Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

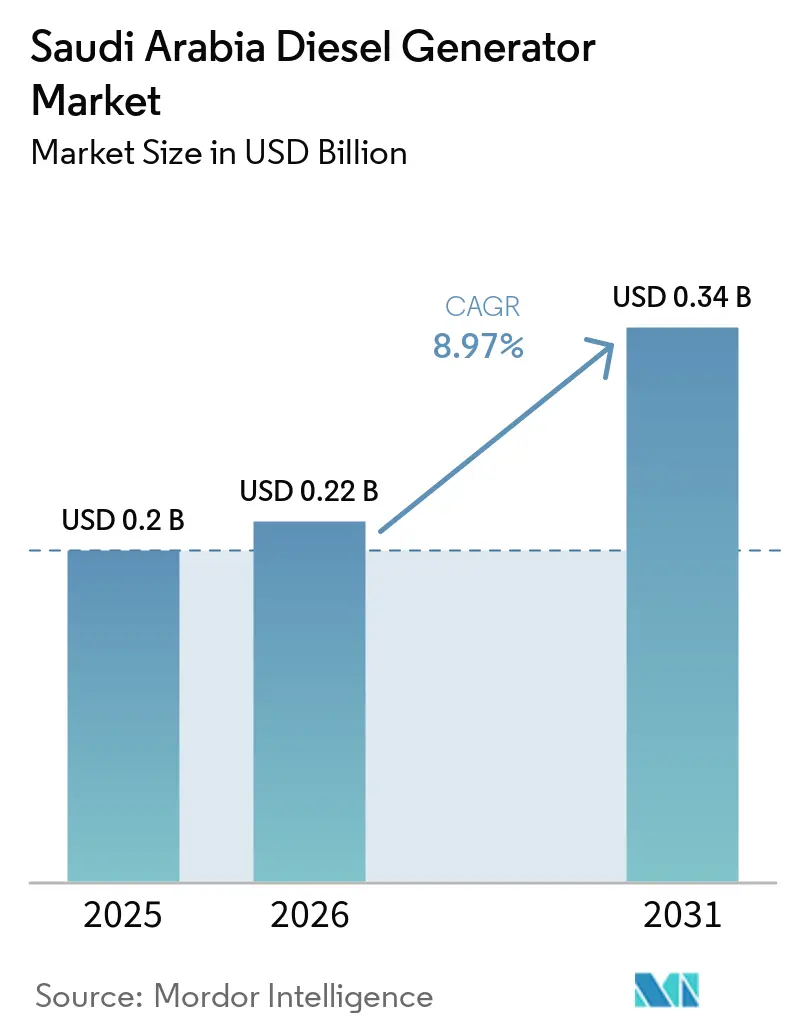

| Base Year Market Size (2025) | USD 0.2 Billion |

| Market Size (2026) | USD 0.22 Billion |

| Market Size (2031) | USD 0.34 Billion |

| Growth Rate (2026 - 2031) | 8.97% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Diesel Generator Market Analysis by Mordor Intelligence

The Saudi Arabia Diesel Generator Market size is expected to increase from USD 0.2 billion in 2025 to USD 0.22 billion in 2026 and reach USD 0.34 billion by 2031, growing at a CAGR of 8.97% over 2026-2031.

Construction-phase electrification for Vision 2030 giga-projects, stringent backup-power rules for health and data-center facilities, and the growing preference for rental fleets keep demand resilient even as new gas-fired plants erode baseload diesel use. Long-term service agreements that bundle predictive maintenance with parts supply are anchoring brand loyalty among industrial clients, while rental operators use fast mobilization and flexible pricing to widen addressable demand. Hybrid diesel-solar-battery systems are gaining traction because they cut fuel use during low-load periods, align with emission rules, and improve total cost of ownership. Emission caps under the draft SASO Stage V rule, noise limits in dense cities, and diesel-price volatility linked to subsidy reforms constrain continuous-power applications, but they also accelerate fleet turnover toward cleaner, more fuel-efficient models. Collectively, these cross-currents position the Saudi Arabia diesel generator market for robust but selective growth driven by standby, peak-shaving, and off-grid uses.

Key Report Takeaways

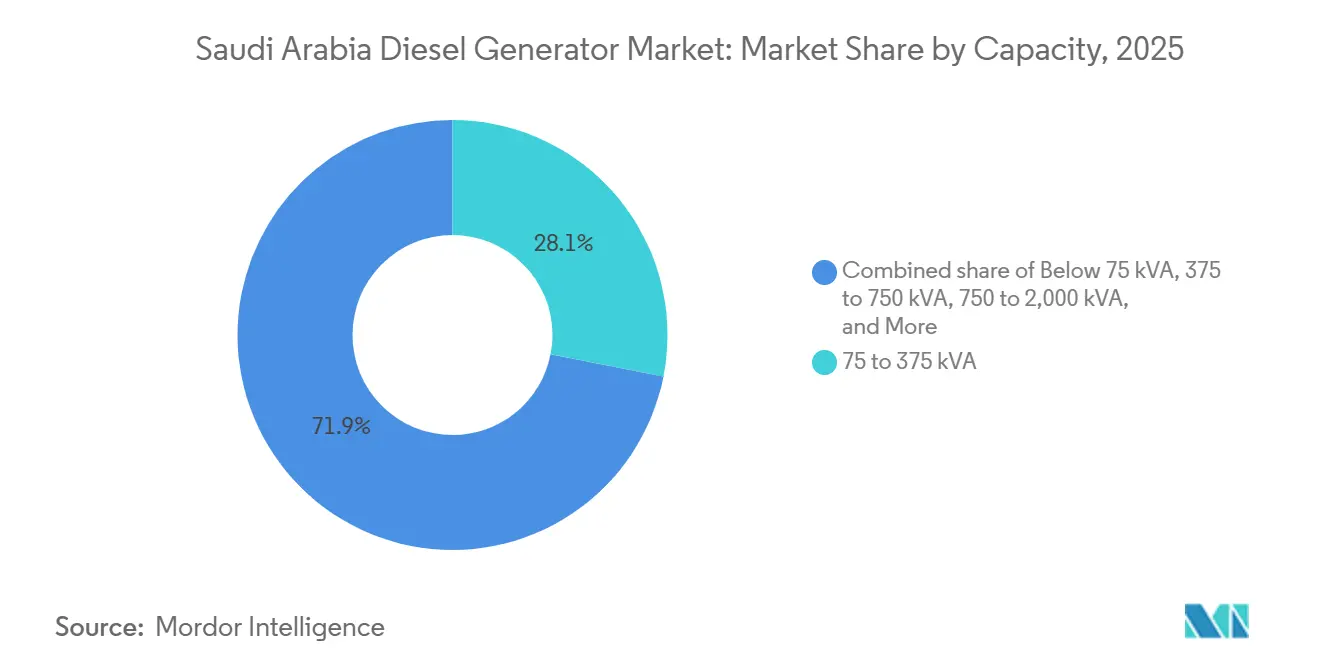

- By capacity, the 75 to 375 kVA band captured 28.1% of the Saudi Arabia diesel generator market share in 2025, while the 375 to 750 kVA band is expected to advance at an 11.1% CAGR through 2031.

- By application, prime and continuous power held 44.5% of demand in 2025 and is expected to grow at 10.0% CAGR through 2031.

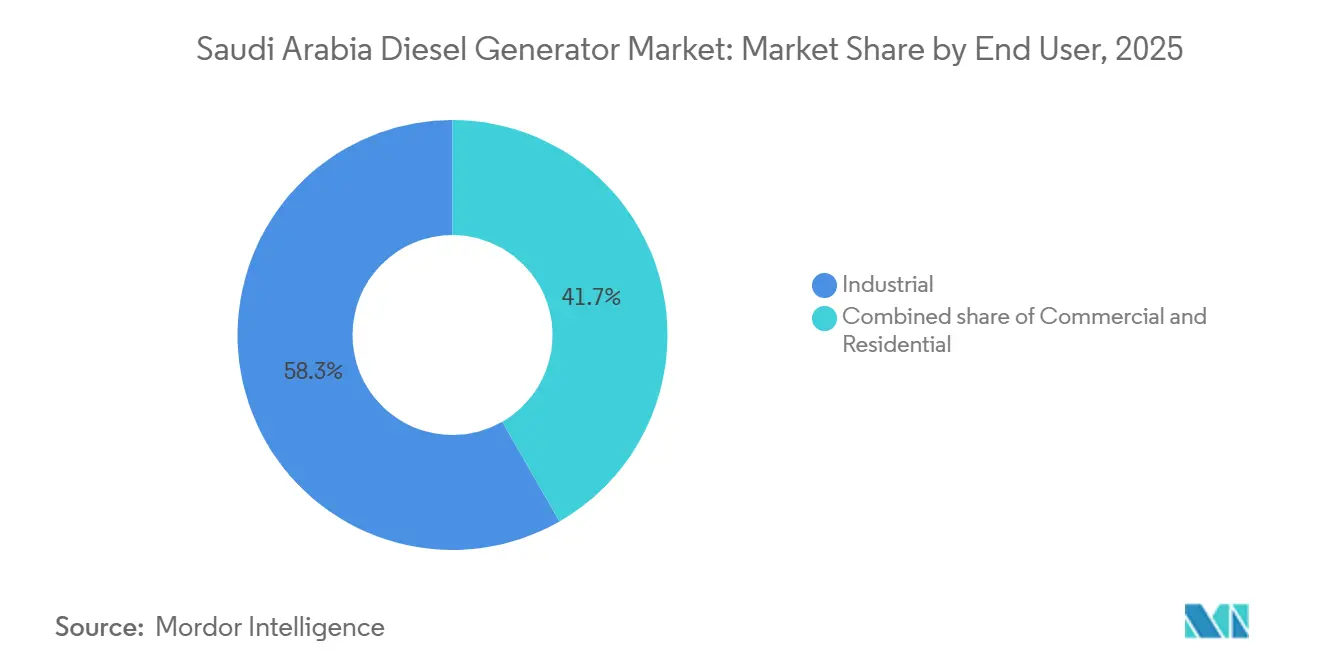

- By end user, industrial sites accounted for 58.3% of revenue in 2025 and are expected to grow at 9.7% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Diesel Generator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Large-scale Vision 2030 infrastructure roll-outs | 2.80% | National, early surge in NEOM and Red Sea corridors | Medium term (2-4 years) |

| Data-center boom demanding Tier-3+ backup power | 2.10% | Riyadh, Jeddah, Dammam clusters | Short term (≤ 2 years) |

| Surge in equipment-rental business models | 1.50% | National reach into GCC projects | Medium term (2-4 years) |

| Mandatory on-site generation for new healthcare facilities | 0.90% | Major cities and health clusters | Long term (≥ 4 years) |

| Military and remote-border electrification programs | 0.60% | Northern and southern borders | Long term (≥ 4 years) |

| AI-enabled predictive-maintenance bundles | 0.80% | Industrial and rental fleets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Large-Scale Vision 2030 Infrastructure Roll-Outs

Gigantic mixed-use projects such as NEOM, Qiddiya, and the Red Sea development require multi-year temporary power for concrete batching, worker camps, and commissioning stages. Construction sites typically deploy 375 to 2,000 kVA sets under 24-month rental contracts, absorbing capacity that once sat idle in depot yards. Early deliveries, including 23 units supplied to NEOM in 2024, signal sustained demand through 2028 before grid tie-ins reduce diesel run-time.[1]Gulf Construction Online, “Early Mobilization at NEOM,” GULFCONSTRUCTIONONLINE.COM Rental companies thus pre-position gensets and fuel-management systems near project sites, counting on predictable utilization. OEMs expecting parts consumption growth are securing local warehousing in Tabuk and Yanbu to cut lead times. As permanent substations enter service late in the decade, diesel dependence will taper, but standby needs will persist to cover grid-outage risk and commissioning tests.

Data-Center Boom Demanding Tier-3+ Backup Power

National ambitions to host regional cloud hubs are scaling installed IT capacity from 300 MW in 2025 toward 1,300 MW by 2030.[2]Data Center Dynamics, “Saudi Data-Center Capacity Surges,” DATACENTERDYNAMICS.COM Tier 3 certifications oblige each hall to maintain 72 hours of autonomy, driving demand for 750 to 2,000 kVA generators paired with lithium-ion UPS. Hyperscale builders lock in generator packages at financial close to satisfy lenders and insurers, making diesel an early procurement item. Fast load pickup, low harmonic distortion, and remote monitoring rank high on bid lists. The short fuse between notice to proceed and first silicon strengthens the business case for in-country stock-holding by OEMs and rental fleet owners. Complementary battery storage is often integrated for spinning-reserve replacement, but diesel remains the last line of defense against extended outages.

Surge in Equipment-Rental Business Models

Developers favor OPEX-light power rentals rather than owning fleets that may stand idle post-project. Registration on the EJAR platform streamlines contracting and boosts transparency, encouraging new entrants to scale fleets quickly. Utilization rates above 90% across several leading providers in 2025 confirm healthy demand. Rental invoices now bundle predictive-maintenance analytics and fuel-optimization software, creating new recurring-revenue streams for both lessor and OEM. Cross-border deployments into Kuwait and Bahrain further enlarge the addressable pool, especially for mid-range 100 to 1,250 kVA units. The trend cushions the Saudi Arabia diesel generator market against capex slowdowns because rental budgets track project timelines more closely than corporate capital cycles.

Mandatory On-Site Generation for New Healthcare Facilities

Regulations aligned with ISO 8528-12 stipulate sub-10-second switchover to backup power and 72-hour fuel autonomy for critical loads.[3]International Organization for Standardization, “ISO 8528-12:2022,” ISO.ORG More than 50 hospitals slated for completion by 2030 must embed redundant diesel sets sized between 750 and 2,000 kVA. Engineers specify automatic transfer switches with direct-cloud supervision to meet infection-control and pharmacovigilance standards. Hospital operators increasingly add battery storage that shoulders momentary load until generators ramp, lowering engine stress and extending overhaul intervals. Because healthcare sites cluster in dense urban zones, operators favor super-silent enclosures meeting 60 dBA at 7 meters, boosting unit cost but protecting patient comfort. These strict rules lock in a reliable, long-duration demand niche.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter diesel-emission caps (SASO Stage V draft) | –1.2% | Enforcement priority in major cities | Medium term (2-4 years) |

| Rising natural-gas generator substitution | –1.8% | Grid-connected industrial zones | Short term (≤ 2 years) |

| Diesel price volatility linked to subsidy reforms | –0.7% | Continuous-power applications | Short term (≤ 2 years) |

| Noise-pollution limits in urban projects | –0.5% | Riyadh, Jeddah, Mecca, Dammam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter Diesel-Emission Caps (SASO Stage V Draft)

The pending SASO Stage V rule adopts Euro VI alignment, forcing particulate filters and selective catalytic reduction on engines above 56 kW. Manufacturers must redesign exhaust paths, qualify catalysts, and update compliance files, adding both cost and lead time. Urban contractors already stipulate Stage V-ready sets for metro expansions and waterfront redevelopments, squeezing older Tier 3 fleets out of premium zones. Rental firms face retrofit or retirement decisions, accelerating replacement cycles, and hiking capex. Owners that upgrade early can charge higher day rates, but compliance audits every three years tighten oversight and lift operating bureaucracy.

Rising Natural-Gas Generator Substitution

Combined-cycle gas turbines totaling 7.2 GW, awarded in 2025, and an additional 3.6 GW under construction, cut into diesel peaking roles.[4]Gulf Construction Online, “Early Mobilization at NEOM,” GULFCONSTRUCTIONONLINE.COM Industrial parks in Jubail and Yanbu now favor pipeline gas or cogeneration plants that undercut diesel’s levelized cost. In the short term, diesel rentals spike during plant build-outs and fuel-switch outages, yet long-run baseload need declines. The Saudi Aramco liquid-fuel displacement program, targeting 1 million barrels per day by 2030, narrows diesel’s prime-power niche further. Suppliers pivot to standby and off-grid pockets to offset the shift.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Capacity: Mid-Range Units Anchor Rental Fleets

The Saudi Arabia diesel generator market size for the 75 to 375 kVA class accounted for USD 56 million revenue in 2025, reflecting widespread use across retail, telecom, and small industrial facilities. Rental operators prefer this bracket because units fit on standard trucks, parallel easily, and share common spares. Variable-speed technology is now present in more than 15% of new sales in this band, lifting fuel efficiency, especially during low-load nights. Above that, the 375 to 750 kVA range is the fastest riser at 11.1% CAGR through 2031 as modular data centers and AI workloads demand single-set simplicity.

Fleet data from a leading lessor shows an average run-time of 2,400 hours per unit per year in the 375 to 750 kVA aisle, validating revenue durability. Sets above 750 kVA remain indispensable for hospitals, desalination, and large construction camps, yet unit counts are lower, keeping their Saudi Arabia diesel generator market share below 20%. At the top end, sets beyond 2,000 kVA fill niche roles in petrochemical complexes and mine sites where prime power justifies high fuel bills. Chinese and Indian brands dominate sub-75 kVA residential sales on price, but limited after-sales coverage restrains their move into industrial duty cycles.

By Application: Prime Power Sustains Despite Grid Expansion

Prime and continuous power applications retained 44.5% of revenue in 2025, fueled by remote mines and drilling rigs that remain off-grid for years. Even with pipeline gas rollouts, many exploration and construction sites still view diesel as the surest path to uptime. A single hour of unplanned stoppage in a petrochemical cracker can cost six figures, so operators run dual redundant sets with automatic failover. Standby systems, however, are climbing faster because data centers, hospitals, and desalination plants cannot tolerate blackouts even for seconds. Saudi Arabia diesel generator market size for standby builds is therefore projected to exceed USD 120 million by 2031 at a double-digit CAGR.

Peak-shaving remains an opportunistic but growing niche where factories fire generators during tariff peaks to flatten utility bills. Dynamic load algorithms, proven in academic trials, are now embedded in commercial controllers that modulate engine RPM every few milliseconds to match demand. Hybrid diesel-battery skids add further savings by letting engines switch off during light loads, extending maintenance windows, and slashing noise. Government policy that rewards demand-charge reduction underpins the economic logic of such systems.

By End User: Industrial Dominance Reflects Petrochemical Intensity

Industrial customers, led by petrochemical and metals plants, represented 58.3% revenue in 2025 and will keep a commanding share through 2031. Continuous process industries need N+1 redundancy for safety and product consistency, so they choose premium OEMs with strong parts pipelines. The emergence of lithium and phosphate extraction under Vision Minerals amplifies prime-power orders for remote exploration camps. Saudi Arabia's diesel generator market share for industrial buyers is expected to remain above 55% even as commercial segments grow.

Commercial clients, especially hotels and malls, mostly buy or rent smaller 75 to 375 kVA units sized for life-safety loads, not full building coverage. They prioritize super-silent enclosures and aesthetic containerization to meet urban bylaws. Residential demand is fragmented and price-sensitive, making it a volume but low-margin play dominated by distributors of cost-focused brands. Government clusters upgrading hospital capacity adds a resilient, specification-driven sub-segment in the 750 to 2,000 kVA class.

Geography Analysis

The Eastern Province commanded the largest slice of the Saudi Arabia diesel generator market in 2025, thanks to the concentration of oil, gas, and petrochemical activity around Jubail, Ras Al-Khair, and Dammam. Thousands of kilometers of pipelines, refineries, and processing plants require black-start sets and safety-critical backup, anchoring repetitive service revenue. Expansion at the Jafurah gas complex and the move to cogeneration nonetheless preserve off-grid needs during construction, turnarounds, and emergency drills. Data-center clusters in Dammam add standby demand for 1,000 kVA sets with ultra-low harmonic distortion and 72-hour autonomy.

The Central Region, dominated by Riyadh, ranks second by value and is the fastest climber at a projected 10.3% CAGR through 2031. Mega-projects such as the Riyadh Metro, King Salman Park, and government district expansions rely on temporary diesel power during excavation and fit-out phases. The surge of hyperscale cloud investments multiplies standby generator procurement because Tier 3+ certifications mandate dual redundant systems. Hospitals built under new health clusters apply the same redundancy logic, reinforcing local demand.

The Western Region stretches from Jeddah to Mecca and up to Yanbu. Mixed-use coastal developments, tourism infrastructure for pilgrim traffic, and petrochemical production in Yanbu combine to keep generator uptake lively. Sustainability pledges at the Red Sea Project promote hybrid systems in which diesel sets operate mainly for contingency, yet they remain integral during early construction and commissioning. NEOM in the northwest forms a frontier demand node: vast distances from the national grid and a construction footprint of 26,500 square kilometers call for hundreds of rental units during the build-out of The Line and Oxagon. Military outposts along the northern and southern borders add steady demand for hardy 100 to 375 kVA units that pair with solar arrays to cut resupply sorties.

Competitive Landscape

Global OEMs led by Caterpillar, Cummins, and Atlas Copco hold dominance in the 375 kVA-plus tier through strong dealer networks, long-term service contracts, and embedded telematics that elevate uptime. Cummins Connected Diagnostics gains adoption in oilfield fleets, enabling condition-based parts orders that shrink downtime windows. Caterpillar supports local assembly in Jeddah to shorten lead times and meet localization quotas. Together, the top three players captured about 53% of high-power shipments in 2025, underscoring a moderately concentrated upper tier.

Regional specialists such as Altaaqa Alternative Solutions, Saudi Diesel Equipment, Himoinsa Middle East, and Byrne Equipment Rental secure market share in sub-375 kVA sets and the thriving rental ecosystem. Their edge lies in fleet availability, rapid mobilization, and flexible month-to-month terms that align with construction cash flows. Energia MTC’s 350 MW fleet, operated at 97% utilization in 2025, illustrates how local players convert proximity and service agility into elevated occupancy and pricing power.

White-space innovation centers on hybrid diesel-battery packages and variable-speed engines that trim fuel burn and ease compliance with Stage V caps. Chinese contenders such as Teksan and Broadcrown press into the mid-range with price-aggressive offerings, yet hurdles in parts logistics and certification limit penetration into mission-critical segments. SASO’s conformity-assessment framework, requiring inspection every three years and data-plate conformity, further privileges brands with local test benches and accredited labs. Overall, rivalry is vigorous but disciplined, as high service entry barriers curb pure-price bidding wars and preserve acceptable margins.

Saudi Arabia Diesel Generator Industry Leaders

Atlas Copco AB

Caterpillar Inc

Generac Holdings Inc

Cummins Inc.

Saudi Diesel Equipment Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Focus Power Jiangsu Co., Ltd. announced the successful completion and delivery of a customized 1500kVA containerized generator set to Saudi Arabia. The generator set is powered by the Cummins KTA50-G3 engine, a globally recognized model renowned for its durability, fuel efficiency, and stable performance under heavy loads. The KTA50-G3 is designed to provide continuous prime power in challenging environments, making it well-suited for construction sites, oil and gas fields, mining operations, and large-scale infrastructure projects.

- June 2025: Cummins Arabia supplied 30 DQLC and 6 DQCA diesel generator sets, delivering a total capacity of 73.2 MW, to support the expansion of hyperscale data centers in Saudi Arabia. This initiative enhances the region's digital infrastructure by providing dependable backup power in extreme climatic conditions while meeting operational efficiency and uptime requirements.

- October 2024: Baudouin introduced a range of high-performance diesel generator sets designed specifically for data center power requirements. These gensets, based on the M33 and M55 platforms, offer outputs ranging from 2000 kVA to 5250 kVA. They comply with Uptime Institute and ISO standards, ensuring reliable and continuous backup power solutions.

- March 2024: Recon Technologies Pvt. Ltd., an authorized GOEM of Mahindra Powerol diesel generators, launched a new range of CPCBIV+ emission-compliant diesel gensets in Hyderabad. With capacities of up to 625 kVA, this advanced series offers improved fuel efficiency, after-treatment systems, remote monitoring capabilities, and seamless grid-to-genset transition, aligning with India's stringent emission regulations.

Saudi Arabia Diesel Generator Market Report Scope

The diesel generator market encompasses the global industry engaged in the production, distribution, installation, and maintenance of diesel-powered generator sets (gensets) designed to generate electricity for backup, standby, prime, or continuous power purposes.

The Saudi Arabia diesel generator market report is segmented by capacity (below 75 kVA, 75 to 375 kVA, 375 to 750 kVA, 750 to 2,000 kVA, and above 2,000 kVA), application (standby/backup power, prime/continuous power, peak-shaving/load management), and end user (residential, commercial, and industrial). The market sizes and forecasts are provided in terms of value (USD).

By Capacity (kVA)

| Below 75 kVA |

| 75 to 375 kVA |

| 375 to 750 kVA |

| 750 to 2,000 kVA |

| Above 2,000 kVA |

By Application

| Stand-by/Backup Power |

| Prime/Continuous Power |

| Peak-shaving/Load Management |

By End User

| Residential |

| Commercial |

| Industrial |

| By Capacity (kVA) | Below 75 kVA |

| 75 to 375 kVA | |

| 375 to 750 kVA | |

| 750 to 2,000 kVA | |

| Above 2,000 kVA | |

| By Application | Stand-by/Backup Power |

| Prime/Continuous Power | |

| Peak-shaving/Load Management | |

| By End User | Residential |

| Commercial | |

| Industrial |

Key Questions Answered in the Report

What is the projected value of the Saudi Arabia diesel generator market in 2031?

The market is forecast to reach USD 340 million by 2031 at an 8.97% CAGR from 2026 to 2031.

Which capacity segment leads current demand?

Units rated 75 to 375 kVA held 28.1% of 2025 revenue because they fit the needs of retail, telecom, and small industrial users.

Why are data centers important to future generator sales?

Tier-3 certifications mandate 72-hour backup autonomy, so hyperscale data centers procure large 750 to 2,000 kVA diesel sets early in construction.

How will SASO Stage V rules affect generator fleets?

Stage V will require particulate filters and catalytic reduction, prompting fleet owners to retire or retrofit older Tier 3 units, especially in cities.

What role do rental companies play in this market?

Rental fleets supply OPEX-friendly power solutions, achieve above-90% utilization, and now bundle predictive-maintenance analytics to stand apart.

Page last updated on: