, strengthen hospital economics and competitive positioning.

National Health Insurance Coverage Expansion Broadens Patient Access

The Cooperative Health Insurance Essential Benefit Package now reimburses up to SAR 15,000 (USD 4,000) per procedure, with co-payments capped at SAR 1,000 (USD 267). Full inclusion in national insurance from 2027 will remove BMI-specific restrictions imposed by some private payers and enlarge the addressable population. Private insurance enrollment already quadrupled from 3 million to 12 million lives, adding SAR 40 billion (USD 10.7 billion) in premium potential tied to bariatric benefits

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procedure and device costs | –1.4% | Rural areas most affected | Medium term (2-4 years) |

| Limited patient awareness outside tier-1 | –0.8% | Secondary cities and rural regions | Long term (≥ 4 years) |

| Shortage of bariatric-trained staff | –0.6% | Nationwide, acute in new centers | Medium term (2-4 years) |

| Post-operative weight regain | –0.5% | All facilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Procedure Costs Create Access Barriers

Robotic stapling adds a 47% premium over laparoscopy, raising direct device cost from USD 1,477 to USD 2,175 per case. Body-contouring surgeries remain self-paid for 94.1% of post-bariatric patients, revealing price elasticity even among high-BMI groups. Small hospitals shoulder SFDA registration fees that inflate procurement budgets and ultimately patient bills, especially where insurance ceilings are lower than actual invoices.

Workforce Development Challenges Constrain Service Expansion

The national fellowship pipeline struggles to match rising theater utilization. Bariatric anesthesia and surgical fellow seats remain scarce, and robotic proficiency requires 26 cases to achieve stable operative metrics. Dietitian shortages in emerging centers hamper long-term follow-up, contributing to variable outcomes and weight-regain episodes. International recruitment faces visa queues, and cultural adaptation slows onboarding, limiting rapid scale-up despite capital investments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Stapling Technologies Drive Market Leadership

Stapling Devices accounted for 35.12% of Saudi Arabia Bariatric Surgery market share in 2025 as they are integral to sleeve gastrectomy and gastric bypass workflows. The launch of the ETHICON 4000 Stapler in 2025 tightens staple-line security and is expected to defend share against multi-fire platforms introduced by competitors. Energy/Vessel-sealing Devices rise in tandem with robotic penetration, while Trocars & Access Instruments benefit from the procedural shift toward laparoscopy and reduced incision profiles.

Gastric Balloons, growing at 9.31% CAGR, attract lower-BMI patients seeking reversible options. Local clinics market the procedure aggressively to corporate wellness programs, broadening intake channels. Suturing Devices retain a niche but essential role in revision surgeries. Electrical Stimulation Systems remain small yet meaningful for high-risk cohorts unsuitable for staples. Domestic manufacturers pursue SFDA approvals for adjunct accessories, aligning with Vision 2030 targets to localize production and lift healthcare self-sufficiency.

By Procedure Type: Sleeve Gastrectomy Dominance Reflects Clinical Preferences

Sleeve Gastrectomy held 78.12% of the Saudi Arabia Bariatric Surgery market size in 2025. Surgeons favor the technique for its streamlined learning curve and consistent excess-weight loss. Procedure standardization and guideline endorsement reduce variability and support scale. Robotic platforms deliver enhanced visualization that helps maintain leak rates below 1%, reinforcing surgeon confidence.

Intragastric Balloon & Endo-Stapling grows at 9.42% CAGR as insurance policies begin covering balloons for BMI 30-35 kg/m² with comorbidities. Gastric Bypass retains utility in complex or revision scenarios, although longer operative times constrain throughput. Adjustable Gastric Banding continues to fade in popularity due to long-term explant needs and follow-up intensity, a trend mirrored across GCC peer markets. Registry data captured by the Saudi National Bariatric Surgery Registry informs continuous improvement initiatives and augments postoperative counseling.

By End User: Hospital Networks Leverage Scale Advantages

Hospitals managed 59.28% of procedures in 2025, capitalizing on intensive-care support, blood-bank services, and multidisciplinary teams. Large networks negotiate volume-based pricing with major suppliers, securing favourable terms for staplers, energy devices, and robotic consumables. Investment in AI-enabled patient scheduling lifts bed turnover, allowing hospitals to accommodate rising domestic and inbound medical tourists.

Ambulatory Surgical Centers, advancing at a 9.09% CAGR, differentiate through same-day discharge and bundled-price transparency. These centers partner with hotels for overnight stays when needed, creating a quasi-hospital environment without the fixed costs of extensive facilities. Dedicated Bariatric Clinics pursue accreditation from the European Accreditation Council for Bariatric Surgery, enhancing international credibility and capturing self-pay GCC visitors seeking quick scheduling.

Competitive Landscape

Market concentration is moderate, anchored by global device leaders with complete portfolios that span stapling, energy, and robotics. Johnson & Johnson MedTech launched direct Saudi operations in 2024, replacing distributor models to deepen surgeon engagement and align with Vision 2030 localization incentives[2]“Johnson & Johnson MedTech Expands in Saudi Arabia,” Healthcare Asia Magazine, healthcareasiamagazine.com. Medtronic maintains in-country education hubs that train residents on vessel-sealing and stapling systems, securing brand loyalty among rising procedure volumes.

Intuitive Surgical’s da Vinci systems set the current gold standard for robotic sleeve gastrectomy, yet makers of modular humanoid arms position new entries for 2026 tender cycles. Local manufacturing counts 206 factories with SAR 3.1 billion in cumulative investment, providing contract-manufacturing options for foreign brands seeking tariff advantages[3]“Medical Device Manufacturing Snapshot,” Medical Travel Market, medicaltravelmarket.com. The SFDA’s updated device code requires post-market surveillance audits, favoring firms with established quality systems and field-service teams capable of rapid compliance.

Hospitals form purchasing consortiums to leverage aggregated demand, elevating single-vendor contracts that reward comprehensive training and technical support. The move shifts negotiating power toward large health systems, pressuring smaller suppliers. Educational partnerships, such as Medtronic’s fellowship grants, bolster workforce expertise and indirectly drive device selection. The overall environment rewards firms that blend clinical evidence, cost-saving technologies, and in-country value creation.

Saudi Arabia Bariatric Surgery Industry Leaders

Medtronic PLC

Johnson and Johnson

Apollo Endosurgery Inc

B. Braun Melsungen AG

Conmed Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: ETHICON launched the 4000 Stapler system in Saudi Arabia with enhanced tissue compression technology that lowers leak risk during sleeve gastrectomy.

- March 2025: King Faisal Specialist Hospital advanced 20 ranks to join Newsweek’s global top-tier hospitals after a 10% rise in new patient admissions and 47% growth in medical-tourism volume.

- February 2024: Johnson & Johnson MedTech transitioned to direct operations in the Kingdom, strengthening clinical education and supply-chain responsiveness.

- September 2024: Saudi Arabia signed healthcare collaboration agreements with Morocco and Thailand to exchange best practices in digital health and specialized surgery, including bariatrics.

Saudi Arabia Bariatric Surgery Market Report Scope

Bariatric surgery or weight loss surgery is used as one of the major treatment procedures for treating obesity. It is generally the last option for patients who have failed to lose weight by several other means. During this procedure, the stomach size is reduced by either removing some parts of the stomach or using a gastric band.

The Saudi Arabian bariatric surgery market is segmented by device (assisting devices (suturing devices, closure devices, stapling devices, and other assisting devices), implantable devices, and other devices).

The report offers the value (in USD) for the above segments.

By Device

| Assisting Devices | Suturing Devices |

| Closure Devices | |

| Stapling Devices | |

| Trocars & Access Instruments | |

| Energy / Vessel-sealing Devices | |

| Implantable Devices | Gastric Balloons |

| Gastric Bands | |

| Electrical Stimulation Systems | |

| Other Devices (Robotic & Endoluminal Platforms) |

By Procedure

| Sleeve Gastrectomy |

| Gastric Bypass |

| Adjustable Gastric Banding |

| Intragastric Balloon & Endo-Stapling |

| Others |

By End User

| Hospitals |

| Specialised Bariatric Centers / Clinics |

| Ambulatory Surgical Centers |

| By Device | Assisting Devices | Suturing Devices |

| Closure Devices | ||

| Stapling Devices | ||

| Trocars & Access Instruments | ||

| Energy / Vessel-sealing Devices | ||

| Implantable Devices | Gastric Balloons | |

| Gastric Bands | ||

| Electrical Stimulation Systems | ||

| Other Devices (Robotic & Endoluminal Platforms) | ||

| By Procedure | Sleeve Gastrectomy | |

| Gastric Bypass | ||

| Adjustable Gastric Banding | ||

| Intragastric Balloon & Endo-Stapling | ||

| Others | ||

| By End User | Hospitals | |

| Specialised Bariatric Centers / Clinics | ||

| Ambulatory Surgical Centers | ||

Key Questions Answered in the Report

What is the current value of the Saudi Arabia Bariatric Surgery market?

The market generated USD 66.82 million in 2026 and is on track to reach USD 98.28 million by 2031.

How fast is procedure volume expected to grow?

Market revenue is predicted to rise at an 8.02% CAGR through 2031, supported by Vision 2030 investments and insurance expansion.

Which procedure is most commonly performed in Saudi Arabia?

Sleeve gastrectomy dominates, accounting for 78.12% of all bariatric surgeries completed in 2025.

What device category holds the largest share?

Stapling devices lead with 35.12% market share because they are essential for sleeve and bypass operations.

How will national insurance reform affect access?

Full inclusion starting in 2027 will remove copay and BMI restrictions, widening eligibility and likely accelerating surgical uptake.

Which care setting is growing the quickest?

Ambulatory Surgical Centres are projected to post a 9.09% CAGR as ERAS protocols enable same-day discharge.

Page last updated on: