Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

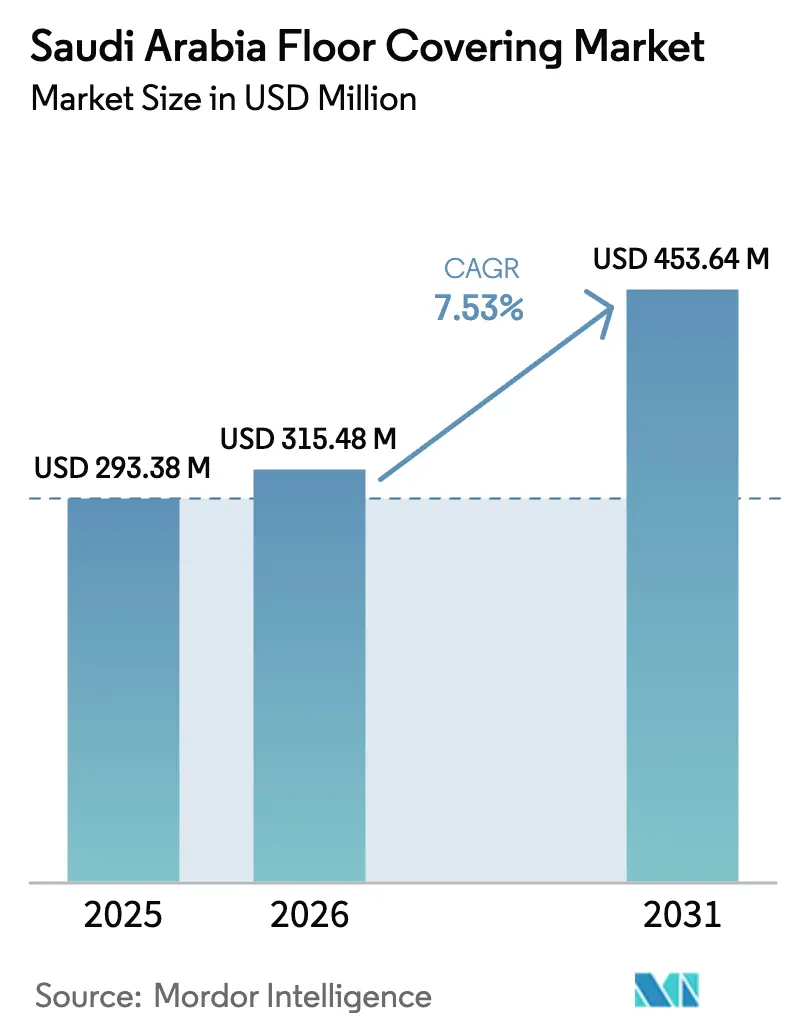

| Base Year Market Size (2025) | USD 293.38 Million |

| Market Size (2026) | USD 315.48 Million |

| Market Size (2031) | USD 453.64 Million |

| Growth Rate (2026 - 2031) | 7.53% CAGR |

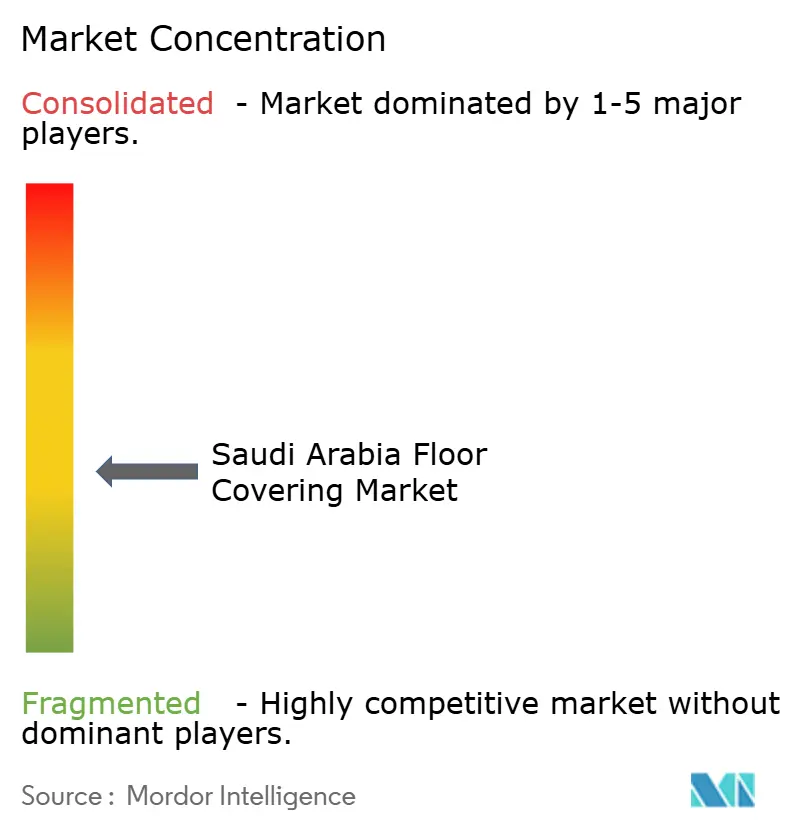

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Floor Covering Market Analysis by Mordor Intelligence

The Saudi Arabia floor covering market size is projected to expand from USD 293.38 million in 2025 and USD 315.48 million in 2026 to USD 453.64 million by 2031, registering a CAGR of 7.53% between 2026 to 2031. The Saudi Arabia floor covering market is experiencing steady growth, driven by large-scale national transformation initiatives that are fueling extensive construction activity across the country. This growth is creating sustained demand for a variety of flooring types, including ceramic, vinyl, carpet, and wood, in both residential and non-residential projects. Strong activity in building construction, particularly in residential developments, is supporting new installations as well as renovation projects, which further boost the uptake of diverse flooring materials and formats. Economic diversification is also playing a significant role, as non-oil sectors continue to strengthen, providing stability to project execution cycles and encouraging the adoption of premium specifications in hospitality, office, and public building projects. Additionally, regulatory developments are shaping market dynamics, with stricter limits on volatile organic compound (VOC) sector projects.

Key Report Takeaways

- By product type, ceramic tiles led with 49.38% of Saudi Arabia's floor covering market size in 2025, while luxury vinyl tiles and planks are projected to expand at an 11.64% CAGR through 2031.

- By construction type, remodeling and retrofit accounted for 62.38% of Saudi Arabia's floor covering market share in 2025, while new construction is projected to expand at a 10.39% CAGR through 2031.

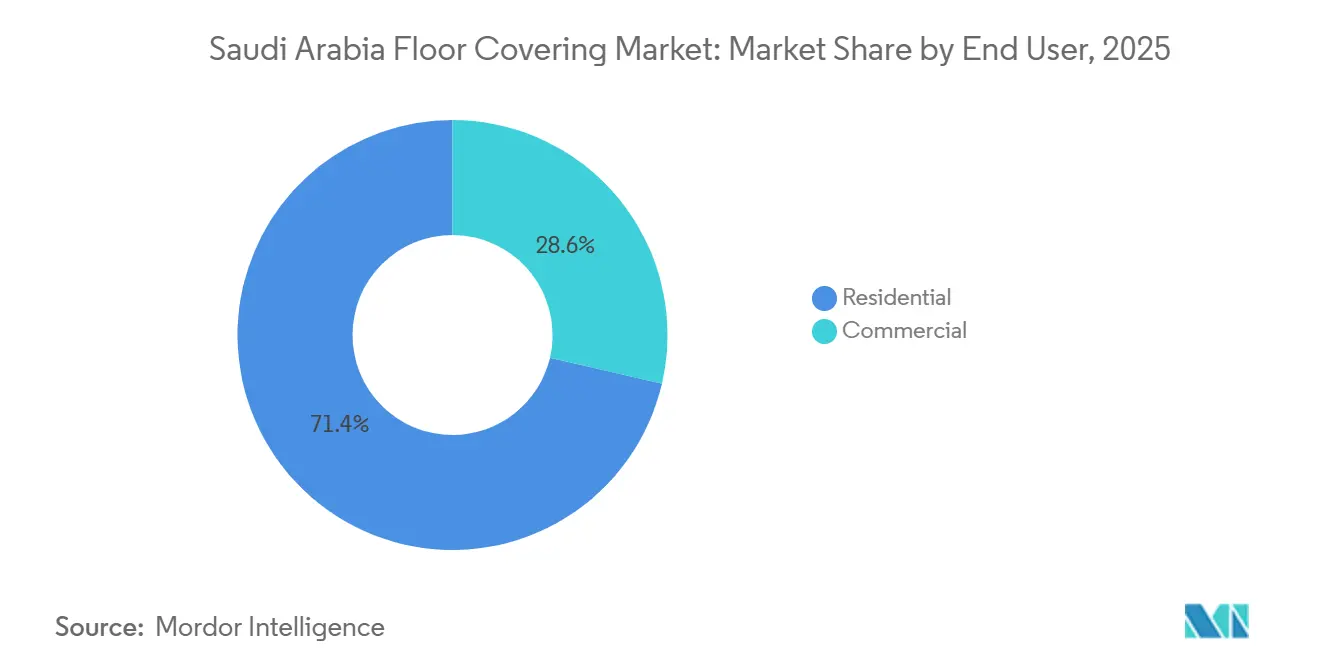

- By end-user, residential applications held 71.36% of Saudi Arabia's floor covering market share in 2025, while commercial is projected to record the highest growth with an 11.22% CAGR through 2031.

- By distribution channel, B2C retail commanded 78.39% of the Saudi Arabia floor covering market share in 2025, while B2B/contractors/builders are projected to grow at a 10.33% CAGR through 2031.

- By cities, Riyadh held 34.35% of Saudi Arabia's floor covering market share in 2025 and is forecast to expand at a 9.84% CAGR through 2031, while Jeddah is projected to grow at an 8.7% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Floor Covering Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 Megaprojects | +1.6% | Giga-project zones and national program clusters | Long term (≥ 4 years) |

| Premium Renovations in Riyadh and Jeddah | +0.9% | Riyadh and Jeddah high-income residential districts | Medium term (2-4 years) |

| Hotel Upgrades from Tourism and Hospitality | +1.1% | Red Sea and Diriyah Gate hospitality corridors | Medium term (2-4 years) |

| Carpet Demand for Majlis and Prayer Areas | +0.5% | Residential villas and majlis spaces nationwide | Short term (≤ 2 years) |

| Low-VOC Vinyl Adoption under SASO Standards | +0.6% | Nationwide under SASO environmental compliance | Short term (≤ 2 years) |

| Modular Offices and Raised-Access Flooring | +0.5% | Grade A offices and business districts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Megaprojects Driving Flooring Market Growth

The Saudi Arabia floor covering market is tied to a sustained megaproject agenda that prioritizes mixed-use districts, tourism assets, and cultural destinations under Vision 2030. Contracting momentum in 2025 included Diriyah Company’s SAR 18.75 billion awards, covering a large retail development with 400 units that carry Najdi-aesthetic finishes and ceramic solutions designed to meet fire and slip standards in high-footfall retail environments (SAR 18.75 billion equals USD 4.99 billion). Delivery of themed destinations is advancing, as Qiddiya’s flagship park completed construction with extensive slip-resistant vinyl, epoxy coatings, and UV-stable outdoor systems sized to both safety and longevity requirements. On the Red Sea, hotels under the InterContinental brand have embedded low-VOC materials into high-end interiors that must meet LEED performance thresholds while operating in humidity-prone microclimates[1]Diriyah Company, “High Profile Projects Announced… H1 2025,” Diriyah Company, diriyahcompany.sa.. The Saudi Green Building Code’s enforcement is bringing energy-efficiency and emissions criteria to the forefront of bids for public and giga-project contracts, which encourages standardized, test-verified flooring systems in ceramic, vinyl, and specialty seamless formats. These execution streams anchor medium to long-term visibility for the Saudi Arabia floor covering market as large projects convert from design into procurement and installation phases.

Riyadh and Jeddah Witnessing a Rise in Premium and Luxury Residential Renovations

High-end renovations in Riyadh and Jeddah are scaling alongside urban repositioning, with villa and apartment owners upgrading from builder-grade finishes to imported stone, engineered wood, and designer LVT to align with rising quality expectations in core districts. Rising homeownership has reinforced a stable base for remodel activity and supports phased interior upgrades that often allocate a meaningful share to flooring due to its aesthetic impact and maintenance benefits. In practice, polished concrete, microcement, and premium porcelain are gaining in areas that demand thermal stability and low upkeep and are being specified where HVAC optimization and dust management are project goals. Developers and homeowners are also responding to sustainability messaging with LEED-aligned materials and low-VOC certification, although style, durability, and lifecycle cost remain the primary selection criteria. The Saudi Arabia floor covering market is therefore seeing renovation-driven demand that complements new-build cycles and improves resilience to short-term swings in contractor awards.

Hotel Flooring Upgrades Driven by Expansions in Tourism and Hospitality (Red Sea, Diriyah Gate)

Tourism investments are rapidly translating into specification-rich flooring packages across resorts, branded residences, and urban hotels. Red Sea Global’s phased openings and AMAALA’s Triple Bay rollout are channeling premium stone, engineered wood, microcement, and antimicrobial vinyl into high-traffic areas and wet zones where performance, maintenance, and LEED alignment are decisive. InterContinental’s resort at The Red Sea showcased low-VOC solutions and modular systems that meet both environmental and operational thresholds set by luxury operators and project owners. In the cultural core, Diriyah’s hospitality pipeline integrates modern building systems with traditional aesthetics, which drives a nuanced mix of slip-resistant ceramic, porcelain with low water absorption, and performance-backed modular finishes in corridors and guest areas. This flow of openings and fit-outs sustains a steady cadence for suppliers that can meet tight delivery schedules, provide installation guidance, and furnish product-level environmental documentation. The Saudi Arabia floor covering market is well positioned to capitalize on the room additions and refurbishment cycles expected through the decade as operators standardize on durable, low-emission materials.

Carpet Sales Surge as Majlis and Prayer Areas Favor Soft Floor Coverings

Carpet and rugs retain cultural importance in majlis rooms and prayer spaces, which supports a recurring baseline for domestic production and imports. In mosques and religious infrastructure, flame-retardant and stain-resistant carpets are a core specification, and they must comply with building and fire codes that reflect high occupancy and frequent cleaning cycles in peak seasons. Hotels and corporate offices continue to use modular carpet tiles in conference rooms and select guest corridors due to acoustic damping and ease of selective replacement, while hard-surface alternatives are often preferred in lobbies and circulation spaces for durability. Over time, luxury vinyl planks and porcelain have reduced carpet’s footprint in utility-heavy areas because of moisture resistance and lifecycle cost advantages. Within this context, the Saudi Arabia floor covering market maintains a stable carpet niche shaped by cultural use cases and compliance obligations in public venues.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oil Revenue Cyclicality and Private Spending | -0.5% | Kingdom-wide private project pipeline | Medium term (2-4 years) |

| Desert Climate and Accelerated Lifecycles | -0.4% | Central and western arid zones | Long term (≥ 4 years) |

| Import Tariffs on Wood and Luxury Vinyl | -0.2% | Import-dependent wood and LVT categories | Short term (≤ 2 years) |

| Fragmented Installer Base and Quality Gaps | -0.2% | Large project sites across regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Impact of Oil Revenue Cyclicality on Private Construction Spending

Short-run revenue shifts have contributed to budget deficits, which can temper near-term contracting momentum in select private and discretionary projects. The FY2025 fiscal position showed a deficit, and this was followed by a FY2026 plan that maintains meaningful capital expenditures, signaling continued support for core infrastructure even as allocations are recalibrated across sectors. In this environment, flooring orders tied to private projects can face deferrals, particularly for high-spec stone and wood packages that require larger deposits and longer lead times. Public-sector anchor programs linked to Vision 2030 continue to provide a floor for demand with multi-year outlays and a pipeline approach that phases execution to preserve continuity. This backdrop keeps the Saudi Arabia floor covering market on a stable trajectory while short-cycle volatility at the project level can temporarily affect procurement schedules.

Import Tariffs Inflate Prices for Wood and Luxury Vinyl

Ad-valorem duties on finished wood and luxury vinyl increase landed costs for imported premium packages, which affects buyer choices in price-sensitive segments and shifts share toward domestic porcelain and other local alternatives. Tariff structures documented for Saudi Arabia remain a reference point for importers and support the trend of localizing production for certain formats where feasible[2]Office of the United States Trade Representative, “2025 National Trade Estimate Report,” USTR, ustr.gov.. Domestic producers have used this window to recapitalize and expand, and selected firms reported higher revenue and profit as projects substitute toward tariff-light options while aligning with Made-in-Saudi content on large public tenders. The net effect is a bifurcation between price-driven segments and prestige imports in luxury hospitality and top-end residential. Over the medium term, this structure supports investment in local capacity and quality upgrades that can lift value capture in the Saudi Arabia floor covering market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ceramic Domination, LVT Disruption

Ceramic tiles held a 49.38% market share in 2025, reflecting strong domestic production, thermal performance, and cost-effectiveness for climate-sensitive applications. Luxury vinyl tiles (LVT) and planks are the fastest-growing segment, with an 11.64% CAGR projected through 2031, driven by modular installation, low-VOC formulations, and acoustic and maintenance benefits in hospitality and healthcare. Ceramic tiles remain resilient in residential and high-traffic areas due to low water absorption and durability, ensuring steady volumes as premium formats expand. Porcelain sets benchmarks for abrasion and thermal-shock resistance, while microcement and polished concrete gain traction in seamless, cost-efficient applications. This performance mix aligns with interior functionality, maintenance, and compliance standards in the Saudi Arabia floor covering market.

The interplay between ceramic dominance and LVT growth is reshaping value distribution. Ceramic tiles dominate mid-tier housing due to availability and cost stability, while LVT penetrates spaces prioritizing acoustic comfort and moisture resistance. In luxury hospitality and offices, engineered wood and stone face cost challenges, shifting demand toward premium porcelain or rigid-core LVT. Carpet and rugs meet cultural and acoustic needs but face competition from hard surfaces in high-maintenance areas. This evolution drives quality improvements as suppliers enhance formulations, documentation, and installer training to meet growing demand in Saudi Arabia.

By Construction Type: Retrofit Leads, New-Build Accelerates

Remodeling and retrofit activities held 62.38% of the market share in 2025, driven by homes requiring replacement flooring and rising interior design expectations in metropolitan areas. New construction is projected to grow at a 10.39% CAGR through 2031, supported by housing units, hospitality projects, and mixed-use developments under active plans. Retrofit projects prioritize dust management, thermal comfort, and lifecycle costs, boosting demand for porcelain and seamless systems in areas with frequent cleaning and temperature changes. New construction employs standardized packages with ceramic, vinyl, and specialty surfaces, promoting factory pre-finishing and rapid-installation modules. These trends ensure stable volumes and increased premium product adoption as the Saudi Arabia floor covering market advances in compliance and quality.

Retrofit projects incur higher costs due to selective demolition and tight timelines, while new construction benefits from bulk delivery and sequencing efficiencies. Pre-fabricated bathroom pods and modular room kits are increasingly used in large projects, integrating factory-installed flooring for faster completion. Residential new-builds balance cost and performance with ceramic and vinyl combinations, offering premium upgrades. Hospitality and cultural venues favor premium materials like stone, engineered wood, and high-spec vinyl for signature spaces, enhancing new construction’s contribution while retrofit sustains baseline demand.

By End-User: Residential Incumbency, Commercial Velocity

Residential applications held a 71.36% market share in 2025, driven by homeownership policies, strong housing starts, and replacement cycles emphasizing thermal stability and low maintenance. Commercial end-users accounted for 28.64% of demand, with an 11.22% CAGR projected through 2031, supported by hotels, retail spaces, educational buildings, and public facilities requiring performance and compliance. Hospitality prioritizes slip resistance, indoor air quality, and durability for high occupancy and frequent cleaning. Retail and mixed-use centers adopt materials like porcelain, microcement, and epoxy in high-abrasion zones, driving market diversification.

Hospitality and leisure lead commercial value capture with premium specifications and modular replacements. Retail corridors and experiential zones use slip-resistant surfaces and polished concrete, benefiting lighting and HVAC strategies. Healthcare facilities demand antimicrobial, ESD-safe, and easy-to-clean surfaces, boosting specification-grade vinyl and specialty coatings. Educational and public buildings balance durability and budget, often using domestic ceramic to meet local mandates. The commercial segment’s 11.22% CAGR significantly contributes to market growth, while residential remains the backbone for steady volume.

By Distribution Channel: Retail Incumbency, B2B Momentum

In 2025, B2C retail channels held 78.39% of the market share, driven by villa renovations and small-contractor purchases through showrooms, home centers, and online platforms. B2B procurement accounted for 21.61% and is expected to grow at a 10.33% CAGR through 2031, as mega-developers consolidate specifications and sign agreements with manufacturers or distributors. Large projects increasingly bypass retail intermediaries for scale pricing and delivery reliability, boosting direct channels and pre-qualified distributors. Online ordering is expanding with improved selection and logistics, but showrooms remain relevant for high-end purchases requiring tactile assessment and installation bundling. This channel mix enhances market access and raises service expectations, strengthening the service layer in the Saudi Arabia floor covering market.

Distributor-mediated deals are common among small and mid-sized contractors relying on warehouse inventory and technical support. For giga-projects and public tenders, direct agreements streamline specifications and submittals, emphasizing EPDs, VOC disclosures, and durability tests. Suppliers differentiate through catalog breadth, installer certification, and after-sales support as projects demand complex finishes. This shift boosts premium vinyl and porcelain lines with documented performance and availability. These trends are increasing B2B contributions to the market as institutional buyers prioritize direct sourcing and technical validation in procurement.

Geography Analysis

Riyadh held a 34.35% market share in 2025 and is expected to grow at a 9.84% CAGR through 2031, driven by its role as the administrative and financial hub with flagship projects. These projects, including cultural, recreational, hospitality, and mixed-use developments, generate demand for ceramic, porcelain, premium vinyl, and specialty flooring for interior and exterior applications[3]Government of Saudi Arabia, “Vision 2030 Annual Report 2024,” Vision 2030, vision2030.gov.sa. . Jeddah, as a coastal commercial hub and gateway to Red Sea tourism, supports demand for imported stone, engineered wood, and specification-grade luxury vinyl tile (LVT) in branded projects. Its luxury positioning and hospitality growth further enhance this demand. Other regions are growing through housing developments, religious tourism infrastructure, industrial expansions, and logistics upgrades, ensuring steady demand for ceramic and compliant vinyl flooring. This regional diversity allows the market to align products with local climates and occupancy patterns while meeting national standards.

Riyadh’s projects require high-performance finishes meeting thermal cycling, slip resistance, and abrasion standards, increasing demand for porcelain and specification-grade vinyl. Jeddah’s coastal climate emphasizes humidity control and UV stability, driving demand for engineered teak, UV-stabilized epoxy, and slip-rated ceramic for outdoor use. In Makkah and Madinah, religious tourism drives demand for abrasion-resistant and hygienic flooring, while the Eastern Province’s industrial sector supports epoxy and chemical-resistant surfaces. These regional needs shape product mixes and installation practices, ensuring stable demand across the Saudi Arabia floor covering market as projects progress into the medium term.

Regulatory Landscape

Saudi Arabia regulates floor coverings primarily through the Saudi Standards, Metrology and Quality Organization (SASO) under the SALEEM Saudi Product Safety Programme, which links market access to product-level conformity assessment and documentation. Floor covering products map into specific SASO Technical Regulations, including the Technical Regulation for Textile Products (relevant to textile floor coverings such as carpets) and the Technical Regulation for Building Materials, Part 4 (covering tiles, ceramics, sanitary ware and related products used in buildings).

Compliance is operationalized through the SABER platform, where importers (and, where applicable, local manufacturers) manage conformity workflows and required certificates. A key procedural anchor is the SABER Shipment Certificate of Conformity (SCoC) requirement: as of October 1, 2025, issuance of SCoC via SABER is mandatory for both regulated and non-regulated products before customs clearance. This tightening increases the risk of clearance delays for incomplete or incorrect submissions and raises the importance of ongoing testing and maintenance of Product Certificates of Conformity (PCoC) with SASO-notified bodies.

Value Chain Analysis

The value chain spans upstream raw materials and compounds (ceramic bodies and glazes, stone, wood derivatives, vinyl and backing materials, and adhesives), midstream manufacturing and finishing (ceramic and porcelain tile lines, carpet and rug production, and resilient flooring conversion), and downstream specification, distribution, and installation. In Saudi Arabia, demand is shaped heavily by project specifications and compliance documentation, so regulatory steps (SASO SALEEM conformity routes and SABER registration, including PCoC and SCoC issuance) sit alongside core supply activities and can affect lead times and SKU selection for both imported and locally produced floor coverings.

Downstream, the market is served through direct project supply to contractors and developers as well as B2C retail and showroom networks concentrated around major hubs such as Riyadh and Jeddah, supported by regional warehousing and last-mile delivery. Execution risk concentrates in (i) reliance on imported inputs for specialty products, which raises exposure to logistics and tariff-driven landed-cost shifts in segments such as premium wood and LVT, and (ii) installation capacity and quality, where a fragmented installer base can create rework and schedule slippage on fast-track programs. These dynamics elevate the premium placed on distributors and manufacturers that bundle inventory planning, compliant submittal packages, and installer training to meet mega-project sequencing and handover requirements.

Competitive Landscape

The market is moderately consolidated, with the top five suppliers holding around half of the market value in 2025. Local and international players compete through product specialization, service offerings, and compliance readiness. Domestic manufacturers focus on cost and availability in ceramic and commodity-grade segments, while multinationals emphasize sustainability documentation, VOC compliance, and modular systems for fast-track construction. Localization efforts include a rigid-LVT facility in Jeddah, reducing import duties and aligning with local content rules. Suppliers are also enhancing installer training and technical support to minimize rework and accelerate project turnover, driving growth in specification-led segments.

Companies are shifting toward resilience and premiumization. Saudi Ceramic Company recovered in 2025 after a 2024 loss, aided by insurance proceeds and steady demand for local porcelain amid import tariffs. Wangkang Ceramics’ Environmental Product Declaration (EPD) meets documentation needs for public and giga-project tenders. In hospitality zones, global brands collaborate with suppliers offering LEED-aligned, modular systems suited to high occupancy and frequent cleaning. These efforts are advancing certified, project-ready portfolios in the Saudi Arabian floor covering market.

Competitive intensity has increased collaboration across the value chain. Manufacturers are investing in local QA labs, pre-approved submittal libraries, and standardized specifications for large programs. Distributors and applicators are training for specialized systems like raised access flooring (RAF) and microcement to address installation challenges and ensure quality. Companies with strong documentation and service capabilities are better positioned to win tenders by competing on total value rather than price, gradually raising capability standards in the Saudi Arabian floor covering market.

Saudi Arabia Floor Covering Industry Leaders

Al Sorayai Group

Al Abdullatif Industrial Investment Co.

Saudi Ceramic Company

Tarkett Middle East LLC

Mohawk Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A major opportunity sits in compliance-led product upgrades and documentation services as procurement tightens around SASO and building-material conformity processes. The October 1, 2025 step-up in mandatory SABER SCoC issuance for both regulated and non-regulated products before customs clearance pushes importers, distributors, and brands to standardize product dossiers, testing, and certificate renewal management. That shift creates whitespace for suppliers that can provide project-ready ranges, such as low-emission and performance-validated vinyl systems and certified ceramic or porcelain products under the relevant SASO technical regulations.

Another opportunity is the flooring integration required by industrialized construction and fast-track delivery methods used across national programs and giga-project execution. Modular and phased delivery tends to favor standardized, easy-to-install systems and reliable logistics. Evidence of continuing construction intensity in 2026 was highlighted by MEED reporting on Saudi construction activity acceleration that year, reinforcing the near-term focus on supplier readiness: high-volume availability, repeatable installation outcomes, and the ability to support phased packages for hospitality, mixed-use, and public developments while meeting Saudi Building Code and SASO conformity requirements.

Recent Industry Developments

- March 2026: ARTEX Industrial Investment Co. reported its 2025 fiscal year net profit of SAR 21.32 million. The disclosure highlighted ongoing operational emphasis across its industrial textile footprint, including categories tied to carpets, rugs, and related materials relevant to soft floor coverings in the Kingdom. Public reporting also supports counterparty confidence for contractors and distributors that rely on financially stable local suppliers.

- November 2025: Red Sea Global announced details around AMAALA's Triple Bay, positioning the ultra-luxury destination with a large resort pipeline and a focus on climate-resilient, design-led interior specifications. The scale and branding profile of the development reinforced demand for higher-spec flooring packages in hospitality, including premium stone, porcelain, and compliant resilient flooring in wet and high-traffic zones.

- July 2024: Saudi Ceramic Company commenced trial and commercial operations at its new porcelain tile plant. The step added domestic capability for porcelain formats used in high-traffic residential and commercial projects, supporting shorter lead times and improved availability versus imports. Local capacity additions also align with procurement preferences that favor reliable supply and consistent quality for large project packages.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the annual value of floor covering materials sold for permanent installation in Saudi Arabia across residential, commercial, and industrial buildings. It includes soft coverings like carpets and rugs, resilient materials like vinyl and rubber, and hard surfaces like tile, stone, wood, and laminate.

Scope exclusions: It excludes temporary event flooring, loose floor mats, and unfinished raw timber.

Segmentation Overview

- By Product Type

- Carpet and Area Rugs

- Wood Flooring

- Ceramic Tiles Flooring

- Laminate Flooring

- Vinyl Flooring

- Stone Flooring

- Other Products

- By Construction Type

- New Construction

- Remodeling/Retrofit

- By End-User

- Residential

- Commercial

- Hospitality & Leisure

- Retail & Shopping Centers

- Healthcare Facilities

- Education

- Corporate Offices

- Public & Government Buildings

- Other Commercial Users

- By Distribution Channel

- B2C Retail

- Home Centers

- Specialty Flooring Stores

- Online

- Other Distribution Channels

- B2B / Contractors / Builders

- B2C Retail

- By Geography

- Riyadh

- Jeddah

- Other

Data Sources, Market Sizing, and Validation

Desk Research

We start by mapping construction and renovation demand in the Kingdom, then align that with how floor coverings are typically specified and purchased. To ground the model in public facts, sources such as Saudi General Authority for Statistics (building and housing indicators), Saudi Customs trade publications, UN Comtrade import data, World Bank macro series, and peer reviewed construction materials journals are used as reference points.

We then tighten the assumptions using company annual reports, investor presentations, and reputable local business press, which help check product mix and pricing direction. For harder to pin down items like shipment splits and long term project pipelines, we also use paid subscriptions for company financials and intelligence, import and export shipment level data, and contract and tender monitoring. These inputs are cross checked against the public series. This list is not exhaustive, and additional sources were reviewed to collect data, validate assumptions, and clarify the market narrative.

Primary Interviews and Surveys

Next, we validate the desk assumptions through interviews and surveys with distributors, contractors and installers, retailers, and material specifiers who see real ordering patterns and substitution behavior. Because this is a Saudi Arabia study, responses were taken from across major demand centers and project led corridors, and the inputs were used to confirm pricing logic, import dependence, and how residential and project demand moves year to year.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 12% | |

| Mid tier: 50% | Functional/Unit leaders: 38% | |

| Smaller Players: 21% | Managers: 50% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where construction activity and renovation demand are converted into a floor covering spending pool, then filtered by material adoption in typical Saudi projects. To keep the math tied to real signals, inputs include building permits and completions, project pipeline timing, import volumes by major flooring categories, average installed area assumptions by building type, and observed price ranges by material family.

Once the demand pool is constructed, we corroborate it with selective bottom-up checks, such as rolling up supplier and distributor revenues from sampled channels, and checking implied volumes using average selling price times estimated square meters sold. Where the channel data is thin, gaps are handled by using conservative ranges from installer feedback, then stress testing the result against trade flows. Forecasting uses scenario analysis supported by expert views on project execution pace, housing formation, and price movement, and the output is converted into consistent USD values using stable currency timing assumptions.

Data Validation & Update Cycle

Before sign off, outputs are triangulated against independent signals such as import trends, construction award momentum, and the implied per square meter spend levels seen in recent projects. Any sharp jumps or drops are reviewed through variance checks, and if the driver is not clear, analysts re contact contributors to confirm whether it is a one off project effect, a pricing change, or a definition mismatch.

Each report is refreshed annually, and interim updates are made when material events occur, such as major project reprioritization or sudden cost swings in key materials. Right before delivery, a fresh review pass is completed so the numbers and assumptions reflect the latest available information.

Mordor Intelligence's Saudi Arabia Floor Covering Market Sizing Compared With Other Published Estimates

Published market values for floor covering in Saudi Arabia can differ widely because the scope is not always aligned and the base year can also vary. In our checks, the biggest gaps usually come from whether only soft coverings are counted, or whether hard surfaces like tile and wood are also included, followed by how imports are converted into consumption and how installation value is treated.

Another driver is how price progression is handled, because some estimates apply broad inflation factors while others use material specific price paths, and that can shift the number quickly in a project heavy market. Refresh cadence also matters because project starts and delays can change expected demand by year, and the spread is easiest to see when a 2024 base is compared with a 2025 base that already reflects newer project delivery assumptions, which is the adjustment applied here by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 293.38 M (2025) | |

| Industry Databook A | USD 595.20 M (2024) | Uses a soft covering scope focused on carpet style products, so hard surfaces are not captured, and the base year is different from 2025. |

| Publisher Catalog B | USD 4.09 B (2024) | The definition appears broader and may include adjacent value elements beyond materials sold for permanent installation, which can inflate the total versus a materials only view. |

The comparison shows that scope choices explain more of the spread than math differences do, especially around whether hard surfaces and installation related value are included. By keeping the definition tied to permanent installation materials and checking it against trade, construction, and channel signals, we end up with a practical number that can be recreated and updated without relying on hidden datasets.

Key Questions Answered in the Report

What is the 2026 size and 2031 outlook for Saudi Arabia floor covering?

It is valued at USD 315.48 million in 2026 and is projected to reach USD 453.64 million by 2031 at a 7.53% CAGR. The trajectory aligns with Vision 2030 construction pipelines and a stronger non-oil base that supports project delivery.

Which flooring products lead and which are growing fastest in Saudi Arabia?

Ceramic tiles lead with a 49.38% share in 2025. Luxury vinyl tiles and planks are the fastest expanding at an 11.64% CAGR through 2031 as specifications favor modular and low-VOC options.

Where is demand strongest by end use, and which uses are accelerating?

Residential accounts for 71.36% in 2025. Commercial is accelerating at 11.22% CAGR through 2031 on the back of hotel, office, retail, education, and public building pipelines.

How are regulations shaping specifications and procurement in Saudi Arabia floor covering?

The Environmental Law under Royal Decree M/165 enforces low-VOC thresholds from January 2025. The Saudi Green Building Code 2024 makes energy and emissions criteria central to permitted projects, lifting demand for certified porcelain and compliant vinyl.

What is the impact of tariffs on wood and luxury vinyl pricing in Saudi Arabia?

Import duties of 12-20% raise landed costs for wood and luxury vinyl. This shifts price-sensitive selections toward domestic porcelain while prestige projects continue to specify imported finishes.

Which cities show the most momentum for floor covering, and why?

Riyadh held 34.35% share in 2025 and is forecast at 9.84% CAGR through 2031 due to a dense giga-project pipeline. Jeddah is rising with coastal hospitality and luxury residential tied to Red Sea tourism.

Page last updated on: