Russia Light Vehicle Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 52.97 Billion |

| Market Size (2026) | USD 55.22 Billion |

| Market Size (2031) | USD 68.04 Billion |

| Growth Rate (2026 - 2031) | 4.25% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Light Vehicle Market Analysis by Mordor Intelligence

The Russia light vehicle market size is expected to grow from USD 52.97 billion in 2025 to USD 55.22 billion in 2026 and is forecast to reach USD 68.04 billion by 2031 at 4.25% CAGR over 2026-2031. In 2025, new passenger-car and light commercial vehicle sales totaled 1,349,230 units (-8.3% YoY), indicating demand normalization after the 2024 rebound amid high rates and cost pressures. Passenger-car demand continues to anchor volumes, yet the strongest momentum comes from light commercial vehicles purchased by e-commerce operators. Fuel-type dynamics show gasoline’s 68.75% grip being slowly eroded by battery-electric options, nurtured by subsidy schemes and pilot cell plants. Regionally, the Far East leverages proximity to Chinese supply chains, becoming the fastest-growing territory even as Moscow keeps the single-largest customer base.

Key Report Takeaways

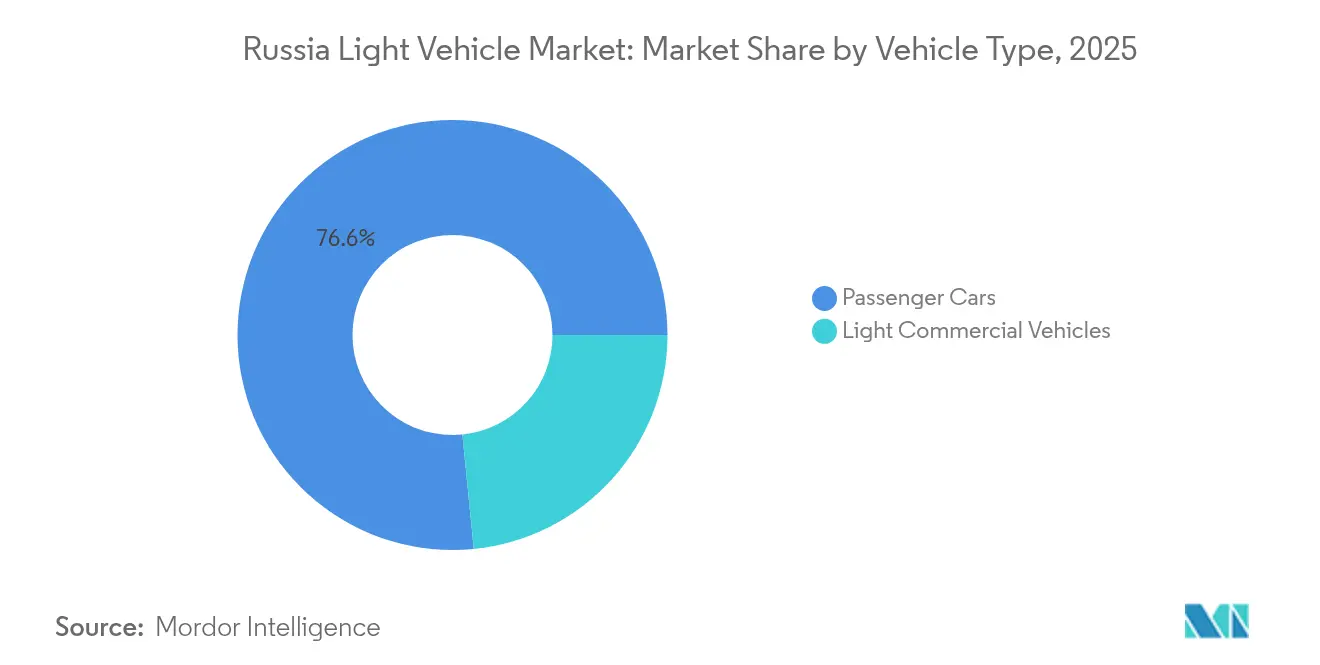

- By vehicle type, passenger cars led with 76.58% revenue share in 2025; light commercial vehicles are forecast to expand at a 4.59% CAGR through 2031.

- By fuel type, gasoline models accounted for 68.10% of the Russia light vehicle market share in 2025, while battery-electric vehicles are set to grow at a 4.97% CAGR to 2031.

- By body type, SUVs and crossovers captured 47.95% of 2025 sales; compact vans are projected to register the fastest 4.41% CAGR between 2026 and 2031.

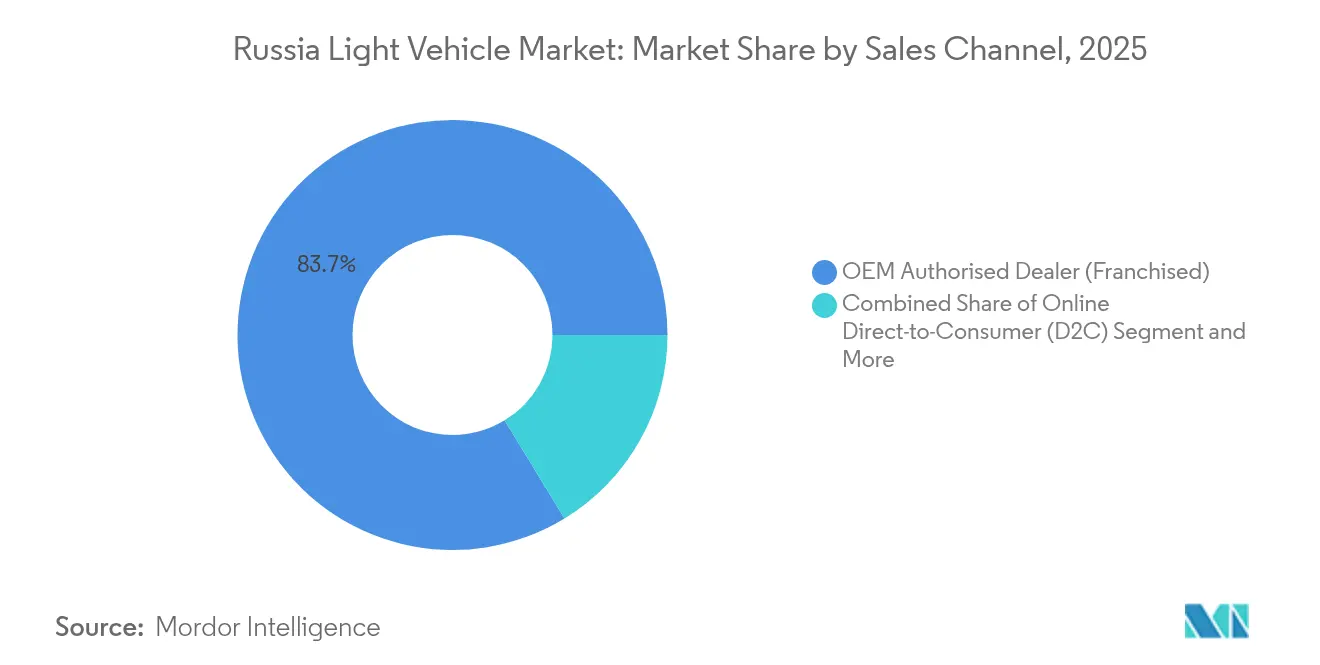

- By sales channel, OEM-authorised dealers controlled 83.72% of transactions in 2025, but online direct-to-consumer channels will rise at a 4.64% CAGR through 2031.

- By region, the Central Federal District commanded 34.12% of 2025 demand, whereas the Far Eastern Federal District is expected to post a 4.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Russia Light Vehicle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chinese OEM influx restoring model availability | +1.8% | National, strongest in Far Eastern FD and border regions | Short term (≤ 2 years) |

| Government subsidies & preferential loans | +1.2% | National, concentrated in Central FD and Volga FD | Medium term (2-4 years) |

| Parallel-import e-commerce platforms lowering vehicle prices | +0.8% | National, strongest impact in border regions | Short term (≤ 2 years) |

| E-commerce boom | +0.7% | Urban centers, Moscow, St. Petersburg, regional capitals | Medium term (2-4 years) |

| Domestic Li-ion cell pilot plants enabling local EV supply chain | +0.4% | National, with production hubs in Central and Ural FD | Long term (≥ 4 years) |

| Adoption of CNG & hybrids | +0.3% | Regions with CNG infrastructure, primarily Central and Volga FD | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chinese OEM Influx Restoring Model Availability

Chinese brands vaulted from below 10% share in early 2022 to more than 60% of 2024 passenger-car sales. Great Wall Motor’s Russia revenue surged 73% to RMB 8.57 billion in 2022, outpacing its consolidated growth[1]“2022 Annual Report,” Great Wall Motor Co., greatwall.com.cn. Assemblers like Haval exploit Eurasian Economic Union tariff rules and vacant Western facilities to widen model menus lost after European withdrawals. Yet dependence cuts both ways; China’s exports to Russia dropped 44% in Q1 2025 as trade-financing risks grew, prompting Moscow to weigh safeguard duties that could slow the influx.

Government Subsidies & Preferential Loans for Domestic Brands

The Ministry of Industry and Trade earmarked RR 15 billion in subsidised-loan quotas through 2026, channelling 20%–35% point-of-sale discounts to about 330,000 units[2]“Subsidised Auto Loan Programme Allocations 2024–2026,” Ministry of Industry and Trade, minprom.gov.ru. The scheme tilts the Russia light vehicle market toward AvtoVAZ, GAZ, and UAZ while allowing locally assembled Chinese models to qualify. Price advantages stimulate near-term volume, yet fiscal ceilings and AvtoVAZ’s forecast for a 25% contraction in 2025 flag durability concerns. The loans have morphed into an industrial-policy lever, nudging buyers toward models hitting localisation thresholds and supporting assembly-plant utilisation in Togliatti and Ulyanovsk.

E-commerce Boom Fuelling Urban LCV Demand

Explosive online-retail growth forces couriers to refresh fleets with nimble vans that slash last-mile costs. The Ford–Sollers joint venture plans electric Transit production in Yelabuga, betting that 4% of LCV parc turns electric by 2025[3]“Transit Production Expansion Announcement,” Ford Sollers JV, ford.ru. Congestion-charging proposals in Moscow and eco-zones in St. Petersburg accelerate demand for smaller, cleaner delivery vehicles. However, roll-out of public fast-chargers lags schedule, and high interest rates crimp small-operator financing, limiting immediate upside.

Adoption of CNG & Hybrids Amid High Pump Prices

Retail gasoline hit levels where compressed-natural-gas payback edges below three years for taxi fleets in Kazan. Hybrid uptake rises in temperate cities yet drops in Yakutsk and Norilsk, where −40 °C winters lift hybrid fuel use by 73%, wiping efficiency gains. Gazprom’s filling-station buildout sustains the CNG option, while recycling fees that punish large engines nudge consumers toward smaller hybrid powertrains. Market segmentation by climate forces OEMs to calibrate powertrain mixes regionally.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Western sanctions | -2.1% | National, most severe in high-tech vehicle segments | Medium term (2-4 years) |

| Volatile ruble & high interest rates | -1.4% | National, concentrated impact in credit-dependent segments | Short term (≤ 2 years) |

| Escalating recycling fees hiking EV ownership cost | -0.8% | National, disproportionate impact on imported EVs | Short term (≤ 2 years) |

| Lack of winter-grade battery thermal control | -0.5% | Siberian FD, Far Eastern FD, northern regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Western Sanctions Disrupting Component Inflows

Tightened export controls on semiconductors, sensors and battery materials force producers to downgrade specs or court pricier Chinese substitutes. AvtoVAZ lifted local-content ratios to 81% but still battles electronics gaps that stall lines several days each quarter. Korea’s March 2024 embargo on lithium-ion batteries hit future EV roll-outs, compelling planners to redesign packs around local chemistries. Sanctions inflate costs, lower quality, and slow technology refresh cycles, clipping the Russia light vehicle market’s value-added trajectory.

Volatile Ruble & High Interest Rates Dampening Demand

The ruble swung between 99 and 110 per USD in 2024, complicating pricing for dealers who reissue invoices weekly. Central-bank policy lifted key rates above 17%, suppressing auto-loan approvals and widening the affordability gap. Used-car credit volumes slid 11% in 2024, constricting trade-in pipelines that new-car dealers rely on for traffic. Cash-rich Chinese OEMs exploit the void by offering direct yuan financing, but most domestic consumers postpone purchases, lengthening ownership cycles and tempering near-term replacement demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Vehicles Drive Electrification

In 2025, passenger cars held a dominant 76.58% share of Russia's light vehicle market. Meanwhile, light commercial vehicles showcased the most rapid growth, boasting a 4.59% CAGR outlook. Fleet buyers in e-commerce hubs run strict total-cost-of-ownership models that reward electric vans once diesel prices and city tolls are factored in. Sollers forecasts electric derivatives will capture 4% of the segment volume by 2025. Additionally, Chinese manufacturers fill showroom gaps left by Western exits, offering 40-plus models that combine premium interiors with attractive warranties.

Light commercial vehicles like refrigerated micro-vans gain traction as grocery chains migrate online. Leasing companies consolidate procurement, negotiating volume rebates that embed Chinese vans into corporate depots. Conversely, taxi agencies cling to inexpensive sedans, extending their lifecycles beyond 10 years due to high borrowing costs. Russia's light vehicle market is recalibrating around functional fleet renewals rather than discretionary household upgrades.

By Fuel Type: Gasoline Dominance Faces Electric Challenge

In 2025, gasoline commanded a robust 68.10% share of Russia's light vehicle market, underscoring the nation's steadfast reliance on traditional powertrains. However, battery-electric vehicles are rising, boasting an impressive projected CAGR of 4.97%. This surge is largely fueled by subsidies that can reduce sticker prices by as much as 35% for eligible buyers. Meanwhile, diesel's prominence is waning, confined mainly to long-haul commercial applications. This decline is largely due to stricter emission norms, which have escalated after-treatment costs. In the Volga region, municipalities are witnessing a surge in CNG fleets, due to Gazprom's expedited establishment of refueling corridors. Hybrid vehicles find their niche, catering to urban commuters who prioritize fuel savings but are cautious about range limitations. While policy initiatives—like heightened recycling fees and suggested privileges for EV lanes—play a pivotal role in shaping future demand, narratives centered on energy security also play a crucial role in influencing consumer behavior, fostering a preference for domestically sourced fuels.

By 2030, the Russia light vehicle market could see a notable surge in electric model sales, contingent on timely battery localization. Meanwhile, gasoline sales are expected to stabilize, bolstered by rural and far-northern regions with sparse charging infrastructure. This duality in powertrains necessitates that suppliers maintain multi-fuel supply chains, adding complexity to inventory management but ensuring a range of consumer choices.

By Body Type: SUV Dominance Reflects Consumer Preferences

In 2025, Sport Utility Vehicles accounted for 47.95% of registrations in Russia's light vehicle market, highlighting a clear preference among buyers of elevated seating and winter-ready vehicles. Chinese brands are tapping into this trend, offering feature-rich C-segment crossovers at prices 15% lower than their European counterparts. As younger households lean towards cargo flexibility over traditional styling, the share of sedans continues to dwindle. Compact vans are rising, boasting a forecasted CAGR of 4.41%, driven by demand from parcel delivery and on-demand grocery services. While pickup trucks occupy a niche, they are gaining traction as a status symbol among urban contractors, suggesting potential growth beyond their traditional utility.

The Russia light vehicle market responds to infrastructure realities: rough regional roads make ground clearance and all-wheel drive practical necessities, explaining crossover popularity. Aftermarket accessory suppliers flourish, offering roof boxes and winter tyre packages that raise transaction values. Styling convergence blurs lines between MPVs and SUVs, enabling OEMs to platform-share and cut development cycles. Body-type diversification reduces vulnerability to single-segment downturns, yet it presses suppliers to manage more SKUs amid ongoing logistics constraints.

By Sales Channel: Digital Disruption Challenges Traditional Distribution

In the Russia Light Vehicle Market, OEM-authorised dealers accounted for 83.72% of 2025's volumes. However, online direct sales are rising at a 4.64% CAGR. This trend particularly appeals to tech-savvy urbanites prioritizing transparent pricing and doorstep delivery. The pandemic hastened the acceptance of virtual showrooms among consumers. Meanwhile, sanctions led to inventory shortages, a gap that online brokers adeptly filled through real-time cross-border sourcing. Even when official allocations waver, grey-market parallel-import intermediaries capitalize on arbitrage opportunities, ensuring the Russia light vehicle market remains buoyant.

Dealer groups adapt by live-streaming walkarounds and offering 24-hour remote-test-drive kits, yet commissions compress as OEMs pilot agent models. Leasing houses face margin pressure from interest-rate spikes but explore subscription services that bundle insurance and tyre storage. Regulatory clarity on digital paperwork, expected in 2026, could unlock faster uptake, while cybersecurity mandates may raise compliance burdens on small web-based resellers.

By Regional Distribution: Central Dominance Faces Eastern Challenge

In 2025, the Central Federal District, centered in Moscow, accounted for 34.12% of the demand, buoyed by rising disposable incomes and a dense network of dealers. Meanwhile, the Far Eastern Federal District, driven by port logistics in Vladivostok and direct rail connections to Northeastern China, is witnessing the fastest growth at a 4.92% CAGR through 2031. Additionally, the waiving of import tariffs for local residents on right-hand-drive conversions bolsters parallel imports, intensifying competition in Russia's light vehicle market.

Volga and Southern districts present balanced profiles, mixing manufacturing bases with agricultural economies that buoy pickup and van sales. Siberia lags on EV uptake because sub-zero climates amplify range anxiety, though mineral-sector payrolls support steady diesel SUV turnover. Regional policy incentives, such as Far East mortgage subsidies that free discretionary income, indirectly boost car ownership. Over time, transport-infrastructure projects like the Amur highway widen dealer catchments, distributing demand beyond legacy urban cores.

Geography Analysis

The Central Federal District retains its 34.12% share through a dense matrix of dealers, service centers and credit institutions that streamline ownership. Luxury marques used to dominate Moscow boulevards, but sanctions and ruble volatility diverted affluent buyers toward mid-range Chinese crossovers offering smartphone-like infotainment features at lower price points. Government procurement propped up volumes with a 36% hike to RR 27.8 billion in 2024, although such stimulus is finite and may taper once electoral cycles pass. Currency swings also reshaped purchasing behaviour, prompting households to negotiate price locks in USD equivalents to hedge ruble risk, complicating dealer finance books.

The Far Eastern Federal District’s 4.92% CAGR projection reflects structural integration with Guangdong and Heilongjiang supply chains. Proximity allows monthly containerized arrivals of knock-down kits, cutting lead times by half relative to Baltic ports. Cross-border fintech platforms settle transactions in yuan, bypassing SWIFT restrictions. Younger demographics in Khabarovsk and Primorye show brand agnosticism, leaning on peer reviews rather than legacy reputations, which benefits agile Chinese entrants. Regional authorities invest in EV-charging corridors along the Trans-Siberian Highway, aiming to support tourist flows and freight electrification.

Siberian and Ural districts marry resource-sector prosperity with climatic adversity. Fleet managers demand block-heaters, battery warmers and reinforced suspension for permafrost roads, leading to higher average transaction prices. Electric adoption slows because energy-density penalties at −35 °C shave usable range by more than half, steering the Russia light vehicle market back toward gasoline and diesel in cold belts. Yet mining-company ESG commitments could trigger pilot procurement of ruggedised electric pickups by 2027, seeding gradual change. Consumer credit in these areas remains scarce, with purchases skewed toward cash and employer-backed loans that dampen cyclical volatility.

Competitive Landscape

In the post-sanctions landscape, a Sino-Russian duopoly emerges. In 2024, AvtoVAZ secured over 40% of the market share, bolstered by tariffs and patriotic messaging. However, Chinese players, spearheaded by Great Wall, Geely, and Chery, are increasingly challenging AvtoVAZ's dominance. Chery, for instance, is redefining market standards by offering ADAS suites, previously exclusive to premium German brands. In response, AvtoVAZ unveils a USD 3 billion capex initiative, modernising its Togliatti lines for modular platforms linked to its upcoming Lada. This ambitious programme aims for 90% localisation by 2028, designed to shield costs from currency fluctuations.

Technology emerges as a terrain of differentiation. Great Wall’s Lemmon architecture supports over-the-air updates and 800-volt charging, features that Russian rivals currently lack. Chinese OEMs leverage scale economies to undercut on price while achieving double-digit operating margins in Russia. Domestic incumbents explore alliances with Persian and Indian suppliers to source electronics free of Western IP blocks, though vetting takes time. Meanwhile, aftermarket players capitalise on parts shortages by importing refurbished European components, maintaining older fleets, and dampening new-car substitution.

Strategic moves pepper the landscape. In 2024 Haval doubled Tula-plant capacity to 150,000 units. That same year AvtoVAZ signed an MoU with Moscow city to pilot battery swapping for taxis. Great Wall inked a memorandum with Russian Railways to streamline inbound logistics, shaving transit cost by 12%. Each initiative underscores how supply-chain leverage now rivals brand cachet as the main competitive weapon within the Russia light vehicle market.

Russia Light Vehicle Industry Leaders

AvtoVAZ (Lada)

Haval (Great Wall)

Chery

Geely

GAZ Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Russia unveiled a plan targeting 60,000 tons of lithium-carbonate output by 2030 to backstop domestic battery plants.

- December 2024: Over three years, the government launched a USD 1.15 billion national vehicle-platform programme to develop modular chassis for multiple segments.

Russia Light Vehicle Market Report Scope

The Russia Light vehicle Market report covers the current and upcoming trends with recent technological developments in various market areas by vehicle, fuel and material type . The country-level analysis and market share of significant light vehicle manufacturing companies across Russia will be provided.

| Passenger Cars |

| Light Commercial Vehicles |

| Gasoline |

| Diesel |

| Hybrid |

| Plug-in Hybrid (PHEV) |

| Battery Electric (BEV) |

| Others |

| Sedan |

| Hatchback |

| SUV / Crossover |

| MPV / Minivan |

| Pickup (Double-Cab) |

| Pickup (Single-Cab) |

| Panel Van |

| OEM Authorised Dealer (Franchised) |

| Parallel-Import Independent Dealer |

| Online Direct-to-Consumer (D2C) |

| Fleet & Corporate Leasing |

| Car Subscription / Short-Term Lease |

| Rental & Car-Sharing Purchases |

| Central FD (incl. Moscow Region) |

| Northwestern FD (incl. St Petersburg) |

| Far Eastern FD (incl. Primorsky Krai) |

| Rest of Russia |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| By Fuel Type | Gasoline |

| Diesel | |

| Hybrid | |

| Plug-in Hybrid (PHEV) | |

| Battery Electric (BEV) | |

| Others | |

| By Body Type | Sedan |

| Hatchback | |

| SUV / Crossover | |

| MPV / Minivan | |

| Pickup (Double-Cab) | |

| Pickup (Single-Cab) | |

| Panel Van | |

| By Sales Channel | OEM Authorised Dealer (Franchised) |

| Parallel-Import Independent Dealer | |

| Online Direct-to-Consumer (D2C) | |

| Fleet & Corporate Leasing | |

| Car Subscription / Short-Term Lease | |

| Rental & Car-Sharing Purchases | |

| By Regional Distribution | Central FD (incl. Moscow Region) |

| Northwestern FD (incl. St Petersburg) | |

| Far Eastern FD (incl. Primorsky Krai) | |

| Rest of Russia |

Key Questions Answered in the Report

What is the current size of the Russia light vehicle market?

The Russia light vehicle market is valued at USD 55.22 billion in 2026 with a projected CAGR of 4.25% through 2031.

Which segment grows fastest within the Russia light vehicle market?

Light commercial vehicles post the quickest pace, forecast to advance at a 4.59% CAGR as e-commerce fleets expand.

How dominant are Chinese brands in Russia’s passenger-car space?

Chinese OEMs holds significant share of passenger-car sales in 2024, a leap from under 10% just two years earlier.

What fuel type is gaining momentum despite cold-weather hurdles?

Battery-electric vehicles show the strongest 4.97% CAGR outlook, supported by subsidies and emerging cell plants even though winter efficiency drops.

Which region is expected to lead Russia light vehicle market growth?

The Far Eastern Federal District should register the fastest 4.92% CAGR to 2031 due to seamless links with Chinese supply chains.

How are Western sanctions affecting local manufacturers?

Sanctions squeeze semiconductor and battery imports, forcing higher-cost sourcing and production pauses, which trim overall market growth by an estimated 2.1% on the forecast CAGR.

Page last updated on: