Sacroiliac Joint Fusion Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

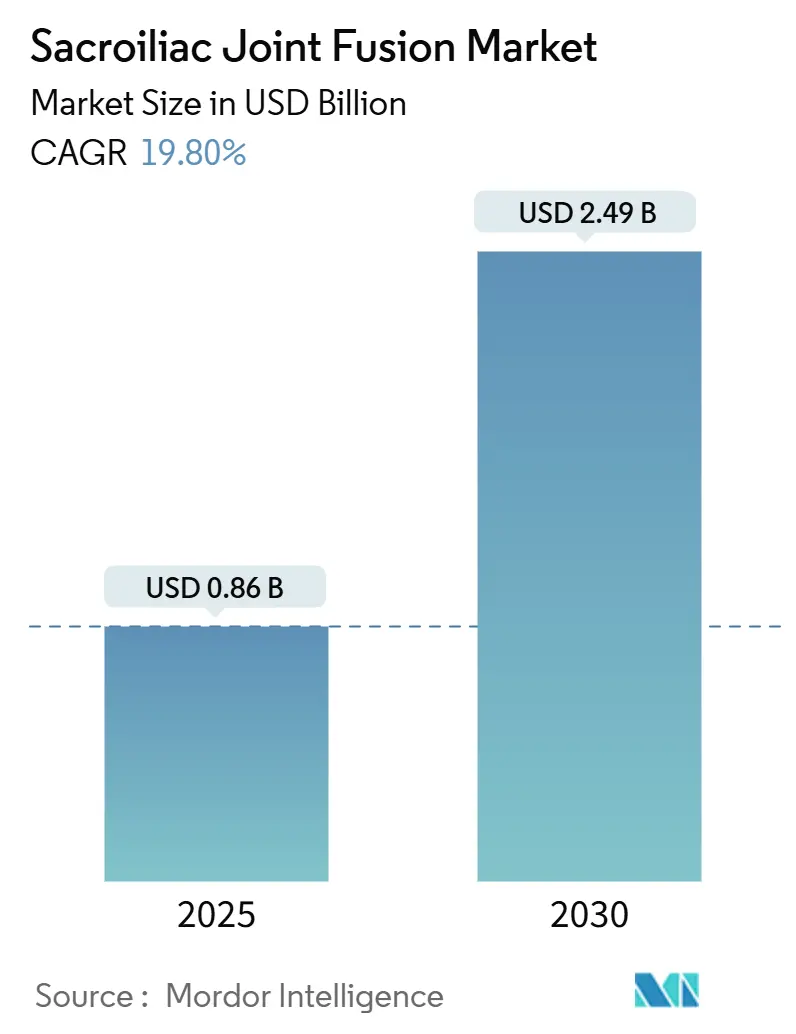

| Market Size (2025) | USD 0.86 Billion |

| Market Size (2030) | USD 2.49 Billion |

| Growth Rate (2025 - 2030) | 19.80% CAGR |

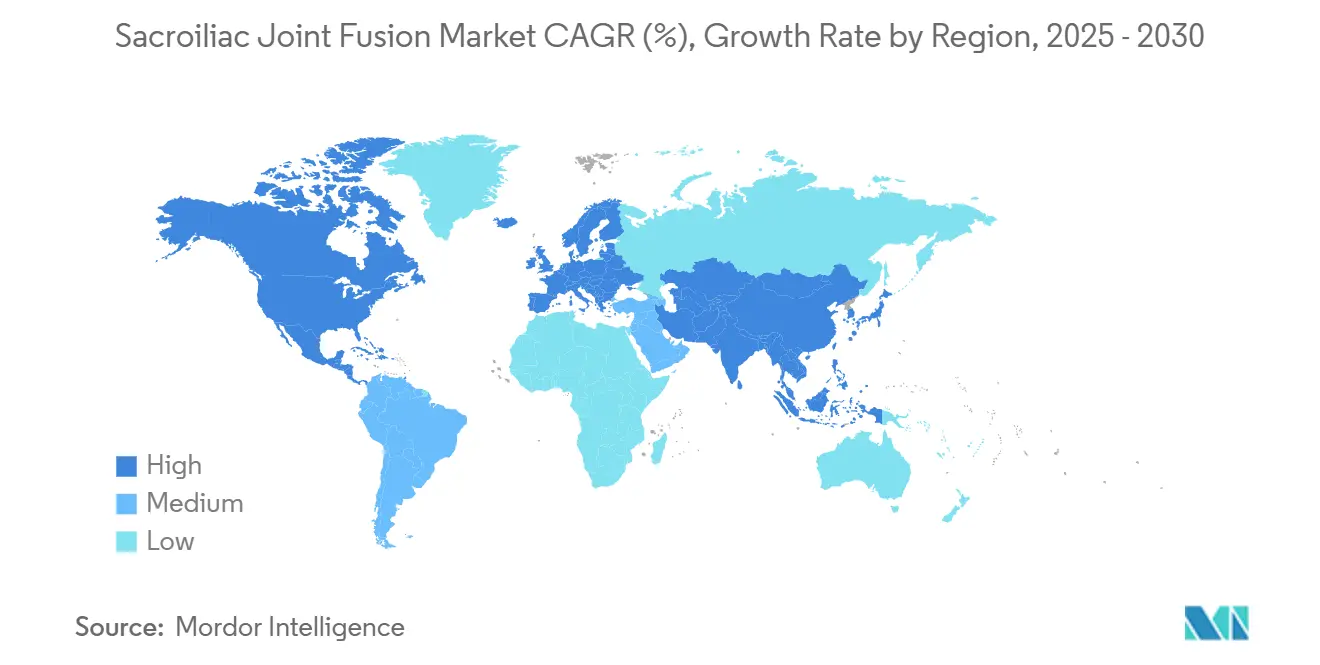

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sacroiliac Joint Fusion Market Analysis by Mordor Intelligence

The sacroiliac joint fusion market was valued at USD 0.86 million in 2025 and, growing at a 19.8% CAGR, is projected to reach USD 2.49 million by 2030. Sustained growth is propelled by the rising clinical recognition of sacroiliac joint dysfunction in chronic lower-back-pain pathways, accelerating adoption of minimally invasive techniques, and favorable reimbursement reforms such as CPT 27279. Titanium implants retain leadership, yet 3-D–printed porous titanium systems are gaining momentum on the back of superior osseointegration and custom-fit potential. North America commands the largest regional foothold as procedural volumes ramp up among interventional pain and spine specialists, while Asia-Pacific delivers the fastest regional CAGR, thanks to expanding surgical capacity and improving payer coverage. Competitive intensity continues to rise as established players leverage evidence-led marketing and new entrants pursue acquisition-enabled scale.

Key Report Takeaways

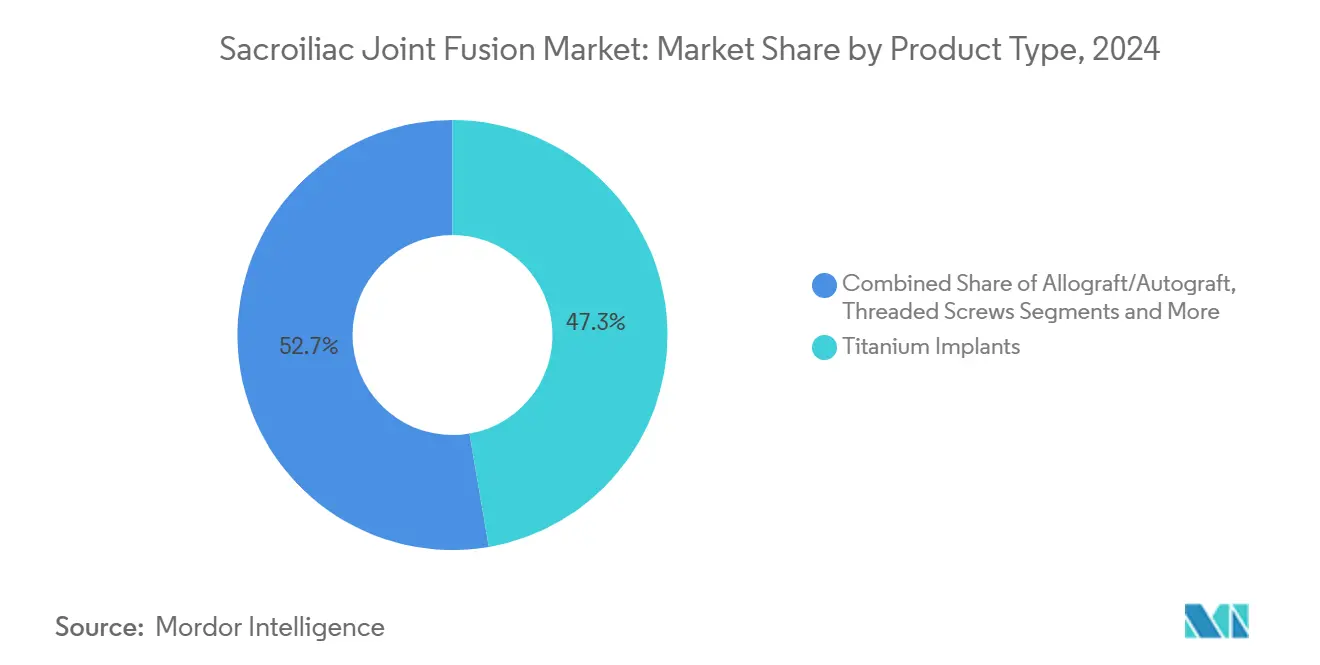

- By product type, titanium implants led with 47.3% revenue share in 2024; 3-D–printed porous titanium is advancing at a 23.4% CAGR through 2030.

- By surgical approach, the lateral minimally invasive technique held 62.4% of the sacroiliac joint fusion market share in 2024. In contrast, posterior and posterior-oblique procedures are forecast to rise at a 25.1% CAGR during 2025-2030.

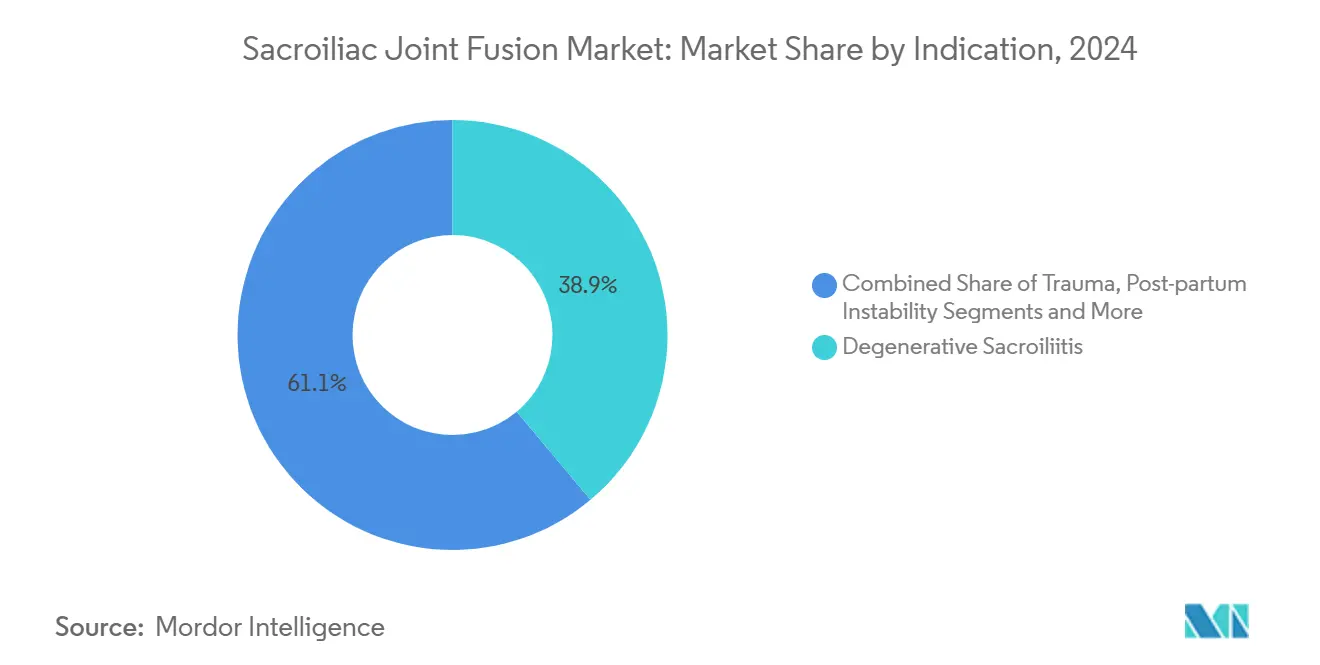

- By indication, degenerative sacroiliitis accounted for 38.9% of the sacroiliac joint fusion market size in 2024; post-lumbar-fusion pain is projected to expand at a 24.6% CAGR through 2030.

- By end user, hospitals captured 66.2% of the sacroiliac joint fusion market share in 2024; ambulatory surgical centers are tracking a 21.2% CAGR to the end of the decade.

- By geography, North America controlled 55.6% of revenue in 2024; Asia Pacific is projected to post the fastest 16.7% CAGR to 2030.

Global Sacroiliac Joint Fusion Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of minimally invasive SI joint fusion | +4.20% | Global; North America leads | Short term (≤ 2 years) |

| Growing geriatric population with sacroiliitis & lower-back pain | +3.80% | Global; developed markets | Long term (≥ 4 years) |

| Expansion of reimbursement (CPT 27279 & X034T) | +3.10% | North America & EU | Medium term (2-4 years) |

| Shift to outpatient settings led by pain physicians | +2.90% | North America expanding to APAC | Short term (≤ 2 years) |

| 3-D–printed porous implants accelerating fusion | +2.70% | Global tech hubs | Medium term (2-4 years) |

| Bundled-payment lumbar-fusion add-on economics | +2.10% | North America; EU pilots | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Minimally Invasive SI Joint Fusion

Minimally invasive procedures jumped 592% from 2015 to 2020, while open techniques declined, underscoring a clear paradigm change. Non-surgical specialists now perform 52.1% of percutaneous fusions, widening the provider base beyond traditional spine surgeons and speeding procedure diffusion.[1]Andrew M. Hersh et al., “Contemporary Trends in Minimally Invasive Sacroiliac Joint Fusion,” Neurosurgery, journals.lww.com The SECURE multicenter study reported a 73.5% responder rate at 12 months for posterior approaches, with fewer complications than lateral access, thereby reducing payer friction for coverage. Medicare cemented these gains by adding CPT 27279, and subsequent private-payer alignments improved reimbursement-to-charge ratios, making outpatient delivery financially attractive. FDA breakthrough device designations, such as the iFuse TORQ TNT, reinforce the clinical-innovation feedback loop that sustains this driver.

Growing Geriatric Population With Sacroiliitis & Lower-Back Pain

Population aging intensifies demand because degenerative sacroiliitis disproportionately affects adults over 65, a cohort projected to expand through 2030 by the World Health Organization.[2]Centers for Medicare & Medicaid Services, “Billing and Coding: Sacroiliac Joint Procedures,” cms.gov Longitudinal evidence shows 23% of multi-level lumbar-fusion patients develop sacroiliac joint pain, a statistic that elevates revision-surgery volumes and fuels device utilization. 3-D–printed porous titanium implants deliver superior bone ingrowth, an attribute valued by older patients who need dependable fusion stability. Study data reveal pain scores fell from 6.8 to 3.8 within six months post-fusion and remained durable for five years, reinforcing the long-term efficacy narrative. This demographic driver is particularly pronounced in mature economies with established reimbursement infrastructures that can absorb per-case costs.

Expansion of Reimbursement (CPT 27279 & X034T)

Medicare’s dedicated CPT 27279 code standardized billing for minimally invasive fusion, cutting administrative delays and incentivizing outpatient migration.[3]World Health Organization, “World Population Ageing: Highlighting the Rising Share of Adults Aged 65 Years and Older,” who.int The X034T add-on further supports advanced implant technologies, while CMS transitional pass-through status for SI-BONE’s iFuse Bedrock Granite locks in elevated outpatient payments for three years. Cost-utility analyses demonstrate that sacroiliac joint fusion attains cost neutrality by year six when weighed against prolonged conservative-care regimens. Commercial payers have followed suit, broadening medical-policy coverage and reducing prior-authorization hurdles. Evidence-based guidelines from global spine societies corroborate coverage for transfixation devices, though debates continue over non-transfixation approaches, creating stratified reimbursement niches.

Shift to Outpatient Settings Led by Pain Physicians

Ambulatory surgical centers (ASCs) now absorb a growing share of procedures as minimally invasive approaches shrink operating times and convalescence windows. Interventional pain physicians have leveraged their diagnostic-injection expertise to transition seamlessly into proceduralists conducting posterior fusions, thereby enlarging the provider pool. The financial calculus for ASCs is favorable because higher margin capture aligns with bundled-payment initiatives, spurring capital investments in imaging and navigation technologies. Regional adoption differences track state-level regulations governing ASC licensure and professional-practice statutes. Facility operators focus on standardized training curricula to accelerate credentialing and minimize learning-curve complications, sustaining outpatient momentum.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited randomized long-term outcome data | -2.40% | Global | Medium term (2-4 years) |

| High device & procedure cost in emerging markets | -1.80% | APAC, Latin America, MEA | Long term (≥ 4 years) |

| Scrutiny of structural allograft failure rates | -1.20% | North America & EU | Short term (≤ 2 years) |

| Surgeon credentialing gaps for new posterior tech | -0.90% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Randomized Long-Term Outcome Data

Most studies reporting on sacroiliac joint fusion extend only to two-year endpoints, limiting definitive comparative-effectiveness assessments. Payors scrutinize the absence of large-scale randomized controlled trials when crafting local-coverage policies, which can throttle reimbursement for emerging posterior devices. Professional bodies urge standardized outcome metrics, but until five-year randomized evidence matures, conservative clinicians remain cautious. Sponsors are funding multi-arm trials due to be completed in 2027 that aim to close this evidence gap. While interim observational data are promising, the restraint tempers some near-term adoption, especially in cost-sensitive systems.

High Device & Procedure Cost in Emerging Markets

Premium sacroiliac implants often exceed the healthcare budgets of patients in lower-income nations, where price-sensitive public insurers dominate. Limited infrastructure and specialist scarcity further restrict the diffusion of minimally invasive spine surgery. Local manufacturing partnerships and tiered pricing strategies are gaining traction in India’s spine sector, but broad affordability remains elusive. The gap creates fertile ground for cost-competitive domestic suppliers yet introduces regulatory-quality concerns. Consequently, Asia-Pacific’s CAGR leadership is uneven—rapid in developed economies, slower in fiscally constrained geographies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Titanium Dominance Drives Innovation

Titanium implants captured 47.3% of 2024 revenue, illustrating enduring reliance on a material whose modulus of elasticity approximates cortical bone and mitigates stress shielding. Sacroiliac joint fusion market size projections show titanium continuing to anchor absolute sales even as porous variants scale. Allograft options remain niche, reserved for biologically focused posterior procedures. The sacroiliac joint fusion market is witnessing sharp growth in 3-D–printed porous titanium, clocking a 23.4% CAGR through 2030 amid mounting evidence for accelerated fusion and patient-specific design flexibility. Hybrid devices combining PEEK cages with porous titanium coatings are emerging to bridge the radiolucency and osseointegration divide, hinting at future category segmentation.

The innovation race pivots on surface topography, with additive-manufactured trabecular lattices enabling bone-through-growth and thus shortening the biological lag to fusion. Competitive differentiation increasingly relies on proprietary printing algorithms and AI-guided design that tailors porosity gradients to individual pelvic morphology. Although per-unit pricing for 3-D–printed implants is higher, hospitals quantify cost offsets through reduced revision risk. In developing markets, titanium remains preferable owing to well-established supply chains and predictable regulatory pathways, reinforcing its position even as premium segments gain share.

By Surgical Approach: Lateral Techniques Lead Despite Posterior Growth

The lateral minimally invasive approach held 62.4% of sacroiliac joint fusion market share in 2024, a dominance underpinned by a decade of surgeon familiarity and robust navigation tools. Sacroiliac joint fusion market size expansion continues in this segment, albeit at a maturing pace as posterior approaches accelerate. Posterior and posterior-oblique techniques are rising at a 25.1% CAGR, favored by interventional pain physicians who value prone positioning and limited soft-tissue disruption. Biomechanical data indicate that posterior integrated transfixation systems supply superior rotational stability with less bone removal, a selling point for osteoporotic patients.

Surgeon preference is sliding toward access strategies that harmonize operating-room efficiency with safety. Lateral access retains traction for complex anatomies requiring triangulated fixation, whereas posterior access excels in outpatient settings requiring minimal hardware and shorter incisions. Open posterolateral fusion has retrenched into small revision niches due to higher morbidity. Technology vendors are tailoring implant lines to accommodate both trajectories, ensuring cross-approach compatibility and thus hedging against clinical-paradigm shifts.

By Indication: Degenerative Conditions Drive Primary Demand

Degenerative sacroiliitis generated 38.9% of sacroiliac joint fusion market size in 2024, mirroring the demographic swell of seniors presenting with joint degeneration. Clear ICD coding and payer familiarity streamline patient access pathways. Post-lumbar-fusion pain, however, clocks the fastest CAGR at 24.6% as awareness of adjacent-segment disease sharpens among spine surgeons. Sacroiliac joint disruption linked to trauma or postpartum instability commands smaller but stable shares, buoyed by expanding diagnostic sophistication in orthopedic and obstetric circles.

Longer spinal arthrodesis constructs accentuate stress transfer into the sacroiliac complex, creating a structural substrate for future dysfunction. Consequently, screening protocols at pre-fusion planning stages increasingly include sacroiliac assessment, feeding downstream procedural volumes. Trauma-driven indications lean toward immediate fixation using high-load capacity implants, whereas degenerative cases prioritize osteoconductive surfaces. Vendors are diversifying implant portfolios to align with nuanced biomechanical demands across indication subsets.

By End User: Hospital Dominance Faces ASC Challenge

Hospitals maintained 66.2% sacroiliac joint fusion market share in 2024, sustained by comprehensive imaging, ICU back-up, and multidisciplinary teams necessary for complex case mixes. Nevertheless, ambulatory surgical centers are expanding at a 21.2% CAGR as procedure times compress and payer bundles incentivize lower-cost venues. Specialty orthopedic clinics and pain-management centers are converging on minimally invasive posterior technologies that fit their ambulatory workflows. Academic institutions function as innovation incubators and credentialing hubs, indirectly influencing adoption curves though they command modest direct volumes.

Outpatient migration is accelerating as ASCs leverage predictable operating-room turn-times and patient-satisfaction advantages. Hospitals are responding by spinning off hospital-owned ASCs or partnering with physician groups to maintain procedural capture. Capital investment decisions now ubiquitously assess sacroiliac joint fusion throughput potential when budgeting for robotic navigation or 3-D imaging upgrades, reaffirming the procedure’s strategic role in musculoskeletal service-line planning.

Geography Analysis

North America held 55.6% of sacroiliac joint fusion market share in 2024, driven by payer clarity and a high density of fellowship-trained spine and pain specialists. Medicare’s CPT 27279 and supportive private-payer policies catalyzed volume growth, with 12,978 documented procedures from 2015-2020 underscoring entrenched adoption. Canada follows a controlled diffusion path through centralized technology assessments, dampening volume relative to population size. Mexico’s private-health sector is tapping medical-tourism inflows that often bundle sacroiliac fusion with other minimally invasive spine procedures, adding incremental demand.

Europe presents a multifaceted landscape wherein Germany tops case counts amid comprehensive statutory insurance coverage. France and Italy accelerate through academic-industry collaborations that validate new implant designs under MDR oversight. The United Kingdom leverages NICE pathways to arbitrate cost-utility thresholds, selectively endorsing high-evidence devices. Spain is widening reimbursement after hospital data showed reduced opioid prescriptions post-fusion. European regulatory rigor ensures quality but can elongate time-to-market, nudging suppliers toward parallel submission strategies.

Asia-Pacific registers the highest regional CAGR at 16.7% through 2030. Japan’s aging demographic aligns seamlessly with sacroiliac fusion’s value proposition, supported by efficient universal coverage. China’s urban tertiary hospitals are early adopters, but rural penetration is muted by budget ceilings. India illustrates dichotomous dynamics: private metros deploy cost-effective domestic implants, yet public facilities lag owing to procurement constraints. Australia and South Korea fill out the region’s mature pockets, integrating sacroiliac fusion into comprehensive spine-service lines. The region’s growth arc hinges on localized manufacturing, skill-transfer programs, and payer recognition of long-term cost offsets.

Competitive Landscape

The sacroiliac joint fusion market demonstrates moderate concentration. SI-BONE remains the clear leader, posting 26% year-over-year revenue growth to USD 49 million in Q4 2024 and delivering its inaugural positive adjusted EBITDA, buoyed by an installed base exceeding 115,000 procedures. Its strategy revolves around peer-reviewed data (over 100 publications) and expansive surgeon-training networks surpassing 4,300 physicians globally. Breakthrough-device iterations like iFuse TORQ TNT extend the brand family into pelvic-fracture fixation, diversifying revenue streams.

Nevro’s USD 40 million acquisition of Vyrsa Technologies in 2025 signaled competitive convergence between neuromodulation and structural fusion, creating a chronic-pain one-stop portfolio. Aurora Spine promotes posterior SiLO TFX systems anchored by biomechanical superiority claims, positioning against lateral incumbents. Large diversified players such as Globus Medical and Medtronic leverage existing distribution to fast-track share capture once proprietary lateral approaches reach patent cliffs. FDA breakthrough pathways and CMS transitional payments amplify first-mover advantages yet invite fast-follower challenges as additive-manufacturing democratizes design.

Competition now coalesces around three vectors: (1) additive manufacturing and AI-driven personalization; (2) procedure-site migration from hospital to ASC; and (3) integrated digital-health tools for remote rehabilitation monitoring. Suppliers vying for emerging-market entry pursue cost-engineered titanium screws coupled with training partnerships to surmount infrastructure deficits. Strategic alliances, such as Osteotec’s 2024 pact with SI-BONE, illustrate channel co-development aimed at cross-border penetration. Moderate consolidation potential persists, but innovation cadence suggests a dynamic equilibrium favoring agile, evidence-rich organizations.

Sacroiliac Joint Fusion Industry Leaders

SI-BONE Inc.

Medtronic plc

PainTEQ LLC

Globus Medical Inc.

Orthofix Medical Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Nevro acquired Vyrsa Technologies for USD 40 million, adding the FDA-cleared V1 SI Fusion System with 3-D–printed transfixing anchors to its chronic-pain portfolio.

- October 2024: SI-BONE performed first-in-human cases with iFuse TORQ TNT, an FDA-designated breakthrough implant for pelvic fractures.

- October 2024: FDA cleared Vy Spine’s 3-D–printed spinal fusion device, advancing additive manufacturing in spine surgery

Global Sacroiliac Joint Fusion Market Report Scope

| Titanium Implants |

| 3D-Printed Porous Titanium Implants |

| Allograft / Autograft Bone Implants |

| Threaded Screws & Plates |

| Hybrid / Composite Implants |

| Minimally Invasive Lateral Transiliac |

| Minimally Invasive Posterior / Posterior-Oblique |

| Open Posterolateral Fusion |

| Inferior Intra-Articular Approach |

| Combined Sacropelvic Fixation |

| Degenerative Sacroiliitis |

| SI Joint Disruption / Trauma |

| Post-partum Pelvic Instability |

| Revision After Lumbar Fusion |

| Others (Tumor, Infection) |

| Hospitals |

| Ambulatory Surgical Centers (ASCs) |

| Specialty Orthopedic & Spine Clinics |

| Pain Management Centers |

| Academic & Research Institutions |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Titanium Implants | |

| 3D-Printed Porous Titanium Implants | ||

| Allograft / Autograft Bone Implants | ||

| Threaded Screws & Plates | ||

| Hybrid / Composite Implants | ||

| By Surgical Approach | Minimally Invasive Lateral Transiliac | |

| Minimally Invasive Posterior / Posterior-Oblique | ||

| Open Posterolateral Fusion | ||

| Inferior Intra-Articular Approach | ||

| Combined Sacropelvic Fixation | ||

| By Indication | Degenerative Sacroiliitis | |

| SI Joint Disruption / Trauma | ||

| Post-partum Pelvic Instability | ||

| Revision After Lumbar Fusion | ||

| Others (Tumor, Infection) | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers (ASCs) | ||

| Specialty Orthopedic & Spine Clinics | ||

| Pain Management Centers | ||

| Academic & Research Institutions | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the sacroiliac joint fusion market in 2030?

The market is forecast to reach USD 2.49 million by 2030, expanding at a 19.8% CAGR.

Which product segment is growing fastest?

3-D-printed porous titanium implants are advancing at a 23.4% CAGR thanks to superior osseointegration.

Which surgical approach is expected to gain share most rapidly?

Posterior and posterior-oblique minimally invasive techniques are projected to rise at 25.1% CAGR between 2025-2030.

Why is Asia-Pacific considered the fastest-growing region?

Rising surgical capacity, demographic pressure, and expanding reimbursement models drive a 16.7% regional CAGR.

How are reimbursement changes influencing procedure adoption?

Dedicated CPT codes, pass-through payments, and bundled-care economics improve provider margins and speed outpatient migration.

Who are the key market leaders?

SI-BONE leads, followed by companies such as Nevro (after Vyrsa acquisition), Aurora Spine, Globus Medical, and Medtronic.

Page last updated on: