Public Safety Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

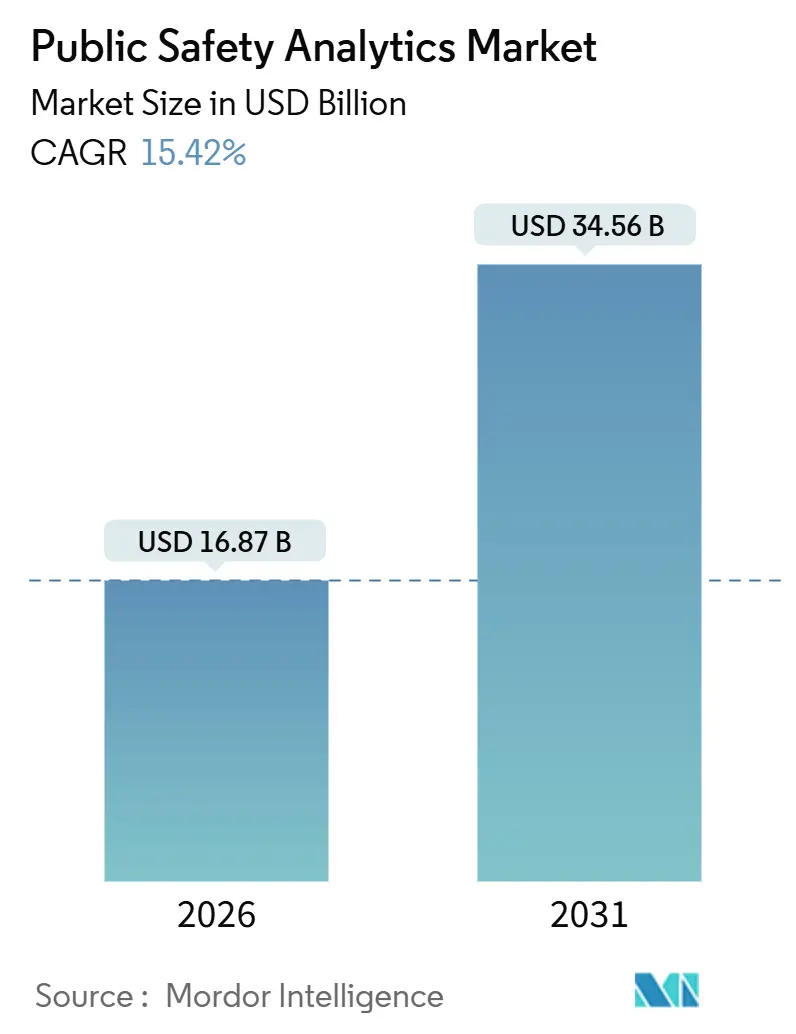

| Market Size (2026) | USD 16.87 Billion |

| Market Size (2031) | USD 34.56 Billion |

| Growth Rate (2026 - 2031) | 15.42% CAGR |

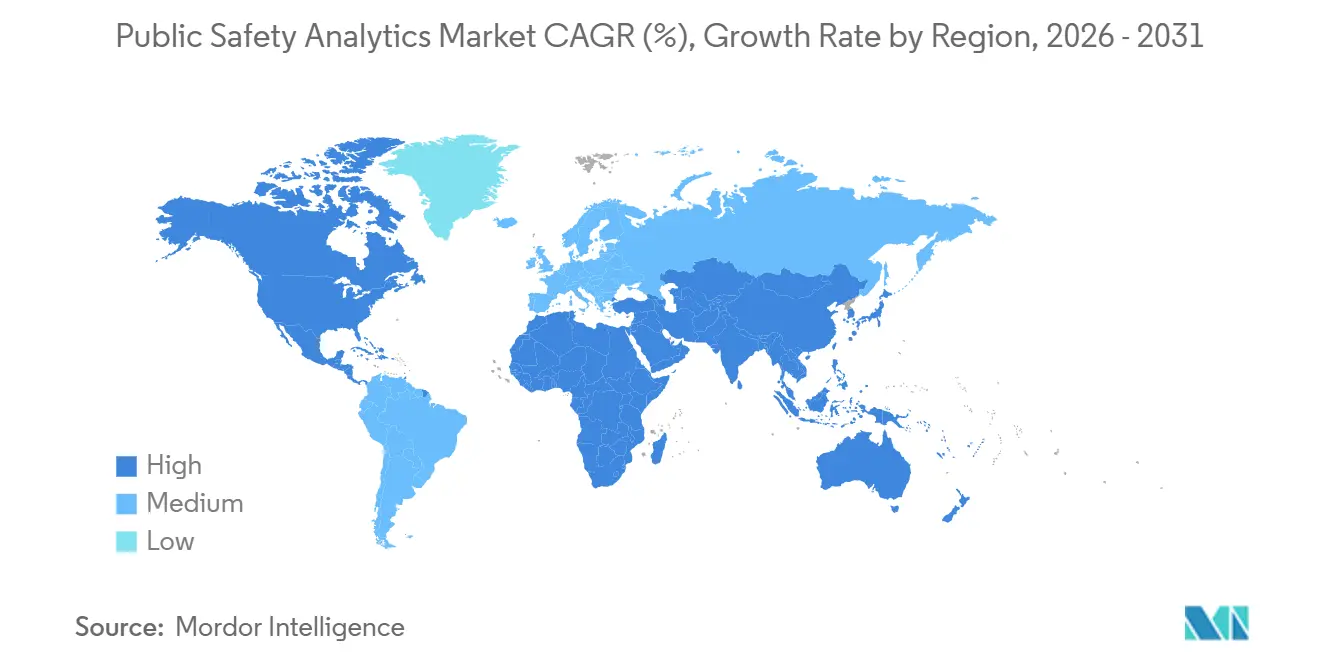

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

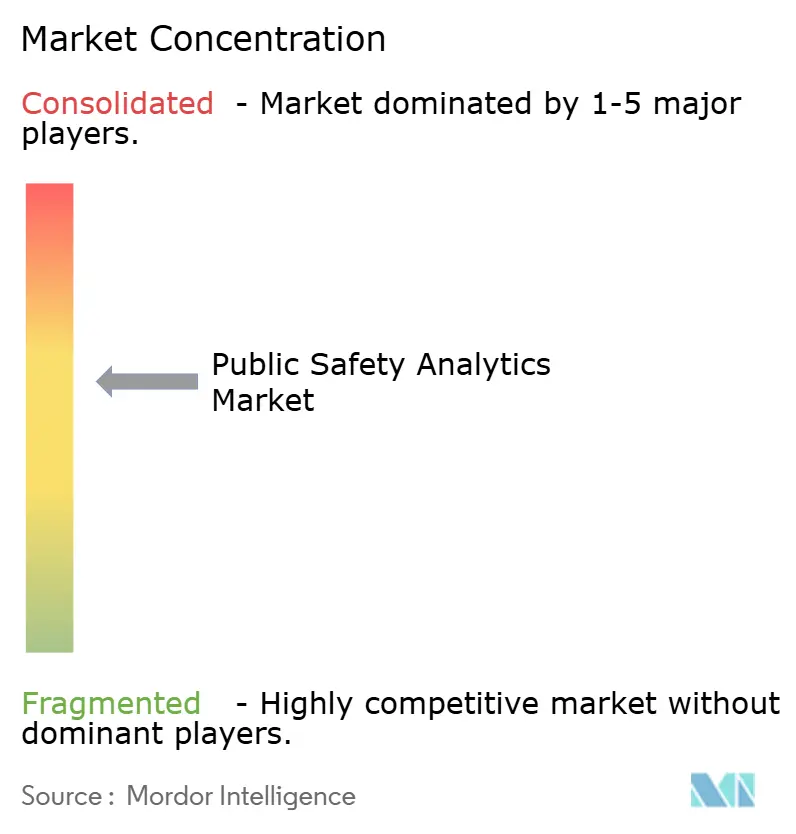

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Public Safety Analytics Market Analysis by Mordor Intelligence

The public safety analytics market size stood at USD 16.87 billion in 2026 and is projected to reach USD 34.56 billion by 2031, reflecting a 15.42% CAGR over the forecast period. The growth trajectory stems from federally mandated Next Generation 9-1-1 upgrades, algorithmic-transparency rules under the EU AI Act, and 5G-enabled edge nodes that stream real-time video from first responders. Vendors able to demonstrate audited datasets and bias-mitigation protocols now enjoy preferred-bidder status in European tenders. In the United States, federal opioid-crisis grants and FirstNet’s 5G core upgrades sustain high software and services demand, while Asia-Pacific city-digitization programs widen the global addressable base for end-to-end command-center platforms. Competitive intensity remains moderate as cloud-native specialists attack discrete use cases that legacy record-management incumbents have been slow to modernize.

Key Report Takeaways

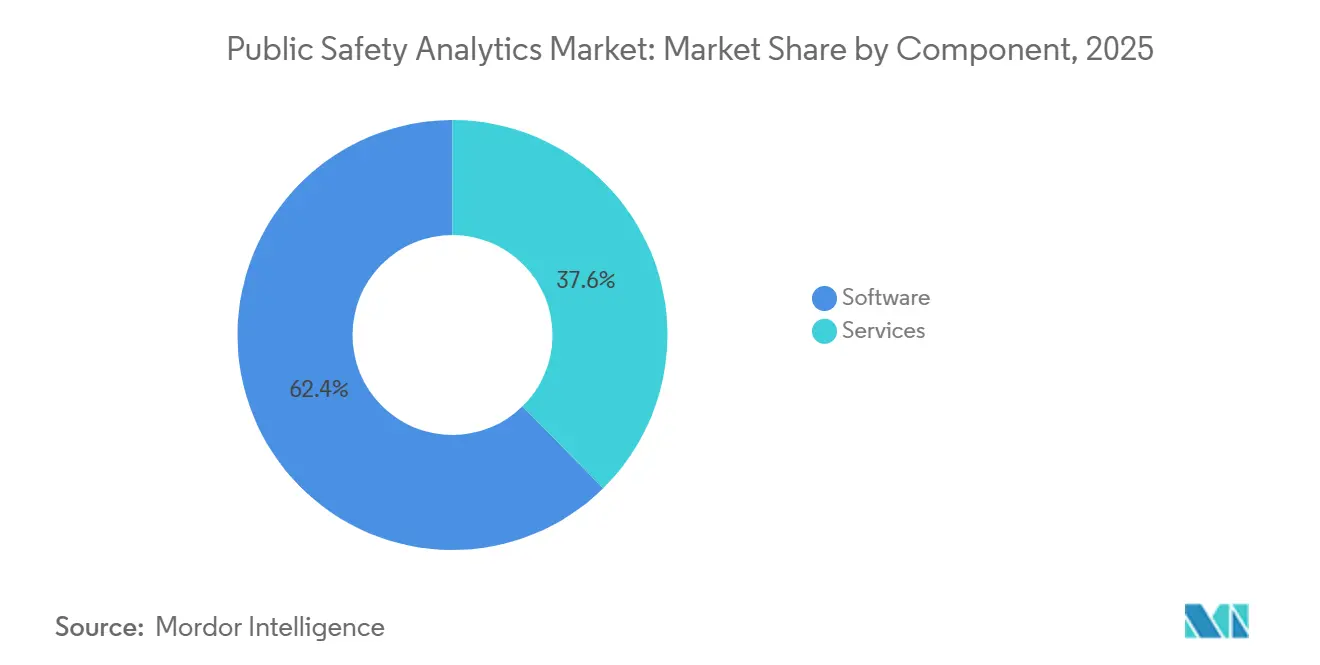

- By component, software led with 62.36% of the public safety analytics market share in 2025 while services are forecast to expand at a 17.02% CAGR through 2031.

- By analytics type, predictive analytics captured 38.63% revenue in 2025 whereas prescriptive analytics is advancing at a 16.43% CAGR to 2031.

- By deployment model, on-premises platforms accounted for 57.74% spending in 2025, yet cloud and Software-as-a-Service offerings are progressing at a 16.65% CAGR.

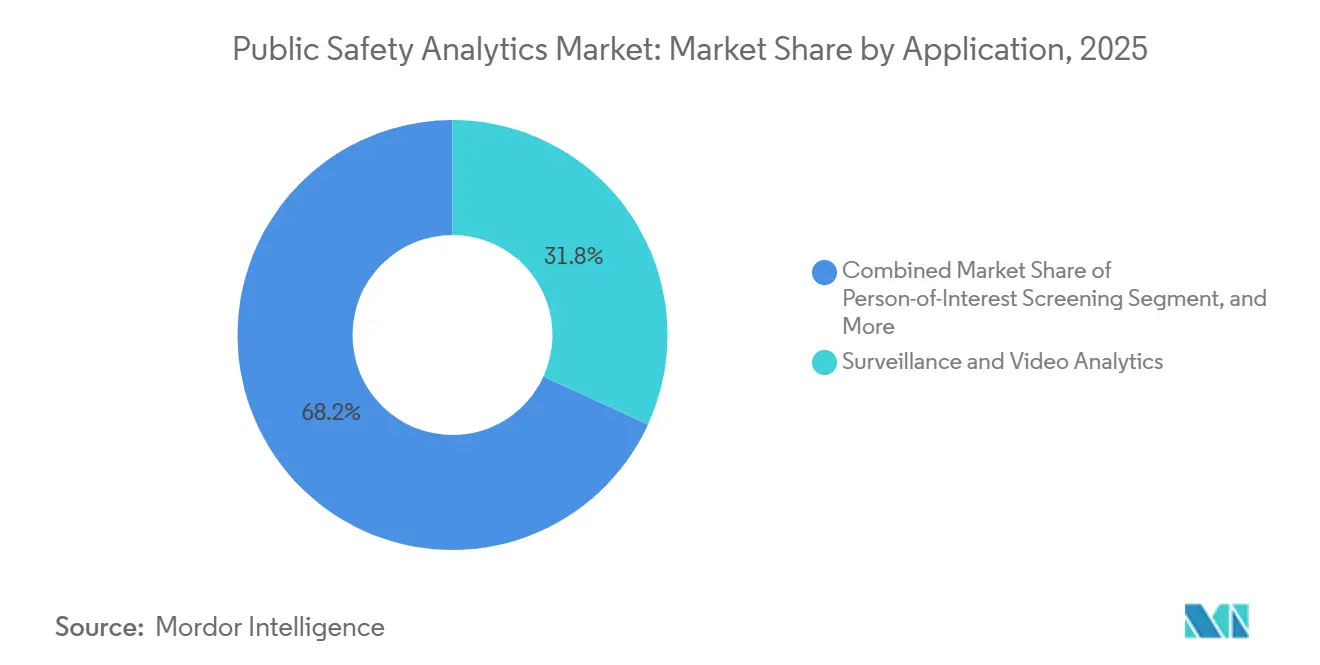

- By application, surveillance and video analytics commanded 31.83% revenue in 2025, while resource-allocation optimization is the fastest-expanding use case at 16.32% CAGR.

- By end-user, law enforcement held 32.84% spending in 2025 and transportation and critical infrastructure segments are growing at a 16.37% CAGR.

- By geography, North America contributed 38.74% revenue in 2025 whereas Asia-Pacific is registering the quickest regional CAGR at 16.54%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Public Safety Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandated NG 9-1-1 Data-Integration Rollouts | +3.8% | North America, with spillover to EU and Asia-Pacific adopting similar standards | Medium term (2-4 years) |

| EU AI Act Requirements for Algorithmic Transparency | +2.9% | Europe core, influencing global vendors serving EU jurisdictions | Short term (≤ 2 years) |

| Accelerating 5G Edge Deployments for First-Responder Video Streams | +3.2% | North America and Asia-Pacific core, early gains in urban metros | Medium term (2-4 years) |

| Rapid Urbanisation Spurring Smart-City Safety Platforms | +2.6% | Asia-Pacific and Middle East, with selective deployments in South America | Long term (≥ 4 years) |

| Federal Opioid-Crisis Funds Requiring Analytics-Led Prevention | +1.7% | North America, concentrated in states with high overdose rates | Short term (≤ 2 years) |

| Satellite EO and GNSS Data Becoming Budget-Line Items for Disaster Readiness | +1.2% | Global, with priority in disaster-prone regions (Asia-Pacific, South America, Africa) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandated NG 9-1-1 Data-Integration Rollouts

The U.S. Federal Communications Commission’s November 2024 order obliges public safety answering points to ingest text, images, and video within 6–12 months of a formal request, pushing many counties to overhaul legacy dispatch platforms.[1]Federal Communications Commission, “FCC Finalizes Next Generation 9-1-1 Location Accuracy Rules,” fcc.gov Multimedia calls demand geospatial precision within 50 meters, a leap from cell-tower triangulation averages of 300 meters, and agencies that miss the deadline face civil-liability exposure demonstrated by recent litigation. Consortia purchasing models have emerged to help rural counties pool upgrade budgets, accelerating opportunities for cloud-native vendors.

EU AI Act Requirements for Algorithmic Transparency

The AI Act classifies law-enforcement analytics as high-risk and mandates audited datasets, bias-testing logs, and human-oversight controls by August 2026.[2]European Commission, “The EU AI Act: High-Risk AI Systems and Compliance Requirements,” digital-strategy.ec.europa.eu Proprietary black-box models now give way to dashboards that surface SHAP values and counterfactual explanations to meet evidentiary standards. Compliance costs favor enterprises with in-house legal teams, prompting smaller firms to partner or exit European procurements. The Act’s extraterritorial reach effectively globalizes transparency norms, influencing product roadmaps in North America and Asia-Pacific.

Accelerating 5G Edge Deployments for First-Responder Video Streams

FirstNet completed a USD 6.3 billion 5G standalone core upgrade in 2024, enabling sub-20-millisecond latency for body-camera and drone feeds in more than 50 U.S. metros.[3]FirstNet Authority, “FirstNet 5G Core Infrastructure and Edge Computing Deployment,” firstnet.gov Edge nodes process video locally, cutting backhaul by 70% and keeping biometric data inside jurisdictional borders. Fire departments in Los Angeles and Phoenix use edge-enabled thermal cameras to spot victims through smoke, trimming rescue times during wildfires.[4]Los Angeles Fire Department, “Edge-Enabled Thermal Cameras for Wildfire Response,” lafd.org However, rural counties face capital hurdles for ruggedized servers and small-cell densification.

Rapid Urbanization Spurring Smart-City Safety Platforms

China counts over 500 smart cities equipped with integrated public-safety analytics that blend surveillance, crowd sensing, and traffic management.[5]Government of China, “Smart-City Safety Platform Rollouts,” gov.cn India’s Smart Cities Mission funds AI-enabled cameras across 100 municipalities, automating unattended-baggage and collision alerts within 10 seconds. Gulf Cooperation Council cities embed public-safety modules inside broader city-tech rollouts, while Southeast Asian metros adopt command-and-control centers for flood and festival management. Interoperability lags due to proprietary data models, driving standards-body engagement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Litigation Risk from Algorithmic Bias Cases | -1.9% | North America and EU, with emerging scrutiny in APAC | Short term (≤ 2 years) |

| Fragmented Legacy RMS/CAD Data Silos Below County Level | -1.4% | North America, particularly in rural and under-resourced jurisdictions | Medium term (2-4 years) |

| Procurement-Cycle Delays Tied to Public-Tender Rules | -0.8% | Global, most pronounced in EU and South America | Medium term (2-4 years) |

| Scarcity of Cleared Data-Science Talent Inside Agencies | -1.1% | North America and EU, with acute shortages in specialized federal roles | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Litigation Risk from Algorithmic Bias Cases

Pasco County, Florida paid USD 105,000 in December 2024 to settle claims that a predictive-policing model disproportionately targeted minority neighborhoods. Similar lawsuits have driven several U.S. departments to pause deployments until external audits validate fairness metrics. Agencies now demand vendor indemnification clauses, inflating insurance premiums for software providers. Civil-liberties groups in San Francisco and Seattle disclosed racial-disparity rates through public-records requests, heightening reputational risks.

Fragmented Legacy RMS/CAD Data Silos Below County Level

Fewer than 40% of U.S. local agencies have adopted National Information Exchange Model standards, leaving neighboring jurisdictions unable to share incident data in real time. Proprietary on-premises platforms installed before 2015 persist in rural counties, with data-migration costs topping USD 500,000 for mid-sized departments. Fusion-center analysts confront inconsistent offense codes and missing geospatial tags, degrading predictive-model accuracy. Cloud consolidation offers a remedy but collides with data-sovereignty concerns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain Momentum as Talent Gaps Persist

Software remained the largest contributor, delivering 62.36% revenue in 2025. Record-management, investigation-management, and criminal-intelligence suites dominate because they plug directly into long-standing dispatch workflows and respect data-sovereignty mandates. Agencies prize modules that overlay geospatial layers on incident data and that backfill evidentiary chains which courts now expect in electronic form. Yet the services sub-segment is clocking a 17.02% CAGR, the fastest within the public safety analytics market. Professional-services teams handle data cleansing, legacy-system migration, and officer training, while managed-service contracts keep machine-learning models updated without straining in-house IT. A U.S. Office of Personnel Management tally showed more than 10,000 unfilled cleared-analytics positions in 2024, a gap that drives agencies to outsourced Public-Safety-as-a-Service agreements.

Demand for services also arises when small municipalities band together under volume contracts that bundle software licenses, cloud hosting, and 24/7 support. Vendors retain cleared data scientists who rotate across multiple counties, scaling scarce talent. As a result, services revenues will increasingly tie into outcome-based pricing schemes, with fees linked to response-time or crime-reduction benchmarks. The expanding role of services therefore not only cushions budget cycles but also deepens customer lock-in across the public safety analytics industry.

By Analytics Type: Prescriptive Capabilities Move Center Stage

Predictive analytics led revenue with a 38.63% slice in 2025, largely through crime-forecasting heat maps refreshed hourly to guide patrol routes. Prescriptive modules, growing at a 16.43% CAGR, fill that void by recommending ambulance repositioning or patrol redeployment. The U.S. Department of Health and Human Services earmarked part of a USD 1.5 billion opioid-crisis grant for overdose hot-spot routing, catalyzing prescriptive adoption in emergency medical services.

Prescriptive models demand high-quality, real-time input, pushing agencies to improve data-governance processes. Fire departments seeking to keep response times below the National Fire Protection Association’s six-minute benchmark employ reinforcement-learning loops to refine engine placement with every call outcome. The public safety analytics market size associated with prescriptive solutions is expected to widen most rapidly in jurisdictions where clean, structured data is already available from smart-city sensors.

By Deployment Model: Hybrid Cloud Threads the Needle on Sovereignty

On-premises systems absorbed 57.74% spending in 2025, a testament to deep-seated concerns about housing criminal evidence in multitenant clouds. State statutes often stipulate that personally identifiable data remain within borders, and only a handful of hyperscalers have achieved FedRAMP High status. However, compute-heavy video analytics make rigid on-premises architectures costly. Hybrid designs that keep raw video local but burst inference workloads to FedRAMP-certified clouds are therefore scaling at a 16.65% CAGR.

Microsoft Azure Government and Amazon Web Services GovCloud both received FedRAMP High authorization by 2024, easing migration fears for federal agencies. Axon’s cloud suite demonstrates how evidence is redacted and transcribed in the cloud while master files stay on agency servers. Cost-benefit analyses show that hybrid models can trim total cost of ownership by 20% over five years, savings that resonate with budget officers and accelerates cloud momentum inside the public safety analytics market.

By Application: Resource-Allocation Optimization Takes Off

Surveillance and video analytics dominated with 31.83% revenue in 2025 as body-camera mandates proliferated. Generative-AI transcription tools now auto-draft incident reports, freeing officers for field work. Yet resource-allocation optimization is the fastest climber at 16.32% CAGR. The Los Angeles Fire Department cut average response times by 8% after deploying a platform that repositions apparatus in real time based on historical call density and current traffic.

As smart-city sensors stream occupancy, weather, and special-event data into command centers, prescriptive engines ingest those feeds to predict surge demand. Public-transport agencies also use the algorithms to adjust staffing at rail hubs prone to crowding. Consequently, the public safety analytics market size tied to resource-allocation optimization is expected to show the sharpest absolute gains through 2031.

By End-User: Critical Infrastructure Operators Accelerate Spend

Law-enforcement agencies remained the largest buyers with 32.84% spending in 2025, spanning case-management, evidence tracking, and community-engagement dashboards. However, transportation and critical-infrastructure entities are expanding budgets at a 16.37% CAGR. Airports now deploy anomaly-detection video analytics that flag unattended bags in seconds, while electric-utility operators integrate radar and acoustic sensors to meet tightening North American Electric Reliability Corporation mandates.

Port authorities rely on cargo-flow anomaly detection to spot contraband, and rail operators fuse passenger-density analytics with threat-detection feeds for safer operations. With uptime mandated by regulators, critical-infrastructure operators contract for service-level agreements that include predictive maintenance, embedding themselves as a durable growth vector inside the public safety analytics industry.

Geography Analysis

North America generated 38.74% of 2025 revenue, powered by United States investments in NG 9-1-1, opioid-crisis analytics, and FirstNet’s 5G edge rollouts. Provinces in Canada are consolidating municipal systems into provincial command centers to improve interoperability, while Mexico focuses deployments along border corridors and metropolitan hubs. Adoption in smaller U.S. counties is rising through state-negotiated consortia contracts that distribute upgrade costs.

Europe’s share reflects rapid uptake in Germany, the United Kingdom, France, Italy, and Spain, all of which must meet the EU AI Act’s transparency mandates by 2026. Nordic countries demonstrate high digital maturity, using prescriptive allocation models across firefighting and emergency medical services. Tender timelines, however, extend procurement cycles beyond 18 months in many EU jurisdictions, slowing the otherwise robust expansion of the public safety analytics market.

Asia-Pacific charts the fastest CAGR at 16.54% as China’s 500-plus smart-city program mainstreams license-plate readers, crowd sensors, and incident-management suites. India’s 100-city initiative, plus Gulf Cooperation Council megaprojects like NEOM, inject steady order flow. Japan and South Korea integrate seismic sensors with analytics to automate earthquake alerts, while Australia deploys satellite GNSS feeds for wildfire prediction. Despite infrastructure gaps in Africa and budget constraints in parts of South America, São Paulo and Buenos Aires showcase integrated command centers blending social-media monitoring with emergency hotlines, illustrating the broader regional potential of the public safety analytics market.

Regulatory Landscape

Public safety analytics procurement is being shaped by AI governance and public-space video rules that increase documentation, auditability, and interoperability requirements. In the United States, OMB Memorandum M-24-10 (March 2024) pushed federal agencies toward NIST AI RMF-aligned governance for rights- or safety-impacting AI, and OMB Memorandum M-24-18 (October 2024) extended AI RMF-aligned requirements into federal procurement, affecting how computer-vision and decision-support analytics are specified and evaluated in bids.

Across Europe, the EU AI Act treats many law-enforcement analytics use cases as high-risk, with compliance obligations referenced in this report context for August 2026. That timeline is expected to accelerate dataset auditing, bias-testing logs, and human-oversight controls within operational workflows. In China, the State Council implemented the Regulations on the Management of Public Security Video Image Information Systems (Decree No. 799) from April 1, 2025, and national standards such as GB/T 46344.1-2025, GB/T 46344.2-2025, GB/T 46344.5-2025, and GB/T 46363-2025 with May 2026 implementation dates add interface and system requirements that reinforce cross-system video/image information sharing and constrain ad hoc integrations. Technical standards such as IEC 62676-2-11:2024 also formalize interoperability profiles for VMS and cloud VSaaS, shaping how vendors design emergency-access tiers, metadata exchange, and third-party connectivity for public safety operations.

Value Chain Analysis

The value chain starts with multi-source data generation (CAD/911 call handling, RMS, body-worn video and fixed CCTV, drones, IoT and traffic sensors, and open-source/social signals), then moves into connectivity and secure transport (including purpose-built 911 and public-safety broadband networks), followed by ingestion, identity resolution, and data engineering. Core platforms (CAD/RMS, digital evidence management, and real-time crime center software) form the system of record, while specialized analytics layers provide video AI (detection, search, redaction), geospatial intelligence, and predictive/prescriptive models. Agencies and integrators complete the chain through configuration, model governance, training, and managed services (PSaaS) that keep pipelines current and compliant.

Recent partnerships show the chain tightening around API-first interoperability and secure delivery. In April 2026, RapidSOS and AT&T integrated RapidSOS HARMONY AI with AT&T ESInet so real-time intelligence from the Safety Network traverses dedicated 911 infrastructure rather than the public internet, aligning with data-sovereignty and security constraints. Platform-embedding has also accelerated: Flock Safety and Coreforce (January 2026) connected LPR and hotlist data into Coreforce RTCC and digital evidence workflows, while Mark43 and ForceMetrics (May 2026) integrated a context and decision-assistance engine into cloud-native CAD/RMS to reduce operator swivel-chair time. Complementary visualization and analytics bundling is evident in Veritone and LeoSight (March 2026), and aerial intelligence workflows expanded with the BRINC Drones and Nova Software partnership (June 2026) to fuse drone capture with mapping and thermal analytics.

Competitive Landscape

Moderate concentration prevails, with the top five suppliers holding roughly 40-45% collective share, leaving headroom for disruptors offering prescriptive modules, satellite-data fusion, or gunshot-detection subscriptions. Incumbents such as Motorola Solutions and Tyler Technologies leverage entrenched record-management and dispatch footprints to cross-sell analytics add-ons, increasing average contract values. Cloud-native challengers pursue open-API strategies that interoperate with legacy systems, winning agencies that prefer incremental modernization.

Strategic moves cluster around AI-talent acquisitions, FedRAMP High certifications, and partnerships with satellite-imagery providers. For instance, multiple vendors integrated wildfire-risk layers derived from earth-observation feeds, appealing to Western U.S. agencies confronting record fire seasons. Explainability is now table stakes; Palantir embeds SHAP diagnostic tools that let detectives interrogate why a location surfaces as a hot spot without scripting SQL queries.

Pricing models evolve toward outcomes, with performance clauses linked to response-time metrics or crime-rate deltas. Although litigation risks temper aggressive deployments, vendors that offer indemnity and bias-testing toolkits differentiate themselves. Over the medium term, mergers among mid-tier firms are likely as scale proves critical for absorbing regulatory overhead inside the public safety analytics market.

Public Safety Analytics Industry Leaders

Splunk Inc. (Cisco Systems Inc.)

SAS Institute Inc.

IBM Corporation

Tyler Technologies Inc.

Omnigo (The Riverside Company)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term opportunity is concentrated in compliance-ready, interoperable analytics that help agencies meet NG 9-1-1 multimedia ingestion mandates and emerging AI governance rules without rebuilding end-to-end stacks. Procurement language is moving toward audit trails, explainability, and controlled data exchange, which creates whitespace for vendors that ship bias-testing logs, redaction-by-default evidence workflows, and standards-aligned interfaces that plug into entrenched CAD/RMS and digital evidence platforms. Interoperability standards such as IEC 62676-2-11:2024 for VMS/VSaaS, and China’s GB/T video information sharing and interface requirements with May 2026 implementations (including GB/T 46363-2025 referenced in the evidence pack), support multi-vendor deployments where agencies can demand defined access tiers and metadata sharing rather than bespoke integrations.

Funding programs and large multi-jurisdiction deployments provide practical routes to scale services and cloud/hybrid delivery models. In the United States, DOJ Bureau of Justice Assistance opened the FY 2026 NIBIN Modernization Program to fund modernization across 194 sites, expanding demand for analytics that connect ballistic imaging outputs to investigative case workflows and digital evidence search. Regional NG 9-1-1 modernization also supports cloud-native call handling and analytics layers, illustrated by Carbyne being selected for the Metropolitan Washington Council of Governments 911 Call Handling System serving 24 local governments (March 2026). Agency contract wins underscore operational use cases beyond surveillance: San Jose signed a nearly USD 3.8 million, seven-year agreement for the Ladris Core platform (March 2026) for emergency management and predictive analytics, while Cognyte disclosed a USD 5 million investigative analytics contract with a tier-1 US law enforcement agency (March 2026). Recurring renewals further validate subscription-style deployments for acoustic and real-time safety platforms, with SoundThinking announcing over USD 23 million in multi-year customer renewals in Q2 2026 (July 2026).

Recent Industry Developments

- July 2026: SoundThinking announced over USD 23 million in multi-year customer renewals for ShotSpotter and its broader safety platform during Q2 2026. The renewals highlight sustained budget allocation for subscription-based, real-time detection and incident analytics, reinforcing the role of recurring services in agency operating models.

- March 2026: Cognyte disclosed a USD 5 million contract with a tier-1 US law enforcement agency to support mission-critical investigations. The award signals continued procurement of specialized investigative analytics alongside core CAD/RMS modernization, especially where agencies need faster triage across large volumes of digital evidence and intelligence data.

- December 2025: Los Angeles Fire Department expanded its prescriptive-dispatch platform citywide after reporting an 8% pilot reduction in response times. The expansion elevates resource-allocation optimization from pilot projects to scaled operations, increasing demand for implementations, integrations, and ongoing model and data-management services.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the public safety analytics market is defined as revenue earned from analytics software and related services used by public safety agencies to combine and analyze data for prevention, situational awareness, and incident response across day to day operations.

Scope exclusions: We exclude physical security and communications hardware (such as cameras, radios, and sensors) and internal back office analytics like HR or payroll tools.

Segmentation Overview

- By Component

- Software

- Record Management

- Investigation Management

- Location/Geo-Spatial Intelligence

- Criminal and Crime Intelligence

- Predictive and Prescriptive Modules

- Services

- Professional Services

- Managed / PSaaS

- Software

- By Analytics Type

- Descriptive Analytics

- Diagnostic Analytics

- Predictive Analytics

- Prescriptive Analytics

- By Deployment Model

- On-Premise

- Cloud / SaaS

- By Application

- Person-of-Interest Screening

- Surveillance and Video Analytics

- Incident Detection and Management

- Pattern Recognition and Hot-Spot Mapping

- Resource-Allocation Optimisation

- By End-User

- Law Enforcement

- Emergency Medical and EMS

- Firefighting and Rescue

- Transportation and Critical Infrastructure

- Other Government Agencies

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to lock the market boundary and identify demand signals that can be tracked year to year. We referenced non-paywalled public sources such as US Department of Justice and Bureau of Justice Statistics releases, FEMA and DHS preparedness program materials, FCC and state level NG911 guidance, and public procurement portals that publish RFPs and award notices. We also reviewed international statistics and policy notes from bodies such as the United Nations Office on Drugs and Crime to understand broader safety and crime data trends.

To support assumptions around solution uptake and pricing structure, we used company annual reports, investor presentations, and product documentation, then cross checked with reputable press and association updates that point to deployment shifts such as cloud adoption and data sharing requirements. Patent databases were checked selectively to confirm where analytics features are being developed, for example video analytics and real time incident decision support. The sources mentioned here are illustrative, and many other public references were also reviewed to collect, cross check, and clarify inputs.

Primary Interviews and Surveys

Primary work focused on validating what agencies and operators actually buy, how contracts are split between software and services, and how deployment choices affect pricing. We covered public sector users, system integrators, and solution providers across APAC, EMEA, and the Americas so adoption timing, renewal cycles, and module level uptake could be confirmed with real world context.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 13% | APAC: 48% |

| Mid tier: 59% | Functional/Unit leaders: 29% | EMEA: 31% |

| Smaller Players: 15% | Managers: 58% | Americas: 21% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the addressable spend pool using public safety digitization signals, and then allocates that spend to analytics demand. We use indicators such as the pace of NG911 and CAD modernization, the share of agencies moving to cloud deployments, typical contract length and renewal timing, and the split between software subscription and services that comes with implementation.

Those totals are corroborated with selective bottom-up approximations, where sampled disclosures, channel checks, and typical ASP by module and deployment mode are multiplied by plausible adoption volumes for key agency types. When data is thin for smaller geographies or niche use cases, gap handling is done through proxy ratios from similar public sector software categories and procurement pattern matching, and then the assumptions are checked again in follow ups.

For forecasting, scenario analysis is used with a light multivariate regression overlay so the outlook can reflect shifts in grant cycles, budget mix, cloud migration speed, and data governance rules. Inputs stay practical, and the final curve is adjusted only after our primary feedback supports both the direction and the magnitude.

Data Validation & Update Cycle

Validation is done through multiple checks that look for mismatches between modeled revenue and independent signals, including procurement activity, agency modernization programs, and observed pricing ranges. Outliers are flagged for review, and we re-contact sources when a large swing is driven by one assumption such as adoption speed, services attachment, or currency treatment.

Before sign-off, the model and core inputs go through an internal review so calculations and logic stay consistent across regions and years. Reports are refreshed annually, and interim updates are made when there are material events such as policy changes, budget reallocations, or notable demand shocks. Right before delivery, a fresh scan is completed so clients receive the latest updated view.

Mordor Intelligence's Public Safety Analytics Market Size Versus Other Published Estimates

Published market sizes for public safety analytics can vary widely even when the topic name looks the same, because scope choices and update timing are not consistent across publishers. The biggest differences usually come from what is counted as analytics revenue, how software subscriptions are separated from implementation services, and which years are used for currency conversion.

In this market, the spread is often driven by refresh cadence and the way ASP is normalized across multi year subscriptions, usage expansion, and services attachment rates. When adjacent areas like hardware led surveillance upgrades are included, or when procurement reality checks are not applied, the number can move without reflecting a true change in analytics adoption.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 16.87 B (2026) | |

| Global Consultancy A | USD 14.60 B (2025) | Uses a different base year and a shorter study window, and the public summary does not clarify how multi year subscription normalization and currency conversion timing are handled, which can shift the starting value. |

| Industry Publisher B | USD 11.79 B (2025) | Starts from a lower 2025 value and provides limited public detail on services attachment treatment and validation checks against procurement signals, which can reduce the estimate for software plus services coverage. |

The table shows that base year choice and normalization rules explain a large part of the gap. By rechecking currency timing, services attachment, and renewal driven ASP progression on a set cadence, Mordor Intelligence keeps the 2026 value tied to observable contracting patterns.

Key Questions Answered in the Report

How large is the public safety analytics market in 2026?

The public safety analytics market size reached USD 16.87 billion in 2026.

What CAGR is projected for public safety analytics to 2031?

The sector is forecast to expand at a 15.42% CAGR through 2031.

Which component grows fastest inside public safety analytics platforms?

Services, including managed and professional offerings, are advancing at a 17.02% CAGR as agencies outsource data-science expertise.

Why is prescriptive analytics gaining traction among public-safety agencies?

Prescriptive modules recommend concrete actions, such as ambulance repositioning, and are expanding at a 16.43% CAGR thanks to opioid-prevention grants and response-time mandates.

Page last updated on: