Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

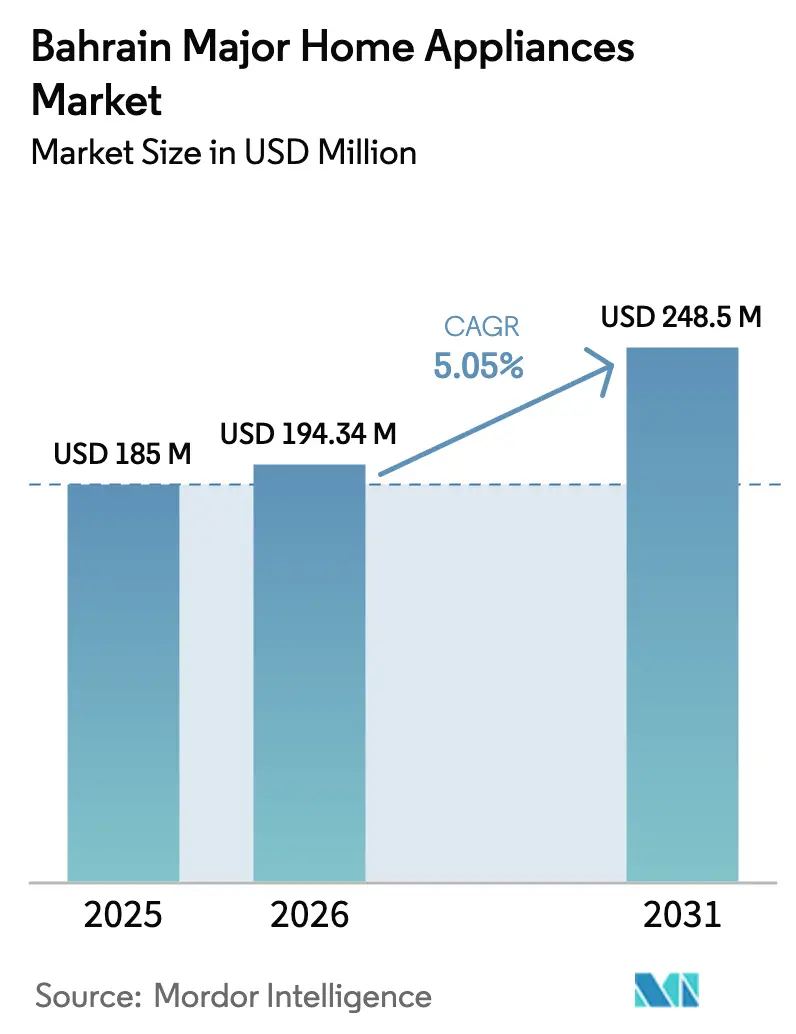

| Base Year Market Size (2025) | USD 185 Million |

| Market Size (2026) | USD 194.34 Million |

| Market Size (2031) | USD 248.5 Million |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bahrain Major Home Appliances Market Analysis by Mordor Intelligence

The Bahrain major home appliances market size in 2026 is estimated at USD 194.34 million, growing from 2025 value of USD 185 million with 2031 projections showing USD 248.5 million, growing at 5.05% CAGR over 2026-2031. Growth reflects the kingdom’s USD 30 billion infrastructure pipeline, rapid housing delivery, and a services-heavy economy that continually renovates retail and hospitality assets[1]International Trade Administration, “Bahrain – Country Commercial Guide,” trade.gov. Manufacturers benefit from a young, digitally engaged consumer base, robust internet penetration, and government incentives that reward energy-efficient technologies aligned with Vision 2030. At the same time, supply chain turbulence and elevated freight costs are prompting inventory realignment, encouraging regional sourcing, and intensifying price competition[2]Leslie Josephs, “Container Rates Surge as Red Sea Crisis Persists,” CNBC, cnbc.com. The interplay of purchaser optimism, regulatory tightening on efficiency, and channel digitization positions the Bahrain major home appliances market for steady value creation across refrigerators, washing machines, air conditioners, and complementary categories.

Key Report Takeaways

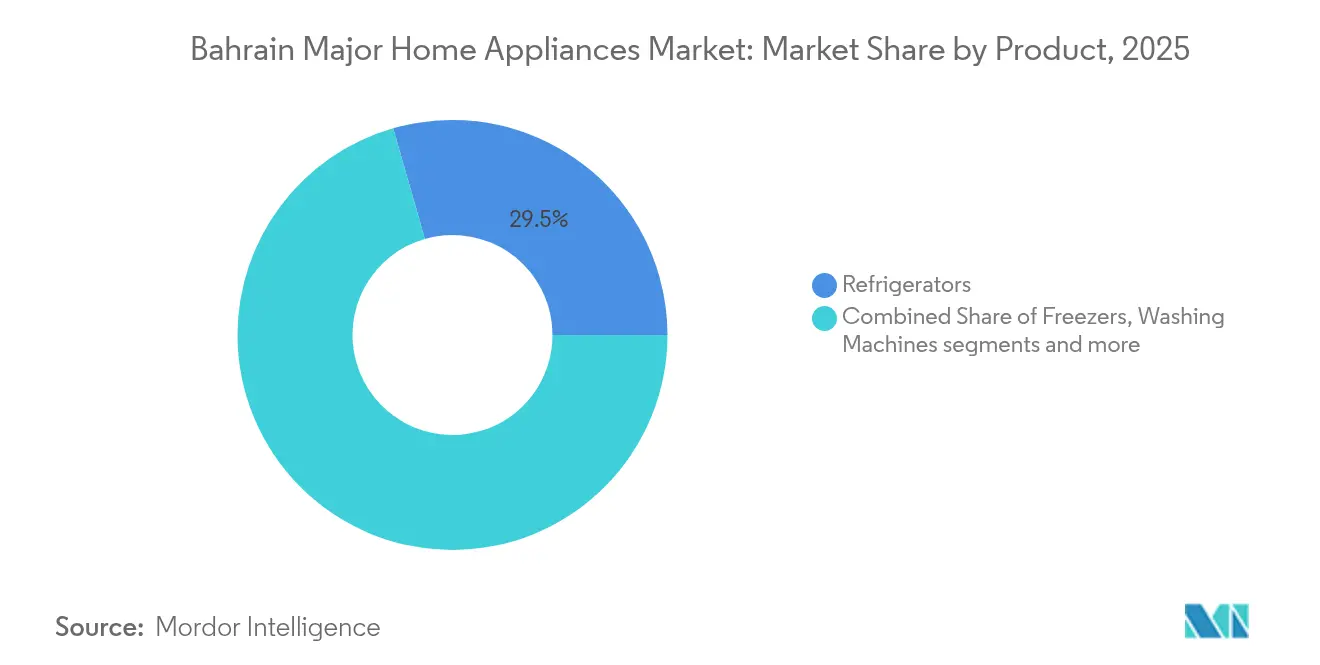

- By product, refrigerators led with 29.45% of Bahrain's major home appliances market share in 2025, while washing machines are poised for the fastest 5.72% CAGR through 2031.

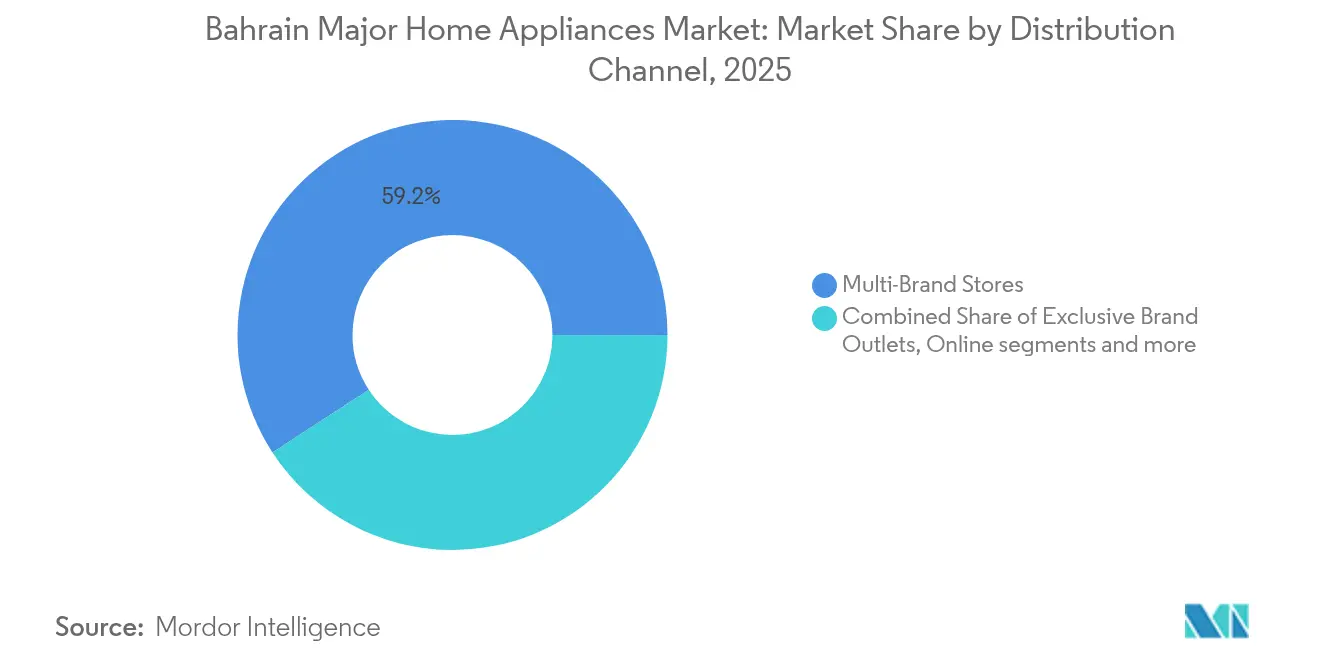

- By distribution channel, multi-brand stores held 59.20% of revenue in 2025, whereas online channels are set to expand at a 6.05% CAGR to 2031.

- By geography, Capital Governorate accounted for 44.40% of Bahrain's major home appliances market share in 2025; Northern Governorate is projected to climb at a 5.32% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bahrain Major Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Disposable Income and Housing Projects | +1.2% | National, concentrated in Capital and Northern Governorates | Medium term (2-4 years) |

| Mandatory Energy-Efficiency Labelling (MEPS) | +0.8% | National, with stronger adoption in urban areas | Long term (≥ 4 years) |

| Expansion of E-Commerce Fulfilment Capacity | +0.6% | National, led by Capital Governorate | Short term (≤ 2 years) |

| Demand for Smart & Connected Appliances | +0.9% | Capital and Muharraq Governorates primarily | Medium term (2-4 years) |

| Tourism-Driven Demand from Short-Stay Rentals | +0.4% | Capital and Muharraq Governorates | Short term (≤ 2 years) |

| Urbanization and Infrastructure Development | +1.1% | Northern and Capital Governorates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Income and Housing Projects

Bahrain is building 40,000 new housing units, of which 20,000 are already under construction, under a government-backed program that stimulates large-ticket household spending. Unit demand surges across refrigeration, laundry, cooking, and air-conditioning categories as new homeowners replace most of their appliances within a short period. The USD 7 billion BAPCO modernization and USD 3.5 billion King Hamad Causeway create jobs that raise middle-class earnings and underpin durable-goods purchases. As deliveries accelerate through 2030, the Bahrain major home appliances market will continue to benefit from first-time outfitting and replacement sales in newly occupied residences.

Mandatory Energy-Efficiency Labelling (MEPS)

GCC-wide Minimum Energy Performance Standards now influence specification choices, and Bahrain’s alignment with these codes is steering buyers toward higher-rated refrigerators, washing machines, and air conditioners. Residential usage accounts for 50% of GCC electricity, making efficient appliance selection a priority for both policymakers and households. Manufacturers able to verify superior kilowatt-hour performance receive an immediate competitive edge and avoid penalties linked to sub-standard models. Because national implementation often serves as a template for neighboring states, compliance success in Bahrain can open wider Gulf opportunities. Over the long term, mature enforcement should lift premium product penetration and moderate household energy bills, sustaining replacement cycles.

Expansion of E-Commerce Fulfilment Capacity

Major retailers logged 70% year-over-year online sales growth in 2024, while e-commerce captured 4.5% of total retail turnover[3]Staff Report, “Lulu’s Online Sales Jump 70% in GCC,” Zawya, zawya.com. Lulu Retail, for example, opened 21 additional stores and doubled down on last-mile delivery hubs that shorten appliance lead times to under 24 hours within Manama. Young digital natives appreciate comparison shopping, installment plans, and doorstep installation, encouraging large refrigerated or laundry items to shift online. Improved payment gateways and omnichannel inventory visibility further diminish historic barriers that favored physical showrooms. As a result, the Bahrain major home appliances market now rewards brands offering frictionless click-to-deliver journeys and unified after-sales support.

Demand for Smart & Connected Appliances

High smartphone penetration and reliable broadband services push consumers to expect home devices that self-diagnose, optimize energy, and integrate with voice assistants. Panasonic’s 2024 regional strategy introduced 74 new SKUs, including Matter-enabled refrigerators and AI-assisted washers, underscoring how intelligence has become a core value proposition[4]Panasonic Marketing Middle East, “Panasonic Unveils 2024 Strategy,” panasonic.com. In Bahrain’s urban districts, Wi-Fi-ready models command premium margins because buyers perceive long-term savings and convenience. Utility companies promoting peak-load management also encourage smart functionality that can throttle consumption in real time. These factors collectively expand the addressable customer base for connected appliances over the medium term, adding momentum to the Bahrain major home appliances market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Import-Price Volatility Linked to Global Freight | -0.8% | National, affecting all distribution channels and price points | Short term (≤ 2 years) |

| High Electricity Tariffs for Upper-Consumption Slabs | -0.6% | National, with stronger impact in residential high-consumption segments | Medium term (2-4 years) |

| Consumer Price Sensitivity | -0.5% | National, concentrated in middle and lower-income demographics | Short term (≤ 2 years) |

| Limited Domestic Manufacturing | -0.4% | National, affecting supply chain resilience and import dependency | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Import-Price Volatility Linked to Global Freight

Ocean freight rates surged past USD 20,000 per container in 2024 following Red Sea disruptions, raising landed costs in Bahrain’s import-dependent appliance sector. General rate increases of 140% squeezed mid-range suppliers with limited hedging capacity, prompting inventory cuts and lengthier stock-out periods. Retailers responded by favoring regional production, bulk orders, and shorter payment terms to manage cash flow. Consumers reacted to price inflation by postponing non-essential upgrades, amplifying price elasticity in categories like dishwashers. Although rates are expected to normalize gradually, the lingering volatility encourages contingency sourcing strategies for participants in the Bahrain major home appliances market.

High Electricity Tariffs for Upper-Consumption Slabs

Bahraini residential tariffs rise steeply once consumption passes designated thresholds, discouraging purchases of energy-intensive devices such as high-tonnage air conditioning systems[5]Mohammed Al-Suwaidi, “Residential Energy Consumption in the GCC,” ScienceDirect, sciencedirect.com. Households in upper slabs frequently downgrade capacity or opt for inverter technology that limits peak draw. This behavior tempers overall unit sales, particularly in the peak summer quarter when electricity bills escalate. The policy simultaneously accelerates the adoption of advanced efficiency features, benefiting brands able to document clear savings. Over the medium term, the tariff structure will continue to shape the product mix, influencing how the Bahrain major home appliances market balances volume growth with efficiency upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Refrigerators Lead, While Washing Machines Accelerate

Refrigerators captured 29.45% of Bahrain major home appliances market share in 2025, reflecting both indispensability and an 8-10 year replacement rhythm. The category’s consistent throughput sustains supplier economies of scale and underpins showroom traffic levels. Advancements in inverter compressors, modular storage, and smart diagnostics now allow brands to upsell premium lines without alienating price-sensitive shoppers. The Bahrain major home appliances market consequently sustains a broad pricing ladder ranging from basic top-mount designs to French-door models equipped with IoT dashboards.

Washing machines, projected to grow at a 5.72% CAGR to 2031, illustrate how urban lifestyles favor time-saving automation. Dual-income households increasingly demand larger drum capacity and wrinkle-free cycles that integrate with wardrobe care apps. Front-load sales are rising faster than top-load alternatives because of perceived water and energy advantages consistent with MEPS. Noise-reduction enhancements also matter in apartment settings common across Manama and Isa Town. Over the forecast window, laundry brands prioritizing slim-depth chassis and smartphone troubleshooting are well positioned to enlarge their Bahrain major home appliances market presence.

By Distribution Channel: Multi-Brand Dominance Faces Digital Disruption

Multi-brand stores accounted for 59.20% of retail value in 2025, underlining Bahraini shoppers’ preference for side-by-side model comparison and immediate stock availability. Within these showrooms, bundled discounts on refrigerator-washing machine pairs remain a proven conversion tactic. The Bahrain major home appliances market size attributable to physical retail is projected to grow modestly as chains refurbish displays and pivot toward experiential layouts featuring connected-home demos. Retailers also allocate greater floor space to high-margin built-in ranges that target villa renovations.

Online platforms, rising at a 6.05% CAGR, are transforming purchase journeys through enriched content, augmented-reality placement tools, and same-day deliveries within the Capital Governorate. A growing share of traffic originates from social commerce links that redirect directly to checkout, simplifying high-value transactions. Exclusive brand-outlet websites further enhance omnichannel cohesion by enabling in-store pick-up and free returns, reassuring hesitant first-time digital buyers. As fulfillment reliability improves, the Bahrain major home appliances market expects digital revenue percentage to climb into double digits before 2031, compressing negotiating margins for brick-and-mortar intermediaries yet widening overall consumer reach.

Geography Analysis

Capital Governorate retained 44.40% of Bahrain major home appliances market size in 2025, commanding enduring leadership within the market, reflecting higher disposable incomes, and dual demand from residential sectors. Manama’s shopping malls consolidate multiple showroom brands that display the latest inverter refrigerators, smart washers, and advanced cooking ranges. Industry feedback indicates urban consumers are more willing to pay a premium for smart functions that synchronize with energy-monitoring apps.

Northern Governorate is the fastest-growing territory, recording a 5.32% CAGR, buoyed by subsidized mortgage schemes and extensive road upgrades linking new suburbs to employment hubs. Developers bundle kitchen and laundry packages into turnkey hand-overs, creating bulk opportunities for manufacturers able to deliver on time and install at scale. Lower land costs also attract build-to-rent investors furnishing properties for expatriate professionals, a segment keen on mid-tier yet reliable appliance brands. Over the forecast horizon, the Bahrain major home appliances market expects Northern Governorate’s contribution to steadily rise, pressing retailers to establish service centers closer to expanding communities.

Muharraq Governorate maintains momentum through aviation and tourism synergies; proximity to the airport favors apartment rentals marketed on short-stay platforms. Property owners replace refrigerators and washers frequently to retain favorable guest reviews, channeling continuous replacement demand into the Bahrain major home appliances industry. Southern Governorate remains the smallest, but its industrial zones are upgrading worker accommodation and logistics depots, creating a niche for robust, low-maintenance appliances. Collectively, governorate trends underscore a gradual decentralization whereby suburban and ex-urban projects generate incremental volume even as Manama keeps its premium halo.

Competitive Landscape

The Bahrain major home appliances market features a moderately concentrated player set where Samsung, LG, and Haier capitalize on broad product spans, multichannel distribution, and intensive marketing. European suppliers such as Electrolux and BSH focus on premium niches that leverage heritage perception and quiet-operation engineering. Supplier ranking shifts quarterly as freight volatility, promotional intensity, and model-year launches spur share swings. BSH reported 14% Middle East turnover growth in 2024, crediting digital campaigns and regional warehousing near the capital. Haier leverages localized after-sales partnerships to increase consumer confidence within budget-tier segments.

Strategic consolidation is reshaping regional footprints. Arçelik purchased Whirlpool’s MENA business for EUR 20 million in 2024, adding production scale and brand rights that enhance bargaining power with GCC retailers. TCL forged a distribution alliance with Jashanmal to secure retail shelves and warranty coverage. Manufacturers emphasize inverter compressors, AI washing algorithms, and interoperability with voice assistants to comply with efficiency rules while differentiating on convenience. Extended-warranty bundling and trade-in programs, such as Samsung Gulf’s 2025 appliance exchange scheme, also aim to shorten replacement cycles.

Supply chain resilience occupies boardroom agendas. Elevated freight charges encourage near-market assembly, evidenced by BSH’s EUR 55 million plant in Egypt that earmarks half of output for GCC markets, including Bahrain. Sharp’s joint venture in Egypt to build 400,000 refrigerators annually by 2026 will further diversify. Brands with Middle Eastern capacity can promise quicker turnaround and lower landed costs, strengthening price competitiveness. Overall, technology leadership, omnichannel presence, and regional manufacturing will dictate share trajectories in the Bahrain major home appliances market.

Bahrain Major Home Appliances Industry Leaders

LG Electronics, Inc.

Haier Smart Home Co. Ltd.

Samsung Electronics Co. Ltd.

BSH Home Appliances

Panasonic Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: BSH Home Appliances invested EUR 55 million to open its first African factory in 10th of Ramadan City, Egypt, allocating 50% of capacity to GCC markets, including Bahrain.

- January 2025: Samsung Gulf introduced an appliance trade-in program that provides structured exchange incentives to Bahraini consumers

- July 2024: Sharp Corporation and Egypt’s Elaraby Group formed Horizon for Home Appliances Manufacturing Co. to build a refrigerator plant with 400,000-unit annual capacity starting March 2026. The facility targets growing demand in the Near/Middle East region with plans to sell approximately 500,000 refrigerators by 2027.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Bahrain's major home appliances market as all large, durable "white-goods" purchased for household cooking, cleaning, refrigeration, and climate control, specifically refrigerators, freezers, washing machines, dishwashers, ovens (including microwaves and combis), and split or window air conditioners. Units placed in serviced apartments and staff accommodation are counted, as they follow the retail supply chain.

Scope exclusion: small countertop devices, personal care gadgets, and consumer electronics sit outside this sizing.

Segmentation Overview

- By Product

- Refrigerators

- Freezers

- Washing Machines

- Dishwashers

- Ovens (Incl. Combi & Microwave)

- Air Conditioners

- Other Major Home Appliances

- By Distribution Channel

- Multi-Brand Stores

- Exclusive Brand Outlets

- Online

- Other Distribution Channels

- By Geography

- Capital Governorate

- Muharraq Governorate

- Northern Governorate

- Southern Governorate

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed appliance distributors, hypermarket buyers, organized retail managers, and after-sales service centers across Manama, Muharraq, and Saar, then cross-checked assumptions with energy label inspectors and fintech facilitators of online sales. These conversations filled data gaps on gray import share, warranty return rates, and seasonality, helping us fine-tune model coefficients.

Desk Research

We pulled baseline values from open datasets such as Bahrain Customs import declarations, UN Comtrade HS-8418/8422/8450 flows, the Information & eGovernment Authority's household formation tables, Bahrain Electricity & Water Authority efficiency label registry, and GCC Standardization Organization directives on MEPS. Macro indicators, GDP per capita, retail sales, and housing completions came from the IMF WEO, Central Bank of Bahrain, and Bahrain Economic Development Board reports. Company filings and retailer presentations mined through D&B Hoovers and Dow Jones Factiva gave recent ASP movements and channel splits. The sources cited are illustrative, not exhaustive, and many other public records supported validation and context building.

Market-Sizing & Forecasting

A top-down construct converts CIF import values and the small local output into retail sell-out using landed cost and channel margin ladders. Supplier roll-ups on three key product families provide a bottom-up sense check before reconciliation. Variables driving volume and ASP forecasts include new dwelling completions, disposable income progression, summer cooling degree days, e-commerce penetration, and retailer promotional intensity. A multivariate regression linked to ARIMA trend curves projects each variable, while scenario analysis captures fuel price or VAT shocks. Missing niche brand data are back cast from freight manifests and averaged ASPs.

Data Validation & Update Cycle

Outputs face variance checks against independent customs tallies and retail scanner signals. An analyst peer reviews anomalies, and our team re-contacts sources when variances exceed three percentage points. Reports refresh yearly, with mid-cycle updates for policy or supply chain events, ensuring clients receive the latest calibrated view.

Why Mordor's Bahrain Major Home Appliances Baseline Stands Out

Published estimates often differ because firms mix product buckets, apply contrasting mark-ups, or refresh at uneven intervals.

Key gap drivers here stem from divergent scope, whether air conditioners and microwaves are in, reliance on unverified import codes, and how quickly analysts reprice shipments during currency moves. Mordor's disciplined variable tracking and yearly refresh narrow these gaps and present a repeatable baseline decision makers can trust.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 185 M (2025) | Mordor Intelligence | - |

| USD 110 M (2024) | Regional Consultancy A | Omits ACs and ovens; estimates solely from two HS codes and lacks retail margin overlay |

| USD 276.1 M (2024) | Trade Journal B | Bundles small appliances and ventilation units; uses household stock x average price shortcut |

| USD 328 M (2024) | Global Consultancy C | Combines major and small appliances; relies on consumer spending survey without import reconciliation |

In sum, the spread reflects scope breadth and validation rigor. By grounding its model in audited trade data, local fieldwork, and a transparent update cadence, Mordor Intelligence delivers a balanced, defensible benchmark for Bahrain's major home appliances opportunity.

Key Questions Answered in the Report

What is the current value of the Bahrain major home appliances market?

The market is valued at USD 194.34 million in 2026 with a 5.05% CAGR forecast to 2031.

Which product segment leads sales in Bahrain?

Refrigerators hold the top position with 29.45% share in 2025, while washing machines are expanding fastest at a 5.72% CAGR.

How important is online retail to appliance sales?

Online channels account for 4.8% of total retail sales and are growing at 6.05% CAGR as consumers embrace quick delivery and digital payment options.

Why are energy-efficient appliances gaining traction?

GCC Minimum Energy Performance Standards and rising electricity tariffs drive households toward efficient models that reduce power bills over time.

Which governorate offers the highest growth potential?

Northern Governorate, supported by large housing projects, is forecast to grow at 5.32% CAGR through 2031.

How are supply chain challenges being addressed?

Manufacturers are investing in regional factories and exploring multimodal logistics to offset volatile ocean freight rates and ensure timely product availability.

Page last updated on: