Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

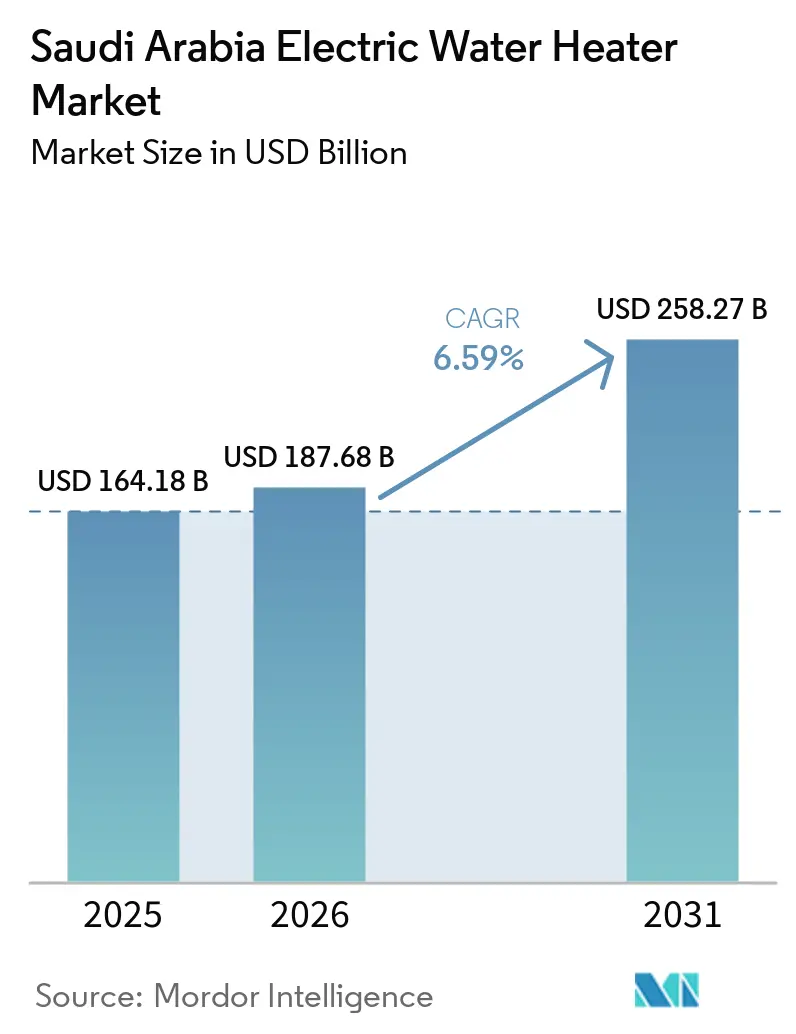

| Base Year Market Size (2025) | USD 164.18 Billion |

| Market Size (2026) | USD 187.68 Billion |

| Market Size (2031) | USD 258.27 Billion |

| Growth Rate (2026 - 2031) | 6.59% CAGR |

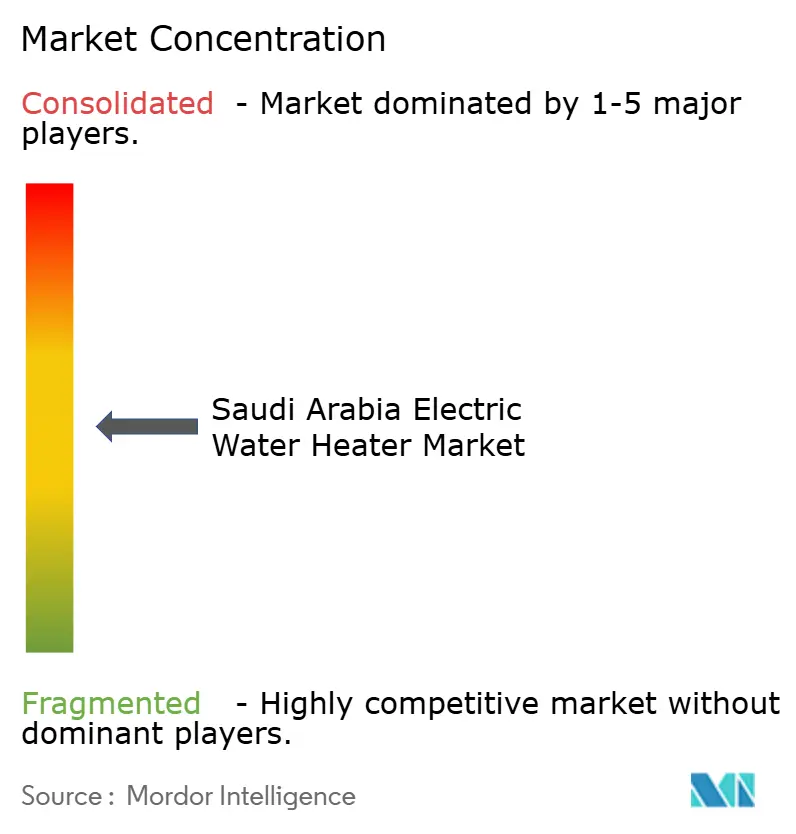

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Electric Water Heater Market Analysis by Mordor Intelligence

The Saudi Arabia electric water heater market size was valued at USD 164.18 billion in 2025 and estimated to grow from USD 187.68 billion in 2026 to reach USD 258.27 billion by 2031, at a CAGR of 6.59% during the forecast period 2026 to 2031. The growth outlook reflects policy-led momentum for efficient electric and heat pump systems, aided by Vision 2030 programs to lower household energy intensity that reinforce spending shifts toward high-efficiency models[1]Saudi Energy Efficiency Center, “Programs and Targets for Household Energy Intensity,” Saudi Energy Efficiency Center, seec.gov.sa. Regulatory tightening by the Saudi Standards, Metrology and Quality Organization pushes the market toward better-insulated tanks, smart-connected controls, and heat pump water heaters that reduce standby losses and total energy draw[2]Saudi Standards, Metrology and Quality Organization, “Energy Efficiency and Labeling for Appliances,” SASO, saso.gov.sa. Smart, connected electric units and heat pumps are gaining share as suppliers highlight energy savings and comfort benefits in new housing and hospitality projects, with product portfolios optimized for Gulf operating conditions. E-commerce reach into secondary cities supports faster adoption of compact electric models, while utility smart-meter rollouts improve the payback case for scheduled heating and demand-response features.

Key Report Takeaways

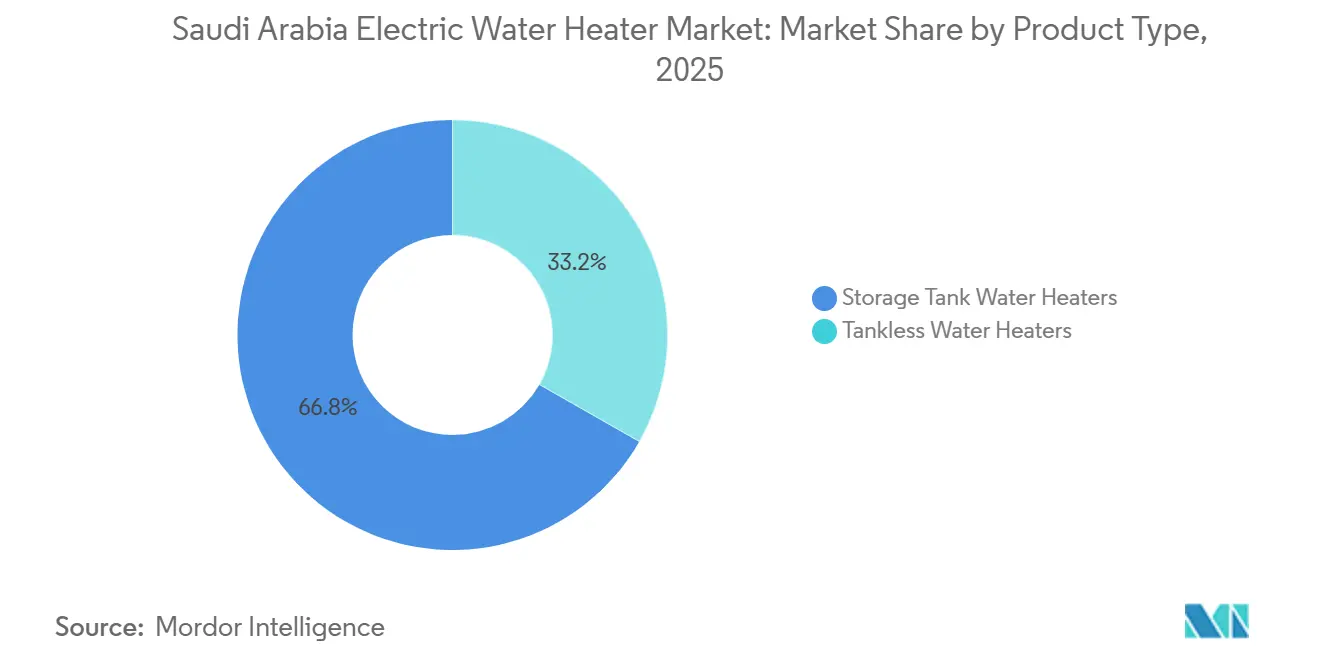

- By product type, storage tank models led with 66.76% revenue share in 2025, while tankless units are forecast to expand at a 7.18% CAGR to 2031.

- By capacity, the 31–100-liter segment accounted for 45.73% share in 2025, and <30-liter small units are projected to grow at a 6.68% CAGR through 2031.

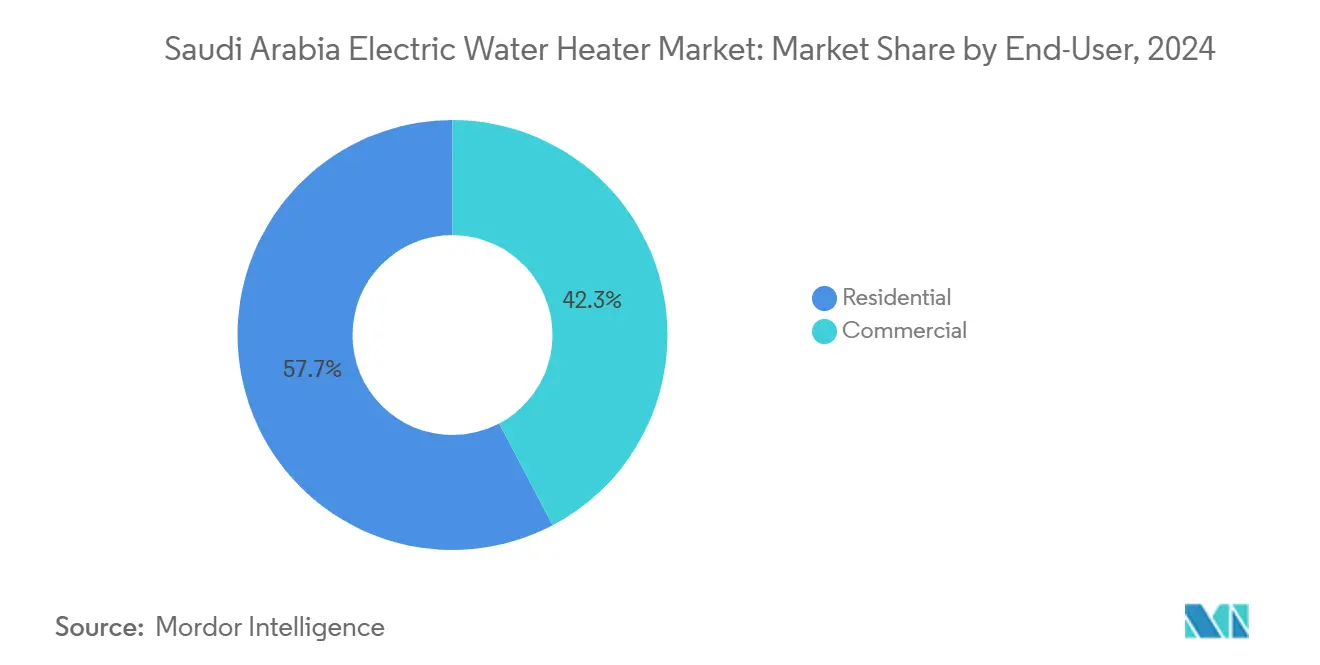

- By end user, residential held 57.73% in 2025, while commercial is set to record a 6.94% CAGR through 2031.

- By distribution channel, offline accounted for 63.84% in 2025, whereas online is projected to rise at an 8.43% CAGR to 2031.

- By geography, the Central Region (Riyadh) captured 28.96% in 2025, and the Western Region is forecast to be the fastest-growing at a 7.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Electric Water Heater Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enforced energy-efficiency and safety standards | +1.8% | National, strongest in Central and Western regions under SASO oversight | Medium term (2-4 years) |

| Electric and storage format alignment with Kingdom of Saudi Arabia practices | +1.2% | National, with concentrated impact in Eastern Province | Long term (≥ 4 years) |

| Residential build-out and hospitality pipeline | +2.1% | Riyadh and Jeddah growth corridors, Western Province clusters | Short term (≤ 2 years) |

| Residential segment leadership and replacement cycles | +1.4% | National, with above-average contribution in the Central Region | Long term (≥ 4 years) |

| GSO 2770:2024 harmonization across GCC | +1.1% | GCC-wide, early gains in Riyadh, Jeddah, Dammam | Medium term (2-4 years) |

| Rapid online channel penetration | +0.9% | National, stronger growth in secondary cities with high 5G coverage | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Enforced Energy-Efficiency and Safety Standards Accelerate Replacement and Premiumization

Saudi Arabia adopted GSO 2770:2024 in October 2024, establishing minimum energy performance for electric storage, instantaneous, and heat pump water heaters, which is reshaping product portfolios and accelerating the exit of models with high standby losses. SASO’s SABER platform ties energy labels to import and market access, which elevates the importance of verified performance claims and reduces the circulation of non-compliant units. The 2026 tightening of insulation and standby-loss thresholds is expected to steer demand into premium features such as Wi-Fi scheduling, demand-response readiness, and heat pump architectures designed for Gulf climates. Manufacturers are emphasizing high Coefficient of Performance ranges, advanced refrigerants, and digital controls to cut wasted energy during off-peak periods. Together, these measures align supply with Vision 2030’s energy-intensity goals while giving consumers clearer signals to replace legacy stock with efficient electric and heat pump alternatives.

Residential Build-Out and Hospitality Pipeline Expand Installed Base and New Demand

Housing delivery under Vision 2030 expanded in 2024, with beneficiary families supported through the Sakani program, providing a solid base for first installs across new urban communities. Large-scale residential communities such as ROSHN’s ALMANAR in Makkah anchor multi-year procurement for SASO-compliant electric systems that match mid-capacity household needs. The New Murabba development in Riyadh, which includes a major residential component, is shaping specifications toward smart-ready and grid-interactive electric water heating that integrates with planned district-wide digital infrastructure. In hospitality, headline projects announced by master developers in Jeddah and the Red Sea zone specify centralized, high-efficiency electric and heat pump clusters that meet safety and hygiene protocols in hot water systems. These residential and commercial buildouts create durable tailwinds for electric formats as developers standardize on efficient products that meet SASO and GSO frameworks and fit into smart building and smart grid plans.

GSO 2770:2024 Harmonization Enables Roll-Out of High-Efficiency Electric/HPWH Across GCC

The Gulf-wide GSO 2770:2024 framework harmonizes minimum energy performance and testing for electric and heat pump water heaters, streamlining conformity for multi-country product rollouts. The inclusion of heat pump categories and alignment to Gulf ambient profiles encourages suppliers to prioritize high-COP designs that remain efficient in local temperatures. Regional production footprints and certification know-how shorten time-to-market for suppliers with established Gulf operations, improving the availability of premium electric solutions. Harmonization also eases cross-border procurement for hospitality and multi-property operators that prefer uniform specifications and consolidated service models[3]GCC Standardization Organization, “GSO 2770:2024 Minimum Energy Performance Requirements,” GCC Standardization Organization, gso.org.sa. As the Saudi Electricity Company continues smart meter and network upgrades, demand-response-compatible electric heating becomes easier to schedule against time-of-use signals, adding to the business case for high-efficiency electric formats.

Rapid Online Channel Penetration Extends Reach to Secondary Cities and Mid-Market

E-commerce growth is supported by near-universal internet access and broad 5G coverage, which expands consumer reach for connected appliances, including water heaters. Electronic payment infrastructure continues to deepen, with card-based digital transactions on scale, which support large-ticket appliance purchases online. Leading platforms in the Kingdom have expanded fulfillment capacity and delivery speed, which brings compact electric models and installation services to cities beyond the main metros. Product pages, verified reviews, and localized content reduce consumer hesitation about smart features and high-efficiency options. Promotional windows around key shopping periods support the trial of heat pump and smart-electric models, while integrated installation and warranty bundles improve conversion for price-sensitive buyers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront and electrical upgrade needs for tankless | -1.4% | National, with a greater impact in areas with limited three-phase coverage | Medium term (2-4 years) |

| Competition from gas, solar, and hybrid configurations | -0.7% | Coastal villa clusters and high-demand commercial hot water loads | Long term (≥ 4 years) |

| Stricter SASO conformity and labeling costs | -0.9% | National, all categories are subject to SABER and notified body testing | Short term (≤ 2 years) |

| Hard-water scaling and maintenance costs | -0.6% | Central and Eastern provinces with high TDS and hardness profiles | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront and Electrical Upgrade Needs for Tankless

Slow Adoption of electric tankless deployment often requires higher-capacity wiring and panel upgrades, which can raise installed costs relative to conventional storage tanks and limit mass adoption in price-sensitive segments[4]Saudi Electricity Company, “Service Levels and Grid Readiness,” Saudi Electricity Company, se.com.sa. In parts of the Northern and Southern belts, three-phase coverage lags major urban centers, which constrain multi-unit tankless specifications in large residential blocks without added utility work. Developers in affordable projects balance energy savings with capital budgets, so higher upfront electrical work can keep tankless penetration below potential even when lifecycle savings are favorable. Pilot programs that incentivize off-peak electric heating can improve paybacks, but broader time-of-use adoption and streamlined installation financing would further support tankless growth. Until those enablers scale, storage tanks will remain the default in many installations because they match existing electrical service levels and do not require panel retrofits.

Competition for Gas/Solar/Hybrid Solutions in Larger/Commercial Uses

Electric water heating competes with natural gas, solar thermal, and hybrid thermal-electric systems in villas and high-load commercial applications, where rooftop area and system integration can favor pre-heating strategies. In large hotels and healthcare settings, solar pre-heat and centralized plant designs can reduce the duty of electrical elements when combined with thermal storage, which trims operating costs and meets sustainability targets. Gas-fired solutions remain present in some greenfield communities and industrial facilities, which can curb the electricity-only share in specific pockets where gas availability and building design make it viable. Electric systems retain an edge in high-rise buildings that prioritize fire-code simplicity and the absence of combustion, which is a factor in dense urban projects across Riyadh and Jeddah. As developers adopt hybridized strategies, the electric segment’s opportunity shifts toward heat pump arrays and smart controls that maximize the electric portion of the load with efficient scheduling.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: On-Demand Efficiency Closes Gap on Storage

Incumbency Storage tanks held 66.76% of 2025 revenue as installers, developers, and households leaned on proven performance, straightforward maintenance, and lower upfront cost profiles. Water hardness in central zones also supports tank-based designs with robust anodes and scheduled decaling, which helps maintain performance and prolong useful life when treatment is limited. At the same time, tankless adoption is growing faster, with a 7.18% CAGR forecast through 2031, supported by regulations that make standby-loss performance a more visible purchase criterion. Smart-ready, on-demand configurations suit high-density buildings and space-constrained apartments, and developers are now specifying connected controls with scheduling and usage analytics. Giga-projects like NEOM and Red Sea properties have issued specifications for electric systems that are grid-interactive and efficient across daily peak patterns, which position tankless and hybridized electric arrays for premium duty cycles. In the near term, storage will continue to anchor base demand, while on-demand gains are likely to concentrate on new-build hospitality and smart apartment clusters.

From a total addressable demand perspective, electric-only formats continue to benefit from safety, code compliance, and interoperability with smart meters and building management systems. Premium storage units that integrate heat pump modules reinforce the efficiencies of on-demand while preserving hot water availability during peak usage windows. As scheduling and demand-response signals reach more buildings, the Saudi Arabia electric water heater market is set to shift toward connected electric configurations that meet SASO label thresholds without sacrificing comfort. The segment’s mix shift keeps the Saudi Arabia electric water heater market efficient even as volumes rise, which supports suppliers that lead in controls, insulation, and refrigerant technology.

By Capacity: Medium Units Anchor Baseline; Small Format Rides E-Commerce Wave

The medium-sized units commanded 45.73% share in 2025, aligning with prevalent household sizing and standard building specifications for new urban communities. Mid-capacity tanks match distribution pressure, flow patterns, and multi-point use, which makes them the default in first installs across mainstream residential projects. Small units below 30 liters are the fastest growing, with a 6.68% CAGR outlook, helped by online availability, same-day delivery options, and the suitability of point-of-use for rental stock and secondary cities. As new homes add smart meters, schedule-based heating improves energy outcomes across all capacities, which supports efficiency gains beyond unit-level ratings. E-commerce platforms and large retailers are expanding SKU depth in compact sizes, often bundled with installation, which addresses adoption barriers in smaller dwellings.

Large-capacity systems remain a smaller portion of residential demand, yet they are integral to hotels, hospitals, and multi-dwelling buildings using centralized plant rooms that allocate hot water to multiple floors. In these settings, heat pump arrays and insulated thermal storage can reduce overall load on electric elements while meeting hygiene and temperature stability requirements. With residential growth underway and procurement centralizing in large communities, the Saudi Arabia electric water heater market size for mid-capacity products is supported by a steady formation of households and developer-standard specifications. In smaller homes and add-on applications, point-of-use units keep expanding via online channels, contributing to category depth and consumer awareness of connected electric options.

By End User: Residential Baseline Meets Commercial Premium Trajectory

Residential accounted for 57.73% of 2025 revenue, anchored by sustained housing delivery and the baseline need for reliable hot water in primary residences. Replacement cycles in hard-water zones sustain recurring demand, which stabilizes volumes across economic cycles since water heating is a non-discretionary function in occupied homes. Smart-ready units add value at the household level by aligning run-times with off-peak tariffs, which support total energy savings and reinforce consumer acceptance of connected electric solutions. The residential segment’s steady advancement sets a floor for industry volumes, while product upgrades elevate average selling prices as features shift toward connectivity and higher thermal performance.

Commercial installations are projected to grow at a 6.94% CAGR to 2031, with hotels, healthcare, and mixed-use complexes deploying centralized heat pump and smart-controlled electric solutions to meet load, safety, and hygiene requirements. Projects under master developers in Jeddah and along the Red Sea are specifying high-efficiency electric arrays for plant rooms, which benefits suppliers with strong GCC certification pathways and service networks. Centralized systems that integrate with building management platforms support temperature stability and Legionella control protocols, which favor premium electric and heat pump systems. The Saudi Arabia electric water heater market benefits as these commercial clusters scale, strengthening the case for higher-efficiency electric portfolios.

By Distribution Channel: Offline Incumbency Faces Digital Disruption

Offline accounted for 63.84% of 2025 revenue on the strength of long-standing installer relationships and the need for immediate replacement in both residential and commercial settings. In regions with high hardness and variable water quality, in-person consultation remains preferred, which sustains store-based sales for tank selection, anodes, and water treatment options. However, online is the fastest-growing channel at an 8.43% CAGR, supported by near-universal internet usage, high 5G coverage, and deepening logistics and payments. As platforms extend same-day delivery and integrate installation booking, connected and compact electric models reach more consumers in secondary cities, which accelerates digital penetration.

Online storefronts are also important for showcasing energy labels, certifications, and smart features in a uniform presentation that builds confidence in performance claims. Offline and online channels converge when installers and retailers adopt QR-enabled verification and digital manuals, while marketplaces add verified partners to expand installation coverage. The Saudi Arabia electric water heater market gains from this channel shift as education, reviews, and transparent specs reduce the perceived risk of adopting heat pump and smart-electric formats. Over the forecast, the Saudi Arabia electric water heater market size grows across both channels, with digital likely outpacing in percentage terms as logistics density and payment friction continue to improve.

Geography Analysis

The Central Region, anchored by Riyadh, captured 28.96% of value in 2025 on the back of ongoing residential delivery and large-scale mixed-use communities that standardize SASO-compliant and smart-ready electric systems. Central projects that require grid-interactive appliances are aligning specifications with utility smart-meter programs to run heaters in off-peak windows and improve household energy intensity. Water hardness in the Central Region necessitates attention to anode design and scale mitigation, which keeps service and replacement consistent in the installed base. New Murabba’s residential component supports long-term adoption of connected electric units due to smart-city integration plans and developer-led standardization. The Saudi Arabia electric water heater market in this region will benefit from continued household formation and replacement cycles that favor efficient electric options.

The Western Region is forecast to be the fastest-growing at a 7.62% CAGR to 2031 as residential and hospitality expansions proceed in Jeddah, Makkah, and Madinah. Jeddah Central’s flagship projects and the broader Red Sea pipeline are increasing demand for centralized electric and heat pump clusters that meet high service-level requirements. Desalinated water is a major supply source along the western coast, which requires attention to remineralization and chemistry in hot water systems, with manufacturers adapting anodes and coatings accordingly. The Saudi Arabia electric water heater market will see higher average selling prices in premium hospitality properties due to advanced controls and heat pump arrays designed for plant rooms. As new hotels and mixed-use districts scale, Western cities provide a strong pull for high-efficiency electric solutions that can be managed through building platforms and comply with safety protocols.

The Eastern Province accounts for a significant share of value, with industrial and residential communities in Dammam, Al Khobar, and Dhahran driving both first installs and replacements. Variable groundwater salinity and hardness in parts of the province require careful system specification, including inhibitors and periodic maintenance for electric tanks, which influences the total cost of ownership. Utility upgrades and smart meter deployments support scheduled heating, which helps optimize electric loads in residential and commercial buildings. Northern and Southern regions benefit from large-scale developments and tourism clusters, which support premium electric specifications in select projects while broadening basic electric storage adoption elsewhere. Over the forecast, the Saudi Arabia electric water heater market size across these regions advances with differing mixes of storage, tankless, and heat pump systems shaped by water quality, building types, and utility readiness.

Competitive Landscape

The market shows moderate concentration, with the top five vendors accounting for about half of the value in 2025, which leaves room for specialist brands and new digital-first entrants. Incumbents gain from faster SASO approvals and established GCC certification processes, which enable rapid listing of compliant electric and heat pump SKUs. Localization in assembly and training helps reduce delivery times and support installers with upskilling on heat pumps and connected controls. Differentiation centers on energy efficiency, connectivity, and service reliability for centralized systems in hotels, hospitals, and multi-dwelling projects. As developer procurement shifts toward integrated packages, suppliers that bundle products, installation, and service contracts are positioned to consolidate share.

Strategic moves underscore this trajectory. Rheem opened an Innovation Learning Center in Riyadh to train contractors on high-efficiency solutions, which strengthens installer preference. Ariston showcased next-generation heat pump water heating and smart connected tanks designed for Gulf climates, highlighting reduced standby and operating energy. A. O. Smith announced price actions and manufacturing shifts to improve supply and margins in premium segments, which signals a focus on efficient products. Bosch expanded its home comfort capacity through acquisition, enabling broader cross-selling opportunities in integrated comfort and water systems. These moves align with the Saudi Arabia electric water heater market's emphasis on efficient and connected solutions that meet tightening standards.

Digital commerce and direct-to-consumer strategies create additional competitive angles. Local e-commerce players now bundle installation and warranty services with electric tanks, offering alternatives to traditional distributor-led channels. As the SEC advances smart metering and demand-response signals, vendors with grid-ready controls can secure rebates and preference in pilot programs. In premium hospitality, centralized heat pump arrays and plant room integration require field support and monitoring that favor established service networks. The Saudi Arabia electric water heater market continues to reward suppliers that combine compliance speed, localized support, and digital ease-of-use in both residential and commercial deployments.

Saudi Arabia Electric Water Heater Industry Leaders

Rheem Manufacturing

Ariston Thermo

A. O. Smith

Saudi Ceramics Company

Orbital Horizon (O-Horizon)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Carrier launched an integrated air-to-water heat pump for residential energy management, combining whole-home temperature control with domestic hot-water supply, positioning it as an efficient alternative to fossil-fuel-based boilers and traditional electric heaters for new constructions and renovations across GCC markets, including Saudi Arabia.

- January 2026: Midea introduced an energy-efficient heat pump water heater for North American homes, highlighting a broader shift from conventional to advanced air-source technology, and positioning Midea for Middle East market entry through distributors targeting Saudi Arabia's Western Province hotel clusters.

- November 2025: Ariston unveiled next-generation sustainable water-heating solutions at Big 5 Global 2025 in Dubai, including the Nuos FIT advanced heat-pump system and Velis Tech WiFi, reinforcing the company’s GCC presence and preparedness for SASO’s tightening standards.

- November 2025: Jeddah Central Development Company partnered with Midad Real Estate to develop Atlantis and One&Only hotels in Jeddah Central’s Beach, Leisure & Lifestyle district, with implications for centralized electric water-heating procurement in expanding hospitality projects.

Saudi Arabia Electric Water Heater Market Report Scope

An electric water heater is an appliance that heats cold water using electricity and is supplied through a system of pipes. This heated water can be used for various purposes, such as taking a hot bath or shower, and in washing machines and dishwashers. Over the decades, several technologies have been developed to make water heaters energy efficient.

The Saudi Arabia Electric Water Heater Market is segmented by product type, capacity, end user, distribution channel, and geography. By product type, the market is divided into storage tank water heaters and tankless water heaters. By capacity, the market is categorized into small, medium, and large water heaters. By end user, the market is segmented into residential and commercial segments. By distribution channel, the market is divided into online and offline channels. Geographically, the market analysis covers the Central Region, Western Region, Eastern Region, Southern Region, and Northern Region of Saudi Arabia. The report provides market size and forecasts for the Saudi Arabia electric water heater market in value (USD) across all the above segments.

By Product Type

| Storage Tank Water Heaters |

| Tankless Water Heaters |

By Capacity

| Small |

| Medium |

| Large |

By End Users

| Commercial |

| Residential |

By Distribution Channels

| Online |

| Offline |

By Geography

| Central Region |

| Western Region |

| Eastern Region |

| Southern Region |

| Northern Region |

| By Product Type | Storage Tank Water Heaters |

| Tankless Water Heaters | |

| By Capacity | Small |

| Medium | |

| Large | |

| By End Users | Commercial |

| Residential | |

| By Distribution Channels | Online |

| Offline | |

| By Geography | Central Region |

| Western Region | |

| Eastern Region | |

| Southern Region | |

| Northern Region |

Key Questions Answered in the Report

What is the current size and growth outlook of the Saudi Arabian electric water heater market?

The Saudi Arabia electric water heater market size was USD 164.18 billion in 2025 and is expected to reach USD 258.27 billion by 2031 at a 6.59% CAGR over 2026–2031.

Which product type leads and which grows fastest in Saudi Arabia?

Storage tanks led with 66.76% revenue share in 2025, while tankless units are projected to grow the fastest at a 7.18% CAGR through 2031.

What end-user segments drive demand in Saudi Arabia?

Residential held 57.73% of revenue in 2025 due to steady first installs and replacements, while commercial is forecast to expand at a 6.94% CAGR, led by hospitality and healthcare projects.

Which regions show the strongest momentum within Saudi Arabia?

The Central Region accounted for 28.96% of the 2025 value, and the Western Region is the fastest-growing with a 7.62% CAGR outlook to 2031 due to large residential and hospitality developments.

How are regulations influencing product choices in Saudi Arabia?

SASO and GSO 2770:2024 standards are raising energy-performance thresholds, steering demand toward insulated tanks, smart-ready controls, and heat pump water heaters optimized for Gulf conditions.

What channels will grow fastest for electric water heaters in Saudi Arabia?

Online channels are projected to grow at an 8.43% CAGR as internet access and logistics deepen, while offline still dominates due to installer relationships and immediate replacement needs.

Page last updated on: