Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

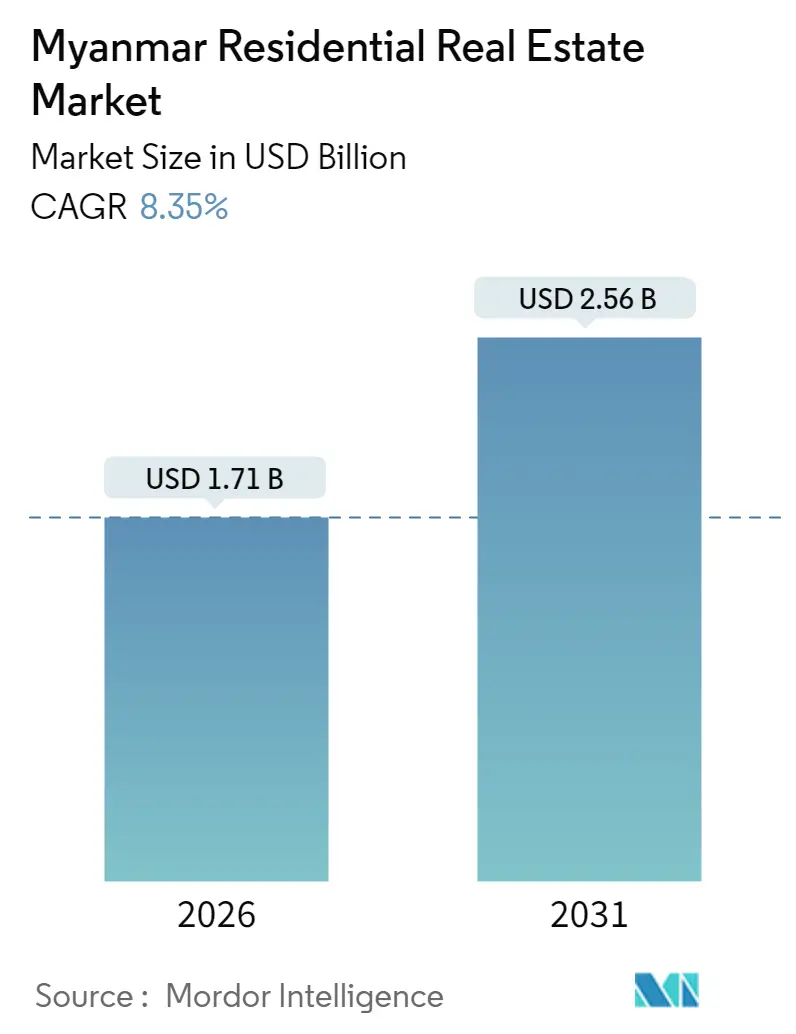

| Market Size (2026) | USD 1.71 Billion |

| Market Size (2031) | USD 2.56 Billion |

| Growth Rate (2026 - 2031) | 8.35% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Myanmar Residential Real Estate Market Analysis by Mordor Intelligence

Myanmar residential real estate market size in 2026 is estimated at USD 1.71 billion, growing from 2025 value of USD 1.58 billion with 2031 projections showing USD 2.56 billion, growing at 8.35% CAGR over 2026-2031. This trajectory underscores the market’s resilience despite the political upheaval since 2021, with urbanization in Yangon and Mandalay, returning diaspora capital, and large-scale infrastructure projects acting as primary growth levers. Developers capitalize on rising demand for secure, amenity-rich condominiums even as inflation, currency volatility, and scant mortgage financing weigh on household purchasing power. Consolidation opportunities are widening because well-capitalized conglomerates enjoy privileged access to land, foreign partners, and government approvals, giving them an edge over smaller peers in a fragmented playing field. Meanwhile, regional cities such as Mawlamyine attract new projects as land prices and regulatory bottlenecks in Yangon push builders outward.

Key Report Takeaways

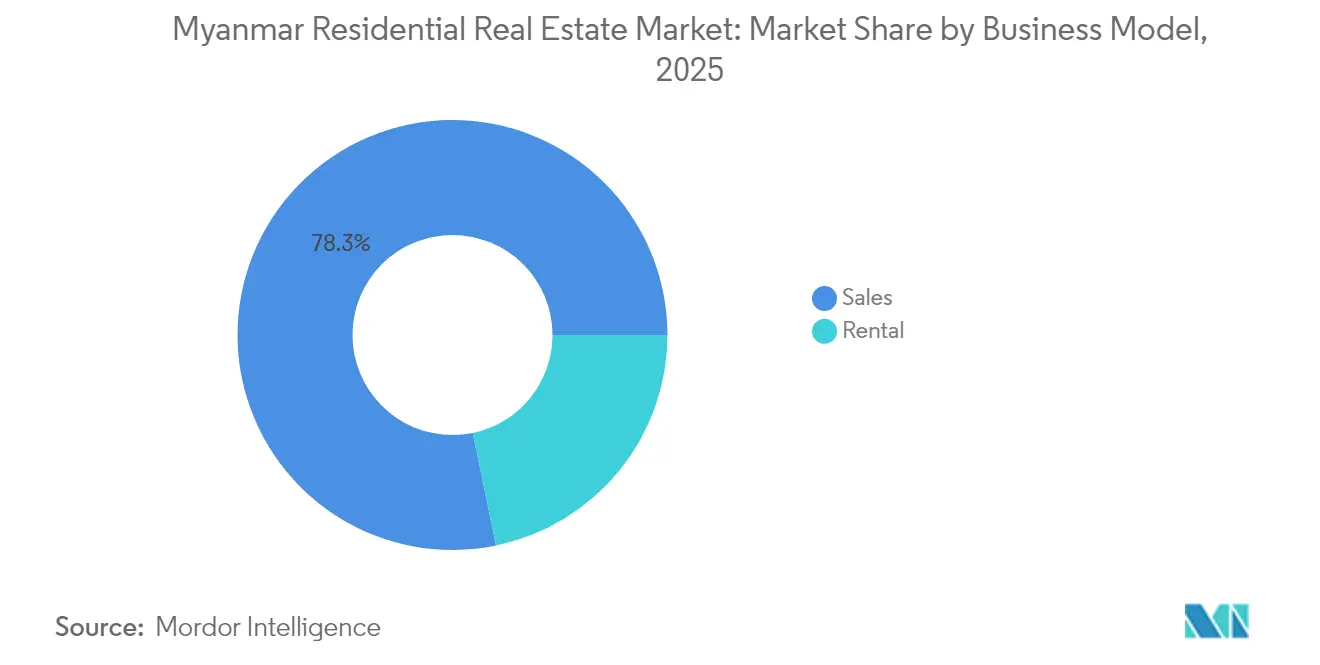

- By business model, sales captured 78.25% of the Myanmar residential real estate market share in 2025, while rentals are advancing at a 9.02% CAGR through 2031.

- By property type, condominiums held 66.45% of the Myanmar residential real estate market size in 2025 and are expanding at a 9.38% CAGR to 2031.

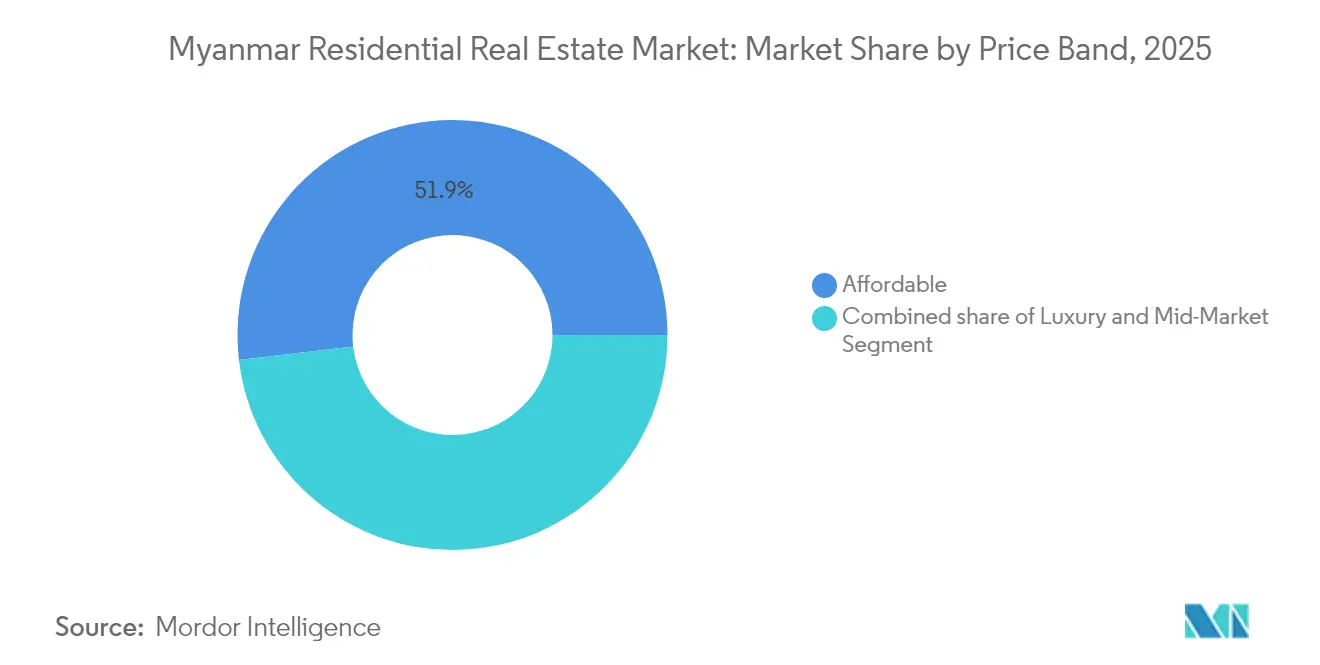

- By price band, affordable housing commanded a 51.85% share of the Myanmar residential real estate market size in 2025; mid-market housing is growing at a 9.21% CAGR through 2031.

- By mode of sale, primary transactions represented 71.05% of the Myanmar residential real estate market size in 2025, while secondary resales are climbing at a 9.28% CAGR to 2031.

- By city, Yangon led with 48.65% revenue share in 2025; Mawlamyine is projected to grow the fastest at 9.76% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Myanmar Residential Real Estate Market Trends and Insights

Drivers Impact Analysis

| Drivers | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanization in Yangon and Mandalay is driving demand for modern housing projects | +2.8% | Yangon, Mandalay, and spillover to Naypyidaw | Medium term (2-4 years) |

| Infrastructure investments under regional connectivity initiatives are creating new residential corridors | +2.1% | Mawlamyine, Kyaukphyu, border regions | Long term (≥ 4 years) |

| Rising interest from diaspora investors in residential properties | +1.9% | Global, concentrated in Yangon premium segments | Short term (≤ 2 years) |

| Emergence of condominiums and gated communities catering to lifestyle and security preferences | +1.6% | Yangon, Mandalay urban cores | Medium term (2-4 years) |

| Government census and urban planning initiatives supporting housing development | +1.2% | National, focus on major townships | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Urbanization in Yangon and Mandalay Driving Demand for Modern Housing Projects

Nationwide census activities using mobile tablets across 594 townships in 2025 supply policymakers with granular housing data, and projects such as the Dagon Seikkan Township master plan signal sustained official backing for large urban extensions. Rural under-employment and a 5% contraction in agricultural output following Typhoon Yagi have intensified rural-to-city migration, inflating demand for affordable and mid-market units. Flagship eco-projects like Oak Village in Pyin Oo Lwin demonstrate that buyers now prize energy efficiency and community design alongside location. With nationwide electrification dipping to 48% in 2025, new projects that guarantee reliable power and internet connectivity enjoy premium pricing. Taken together, urban migration and lifestyle shifts keep the Myanmar residential real estate market on a steady growth path[1]Department of Population, “Myanmar Inter-Censal Survey 2024 Snapshot,” Ministry of Immigration and Population, moi.gov.mm.

Infrastructure Investments Under Regional Connectivity Initiatives: Creating New Residential Corridors

Kyaukphyu’s USD 7.3 billion deep-sea port and adjoining residential zone won renewed cabinet backing in 2025, opening long-term demand corridors in Rakhine State. Parallel upgrades under the Yunnan-Lincang Border Economic Cooperation Zone and the Kaladan Multi-Modal Transit Transport Project shorten travel times, spur industrial job creation, and seed fresh housing clusters along highways and logistic parks. By 2025, 152 km of rural roads will be newly paved, connecting 14 million residents to all-weather routes and enlarging developers’ land banks outside congested metros. Nevertheless, sporadic fighting in Kachin and Shan borderlands complicates site selection and inflates security costs, underscoring uneven project execution. Even so, connectivity dividends outweigh risks, adding 2.1% to forecast CAGR as new commuter belts take shape[2]Asian Development Bank, “Rural Roads and Access Project Completion Report,” Asian Development Bank, adb.org.

Rising Interest From Diaspora Investors in Residential Properties

The kyat’s 40% slide against the U.S. dollar in early 2024 triggered capital flight, with Myanmar buyers picking up 1,050 Thai condominiums worth USD 152.9 million in the first nine months alone. Domestically, condominium purchases in Yangon’s Bahan and Dagon neighborhoods remain popular hedges against inflation despite tightened banking rules that complicate foreign currency transfers. New income-tax levies on overseas workers aim to recapture hard currency, but compliance hurdles steer a portion of diaspora wealth back into local bricks-and-mortar. Property developers now court diaspora buyers with installment plans and online marketing, offsetting soft local demand. The resulting inflow of high-quality capital helps stabilize the Myanmar residential real estate market during volatile macro cycles.

Emergence of Condominiums and Gated Communities Catering to Lifestyle and Security Preferences

With the military controlling just 30% of the country and resistance forces holding over 40%, urban households increasingly favor gated projects with 24-hour surveillance. The Condominium Law still permits foreigners to own up to 40% of units above the sixth floor, a rule developers exploit to widen their buyer pool. Projects such as Oak Village weave renewable energy systems and smart-home controls into site planning, aligning with international ESG preferences. Premium inventory in StarCity and Yoma Central is approaching sell-out stages despite wider market turbulence, underscoring confidence in secure, amenity-rich formats. Gated and vertical communities now set the design benchmark, lifting unit prices while upgrading urban living standards.

Restraints Impact Analysis

| Restraints | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Political and economic instability deterring large-scale residential investment | -3.8% | National, most severe in conflict zones | Short term (≤ 2 years) |

| Severe inflation and currency devaluation limiting purchasing power | -3.2% | National, middle-income segments hardest hit | Short term (≤ 2 years) |

| Weak mortgage financing system and banking sector constraints | -2.1% | National, limited access to formal credit | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Political and Economic Instability Deterring Large-Scale Residential Investment

Armed clashes have intensified in 2024-2025, shrinking junta-controlled territory to 30% and wiping USD 11 billion off national assets after the March 2025 earthquake. Foreign direct investment collapsed to USD 150 million in the first seven months of 2024, versus USD 3.8 billion in 2020, leaving many projects starved for offshore capital. Conflict-driven logistics disruptions reduced agricultural output by 5%, undercutting rural incomes that might fund remittances for urban housing. With 40% of youth eager to emigrate rather than enlist in compulsory service, the domestic buyer pool has thinned. Until peace prospects improve, large-scale residential schemes face slower presales, lengthier construction cycles, and higher financing costs[3]World Bank, “Myanmar Macro-Poverty Outlook April 2025,” World Bank, worldbank.org.

Severe Inflation and Currency Devaluation Limiting Purchasing Power

Average inflation reached 25.4% in 2024-2025 while real wages for construction labor fell 21-28%, inflating build costs and eroding homebuyer savings. The poverty rate nearly doubled to 49.7% in 2023, and 76% of the population now lives at or near poverty thresholds, suppressing non-essential housing demand. Food prices climbed 50% in 2022, and the dual exchange-rate regime muddies property valuations, especially for foreign-currency-denominated units. Developers resort to graduated payment plans, yet affordability gaps persist, especially outside expatriate and elite buyer circles. Unless macro-stability returns, inflation remains a critical drag on the Myanmar residential real estate market.

Segment Analysis

By Business Model: Sales Dominance Amid Rental Growth

Sales transactions claimed 78.25% of the Myanmar residential real estate market share in 2025 as cultural norms still prize outright ownership, and mortgage scarcity enforces cash-based deals. Primary developers sweeten presales with 18- to 36-month installment plans, leveraging direct financing to compensate for weak bank lending. Rentals, though smaller, are expanding at a 9.02% CAGR, fueled by mobile young professionals and a growing expatriate NGO workforce concentrated in central Yangon. Short-lease flexibility attracts middle-income households cautious about long-term debt, while currency volatility prompts landlords to quote rents in USD to hedge depreciation. Foreign buyers restricted to condominiums rely on rental yields rather than capital gains, sustaining investor appetite.

The rental pipeline is thickest around Yankin, Bahan, and Sanchaung townships, where occupancy for Grade-A apartments held above 80% even during 2024’s political unrest. Co-living concepts have surfaced in Mandalay and Naypyidaw, targeting civil servants and consultants on short projects. Conversely, sales transactions skew toward newly urbanized suburbs like Dagon Seikkan, where land is cheaper and supply pipelines plentiful. Developers with in-house leasing arms capitalize on both revenue streams, signaling a gradual but steady diversification of the Myanmar residential real estate market.

Note: Segment shares of all individual segments available upon report purchase

By Property Type: Condominiums Lead Urban Development

Condominiums commanded 66.45% of the 2025 property mix and contributed to the bulk of Myanmar's residential real estate market size gains, advancing at a 9.38% CAGR as vertical projects maximize scarce urban land. Foreign-ownership provisions allowing 40% strata title to non-citizens enhance investor liquidity, and integrated amenities such as gymnasiums, co-working lounges, and back-up generators differentiate them from aging walk-ups. Landed villas persist around Inya Lake and Pyin Oo Lwin, but price points above USD 500,000 restrict their buyer base to elite families and diaspora executives.

The shift to high-rise living is further reinforced by municipal caps on building heights that favor consolidated master plans over piecemeal lot redevelopment. Mixed-use megaprojects such as Yoma Central bundle residential towers with office blocks, hospitality, and retail, creating one-stop lifestyle hubs. Developers increasingly integrate photovoltaic panels, rainwater harvesting, and smart-access controls to future-proof assets against energy shortfalls and security threats. Such innovations bolster buyer confidence and sustain absorption rates, especially when bankable branding partners are involved.

By Price Band: Affordable Housing Drives Volume

Affordable units priced below USD 35,000 generated 51.85% of 2025 transaction value, supported by DUHD lotteries and public-private JV projects. However, the mid-market tier (USD 35,000-100,000) is the fastest-rising slice, expanding at 9.21% CAGR as young professionals demand better finishes, elevators, and secure parking. Developers tackle affordability by offering compact 450- to 600-sq-ft layouts, shared recreational spaces, and modular construction that trims per-square-foot costs.

Luxury inventory retains a niche following among diplomats, energy executives, and returning diaspora, yet political risk premiums and capital controls temper price escalation. In Yangon’s prime Golden Valley, ask prices dipped 8% in 2024 before stabilizing on scarce supply and foreign buyer interest. Elsewhere, subsidized housing projects in Shwe Pyi Thar and Hlinethaya townships close the gap between policy rhetoric and real delivery, although land title complexity and infrastructure deficits challenge pace and scale.

Note: Segment shares of all individual segments available upon report purchase

By Mode of Sale: Primary Market Strength

Primary launches formed 71.05% of deals in 2025, reflecting the Myanmar residential real estate market’s early-stage evolution and the limited stock of modern second-hand apartments. Developers wield aggressive marketing, virtual walk-throughs, and early-bird discounts to hit presale targets that unlock construction loans. Down-market condominiums in south Dagon sold out within weeks after developers tied up financing with home-grown micro-lenders, evidence of pent-up demand for entry-level units.

Secondary transactions, growing at 9.28% CAGR, are concentrated in older downtown Yangon buildings where owners capitalize on diaspora-driven appreciation. The secondary market’s maturation spurs the development of valuation standards, real estate agencies, and legal closing services that enhance market transparency. Cross-listing of resales on digital platforms accelerates price discovery, drawing speculative capital even amid political uncertainty. Collectively, the two channels work in tandem to deepen liquidity and price signals across the Myanmar residential real estate market cycles.

Geography Analysis

Yangon’s 48.65% foothold in the Myanmar residential real estate market continues because of its superior transport links, diversified employment, and a deepening service economy anchored by international banks and telecoms. Flagship compounds such as StarCity envision 40,000 units over multiple phases, providing scale efficiencies and cross-subsidized affordable blocks that broaden buyer reach. Yet permit suspensions for non-compliant towers underscore persistent governance hurdles, nudging some developers toward satellite towns where approvals are quicker and land is one-third the cost. Price resilience varies sharply: premium lakefront plots hold value, while older CBD walk-ups saw 25-30% corrections amid pandemic-era vacancies. Despite volatility, diaspora inflows and global NGO staff sustain demand for well-managed condominiums that guarantee power backup and security.

Mawlamyine, scaling at 9.76% CAGR through 2031, benefits from its proximity to Thailand and new port facilities funded under the China-Myanmar Economic Corridor. Highway upgrades slashing Yangon commute times to under five hours improve labor mobility and open weekend-home markets. Industrial park leases to garment and agro-processing firms boost job counts, and lower land prices—often 60-70% below Yangon—attract developers targeting USD 30,000-45,000 unit brackets. Nevertheless, sporadic border unrest demands elevated security spending and contingency planning, while limited local banking services slow mortgage uptake.

Mandalay, Naypyidaw, and the Rest of Myanmar contribute to the balance of market opportunity. Mandalay’s role as a cultural and trading hub feeds mixed-use projects near the Mandalay Palace moat, where land reclamation schemes enable waterfront condos. Naypyidaw’s vast boulevards and government offices create predictable demand for townhouse rentals among civil servants and military families. Elsewhere, secondary hubs like Taunggyi and Pyay gain from road and bridge improvements tied to ADB rural access programs, making land-banking attractive for early entrants. Across these regions, the Myanmar residential real estate market expands on the back of infrastructure synergies, though weaker professional services and banking depth temper velocity.

Competitive Landscape

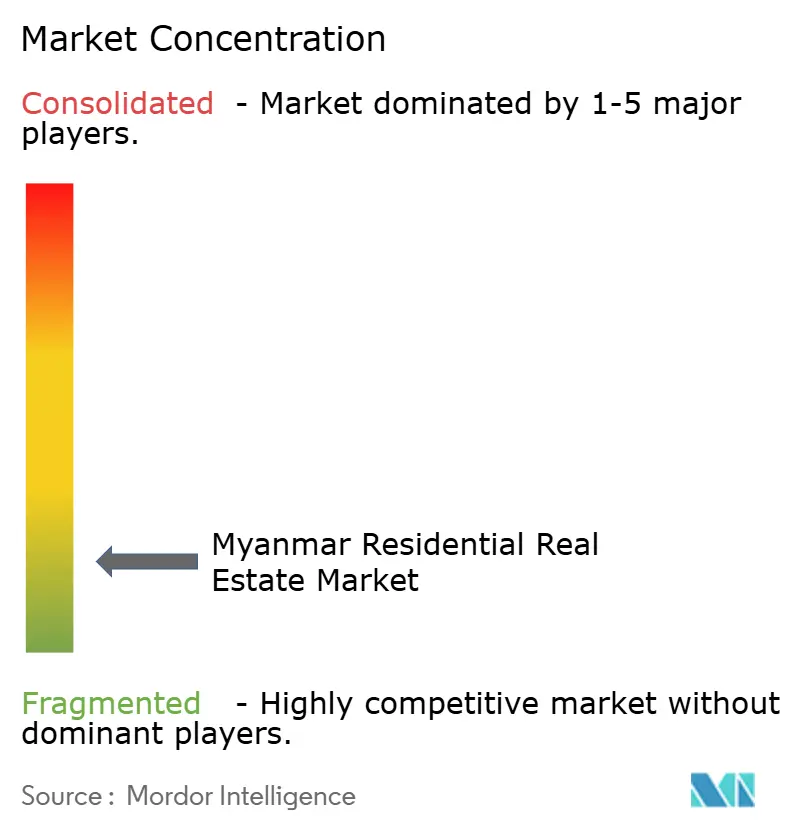

The Myanmar residential real estate market remains fragmented, with no single developer holding a double-digit share. Yoma Strategic Holdings returned to profitability in 2024 with USD 220.8 million revenue, leveraging mixed-use pipelines such as Yoma Central to spread risk across residential, office, and hospitality verticals. Shwe Taung Group exploits integrated capabilities in cement, aggregates, and engineering to cut construction costs and deliver large townships like City Loft. KBZ Group uses its banking arm to pre-qualify buyers, accelerating unit absorption even in soft markets.

Foreign players such as Keppel Land partner with local license holders to comply with land-title restrictions while injecting capital and quality standards. Township models dominate strategic thinking, providing captive demand for retail and school facilities that enhance land values. Smart-home features and rooftop solar arrays increasingly appear in upper-mid projects, marking a gradual tech upgrade. Affordable-housing specialists seize government tenders that bundle low-cost land with CHID loans at sub-market interest, though execution risks remain elevated. Against this backdrop, consolidation is likely as well-funded conglomerates acquire stalled projects from distressed smaller builders, tightening supply and raising barriers to entry.

Myanmar Residential Real Estate Industry Leaders

Marga Group

Shwe Taung Group

Yoma Strategic Holdings

Dagon Group

Eden Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The launch of a 249-unit affordable housing sale across four projects by the Department of Urban and Housing Development, coupled with CHID loans for 2,020 pre-qualified buyers who deposited over USD 1,430 each, is expected to enhance accessibility to affordable housing and address the growing demand for such units.

- January 2025: The unveiling of Clover 35, a high-rise in Mandalay by Yar Zar Group, reflects the increasing interest in vertical developments and signals a growing trend toward urbanization and modern infrastructure in the region.

- January 2025: The commencement of Tower 4 at 169 Residence by MTP Construction demonstrates the effectiveness of phased build-and-sell strategies in managing market volatility and aligning supply with fluctuating demand.

- January 2025: The opening of pre-sales for CBD Kywel Sel Kan, a mixed-use complex integrating residential and retail spaces, highlights a shift toward creating self-sustained urban hubs that cater to evolving consumer preferences for convenience and integrated living.

Myanmar Residential Real Estate Market Report Scope

Real estate (land and any buildings on it) used for residential purposes is commonly referred to as residential real estate; single-family dwellings are the most prevalent type of residential real estate. A complete background analysis of the Myanmar Residential Real Estate Market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact is included in the report.

The Myanmar residential real estate market is segmented by type (villas/landed houses and condominiums/apartments) and by cities (Yangon, Mandalay, Naypyidaw, Mawlamyine, and Other Cities). The report offers market size and forecasts in values (USD) for all the above segments.

By Business Model

| Sales |

| Rental |

| By Business Model | Sales |

| Rental |

Key Questions Answered in the Report

What is the forecast size of the Myanmar residential real estate market by 2031?

The Myanmar residential real estate market size is projected to reach USD 2.56 billion by 2031.

Which city is expected to grow fastest in residential property demand?

Mawlamyine is set to expand at a 9.76% CAGR, the fastest among Myanmar’s city markets through 2031.

How large is the sales segment compared with rentals?

Sales held 78.25% of 2025 transactions, while rentals, though smaller, are growing faster at 9.02% CAGR.

Why are condominiums the leading property type?

Condominiums capture a 66.45% share due to urban land scarcity, foreign-ownership allowances, and demand for secure amenities.

Page last updated on: