Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

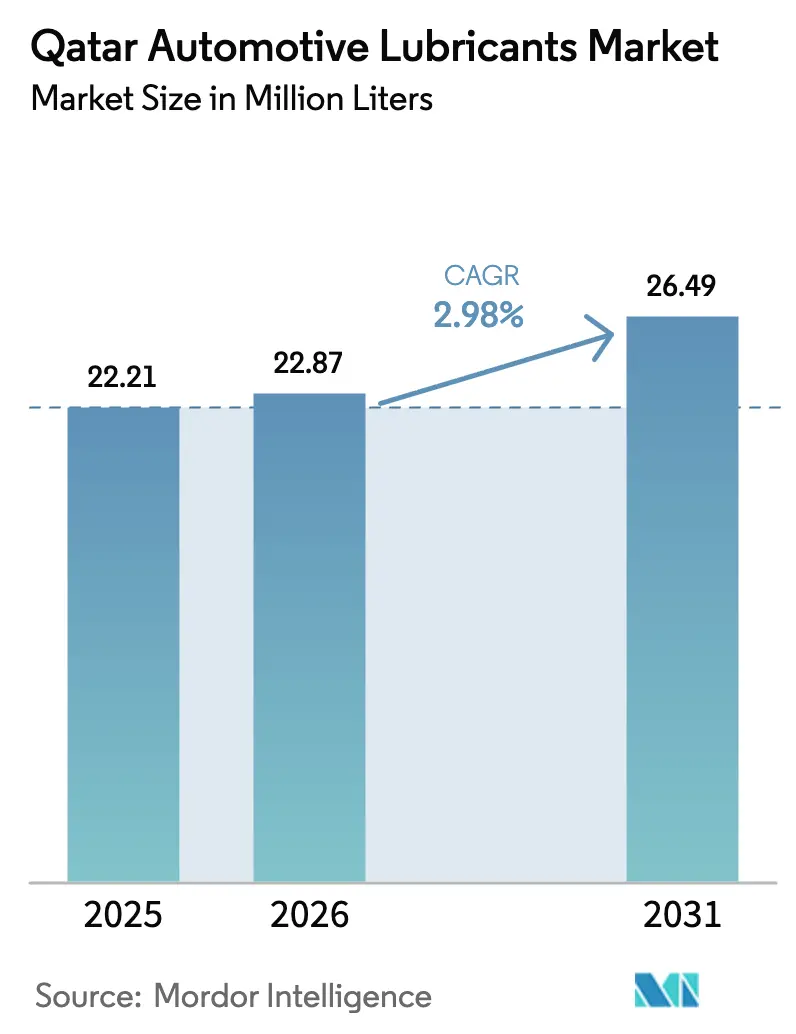

| Base Year Market Size (2025) | 22.21 Million liters |

| Market Volume (2026) | 22.87 Million liters |

| Market Volume (2031) | 26.49 Million liters |

| Growth Rate (2026 - 2031) | 2.98% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Qatar Automotive Lubricants Market Analysis by Mordor Intelligence

The Qatar Automotive Lubricants Market size is expected to grow from 22.21 Million liters in 2025 to 22.87 Million liters in 2026 and is forecast to reach 26.49 Million liters by 2031 at 2.98% CAGR over 2026-2031. Robust new-vehicle registrations in 2024, a premiumization shift toward fully synthetic grades, and a domestic supply of gas-to-liquids (GTL) base oil from Pearl GTL keep volumes expanding even as longer drain intervals curb per-vehicle consumption. Automatic transmission adoption, extreme-heat operating conditions, and public-bus electrification targets are reshaping product-mix priorities for suppliers seeking higher-margin niches. Construction, logistics, and oil-and-gas projects continue to enlarge the commercial-vehicle fleet, sustaining heavy-duty demand despite cyclical construction spending. Meanwhile, additive import dependence, predictive-maintenance tools, and the gradual rise of e-fluids serve as structural brakes on bulk-volume growth, forcing market participants to pivot toward solution-based offerings.

Key Report Takeaways

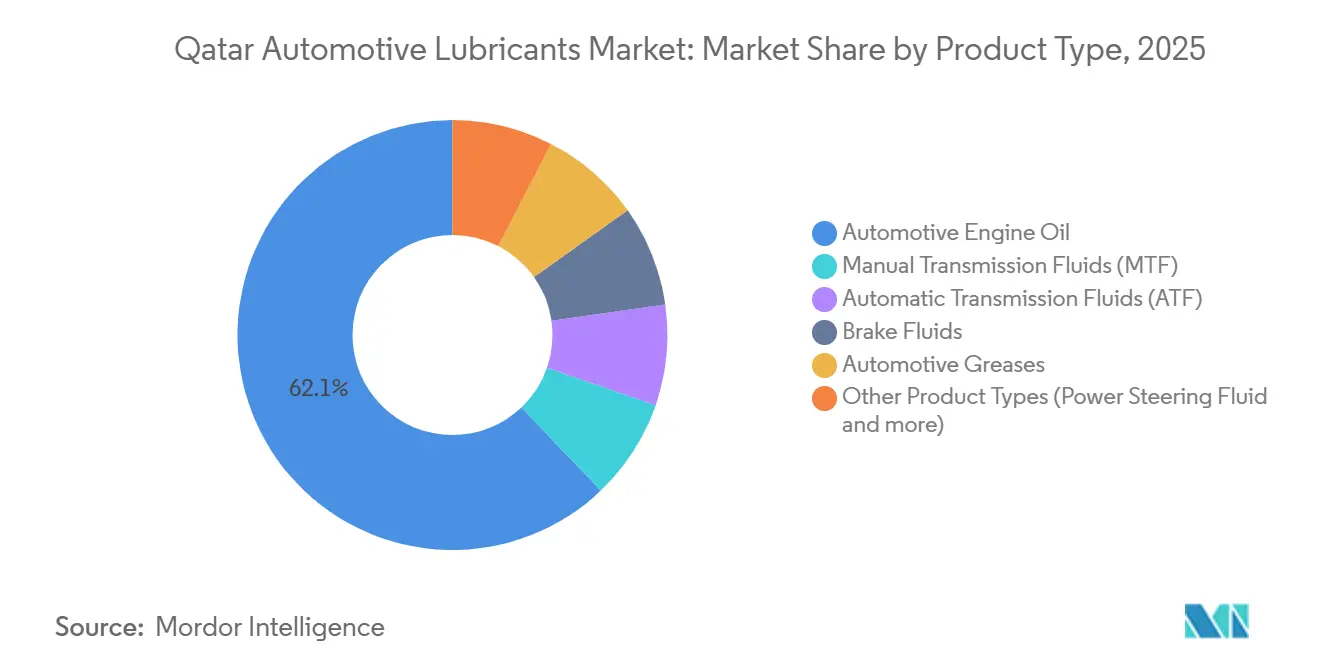

- By product type, engine oil led with 62.12% share of the Qatar automotive lubricants market in 2025, while automatic transmission fluids are forecast to grow at a 3.34% CAGR through 2031.

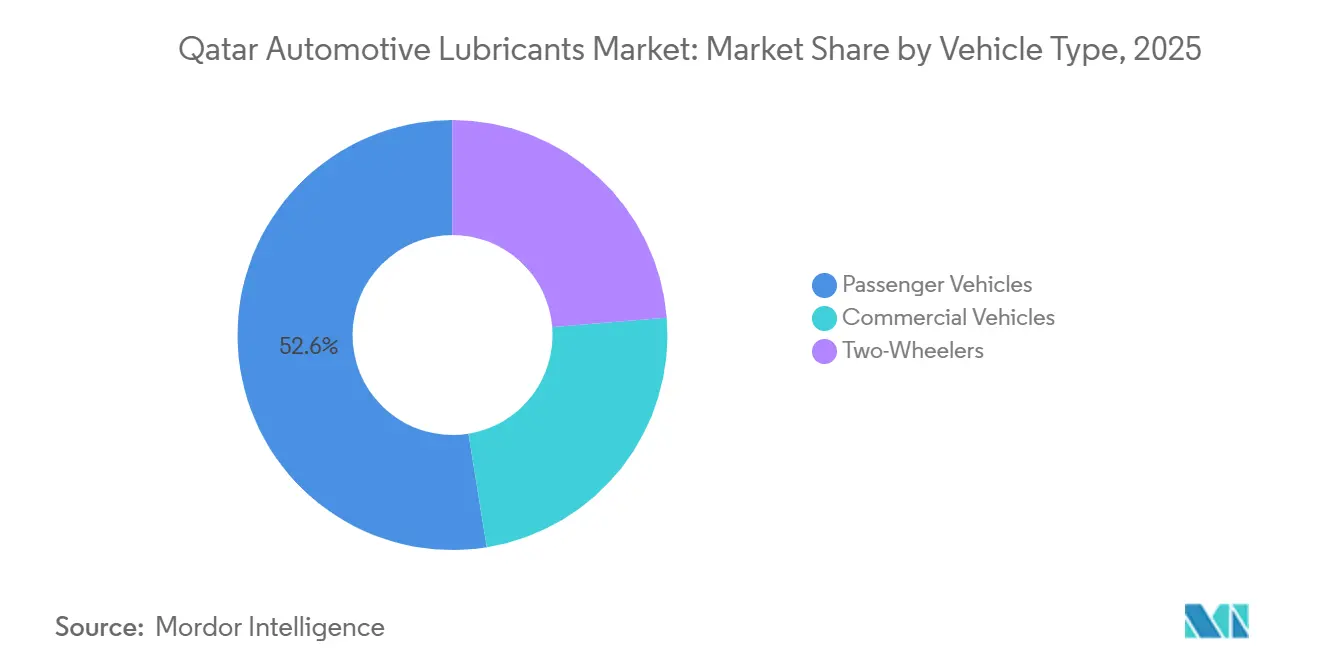

- By vehicle type, passenger cars held 52.55% of the Qatar automotive lubricants market share in 2025, while two-wheelers are advancing at a 3.56% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Qatar Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of passenger-car parc post-FIFA 2022 and infrastructure boom | +0.8% | National, concentrated in Doha, Al Khor, Lusail, Ras Laffan | Medium term (2-4 years) |

| Construction and logistics projects fuelling commercial-fleet lubricant demand | +0.7% | National, with industrial zones in Central/Northern Qatar and Al Shaheen oil & gas expansion in South | Medium term (2-4 years) |

| Heat-resistant synthetic-oil adoption in extreme climate | +0.5% | National, heightened in coastal and industrial areas experiencing >45°C peaks | Long term (≥ 4 years) |

| GTL base-oil availability from Pearl plant lowering input costs | +0.4% | National production, regional export spillover to GCC | Long term (≥ 4 years) |

| EV-specific e-fluid niches emerging from Qatar e-mobility targets | +0.2% | National, early adoption in public transport (buses), gradual private-vehicle penetration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heat-Resistant Synthetic-Oil Adoption in Extreme Climate

Qatar logs 107 days annually above 40°C, creating thermal stress that degrades conventional lubricants and accelerates oxidation. Fleet owners increasingly select fully synthetic 0W-20 and 5W-30 grades that sustain viscosity at elevated temperatures, boosting low-viscosity penetration by 15% year on year. Shell’s GTL-derived PurePlus base oils and TotalEnergies’ Quartz series address this need with higher viscosity indices and low volatility, allowing drain extensions without engine-wear penalties. Government adaptation plans that emphasize infrastructure resilience add urgency to premium-grade adoption, and distributors position long-life synthetics as a total-cost-of-ownership play for private and fleet users. The widespread shift raises average revenue per liter, yet it simultaneously reduces total liters sold per vehicle. Suppliers therefore combine product upgrades with value-added services such as oil-analysis programs to protect margins.

Expansion of Passenger-Car Parc Post-FIFA 2022 and Infrastructure Boom

Vehicle registrations in the first eight months of 2024 reached 62,163 units, up 13.7% from the same period in 2023, with private cars making up more than 70% of the total. Stadiums, highways, and urban-connectivity projects completed for the FIFA World Cup keep mobility demand elevated, especially in Doha and Lusail. Rising GDP per capita and an expanding population drive luxury-vehicle sales, which now represent about one-third of new registrations and require OEM-approved synthetic lubricants. The Ministry of Transport’s Freight Master Plan also encourages larger commercial fleets, linking ground freight with air and sea modes through 2050. Seasonal registration spikes in May and August provide predictable retail peaks that service centers can use to optimize inventory and promotions.

Construction and Logistics Projects Fuelling Commercial-Fleet Demand

Hamad Port expansions, airport-cargo growth, and North Field LNG developments pushed the logistics market from USD 9.5 billion in 2024 toward a projected USD 13.49 billion by 2030, advancing at a 6.01% CAGR. Industrial-vehicle counts rose 45% over the previous three years, and construction-equipment registrations increased 28% between 2022 and 2023, sustaining heavy-duty lubricant demand. Caltex’s multi-year supply agreement with UrbaCon Trading & Contracting highlights the importance of fleet contracts, while public tenders from Qatar Primary Materials Company illustrate ongoing lubricant procurement for large earth-moving assets. The national development strategy targets 4% annual non-hydrocarbon GDP growth, ensuring a pipeline of infrastructure and logistics projects that anchor commercial-vehicle lubricant volumes.

GTL Base-Oil Availability from Pearl Plant Lowering Input Costs

Shell’s Pearl GTL complex produces about 30,000 barrels per day of Group III base oil that displays 99.5% purity and a high viscosity index, enabling ultra-low-viscosity formulations such as 0W-16. Woqod blends the locally marketed OTO range with this feedstock, offering premium quality at competitive prices through a broad retail network. A 20-year naphtha-supply contract signed in 2024 ensures long-term feedstock security for downstream petrochemicals and lubricants, reinforcing Qatar’s regional export advantage. Stable domestic supply lowers transport costs and buffers local blenders against global freight volatility, supporting price competitiveness and higher gross margins.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extended drain intervals curbing per-vehicle oil volumes | -0.6% | National, accelerated in luxury and fleet segments adopting synthetic oils | Medium term (2-4 years) |

| High additive import dependence driving price volatility | -0.3% | National, affecting all blenders and distributors | Short term (≤ 2 years) |

| Predictive-maintenance digital tools cutting over-lubrication | -0.2% | National, concentrated in commercial fleets and logistics operators | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Extended Drain Intervals Curbing Per-Vehicle Oil Volumes

Synthetic lubricants meeting GF-6 and API SP standards now support 7,500- to 10,000-mile oil-change intervals, shrinking per-vehicle consumption by up to 60%. Luxury-vehicle owners adopt these products fastest, encouraged by OEM service packages that emphasize fewer visits and lower lifetime maintenance costs. Shell and TotalEnergies both promote long-life ranges that comply with Euro 5 emission controls, yet longer intervals reduce overall volume growth even as average selling prices rise. Blenders respond with premium add-on services, oil analysis, warranty extensions, and fleet contracts, to preserve revenue streams. The net effect is slower liter growth despite healthy revenue yields per unit of lubricant sold.

High Additive Import Dependence Driving Price Volatility

More than 85% of lubricant additives consumed in Qatar come from overseas suppliers, exposing blenders to freight spikes and currency swings. Domestic refinery throughput of 337,000 barrels per day in 2024 meets fuel needs but does not generate significant additive intermediates. QALCO must therefore hedge supply contracts and build safety stocks to avoid shortages, passing extra costs through to distributors during tight markets. Headline consumer inflation moderated to 2.5% in late 2023, yet petrochemical input costs remain volatile, especially as freight rates fluctuate. Suppliers with local GTL feedstock and flexible blending recipes hold a cost advantage in this environment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine Oil Dominance Meets ATF Acceleration

Automotive engine oil accounted for 62.12% of the Qatar automotive lubricants market in 2025, supported by strong passenger-car uptake of 0W-20 and 5W-30 synthetics and commercial-fleet reliance on 15W-40 multigrades[1]Gulf Times, “Automatic Transmission Fluids Outpace Market,” gulf-times.com. Automatic transmission fluids are forecast to grow at 3.34% per year, outpacing the broader market as automatic transmissions become standard in new light-duty and even heavy-duty vehicles. Caltex, Shell, and TotalEnergies have tailored multi-vehicle ATF formulations that meet OEM specifications across stepped automatics, CVTs, and dual-clutch systems, capturing higher margins per liter thanks to specialized additive packages.

Growth in ATF demand reflects driver-comfort priorities and fleet-management economics. Luxury-car imports, a sizable share of new registrations, arrive almost exclusively with automatic gearboxes that require advanced low-viscosity, anti-shudder fluids. In parallel, logistics firms favor automatic trucks to reduce driver fatigue and improve fuel efficiency, further tilting volumes toward ATF. While brake fluid and manual-transmission fluid remain stable niches, suppliers continue to expand coolant and grease lines to capture ancillary workshop spend, especially as extended drain intervals compress engine-oil turnover.

By Vehicle Type: Passenger Cars Lead, Two-Wheelers Sprint

Passenger cars held 52.55% of the Qatar automotive lubricants market share in 2025, buoyed by an ownership density of 627 cars per 1,000 residents in Doha and adjacent industrial zones. Despite extended drain intervals, volume growth remains intact as total registrations climb and luxury-car owners opt for premium synthetics blended with GTL base oils. The Qatar automotive lubricants market size attributable to private-car servicing is forecast to rise modestly through 2031, though per-vehicle liters consumed will trend lower. Two-wheelers are projected to grow at 3.56% CAGR, the fastest of all vehicle classes, as last-mile delivery services and cost-conscious expatriate commuters select motorcycles and scooters[2]QatarDay, “Two-Wheelers Gain Ground in Delivery Sector,” qatarday.com.

Commercial-vehicle lubricants also benefit from construction and logistics activity, but rising digital-maintenance adoption will temper per-asset consumption. Heavy-duty engine-oil suppliers highlight formulations that manage soot and maintain total base number (TBN) under Euro 5 diesel regulations. Meanwhile, motorcycle-oil brands such as FUCHS Silkolene tailor 4-stroke and 2-stroke lines to the hot local climate, and distributors encourage bulk purchase programs for delivery-fleet operators that conduct high-frequency oil changes. Ministry-led smart-mobility initiatives could further accelerate two-wheeler adoption by easing congestion in urban corridors, extending the segment’s above-average growth run.

Geography Analysis

Doha, Al Khor, Lusail, and Ras Laffan together host more than 65% of industrial licenses and vehicle ownership, making them the epicenter of lubricant demand. The post-FIFA infrastructure legacy concentrated highways, metro extensions, and service centers in these urban hubs, producing heightened lubricant sales throughout 2024 and 2025. Southern districts anchored by the Al Shaheen oil-and-gas field now rank as the fastest-growing corridor, spurred by industrial-vehicle additions linked to LNG expansion and energy-sector developments. Ras Laffan’s Pearl GTL plant provides a local base-oil stream, giving Qatar a rare cost advantage over regional neighbors that rely on imports.

Regulatory alignment with Gulf Cooperation Council standards simplifies cross-border trade; Euro 5 diesel limits and the GSO 1785-2:2023 standard require ACEA oil sequences, effectively lifting the performance bar and squeezing lower-tier imports. Invest Qatar offers logistics incentives covering up to 40% of qualified capital spending for projects exceeding QAR 25 million, positioning Qatar as a re-export platform for premium lubricants destined for other GCC markets. The TASMU Smart Qatar initiative seeks to halve import costs and raise logistics’ GDP contribution to 10%, which would further reduce distribution expenses for lubricant enterprises. A 20-year naphtha-supply accord between QatarEnergy and Shell deepens downstream integration, supporting local availability of petrochemical intermediates essential for lubricant blending.

Competitive Landscape

The Qatar Automotive Lubricants market is moderately consolidated, with ExxonMobil and FUCHS competing with homegrown QALCO and regional supplier ENOC. Shell leverages Pearl GTL’s output to co-brand the OTO range with Woqod, distributing through a nationwide service-station network. TotalEnergies extended an exclusive supply pact with Q-Auto, covering Audi, Volkswagen, and Skoda service centers until 2028, locking in premium-grade volumes for the luxury segment. Suppliers are now vying to bundle telematics, predictive analytics, and e-fluid portfolios as differentiators, anticipating rising EV penetration.

Qatar Automotive Lubricants Industry Leaders

ExxonMobil Corporation

Qatar Lubricants Company (QALCO)

TotalEnergies

Shell plc

BP p.l.c.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: TotalEnergies Marketing Qatar and Q-Auto, a provider of mobility solutions and dealer of automotive brands in Qatar, renewed their partnership for the exclusive supply of premium automotive lubricants in Qatar until 2028. The collaboration ensures that Quartz premium engine oils by TotalEnergies will continue to be used exclusively across Q-Auto’s after-sales service network.

- February 2024: Qatol has partnered with Q-Tire, merging Q-Tire's tire services with Qatol's range of automotive lubricants. This collaboration is set to enhance the sales of Qatol's products, including heavy-duty engine oils, transmission fluids, and brake fluids, leveraging Q-Tire's vast network throughout Qatar.

Qatar Automotive Lubricants Market Report Scope

Automotive lubricants, encompassing motor oils, transmission fluids, and greases, play a crucial role in enhancing vehicle longevity and performance. These vital fluids and greases not only reduce friction, wear, and heat between moving engine and transmission parts but also clean, cool, and prevent corrosion.

The market is segmented based on product type and vehicle type. The market is segmented by product type into automotive engine oil, manual transmission fluids (MTF), automatic transmission fluids (ATF), brake fluids, automotive greases, and other product types (power steering fluid and more). By vehicle type, the market is segmented into passenger vehicles, commercial vehicles, and two-wheelers. The market sizing and forecasts for each segment are based on volume (liters).

By Product Type

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids (MTF) | |

| Automatic Transmission Fluids (ATF) | |

| Brake Fluids | |

| Automotive Greases | |

| Other Product Types (Power Steering Fluid etc.) |

By Vehicle Type

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids (MTF) | ||

| Automatic Transmission Fluids (ATF) | ||

| Brake Fluids | ||

| Automotive Greases | ||

| Other Product Types (Power Steering Fluid etc.) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers |

Key Questions Answered in the Report

How large is the Qatar automotive lubricants market in 2026?

The Qatar automotive lubricants market size is 22.87 million liters in 2026, on its way to 26.49 million liters by 2031.

What CAGR is forecast for automotive lubricants demand in Qatar?

Volume demand is projected to rise at a 2.98% CAGR between 2026 and 2031.

Which product type holds the largest share of lubricant volumes?

Engine oil leads with 62.12% of total volume in 2025.

Which segment is growing fastest in Qatar’s lubricant market?

Automatic transmission fluids are expanding at 3.34% CAGR through 2031.

How will electrification influence lubricant demand?

Public-bus electrification and rising EV sales will lower engine-oil volumes but create new demand for dedicated e-fluids such as battery-cooling liquids.

Page last updated on: