Rubber Bonded Abrasive Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.33 Billion |

| Market Size (2031) | USD 1.54 Billion |

| Growth Rate (2026 - 2031) | 3.05% CAGR |

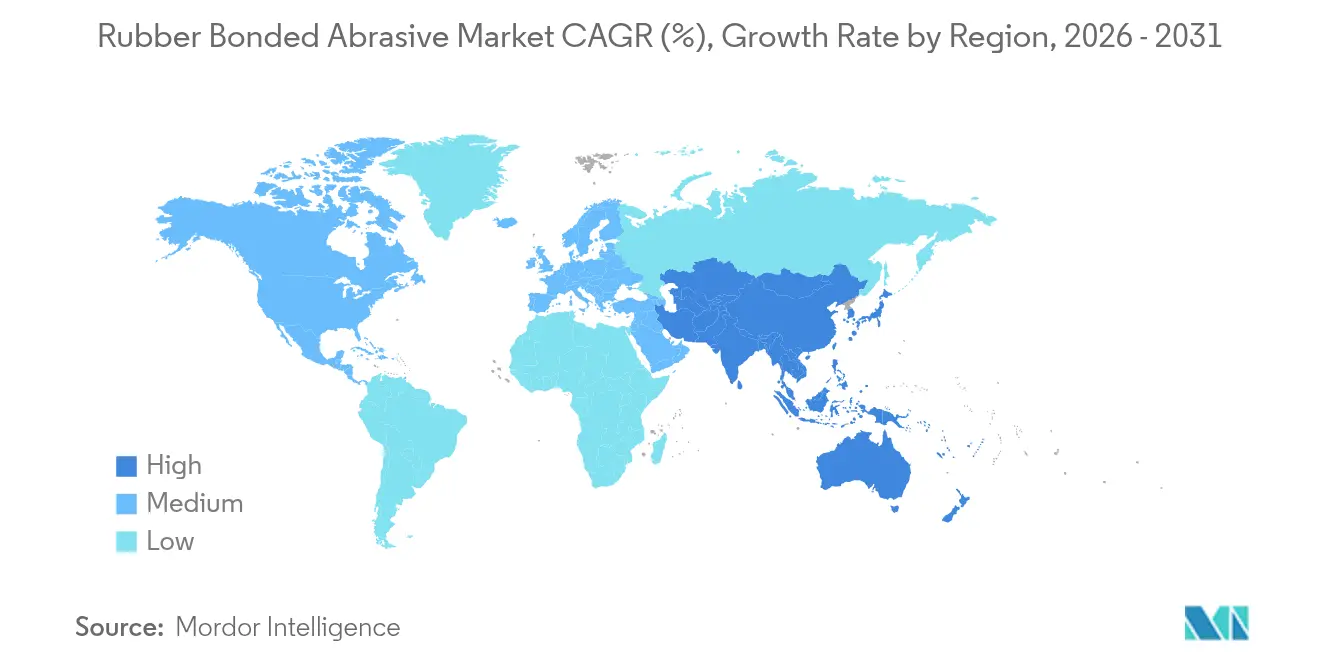

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

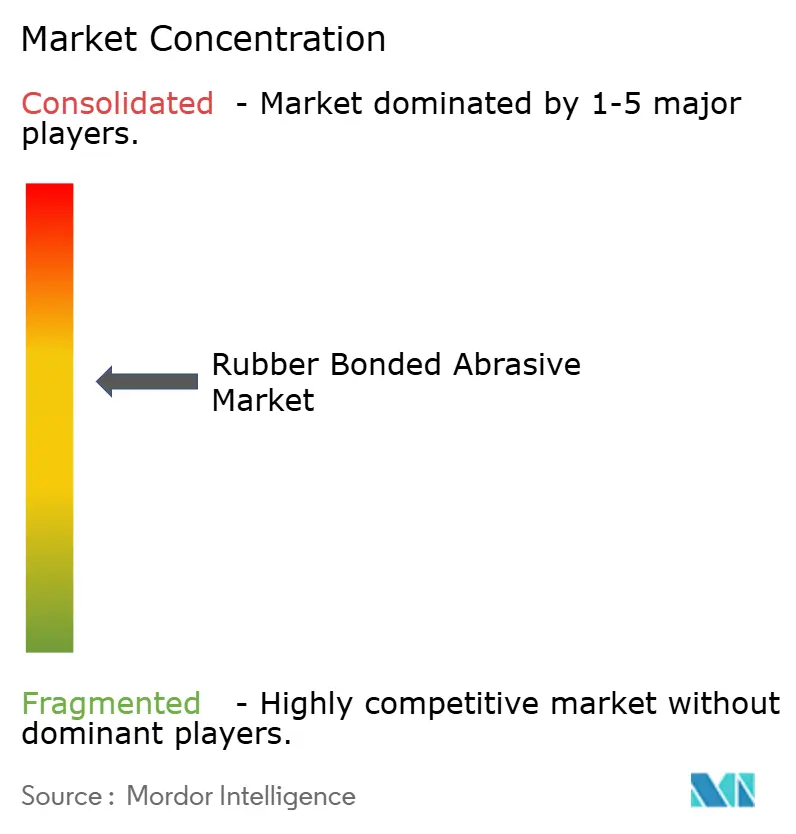

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rubber Bonded Abrasive Market Analysis by Mordor Intelligence

The Rubber Bonded Abrasive market size is expected to grow from USD 1.29 Billion in 2025 to USD 1.33 Billion in 2026 and is forecast to reach USD 1.54 Billion by 2031 at 3.05% CAGR over 2026-2031. The measured expansion signals a shift from volume-led demand toward value-added, high-precision applications as manufacturers prioritize vibration control and surface integrity. Wheels remain the workhorse in heavy-duty grinding, while points and sticks are gaining share in electronics and medical finishing lines. Specialty rubber grades featuring low-volatile organic compound (VOC) chemistries are scaling up in response to tightening environmental regulations. Asia-Pacific retains its dual position as the largest consumer and the fastest-growing region, supported by sustained industrialization and the dispersion of precision manufacturing capabilities. Competitive dynamics point to moderate consolidation, yet regional players find room to expand by offering supply-chain resilience and tailored formulations.

Key Report Takeaways

- By product type, wheels led with 47.72% of the Rubber Bonded Abrasive market share in 2025, while points and sticks recorded the highest projected CAGR at 3.92% to 2031.

- By rubber type, natural rubber commanded a 44.10% share, whereas other specialty rubbers are expected to expand at a 4.01% CAGR through 2031.

- By application, the powertrain segment accounted for 28.35% share of the Rubber Bonded Abrasive market size in 2025; other applications are forecast to grow at 4.22% CAGR between 2026-2031.

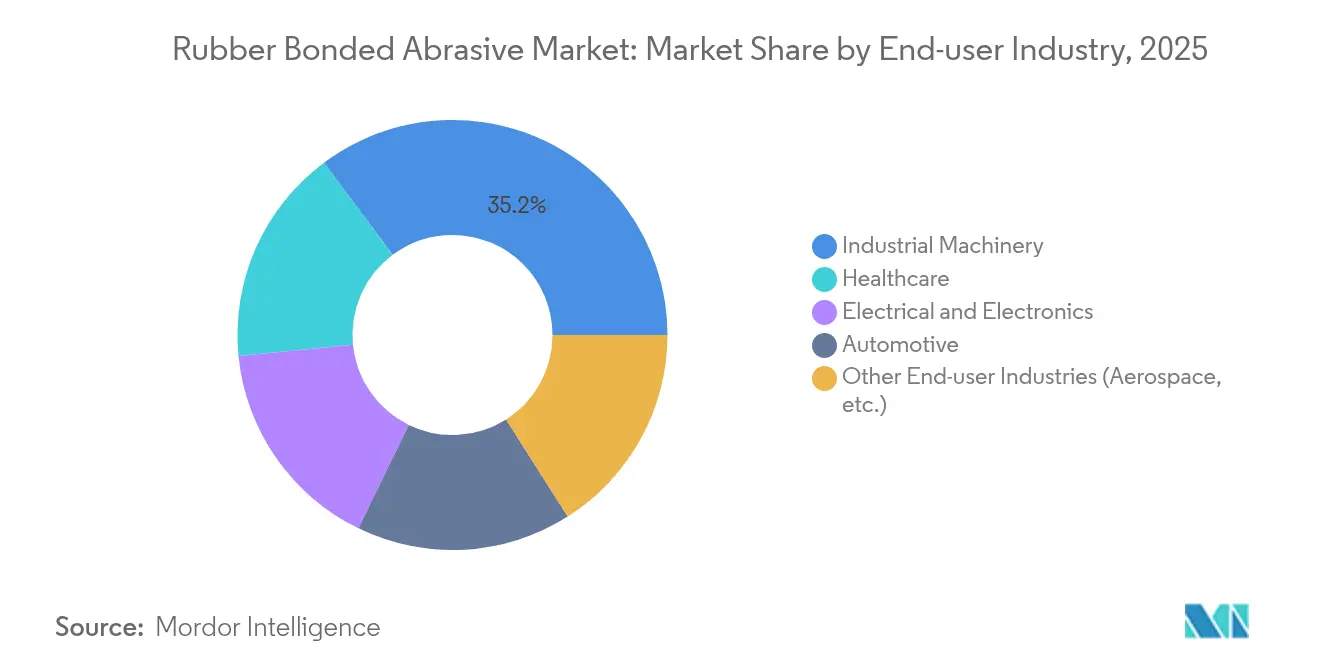

- By end-user, industrial machinery dominated with a 35.20% share in 2025, while healthcare is advancing at a 4.11% CAGR to 2031.

- By geography, Asia-Pacific captured 39.25% of the global Rubber Bonded Abrasive market share in 2025 and is projected to rise at a 4.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Rubber Bonded Abrasive Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Metal and Steel Fabrication | +0.8% | Global, concentrated in Asia-Pacific and North America | Medium term (2-4 years) |

| Expanding Automotive OEM Production Capacities | +0.6% | Global, led by Asia-Pacific | Medium term (2-4 years) |

| Process-automation and CNC Integration Boosting Productivity | +0.5% | North America & Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Rapid Uptake in 3D-printed Metal Finishing | +0.4% | North America & Europe, early adoption in Asia-Pacific | Short term (≤ 2 years) |

| Increase in Electronics and Semiconductors Manufacturing | +0.3% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Metal and Steel Fabrication

Steel capacity additions for infrastructure and shipbuilding amplify the need for compliant grinding tools to prevent thermal distortion. Rubber bonded wheels withstand the high pressures of plate grinding, where vitrified alternatives can fracture. Synthetic-enhanced compounds now extend wheel life, balancing productivity with cost control. Localization of fabrication in North America and Europe opens new demand pockets as buyers seek alternatives to imported grains. Automated grinding lines favor rubber bonded designs because their predictable wear supports longer unattended runs [1]U.S. International Trade Commission, “Abrasive Products: Global Supply Chain Review,” usitc.gov.

Expanding Automotive OEM Production Capacities

Global automakers are enlarging facilities to serve electric vehicle programs that call for precise finishing of powertrain and battery housings. Fine-grit rubber bonded wheels deliver mirror finishes without subsurface damage on steel and aluminum components. Investment announcements in Europe and the United States point to long-term grinding infrastructure upgrades. The segment’s tilt toward lightweight materials enhances rubber bonded traction because the same wheel can shift from steel to composites with minor parameter changes.

Process-automation and CNC Integration Boosting Productivity

Computerized Numerical Control (CNC) grinders equipped with in-process conditioning rely on wheels that wear predictably across long unattended cycles. Rubber bonded abrasives meet this need and are now being paired with sensors that feed performance data into factory analytics platforms. As Industry 4.0 spreads, smart wheels enable predictive maintenance scheduling that reduces downtime. The synergy between consistent wheel behavior and AI-driven optimization is cementing rubber bonded adoption in advanced machining centers.

Rapid Uptake in 3D-Printed Metal Finishing

Additive manufacturing of aerospace and medical parts is creating complex geometries that conventional wheels cannot reach. Rubber bonded points and sticks adapt to internal channels without damaging delicate lattice structures. New magnetic abrasive finishing systems incorporate rubber bonded media to achieve low-Ra surfaces on titanium and Inconel. As automated post-processing cells scale, demand for specialized rubber bonded formulations tailored to 3D-printed alloys is set to climb.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental Regulations on Rubber and VOC Emissions | -0.4% | Global, with strictest enforcement in North America and Europe | Short term (≤ 2 years) |

| Raw-material Price Volatility | -0.3% | Global, with highest impact in Asia-Pacific | Medium term (2-4 years) |

| Shift Toward Super-abrasives in Precision Grinding | -0.2% | North America & EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Environmental Regulations on Rubber and VOC Emissions

Proposed United States Maximum Achievable Control Technology (MACT) standards and tighter European Registration, Evaluation, Authorization and Restriction of Chemicals (REACH) rules are elevating compliance costs for rubber compounders. Manufacturers are reformulating with low-VOC curatives and investing in thermal oxidizers to capture hazardous air pollutants. Small producers may struggle with the capital burden, accelerating consolidation. R&D pipelines now prioritize bio-based alternatives that maintain elasticity while reducing emissions, positioning early adopters for future growth [2]Environmental Protection Agency, “National Emission Standards for Hazardous Air Pollutants: Rubber Processing Amendments,” epa.gov.

Raw-material Price Volatility

Natural rubber prices fluctuate sharply due to weather, disease, and currency swings in Thailand, Indonesia, and Malaysia. Synthetic substitutes mirror oil price movements, limiting hedging strategies. Supply shocks of 20-30% within a quarter compress margins and complicate contract pricing. Pilot programs to cultivate domestic rubber crops in the United States remain nascent and cannot yet offset global supply risk, keeping input costs unpredictable for the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Wheels Dominate While Points Accelerate

Wheels represented 47.72% of the Rubber Bonded Abrasive market size in 2025, reflecting their indispensability in high-volume heavy-duty grinding. Their broad contact surface supports rapid stock removal on crankshafts and steel plates. Points and sticks, although smaller in volume, are climbing at 3.92% CAGR as electronics and medical plants require pinpoint accuracy for finishing delicate parts. Blocks and segments serve niche applications such as turbine blade root grinding where geometry flexibility is paramount.

CNC adoption is reinforcing demand for shape-stable points that uphold tolerances across extended cycles. Hybrid wheel designs that integrate segment adaptability within a wheel body are emerging, offering shops the productivity of wheels and the finesse of points without tool changeovers.

By Rubber Type: Natural Leads but Specialty Compounds Gain

Natural rubber held 44.10% of the Global Rubber Bonded Abrasive market share in 2025 owing to its elasticity and vibration damping during heavy grinding. Specialty rubbers, such as silicone, nitrile butadiene rubber (NBR), and neoprene are projected to log 4.01% CAGR, driven by elevated temperature resistance and chemical stability. NBR excels where oil resistance is vital, particularly in powertrain grinding lines, while neoprene finds use in marine environments.

Sustainability pressures are steering research and development (R&D) toward bio-based synthetics that parallel natural rubber performance but mitigate supply risk. Nanotube-enhanced rubber composites promise greater thermal conductivity, enabling higher peripheral speeds without wheel degradation.

By Application: Powertrain Core but Diversification Evident

Powertrain dominated with 28.35% share of Rubber Bonded Abrasive market size in 2025 as crankshaft and camshaft grinding rely on compliant wheels to avoid residual stress. Other applications, mainly cutting and forming tools, are expanding at 4.22% CAGR on the back of 3D printing post-processing needs. Gears and bearings remain stable, with noise-reduction targets driving finer grit usage. Turbine components command premium pricing due to stringent finishing tolerances.

Electrification is redefining powertrain grinding, shifting focus to lightweight aluminum housings and composite motor laminations. Rubber bonded wheels versatile enough to migrate between steel and non-ferrous substrates without changeover, are becoming OEM standards.

Geography Analysis

Asia-Pacific accounted for 39.25% of the Global Rubber Bonded Abrasive market share in 2025 and is on course for 4.02% CAGR to 2031. China’s vast automotive, electronics, and machinery sectors anchor demand, while national programs encouraging high-quality manufacturing are elevating precision grinding standards. Japan’s advanced electronics industry requires high-purity wheels, and South Korea’s semiconductor surge is lifting ultra-precision point consumption.

North America is witnessing a rebound as reshoring and defense investments spur the adoption of specialty wheels capable of processing advanced alloys. The United States is particularly active in integrating smart grinding solutions that tie rubber bonded wheel performance data into plant-wide digital twins. Europe shows steady demand but stands out for its leadership in low-VOC formulations to comply with stringent environmental frameworks.

South America and the Middle East and Africa trail in volume yet present upside potential. Brazil’s automotive rebuild and Gulf infrastructure megaprojects are spurring procurement of heavy-duty wheels. Technology transfer from global suppliers, coupled with foreign direct investment, is laying the foundation for local finishing capacity, positioning these regions for incremental uptake of rubber bonded products.

Competitive Landscape

The Rubber Bonded Abrasive market is moderately consolidated with the presence of major players including Saint-Gobain, 3M, Tyrolit – Schleifmittelwerke Swarovski AG & Co KG, CUMI., and PFERD INC. Saint-Gobain, 3M, and CUMI leverage wide portfolios, proprietary compounds, and global logistics to defend share. R&D spending focuses on low-emission binders and wheels compatible with automated dresser systems. Partnerships between wheel suppliers and grinding-machine builders are emerging to offer turnkey performance guarantees. Regional producers capitalize on supply-chain disruptions by offering faster lead times and localized technical support. In North America and Europe, customers favor vendors that can assure raw material transparency and regulatory compliance.

Rubber Bonded Abrasive Industry Leaders

3M

PFERD INC.

CUMI.

Tyrolit – Schleifmittelwerke Swarovski AG & Co KG

Saint-Gobain

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: The European Union passed the new REACH regulation, which set stricter safety and environmental standards for rubber-bonded abrasives and other industrial products. This can create new challenges for the rubber-bonded abrasives market.

- May 2023: Sak Abrasives Inc., a wholly owned subsidiary of Sak Industries Private Ltd., announced its acquisition of Jowitt & Rodgers Co., which custom designs different bonded abrasives to meet the industry’s needs.

Global Rubber Bonded Abrasive Market Report Scope

The Rubber Bonded Abrasive market report includes:

| Wheels |

| Points and Sticks |

| Blocks and Segments |

| Others |

| Natural Rubber |

| Nitrile (NBR) |

| Neoprene |

| Other Rubber Types (Silicone, etc.) |

| Powertrain |

| Gears |

| Bearings |

| Turbines |

| Other Applications (Cutting and Forming Tools, etc.) |

| Industrial Machinery |

| Automotive |

| Electrical and Electronics |

| Healthcare |

| Other End-user Industries (Aerospace, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Wheels | |

| Points and Sticks | ||

| Blocks and Segments | ||

| Others | ||

| By Rubber Type | Natural Rubber | |

| Nitrile (NBR) | ||

| Neoprene | ||

| Other Rubber Types (Silicone, etc.) | ||

| By Application | Powertrain | |

| Gears | ||

| Bearings | ||

| Turbines | ||

| Other Applications (Cutting and Forming Tools, etc.) | ||

| By End-user Industry | Industrial Machinery | |

| Automotive | ||

| Electrical and Electronics | ||

| Healthcare | ||

| Other End-user Industries (Aerospace, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the anticipated Global Rubber Bonded Abrasive market size in 2026?

The Rubber Bonded Abrasive market size is expected to reach USD 1.33 Billion in 2026.

Which region leads the Rubber Bonded Abrasive market and how fast is it growing?

Asia-Pacific leads with 39.25% share and is projected to post a 4.02% CAGR through 2031.

What product segment is expanding the quickest?

Points and sticks are rising at a 3.92% CAGR as precision finishing demand grows.

How are environmental regulations influencing product development?

Manufacturers are investing in low-VOC rubber formulations and emission-control systems to comply with stricter EPA and REACH standards.

Which end-user industry is growing fastest?

Healthcare is advancing at a 4.11% CAGR due to demand for precision-ground medical devices.

Page last updated on: