Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

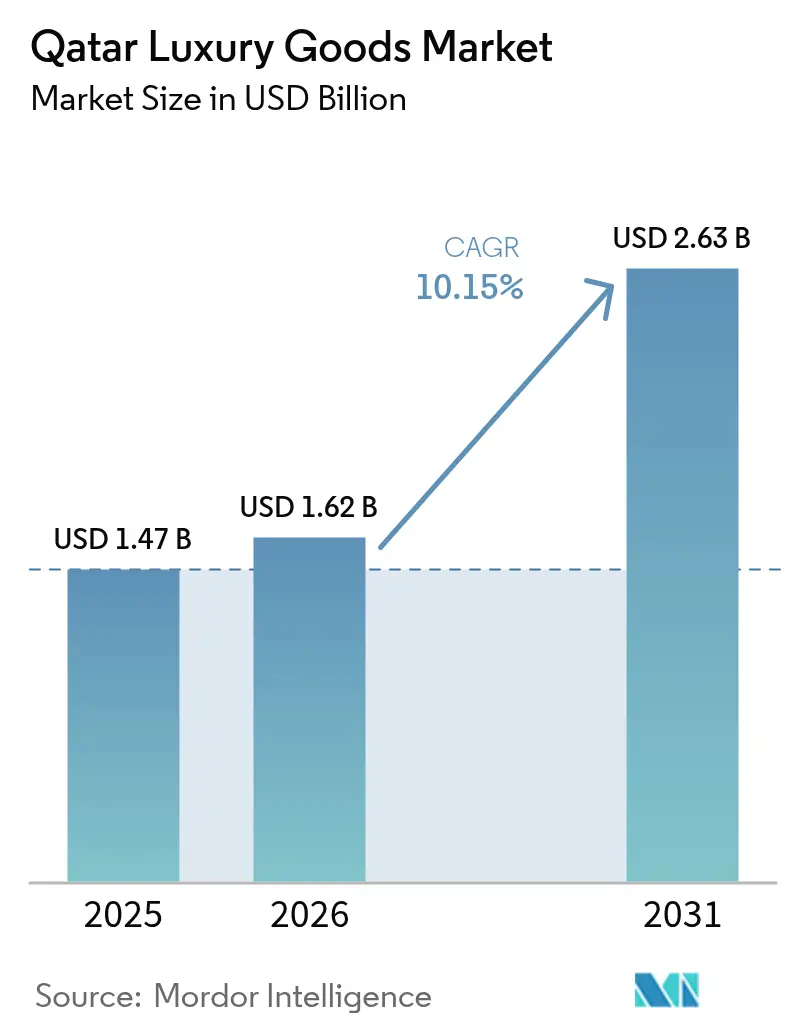

| Base Year Market Size (2025) | USD 1.47 Billion |

| Market Size (2026) | USD 1.62 Billion |

| Market Size (2031) | USD 2.63 Billion |

| Growth Rate (2026 - 2031) | 10.15% CAGR |

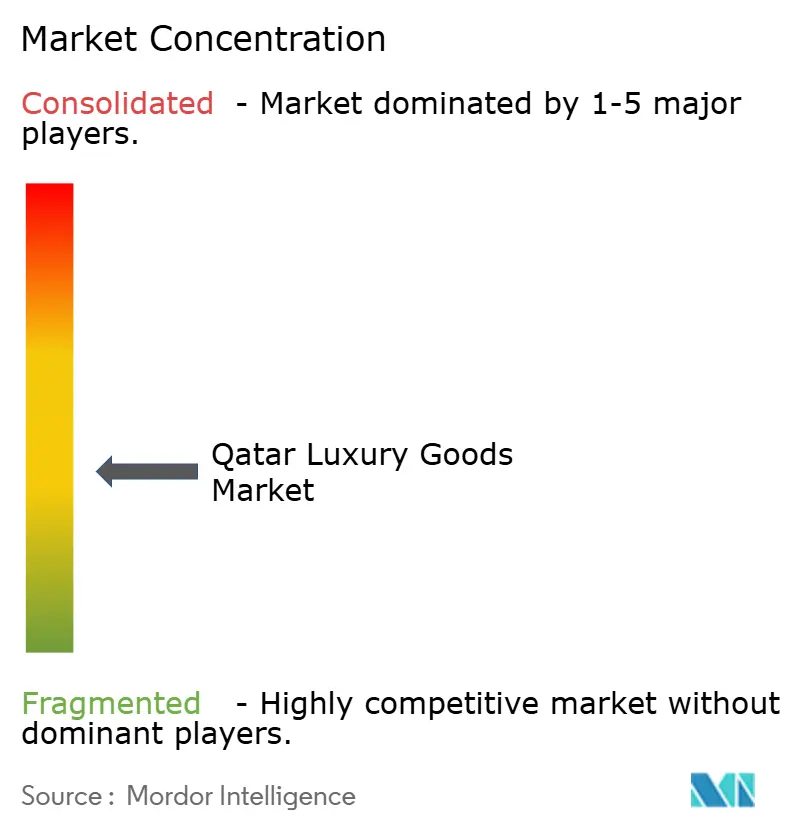

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Qatar Luxury Goods Market Analysis by Mordor Intelligence

The Qatar luxury goods market size is expected to grow from USD 1.47 billion in 2025 to USD 1.62 billion in 2026 and is forecast to reach USD 2.63 billion by 2031 at 10.15% CAGR over 2026-2031. Qatar’s post-World Cup infrastructure, a decisive move to cut business registration fees by up to 90%, and the rollout of an Integrated GCC Customs Tariff in January 2025 have triggered an influx of marquee brands and sustained retail expansion. Visitor arrivals rose 25% year-on-year to more than 5 million in 2024, reinforcing tourism’s role in channeling external demand into the Qatar luxury goods market, according to Qatar Tourism [1]Qatar Tourism, “Monthly Tourism Performance Report,” visitqatar.com. Per-capita GDP of USD 108,570 underpins the country’s purchasing power, while sovereign-backed investments in assets such as Valentino, Balmain, Harrods, and Printemps create a vertically integrated luxury ecosystem that few rivals can replicate. The market’s moderate concentration invites global players to compete, yet Qatar’s affluent consumer base preserves exclusivity and pricing power.

Key Report Takeaways

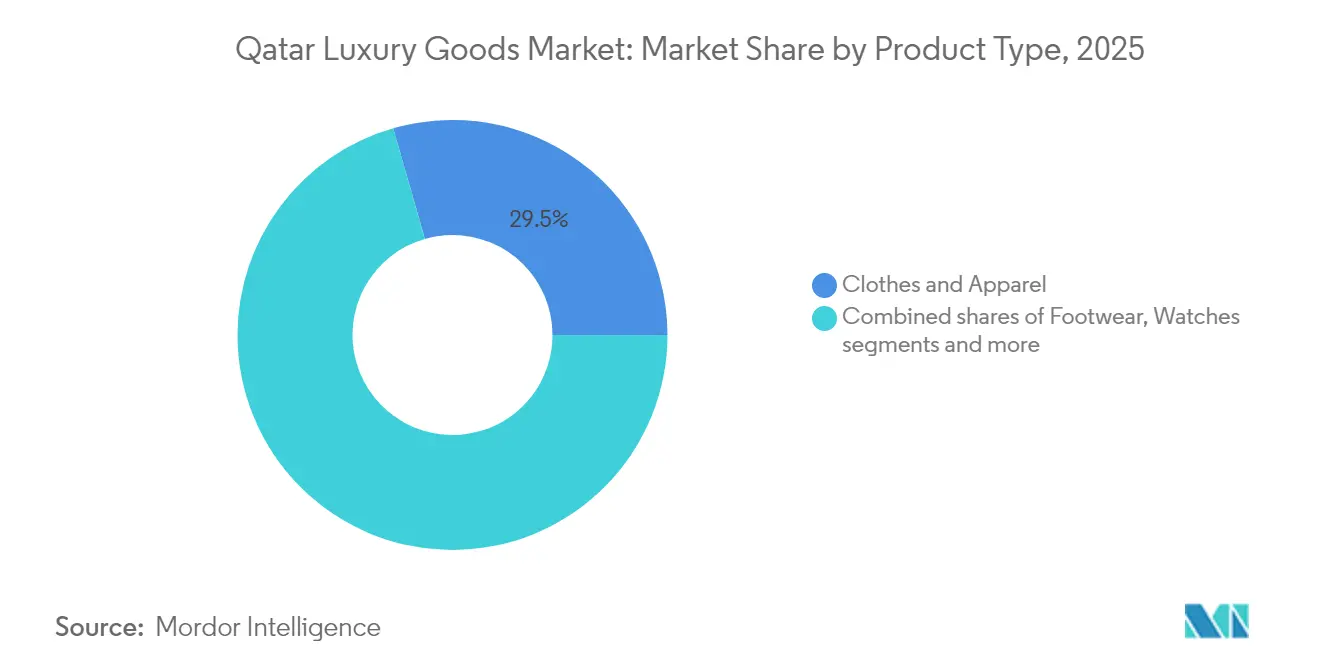

- By product type, clothing and apparel held 29.45% of the Qatar luxury goods market share in 2025; watches are projected to grow at a 10.34% CAGR to 2031.

- By end user, women commanded 56.30% share of the Qatar luxury goods market size in 2025, whereas men are poised for a 10.22% CAGR between 2026-2031.

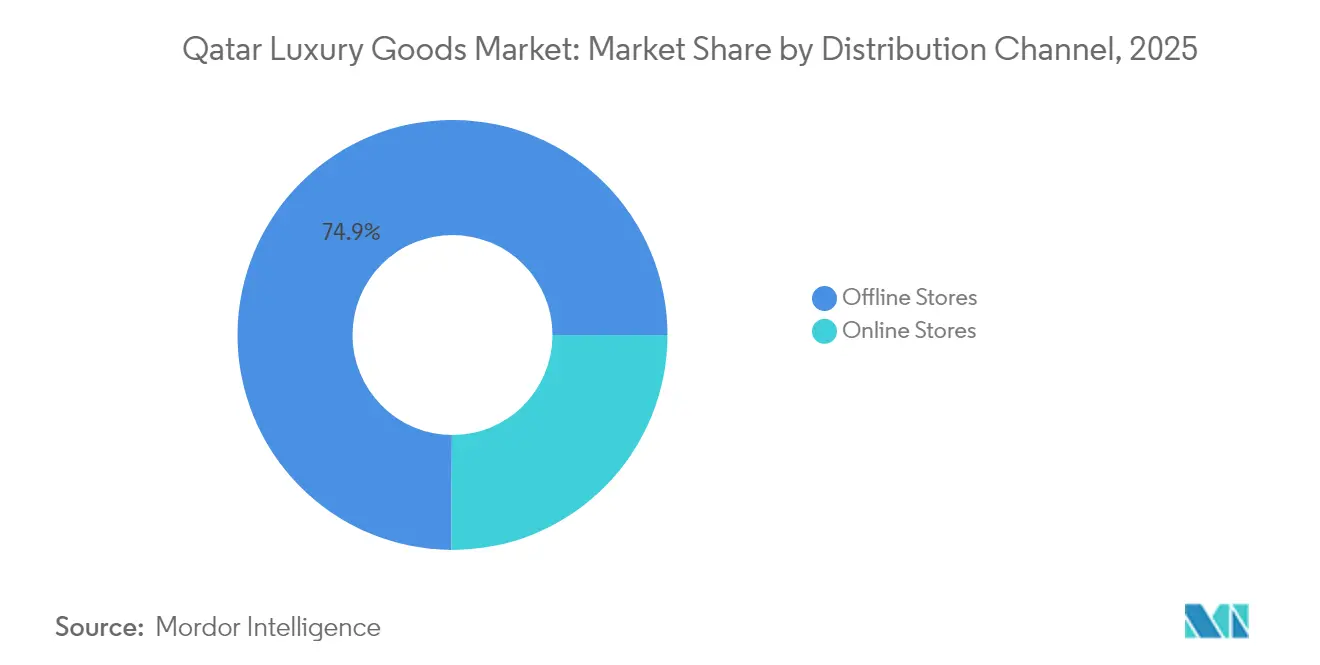

- By distribution channel, offline stores captured 74.90% of the Qatar luxury goods market in 2025, while online stores are forecast to rise at an 10.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Qatar Luxury Goods Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Strategic Investment and Initiatives Propelling the Market | +2.1% | National, with spillover to GCC | Medium term (2-4 years) |

| Aggressive Marketing by Reputed Brands | +1.8% | National, concentrated in Doha and Lusail | Short term (≤ 2 years) |

| Influence of Western Culture | +1.4% | National, urban centers primarily | Long term (≥ 4 years) |

| Consumer Emphasis on Sustainability | +0.9% | National, with early adoption in luxury segments | Medium term (2-4 years) |

| Growing Tourism Sector | +2.3% | National, with international visitor focus | Short term (≤ 2 years) |

| Digitalization and E-Commerce Growth | +1.2% | National, with mobile-first adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing strategic investment and initiatives propelling the market

Qatar's infrastructure investments and regulatory reforms have fundamentally transformed its luxury goods market. The extensive USD 200-300 billion infrastructure program, initially launched for the World Cup preparations, continues to drive substantial growth in luxury consumption through significant developments like the Simaisma coastal project, which incorporates the prestigious Trump International Golf Club and high-end luxury villas. The government's strategic decision in July 2024 to reduce business registration fees by up to 90%, significantly encourages luxury brand establishment in the market. These reduced operational costs provide Qatar's luxury retailers with substantial competitive advantages compared to other markets in the region, where establishment costs remain considerably higher. The Third National Development Strategy, with its comprehensive focus on private sector growth and foreign investment attraction, firmly positions Qatar as a key destination for international luxury brand expansion and market development.

Aggressive marketing by reputed brands

Global luxury brands are adapting their marketing strategies to align with Qatar's cultural values and affluent consumer preferences. The brands are focusing on personalized experiences and exclusive offerings that resonate with local tastes and traditions. Louis Vuitton opened its first airport lounge at Hamad International Airport in August 2024, offering a unique blend of French cuisine with local flavors. The lounge provides travelers with an immersive luxury experience, combining high-end retail with premium hospitality services. Audemars Piguet released a Qatar-specific Royal Oak timepiece featuring Eastern Arabic numerals and a burgundy Grande Tapisserie dial, reflecting the brand's commitment to regional customization. This limited edition watch incorporates design elements that appeal specifically to Qatar's luxury watch enthusiasts. The inaugural Arabia Luxury Travel Show in Doha in January 2025 drew more than 160 luxury tour operators from markets including Russia, Belarus, and Kazakhstan, reinforcing Qatar's position as a luxury tourism destination. The event showcased Qatar's luxury hospitality infrastructure and its capacity to host high-profile international events in the luxury segment.

Influence of western Culture

Western cultural influences in Qatar are reshaping luxury consumption patterns, particularly among the younger generation and expatriate population. The Place Vendôme in Lusail City exemplifies this shift through its European architectural design and premium retail offerings, featuring over 500 retail outlets across 1.5 million square feet of space. The market evolution is evident in the emergence of mixed-gender retail spaces and increased consumer preference for Western luxury brands among Qatari nationals, with international brands accounting for approximately 70% of luxury purchases. Retail destinations like AlHazm Mall combine traditional Arabian elements with European architectural features, reflecting the market's cultural fusion through its 125 high-end boutiques and restaurants. Qatar's position as a host for global luxury events, such as the Doha Jewelry and Watches Exhibition, and its development as a premium tourism destination strengthens the demand for international luxury brands and retail experiences, contributing to an annual growth rate of 15% in the luxury retail sector.

Consumer emphasis on sustainability

Qatar's luxury consumers increasingly prioritize sustainability, prompting brands to implement environmental and social responsibility programs. The partnership between Mashreq Bank and Landmark Retail in November 2024, Qatar's first private sector sustainability-linked finance initiative, demonstrates a commitment to sustainable luxury retail practices. The program focuses on renewable energy adoption, responsible sourcing, and waste reduction across Qatar retail operations. QNB Group's USD 9 billion in sustainable finance and its role in Qatar's first sovereign green bond issuance show financial sector support for luxury brands' sustainability initiatives. Qatar's younger affluent consumers view environmental responsibility as a key factor in luxury purchasing decisions. In response, luxury brands in Qatar are adopting circular economy practices, sustainable packaging, and transparent supply chain reporting to align with these consumer preferences.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of Counterfeit Products | -1.1% | National, with cross-border challenges | Medium term (2-4 years) |

| Lesser Demand from Price Sensitive Consumers | -0.8% | National, affecting mid-tier luxury segments | Short term (≤ 2 years) |

| Small Population Size | -1.3% | National, structural demographic constraint | Long term (≥ 4 years) |

| Geopolitical Instability | -0.7% | Regional, with spillover effects | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Availability of counterfeit products

Counterfeit luxury goods pose a significant challenge to Qatar's luxury market, despite strong regulations and enforcement measures. According to the OECD's 2025 report, global counterfeit trade reached USD 467 billion, representing 2.3% of total global imports [2]Organization for Economic Co-operation and Development, “Trade in Counterfeit and Pirated Goods 2025 Update,” oecd.org. The luxury goods segment, particularly clothing, footwear, and jewelry, remains susceptible to counterfeiting due to high profit margins and consumer demand. While Qatar's Ministry of Commerce and Industry implements comprehensive consumer protection and anti-fraud measures, counterfeiters continuously adapt their methods through local production facilities and small-scale shipments to evade detection. The ministry conducts regular market inspections and collaborates with customs authorities to intercept counterfeit goods at entry points. Qatar's position as a regional trade hub requires ongoing monitoring, enhanced technological solutions, and strengthened international collaboration to protect market authenticity and maintain consumer confidence. The government also focuses on consumer education programs to help buyers identify authentic products and understand the risks associated with counterfeit purchases.

Lesser demand from price sensitive consumers

Qatar's GDP per capita of USD 69.54 thousand, as reported by the International Monetary Fund, highlights the market's substantial purchasing power, yet price sensitivity exists in specific consumer segments, particularly in mid-tier luxury categories [3]International Monetary Fund, "Gross domestic product (GDP) per capita in Qatar", www.imf.org. The luxury industry faces significant pricing pressures due to rising inflation, with Qatari consumers becoming increasingly selective in their luxury purchases across various product categories. Luxury brands must carefully balance their premium positioning while ensuring market accessibility through strategic pricing and product offerings. Qatar's luxury retailers have responded by introducing comprehensive entry-level product ranges and flexible payment options to address price sensitivity without compromising brand value. The substantial expansion of pre-owned luxury goods markets and rental service platforms indicates consumers are actively seeking alternative methods to access luxury items within their budgetary constraints, reflecting a shift in luxury consumption patterns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Watches Drive Premium Innovation

Clothing and apparel hold the largest market share of 29.45% in Qatar's luxury goods market in 2025, driven by demand for occasion wear and premium tailoring. The segment's dominance reflects Qatar's strong fashion consciousness and cultural emphasis on formal attire. International luxury brands maintain a significant presence through high-end boutiques in premium shopping destinations, while local luxury fashion houses cater to traditional dress preferences with bespoke services. The market benefits from Qatar's position as a regional fashion hub, attracting both local and international designers. The segment's growth is supported by regular fashion events and exhibitions that showcase luxury collections. Additionally, the increasing number of high-net-worth individuals and expatriates contributes to the sustained demand for luxury clothing and apparel.

The watch segment is projected to grow at a CAGR of 10.34% through 2031. The market expansion is supported by increasing consumer perception of luxury timepieces as both status symbols and investments. Regional exclusives, such as the Qatar-specific Royal Oak, demonstrate the effectiveness of market-specific offerings. The growth is further strengthened by the expansion of authorized dealers and growing collector communities. The segment benefits from rising interest in limited-edition timepieces among young professionals and watch enthusiasts. The market is also bolstered by Qatar's position as a luxury retail destination, attracting international watch collectors and enthusiasts. The jewelry segment draws strength from Doha’s growing role as a precious-stone trading hub, underscored by the January 2025 diamond and gemstone showcase. Footwear and eyewear gain from rising outdoor leisure trends, while leather goods align with the resurgence of international business travel via Hamad International Airport. Beauty and personal care see steady uptake among a youthful, wellness-focused consumer base.

By End User: Women Lead the Market Growth

In 2025, women accounted for 56.30% of Qatar's luxury goods market, with strong preferences in fashion, jewelry, and beauty segments. This dominance reflects women's significant purchasing power and their role as primary decision-makers in luxury consumption. Female consumers show particular interest in high-end designer clothing, premium cosmetics, and fine jewelry collections. The market has responded with expanded product lines specifically targeting female preferences, including limited-edition releases and personalized shopping experiences. Traditional luxury houses have strengthened their presence in Qatar's female-oriented market through exclusive collections and VIP services. Additionally, digital marketing strategies increasingly focus on female consumers, offering virtual try-ons and personalized recommendations.

The men's segment is projected to grow at a 10.22% CAGR through 2031. This growth stems from global menswear trends, increased business travel, and evolving masculinity perceptions in the Gulf region, resulting in higher expenditure on grooming products, fashion items, and luxury watches. Male consumers are showing increased interest in premium grooming services, bespoke tailoring, and high-end accessories. The market has witnessed a surge in male-focused luxury boutiques and specialized retail experiences. Luxury brands are expanding their men's collections to include diverse product categories beyond traditional offerings. The rise of male influencers and fashion-conscious professionals has further accelerated this growth trend. The unisex category continues to expand, particularly through gender-neutral fragrances and accessories, appealing to younger consumers seeking versatility. This segment's growth aligns with changing social attitudes and increased demand for inclusive luxury offerings.

By Distribution Channel: Digital Transformation Accelerates

In 2025, physical retail stores hold a 74.90% market share in Qatar's luxury market, reflecting consumers' strong preference for tangible product experiences, personalized service interactions, and detailed product evaluations. The country's luxury retail infrastructure includes prominent locations such as Place Vendôme, which houses over 500 retail outlets, AlHazm Mall's distinctive architectural design with premium boutiques, and Lusail City's extensive retail developments spanning multiple districts, which provide established platforms for luxury brands. The market's expansion is supported by increased investments in digital capabilities, including advanced virtual try-on features with 3D modeling, personalized online services with AI-driven recommendations, and integrated omnichannel strategies that seamlessly connect online and offline experiences.

The online stores segment is projected to grow at a 10.88% CAGR through 2031. The growing digital presence has influenced consumer purchasing patterns, contributing to increased online luxury sales through mobile applications, social commerce, and dedicated e-commerce platforms. However, the online channel faces specific challenges, including product authenticity concerns in the secondary market, verification of materials and craftsmanship, and replicating the traditional luxury shopping experience. In response, luxury brands are implementing blockchain-based authentication technologies, strengthening consumer awareness about genuine products through digital certificates and tracking systems, and developing immersive digital tools such as augmented reality and virtual showrooms to enhance the online shopping experience. These market conditions require continuous adaptation of digital strategies by luxury brands, including regular updates to user interfaces, security protocols, and customer engagement methods.

Geography Analysis

Qatar's luxury goods market operates within a unique geographic context that leverages the nation's strategic position as a regional hub while serving both domestic and international consumer bases. Doha Municipality holds 59.60% of the market share in 2025. The geographic concentration of luxury retail in Doha and the emerging Lusail City creates critical mass for luxury brand operations while serving the broader GCC market through tourism and cross-border shopping. The nation's hosting of 5 million tourists in 2024, representing 25% year-on-year growth, demonstrates its increasing appeal as a luxury destination, according to Qatar Tourism.

The geographic dynamics are further enhanced by Qatar's successful post-World Cup transformation, which created world-class infrastructure supporting luxury retail operations. The development of integrated luxury ecosystems like Place Vendôme in Lusail City and the expansion of Hamad International Airport's luxury retail offerings position Qatar as a regional luxury hub. Qatar's strategic location enables efficient access to key source markets, with Saudi Arabia, India, the UK, Germany, and the USA representing primary visitor origins.

Al Wakrah region registers the highest CAGR with 10.33% during the forecast period. Regional integration opportunities continue expanding through Qatar's participation in the GCC luxury market development and its strategic investments in global luxury assets. Qatar's sovereign wealth fund, Mayhoola's ownership of prestigious brands including Valentino, Balmain, Harrods, and Printemps creates unique synergies between Qatar's domestic market and global luxury operations. The geographic positioning enables Qatar to serve as both a luxury consumption destination and a strategic investment platform for global luxury expansion. The nation's commitment to tourism growth, targeting 6 million visitors by 2030 and increasing tourism's GDP contribution to 10-12%, reinforces its geographic advantages in the luxury sector, according to Qatar Tourism.

Regulatory Landscape

Qatar luxury goods imports and retailing operate under a multi-agency framework. The General Authority of Customs (GAC) oversees border procedures and duty collection, while the Ministry of Commerce and Industry (MOCI) manages in-market control, consumer protection, and enforcement through its Quality License and Market Control Department. Importers are required to follow unified importation procedures and Customs Law No. 40 of 2002, using the Al-Nadeeb automated clearance system for declarations and release processes.

Technical compliance and product eligibility are shaped by the Qatar General Organization for Standardization (QS), which issues Qatari standards and technical regulations that often align with Gulf Standards Organization (GSO) requirements. For regulated product categories, the Product Conformity Assessment (PCA) program requires a Certificate of Conformity (CoC) prior to shipment, which makes pre-shipment documentation a practical gate for customs release. Qatar also prohibits goods that infringe intellectual property rights or violate applicable standards, reinforcing the need for authenticated supply chains for luxury apparel, jewelry, watches, and accessories.

Competitive Landscape

Qatar's luxury goods market demonstrates moderate fragmentation, featuring global luxury conglomerates alongside regional players and local brands. International companies such as LVMH, Chanel, and Richemont maintain strong positions in the high-end segment through their established brand heritage and global supply chains. The market structure allows for healthy competition while maintaining high standards of luxury retail offerings across various product categories.

Digital transformation and sustainability initiatives shape market dynamics, with companies implementing AI and blockchain technologies for authentication and personalized services. These technological advancements enable brands to enhance inventory management, reduce counterfeiting, and deliver customized shopping experiences. The market competition intensifies through omnichannel retail strategies and social media partnerships, notably with regional influencers like Haneen Alsaify.

Companies leverage digital platforms to reach younger consumers while maintaining traditional retail excellence. Companies that incorporate sustainable and ethical practices into their operations gain advantages as consumer awareness of these issues increases. This includes initiatives in responsible sourcing, waste reduction, and transparent supply chain management, which resonate particularly well with Qatar's environmentally conscious luxury consumers.

Qatar Luxury Goods Industry Leaders

-

LVMH Moët Hennessy Louis Vuitton SE

-

Kering SA

-

Richemont SA

-

Chanel SA

-

Rolex SA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Destination development in Lusail is widening room for luxury retail clusters beyond established hubs in Doha. In June 2026, Qatar Museums and Lusail Real Estate Development Company unveiled the Al Maha Island masterplan in Lusail, combining a Herzog & de Meuron-designed museum with a contemporary souk and luxury boutique residential zones. In July 2026, Parsons received a three-year program and construction management contract for the Lusail City Infrastructure Program covering 38 square kilometers of mixed-use districts. Together, these projects expand the pipeline of premium footfall locations that luxury brands, department stores, and travel retail operators can use for experiential formats.

Digital-led clienteling and trust infrastructure are another focus as shoppers increasingly move between discovery and purchase across channels. A June 2026 Visa consumer study reported that 90% of consumers in Qatar use AI-powered technologies in their shopping journeys, which supports investments in personalization, omnichannel appointment booking, and authenticated product data across online-to-offline journeys. The same market conditions also point to continued spend on provenance and compliance tooling for high-value categories, particularly watches and jewelry, as retailers work to reduce counterfeit risk while supporting documentation needs and after-sales services across established venues such as Place Vendome, Printemps Doha, and Hamad International Airport retail.

Recent Industry Developments

- May 2026: Al Majed Jewellery introduced Gerald Genta and Daniel Roth to its Doha retail offering, widening access to niche high-watchmaking brands in Qatar. The expansion supports curated multi-brand retailing for mechanical timepieces and lifts emphasis on specialist in-store storytelling and after-sales capabilities.

- May 2026: Place Vendome in Lusail opened HOKA's first standalone store in Qatar. The entry expands the premium footwear mix inside a flagship luxury mall and underscores how destination retail hubs are using brand-first country debuts to diversify traffic and capture lifestyle-led luxury spend.

- March 2025: Doha Oasis acquired Ever Fashion Luxury Group, adding a portfolio of more than 26 international fashion brands, including Jimmy Choo and Dolce & Gabbana, into its retail mix. The acquisition consolidates brand distribution under a destination operator and improves negotiating leverage on tenanting, merchandising, and cross-brand activation in Qatar's luxury ecosystem.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Qatar luxury goods market is defined as consumer spending on premium, branded discretionary products sold at luxury price points through offline retail and online channels within Qatar.

Scope exclusions: We exclude mass-market premium brands, second-hand resale-only transactions, and informal gray-market imports that do not pass through reported retail or authorized distribution.

Segmentation Overview

-

By Product Type

- Clothing and Apparel

- Footwear

- Eyewear

- Leather Goods

- Jewelry

- Watches

- Beauty and Personal Care

-

By End User

- Men

- Women

- Unisex

-

By Distribution Channel

- Offline Stores

- Online Stores

-

By Geography

- Doha Municipality

- Al Rayyan

- Al Wakrah

- Other Municipalities

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the basic demand context and to set realistic boundaries for what can be counted as luxury spending in Qatar. We referred to public sources such as Qatar Planning and Statistics Authority releases, Qatar Central Bank data on inflation and consumption indicators, UN Comtrade trade statistics, and International Monetary Fund macro series to align growth drivers with the timeline.

To convert context into workable sizing inputs, we also reviewed import trends for high-value consumer categories, airport and tourism statistics published by official entities, and public retail developments reported through association websites and reputed press. Company annual reports, filings, and investor presentations were used to sanity-check channel mix and the direction of pricing. Where needed, we also used paid subscriptions for company financials and intelligence, news and financials, and shipment-level trade data to validate directionally, not to replace primary checks. These source examples are not exhaustive, and many other references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary inputs were gathered through expert interviews and structured surveys across retailers, distributors, brand-side roles, and category specialists who understand luxury demand and pricing behavior in Qatar. We covered viewpoints tied to the key buying pools in the country, and we used these conversations to confirm category boundaries, channel splits, and the pace of price increases (including the effect of promotions and launches).

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 16% | |

| Mid tier: 43% | Functional/Unit leaders: 33% | |

| Smaller Players: 22% | Managers: 51% |

Market-Sizing & Forecasting

Market sizing used a top-down approach where Qatar-level demand was reconstructed using a spend pool view and then filtered through luxury-eligible categories, channels, and buyer cohorts. Once the totals were built, we corroborated them with selective bottom-up approximations using sampled store count checks, category-level price banding, and volume proxies where they were available.

Inputs that shaped the model included high-income population and visitor flows, retail footprint additions in premium malls, import value movement for relevant goods, price inflation and exchange-rate timing for converted values, and online penetration for luxury shopping. Where a data gap existed for a narrow niche, the assumption was set using adjacent category ratios confirmed in interviews, and then stress-tested so it stayed consistent with the overall spending envelope.

For forecasting, scenario analysis was used, since luxury demand in Qatar can move quickly with tourism cycles and retail launches, and experts helped us pick realistic ranges for price progression and category mix. The final forecast path was kept traceable to these drivers so the steps can be repeated and updated with new signals.

Data Validation & Update Cycle

Validation was handled through multiple checks that compare the model outputs against independent signals, and we revisited assumptions when the numbers drifted from what the market can practically absorb. Outliers were flagged at category and channel level, then reviewed by another analyst before sign-off so arithmetic and logic errors are not carried forward.

The report is refreshed annually, and interim updates are triggered when material events change demand drivers, pricing, or import behavior. Before delivery, a fresh review pass is completed so clients receive the most current view supported by the latest available public indicators and re-checks with primary contacts.

Mordor Intelligence's Qatar Luxury Goods Market Size Compared With Other Published Estimates

Published market values for Qatar luxury goods can look far apart because the market is small enough that a single scope choice can shift the total meaningfully. We see the biggest differences coming from what is counted as luxury, the year used as the base, and how pricing and currency timing are handled.

Key gap drivers tend to show up when some estimates bundle in adjacent big-ticket categories, or when they use aggressive price escalation without checking it against retail realities. Import signals, visitor-spend direction, and offline store activity are the checks that keep Mordor Intelligence's estimate tied to personal luxury categories actually sold through measured retail channels in Qatar.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.47 B (2025) | |

| Global Consultancy A | USD 2.10 B (2024) | Uses an earlier base year and a broader basket that explicitly includes high-end vehicles, which can lift the total beyond personal luxury goods retail. |

| Industry Publisher B | USD 1.20 B (2024) | Applies a narrower interpretation centered on select categories and channels, and may understate price progression and premium retail expansion in the base-year build. |

Across the three numbers, the spread is explained mainly by category boundaries and base-year alignment, followed by how pricing and currency timing are treated. By keeping the model tied to observable demand signals and clear inclusion rules, we end up with a practical estimate that can be updated the same way each year.

Key Questions Answered in the Report

What is the current value of the Qatar luxury goods market?

The market is valued at USD 1.62 billion in 2026 and is projected to reach USD 2.63 billion by 2031.

Which product segment is growing the fastest?

Watches display the strongest momentum with a 10.34% CAGR forecast for 2026-2031.

How dominant are offline stores versus online channels?

Offline outlets captured 74.90% of sales in 2025, but online stores are rising quickly at an 10.88% CAGR.

Why are men the fastest-growing customer group?

Changing cultural norms, higher business travel, and greater exposure to global fashion are driving male consumption at a 10.22% CAGR.

Page last updated on: