Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

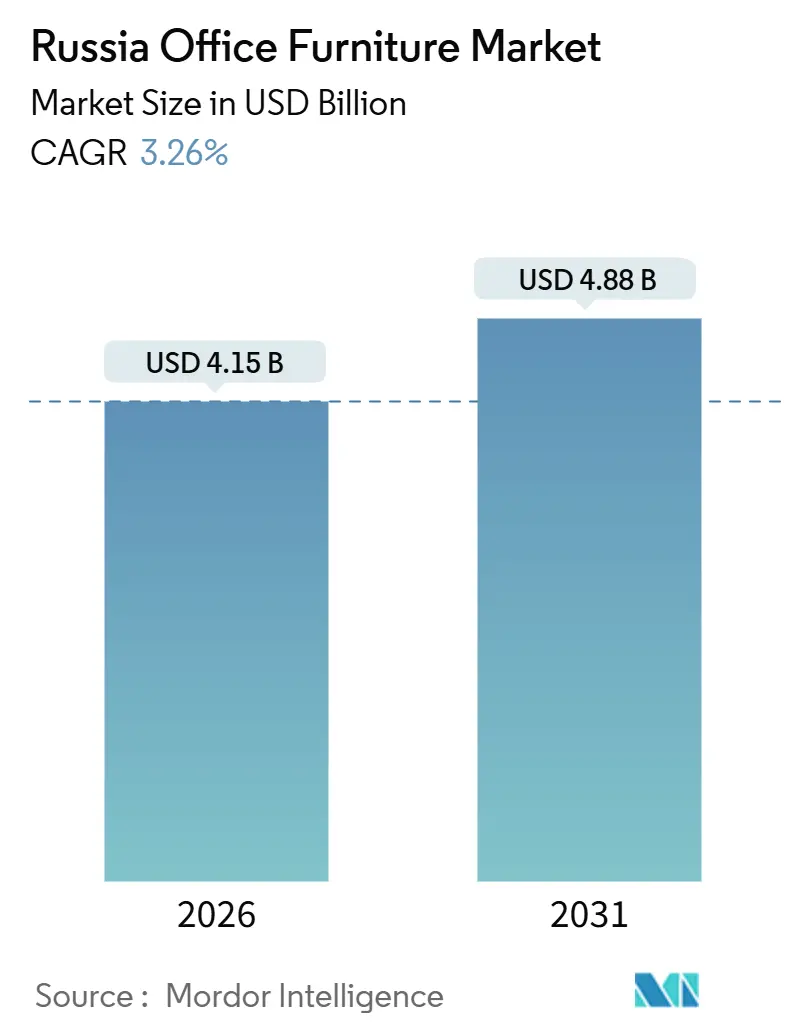

| Market Size (2026) | USD 4.15 Billion |

| Market Size (2031) | USD 4.88 Billion |

| Growth Rate (2026 - 2031) | 3.26% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Office Furniture Market Analysis by Mordor Intelligence

The Russia office furniture market size is USD 4.15 billion in 2026 and is projected to reach USD 4.88 billion by 2031, registering a 3.26% CAGR from 2026 to 2031. Growth conditions remain uneven as manufacturers navigate a 16% key rate that raises financing costs, increasing the emphasis on pre-leased projects and state tenders, which provide higher visibility and more predictable cash flows [1]Source: Bank of Russia, “The Bank of Russia’s Statement on Monetary Policy,” Bank of Russia, cbr.ru. Fit-out intensity remains supported by commissioning activity and longer pre-lease pipelines, which protect build-out schedules and direct orders to compliant vendors under localization rules. E-commerce platforms continue to open access to provincial buyers and SMEs, enabling online configuration, faster delivery, and transaction tools that expand assortment reach. Ergonomic mandates and workplace health guidance also influence both B2B refits and B2C home-office purchases, with specifications rooted in national labour guidelines and certification norms that push demand toward tested and documented products.

Key Report Takeaways

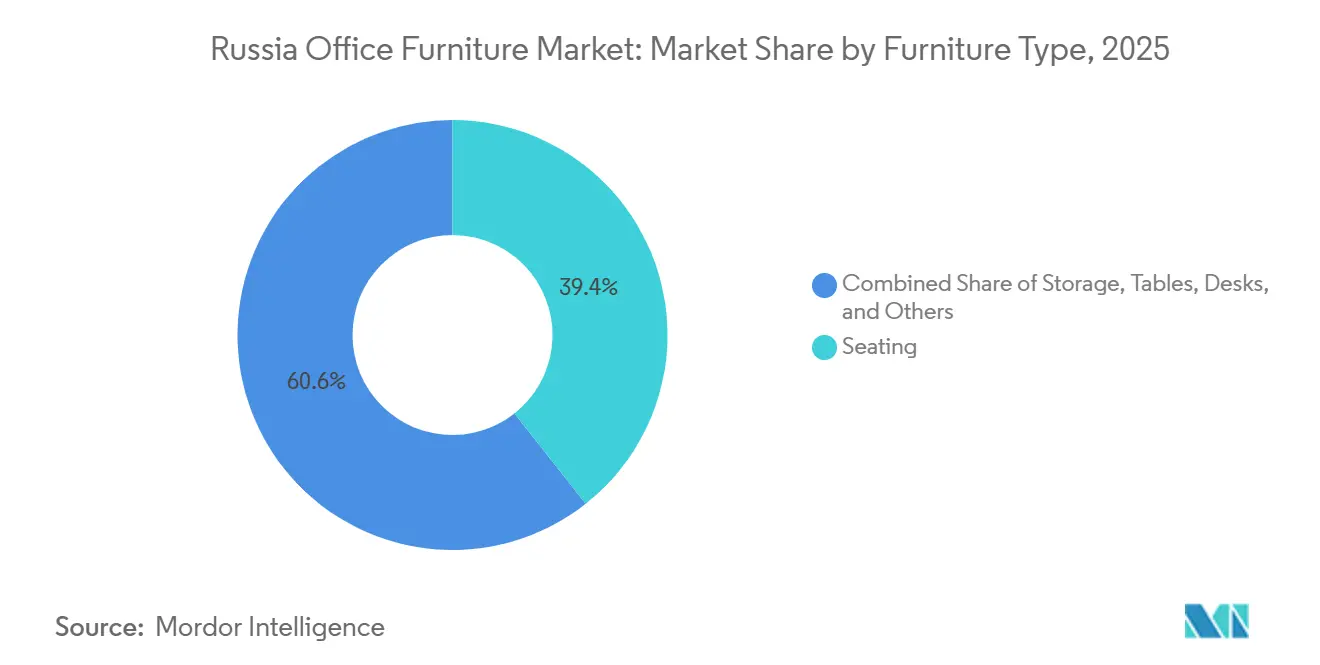

- By furniture type, Seating led with 39.37% of the Russia office furniture market share in 2025, while Desks are projected to expand at a 7.98% CAGR through 2031.

- By distribution channel, B2B held 54.87% of the Russia office furniture market share in 2025, while Retail is forecast to grow at an 8.87% CAGR to 2031.

- By geography, the Central Federal District accounted for 48.87% of the Russia office furniture market share in 2025 and is set to advance at a 5.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Russia Office Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Office real estate commissioning and pre-leased supply in Moscow | +1.8% | Central Federal District, spill-over to Northwestern Federal District | Medium term (2-4 years) |

| Procurement localization under PP 616/2013 | +1.5% | National, strongest in the Central Federal District | Long term (≥ 4 years) |

| E-commerce and marketplace penetration | +1.2% | National, early gains in Central, Volga, Ural, expanding to Siberian | Short term (≤ 2 years) |

| Hybrid or remote work and ergonomic demand | +0.9% | National, concentrated in major urban centres | Medium term (2-4 years) |

| Adoption of acoustic booths and partitions | +0.6% | Central and Northwestern Federal Districts | Short term (≤ 2 years) |

| Smart or height-adjustable desks and tech-integrated workstations | +0.4% | Central Federal District, early adopters in tech | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Office Real Estate Commissioning and Pre-Leased Supply in Moscow Sustains Fit-Out Demand into the Late 2020s

Commissioning activity in Moscow remained strong into late 2025, which aligned turnkey furniture packages to pre-leased pipelines and sustained order flow into 2026 handovers. Pre-lease structures reduce developer risk and anchor specifications earlier in the cycle, which locks in compliant domestic vendors for integrated design, supply, and installation scopes under localization rules. The 16% policy rate raises the hurdle for speculative projects, so capital prioritizes pre-committed office space that is more likely to proceed to fit-out without scope cuts or schedule drift. Manufacturers aligned to major tenants and campus-scale projects reported stable pipelines and multi-year production plans, which offset volume headwinds in discretionary refurbishments. Vacancy stayed tight relative to an 8% equilibrium reference point, which helped landlords uphold rent increases that support capex for interior upgrades and related furnishings across higher-grade buildings.

Procurement Localization (PP 616/2013) Shifts Public-Sector and SOE Demand to Domestic Producers

The localization framework channels public-sector and state-affiliated orders to domestic and EAEU-origin suppliers, which creates a stable demand pool for compliant office furniture producers that can document origin and certification. Eligibility depends on registration and technical conformance, which raises barriers for import-heavy assemblers and rewards integrated manufacturers able to internalize key components and documentation. Large financial and energy groups cascade localization through contractor requirements, so indirect demand also tilts to domestic sources even outside formal tender procedures. Incumbents that invest in compliant processes, quality systems, and lab testing have a structural advantage in government-linked projects and multi-year frameworks. The VAT rate rise to 22% that starts from early 2026 creates cost-structure nuances across foreign and domestic supply chains, so working-capital and tax-treatment planning remain central to margin defense among local manufacturers.

E-Commerce And Marketplace Penetration Accelerate B2B And B2C Sales and Assortment Breadth

Marketplace features now include configuration tools, visual previews, and distributed fulfillment, which cut delivery times to short windows across major cities and extend reach across regional centers. These platforms have grown as procurement channels for SMEs and regional branches that seek transparent pricing, faster dispatch, and invoice-ready transactions. The Russia office furniture market benefits from demand aggregation on trusted portals, which narrows the historical advantage of local distributors that once depended on geographic exclusivity. Commission structures and co-marketing fees trade off with access to very large registered-user bases, which reshapes merchandising and accelerates product refresh cycles for responsive brands. As omnichannel execution becomes standard, logistics speed and SKU depth often outweigh traditional brand awareness in purchasing decisions across the Russia office furniture market.

Hybrid Or Remote Work Raises Demand for Ergonomic Seating and Home-Office Desks

Hybrid patterns continue to influence office reconfigurations and home-office setups, with ergonomic specifications embedded into procurement practices under labor guidance. Corporate facility teams are adopting mobility and adjustability as standard attributes to support hot-desking and activity-based zones, which increases the share of modular seating and benching systems in the Russia office furniture market. On the home side, consumers proceed with incremental upgrades targeted at health and posture rather than large-scale remodels, which supports mid-priced ergonomic lines from domestic suppliers. Installation options on marketplaces expand affordability for regional buyers, which brings remote and hybrid workers into the addressable base for performance-certified seating and desks. These shifts reinforce compliance and testing as differentiators, since public-sector and large private buyers increasingly specify conformance to ergonomics and safety standards in bid documents.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High interest rates and softer corporate or residential demand | -1.4% | National, steeper outside the Central Federal District | Short term (≤ 2 years) |

| Input cost volatility and component import frictions | -0.9% | National, severe where customs is a primary entry point | Medium term (2-4 years) |

| Customs reclassification risk on fittings duties | -0.7% | National across major ports of entry | Short term (≤ 2 years) |

| Compliance burden for TR CU 025/2012 EAC or GOST | -0.3% | National across the EAEU supply chain | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Interest Rates and Softer Corporate or Residential Demand Slow Large Refits

The 16% key rate raises the cost of inventory and project financing, which lowers the net present value of long-dated leases and dampens discretionary refits in the Russia office furniture market. Corporate buyers respond by extending replacement cycles, reducing average ticket values, and favoring standardized modular systems over bespoke collections. Financing conditions tightened at the supplier level as well, with shorter tenors and stricter covenants reinforcing the advantage of low-leverage manufacturers that can extend terms to key customers. Demand resilience skews toward the Central Federal District, where office pipelines and government contracting remain more stable, which keeps the Russia office furniture market more concentrated around the capital. Consumer-facing categories linked to home offices continue to sell through, but the mix shifts toward value tiers when real wages trail headline inflation pressure.

Input Cost Volatility and Component Import Frictions Lift End-Prices

Tariff exposure, customs classification shifts, and currency swings raise landed costs for metal hardware, actuators, and fittings that are integral to seating and desk systems in the Russia office furniture market. Domestic material inputs are also priced higher due to competing demand, which pushes producers toward backward integration strategies that internalize component manufacturing and stabilize bill-of-materials costs. Manufacturers have staggered price increases to protect share while covering cost inflation, which leaves margins sensitive to further shocks in transport and import fees. VAT treatment at 22% from early 2026 requires careful tax planning along multi-stage domestic production chains to avoid a cumulative burden relative to single-levy imports[2]Source: President of Russia, “Meeting on Support for Investment Projects in Domestic Industry,” Office of the President, kremlin.ru. Scale players hedge through multi-year supply contracts and currency tools, while sub-scale assemblers face spot markets and higher working-capital costs that can pressure continuity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Furniture Type: Desks Surge on Hybrid-Work and Ergonomic Mandates

Seating accounted for 39.37% of revenue in 2025, while desks are the fastest-growing category with a 7.98% CAGR through 2031, which aligns with hybrid layouts and height-adjustability adoption within the Russia office furniture market. This mix supports modular benching, mobile task seating, and tech-ready workstations that compress fit-out schedules and simplify reconfiguration across projects in the capital and major regional centers. Ergonomics guidance drives standardization of adjustability and posture support features, so buyer specifications emphasize certified components and documented conformance. The Russia office furniture industry reflects this shift in product development roadmaps, with integrated producers calibrating value lines around mandated attributes and support services. As desk systems add height variability and power integration, lifecycle costs and service commitments become more important to procurement teams that assess durability and warranty as part of the total cost of ownership.

Within this category, acoustic dividers, collaborative tables, and lounge seating complement open-office layouts and video-call intensity, which extends demand to add-on components that raise functional performance without extensive partitioning. Certified solutions help public buyers enforce tender specifications that require conformance to ergonomic and safety standards, which favors incumbents with in-house compliance capabilities in the Russia office furniture market. The Russia office furniture market size for desks is aligned with adoption beyond technology firms, as financial and administrative tenants extend wellness policies to more facilities under standardized fit-out kits.

By Distribution Channel: B2C Retail Accelerates Amid E-Commerce Expansion and Home-Office Demand

B2B channels held 54.87% of shipments by value in 2025, and B2C retail is projected to post an 8.87% CAGR as marketplaces and home centers broaden reach and speed across regions in the Russia office furniture market. Online channels now serve both consumers and SME buyers with configuration, invoicing, and fast fulfillment, which changes the basis of competition from legacy distribution coverage to digital merchandising and logistics. As retail share expands, manufacturers optimize assortments and packaging for parcel networks and hub-and-spoke models, which raises the role of co-marketing and ratings in demand generation. Framework contracts and project scopes still define the largest single orders, so mixed-channel portfolios remain the dominant strategy for resilient revenue in the Russia office furniture market. Value growth in B2C home-office kits reinforces the link between labor guidance and retail assortment, as ergonomics becomes a baseline promise rather than a niche feature set.

Home centers and specialist showrooms continue to capture buyers who prefer coordinated purchases across lighting, cable management, and décor, which integrates furniture into one-stop projects across regional cities. Manufacturers leverage marketplaces to enter distant regions without physical stores, which helps balance capital discipline with nationwide exposure across the Russia office furniture market. The Russia office furniture market size associated with B2B frameworks remains anchored by tender-driven orders and pre-leased project kits, which sustains average order values well above consumer transactions. As B2C grows, retailers adopt B2B features such as bulk pricing and project management, while B2B vendors deploy digital catalogs and rapid-ship programs to protect their share. This convergence lifts standards for service and fulfillment, which ultimately raises the competitive bar across the Russia office furniture industry.

Geography Analysis

The Central Federal District led with a 48.87% share in 2025 and a forecast 5.24% CAGR to 2031, underpinned by concentrated commissioning, federal procurement, and headquarters demand centered in the capital in the Russia office furniture market. Pre-leased projects in Moscow anchor turnkey fit-outs and sustain supplier pipelines, which give integrated producers a consistent schedule of design, supply, and installation scopes. Tight vacancy relative to equilibrium allows rent pass-throughs that keep interior upgrades viable, which supports higher-value furniture programs in Grade A and B-plus buildings. Project delivery windows are compressed, which favors suppliers with proximity to the capital and the ability to staff installation teams at scale in the Russia office furniture market. The Russia office furniture market share earned by the district reflects this durability in institutional and corporate projects, which keeps the region structurally ahead of secondary markets on value capture.

The Northwestern Federal District contributes meaningful demand through St. Petersburg’s innovation and logistics roles, which support mid-tier ergonomic assortments and modular desk systems tuned to functional fit-outs. Office stock additions and R&D footprints maintain a steady cadence of projects, and procurement behavior emphasizes reliable delivery and standardized specifications across multi-site footprints in the Russia office furniture market. Logistics links to Baltic-facing trade and project contractors also influence supplier selection and service expectations, which pushes vendors to guarantee parts availability and after-sales support. Market growth in the district remains healthy yet below the Central District because corporate pipelines outside the city center are more cyclical and price sensitive. As acoustic, ergonomic, and modular categories gain traction, local manufacturers and distributors strengthen assortments that balance performance and affordability for the Russia office furniture market.

The Southern Federal District and the broader Rest of Russia pool together diverse demand across manufacturing, energy, services, and government, which produces steady but project-driven ordering patterns in the Russia office furniture market[3]Source: Expocentre, “MEBEL 2025: Relevant Issues of Furniture Retail,” Expocentre, meb-expo.ru. Regional hubs add office capacity at a smaller scale than Moscow, which sustains distributor networks and hybrid direct models that integrate showroom exposure with online selection. Logistics costs and distance from central production clusters require careful inventory planning, which can lengthen replenishment schedules unless suppliers dedicate regional stock or forward-deployed kits. As marketplaces reduce friction, buyers in these regions access standardized ergonomic ranges that meet national guidance, which helps narrow historical product gaps between the capital and regional cities. Through the forecast horizon, the Russia office furniture market size remains weighted to the Central Federal District on value, while volume expansion outside the capital continues in line with incremental office stock and SME formation.

Competitive Landscape

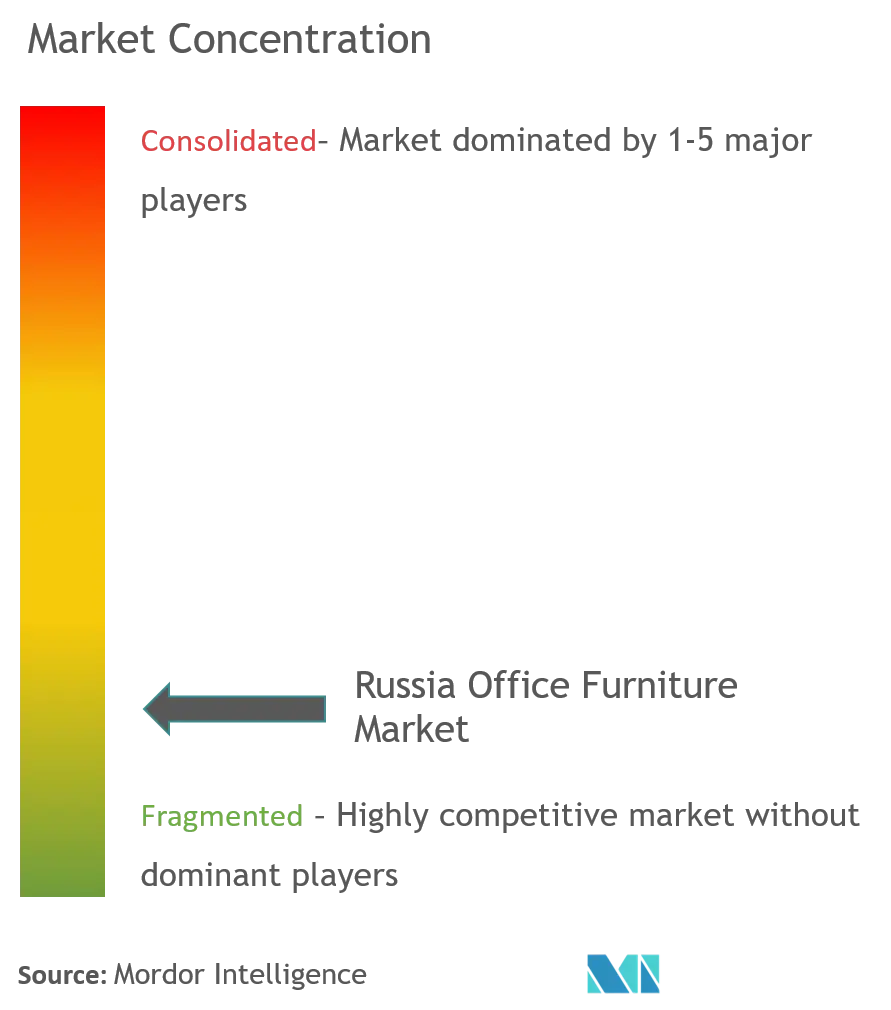

The Russia office furniture market remains fragmented, with no single player above 10% of national sales, which reflects the split between standardized categories with many rivals and specialized scopes with higher barriers and fewer credible bidders. Integrated manufacturers that combine certification speed, in-house component capability, and project execution tend to dominate government-linked and pre-leased pipelines under localization norms. FELIX and peers have invested in production planning and compliance processes that enable fast turn bid responses and consistent launch cycles, which is especially important when specifications finalize close to handover dates. Elevated policy rates reward firms with stronger balance sheets that can offer credit terms, which is difficult for smaller players that rely on factoring at higher costs. Omnichannel coverage has become a core differentiator that connects B2B frameworks, showrooms, and marketplaces into a single commercial system for the Russia office furniture market.

Retail-led disruptors have advanced through lower prices and rapid delivery, but installation, warranty servicing, and corporate financing often still favor established manufacturers and specialist B2B distributors. Marketplaces function as infrastructure rather than direct rivals for most producers, who trade commissions for reach and logistics that amplify assortment exposure in the Russia office furniture market. Private-label initiatives and vertical integration continue to appear on both retailer and distributor sides, which keeps value-chain boundaries fluid and rewards defensible assets like proprietary designs and sticky customer relationships. Company programs that align wellness data, IoT features, and ergonomic certifications position for premium segments where corporate buyers seek measurable outcomes and reported compliance. Certification and after-sales obligations limit the number of credible participants in specialized scopes, which moderates rivalry and sustains pricing discipline even as standardized lines see stronger price competition in the Russia office furniture market.

Exhibition platforms have assumed a larger role in technology diffusion and automation adoption, which helps suppliers offset labor constraints while raising throughput and consistency. MEBEL and WOODEX convenings report rising interest in robotics and high-efficiency manufacturing solutions across cutting, welding, painting, and upholstery, which supports investment in capacity with stronger unit economics in the Russia office furniture market. Company modernization programs reflect this trajectory and present new mid-price ergonomic lines that align with mainstream demand without compromising on conformance or serviceability. Producers increasingly bundle design support, site surveys, and maintenance into project proposals, which raises switching costs and improves lifecycle outcomes for customers. The Russia office furniture market will continue to favor suppliers that combine compliance readiness, execution speed, and multi-channel access over those relying on a single route to market or limited service scope.

Russia Office Furniture Industry Leaders

FELIX

Burokrat

Metta

Wildberries

Hoff

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Mebel and the Furniture Retail Forum 2025 in Moscow focused on digital transformation, omnichannel integration, and B2B or B2C convergence strategies across manufacturers and retailers.

- December 2025: Woodex-2025 gathered domestic and international equipment providers and spotlighted robotization and efficient furniture production themes, with an annual cadence from 2026.

- August 2025: Nordeco declared a year of large-scale modernization with new ergonomic lines, acoustic solutions, and technology investments supported by a digital configuration platform.

- February 2024: A presidential meeting detailed investment support for domestic industry and supply-chain resilience measures that impact furniture inputs and logistics.

Russia Office Furniture Market Report Scope

Office furniture refers to the essential furnishings in office settings, crucial for creating a comfortable, functional, and organized workspace. The report provides an in-depth analysis of the Russian office furniture market, exploring national accounts, the economic backdrop, and emerging segment-specific trends. It also sheds light on significant changes in market dynamics, presenting a comprehensive market landscape.

The Russia office furniture market is segmented by furniture type, distribution channel, and geography. By furniture type, the market is segmented into seating, tables, storage, desks, and other office furniture types. By distribution channel, the market is segmented into B2B/direct, B2C/retail, comprising home centres, specialty stores, online, and others. By geography, the market is segmented into Central Federal District, Northwestern Federal District, Southern Federal District, North Caucasus Federal District, and Rest of Russia. The report offers market sizes and forecasts for the Russian office furniture market in terms of value (USD) for all the above segments.

By Furniture Type

| Seating |

| Tables |

| Storage |

| Desks |

| Other Furniture Type (Desk Divider, Office Sofas, Bookcases, Benches, Stools etc.) |

By Distribution Channel

| B2B/Directly from Manufacturer | |

| B2C/Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Distribution Channel |

By Geography (Russia)

| Central Federal District |

| Northwestern Federal District |

| Southern Federal District |

| North Caucasus Federal District |

| Rest of Russia |

| By Furniture Type | Seating | |

| Tables | ||

| Storage | ||

| Desks | ||

| Other Furniture Type (Desk Divider, Office Sofas, Bookcases, Benches, Stools etc.) | ||

| By Distribution Channel | B2B/Directly from Manufacturer | |

| B2C/Retail | Home Centers | |

| Specialty Furniture Stores | ||

| Online | ||

| Other Distribution Channel | ||

| By Geography (Russia) | Central Federal District | |

| Northwestern Federal District | ||

| Southern Federal District | ||

| North Caucasus Federal District | ||

| Rest of Russia | ||

Key Questions Answered in the Report

What is the current size and projected growth for the Russia office furniture market by 2031?

The market size is USD 4.15 billion in 2026 and is set to reach USD 4.88 billion by 2031 at a 3.26% CAGR, reflecting steady expansion under localization policies, office commissioning, and online channel gains.

Which product category and channel leads growth within the Russia office furniture market?

Seating led revenue at 39.37% in 2025, while desks are the fastest-growing category at 7.98% CAGR, and B2B held 54.87% value share, with B2C retail forecast to grow at 8.87% CAGR.

How is localization shaping procurement in the Russia office furniture market?

Public-sector and SOE procurement rules prioritize domestic and EAEU-origin goods, which creates steadier tender pipelines for compliant suppliers while raising documentation and testing requirements.

How do high interest rates affect purchasing and projects in the Russia office furniture market?

The 16% key rate increases financing costs for inventory and fit-outs and encourages buyers to extend replacement cycles and shift toward standardized systems with lower upfront spend.

What role do marketplaces play in the Russia office furniture market?

Marketplaces provide configuration, fast fulfillment, and invoicing that open access to regional buyers and SMEs, which expands assortment reach and shortens shipping times.

Which region accounts for the largest share of the Russia office furniture market?

The Central Federal District led with 48.87% in 2025 and is projected to grow at 5.24% through 2031, supported by commissioning activity and tender concentration in the capital.

Page last updated on: