Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

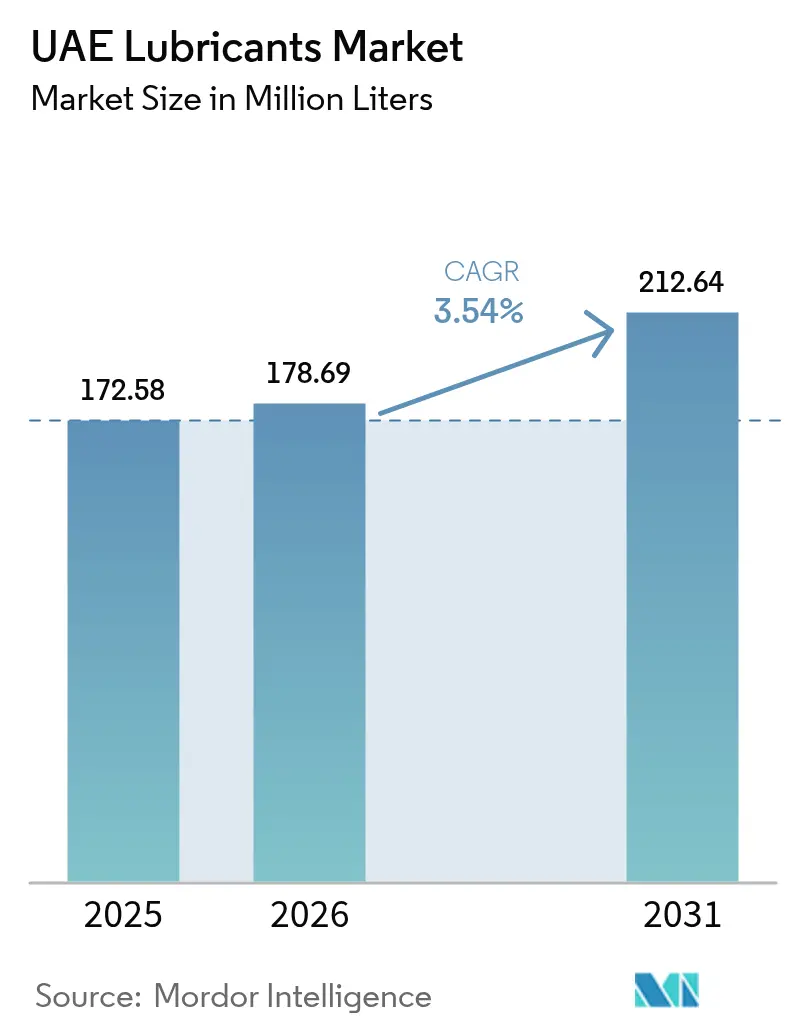

| Base Year Market Size (2025) | 172.58 Million liters |

| Market Volume (2026) | 178.69 Million liters |

| Market Volume (2031) | 212.64 Million liters |

| Growth Rate (2026 - 2031) | 3.54% CAGR |

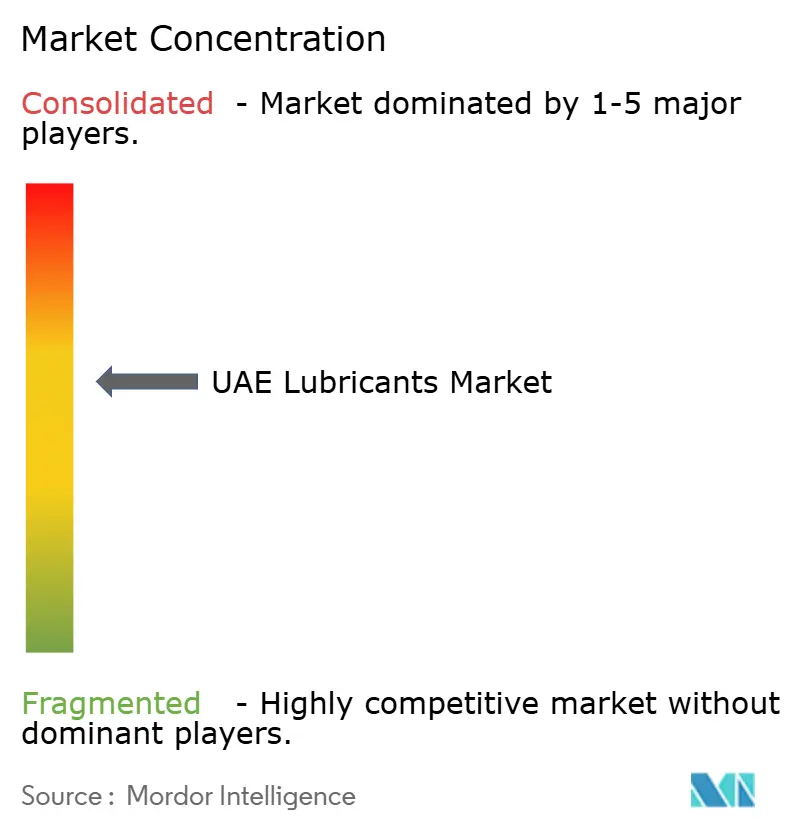

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Lubricants Market Analysis by Mordor Intelligence

The UAE Lubricants Market size is expected to increase from 172.58 million liters in 2025 to 178.69 million liters in 2026 and reach 212.64 million liters by 2031, growing at a CAGR of 3.54% over 2026-2031. Robust refinery integration at Ruwais is lowering feedstock costs, while Euro-5 regulations that took effect in 2026 are accelerating the adoption of low-SAPS synthetics. Construction and rail projects that followed EXPO 2020 are sustaining demand for hydraulic and gear oils in heavy equipment fleets, and ADNOC’s In-Country Value (ICV) program is channeling industrial procurement toward local blenders. At the same time, the counterfeit trade and volatile Asian freight rates are creating cost pressures that disproportionately affect smaller players. International majors are responding with GTL-derived and bio-based product launches, reinforcing premium positioning in the increasingly competitive UAE lubricants market.

Key Report Takeaways

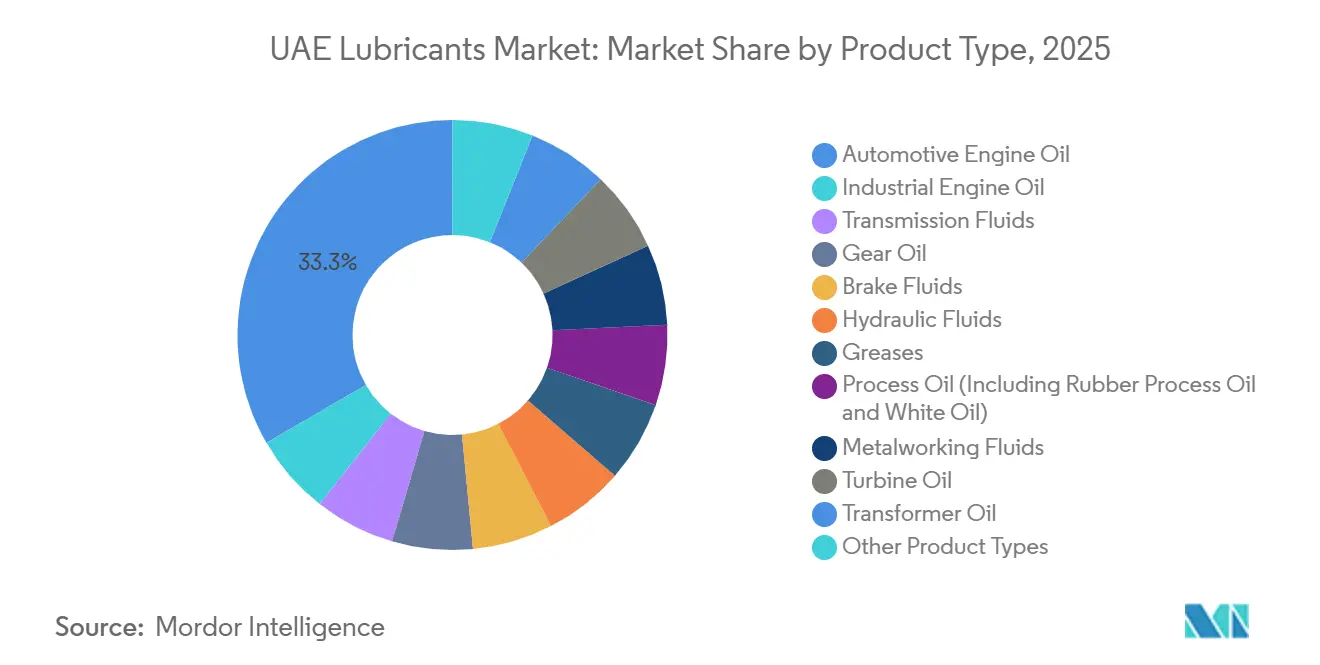

- By product type, automotive engine oil led with 33.35% of the UAE lubricants market share in 2025, while industrial engine oil is forecast to advance at a 3.65% CAGR to 2031.

- By end-user, automotive accounted for 53.12% of the UAE lubricants market size in 2025, whereas industrial is projected to grow at a 3.55% CAGR through 2031.

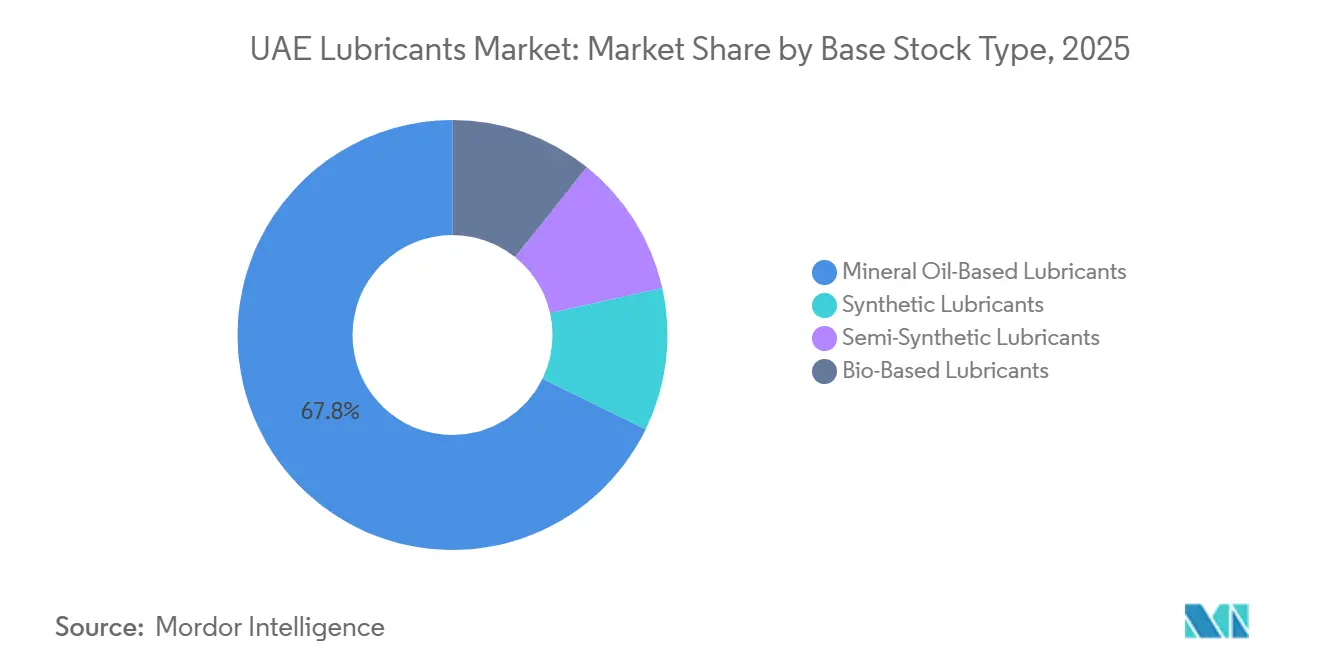

- By base stock, mineral oils held 67.78% of the UAE lubricants market size in 2025; bio-based formulations are expected to expand at a 4.09% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gradual shift from Group I to Group II/III base-oils in UAE blending plants | +0.8% | UAE (Abu Dhabi, Dubai blending hubs), with export spill-over to GCC and East Africa | Medium term (2-4 years) |

| ADNOC's expansion of Ruwais refinery boosting local base-oil availability | +0.6% | UAE national, with downstream benefits for Jebel Ali and Fujairah re-export terminals | Short term (≤ 2 years) |

| Strong post-COVID rebound in UAE construction equipment parc | +0.5% | UAE (Abu Dhabi, Dubai, Sharjah construction corridors), Northern Emirates industrial zones | Short term (≤ 2 years) |

| Government "Make it in the Emirates" industrialisation push raises industrial-oil demand | +0.7% | UAE national, concentrated in KIZAD, Khalifa Industrial Zone, and Ruwais petrochemical cluster | Medium term (2-4 years) |

| Mandatory Euro-5 import standards driving demand for premium synthetics | +0.9% | UAE national, with accelerated adoption in Dubai and Abu Dhabi fleets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Gradual Shift from Group I to Group II/III Base Oils in UAE Blending Plants

Blending facilities in Abu Dhabi and Dubai are accelerating the migration to hydro-cracked Group II and III stocks as OEMs demand longer drain intervals. ADNOC’s 600,000-ton-per-year Group III project with Neste delivers base oils with viscosity indices above 120, enabling 0W-20 and 5W-30 formulations that meet ACEA C3 and API SP. Localizing supply trims blending costs by up to 12% versus imports and has allowed ADNOC Distribution to extend its Voyager export footprint to 50 countries. Group II uptake is strongest in gear and hydraulic oils, where oxidation stability lengthens equipment life in high-temperature petrochemical applications[1]ADNOC Distribution, “Q3 2025 Management Discussion & Analysis,” adnoc.ae.

ADNOC Expansion at Ruwais Boosting Local Base-Oil Availability

The 420,000 bbl/d crude-capacity expansion at Ruwais added hydrocracking units that supply Group II/III feedstock at transfer prices 10-15% below spot CFR UAE levels. Vertical integration now supports bulk deliveries of turbine and compressor oils to power-generation clients within 48 hours, compared with a week or more for imported material. Proximity to KIZAD and the Ruwais petrochemical cluster cuts logistics costs by USD 15-20 per tonne and strengthens the UAE lubricants market position of domestic producers.

Strong Post-COVID Rebound in UAE Construction Equipment Parc

Large projects such as Etihad Rail Stage 2, Dubai Creek Harbour, and Yas Bay have raised demand for ISO VG 46/68 hydraulic fluids and EP gear oils in excavators and tower cranes. ADNOC Distribution expanded its oil-change network to 230 service points by mid-2025, mirroring higher preventive-maintenance activity in rental fleets that account for roughly 40% of the machinery parc. Cross-segmentation with offshore drilling has also lifted synthetic gear oil sales approved for top-drive gearboxes.

Government "Make it in the Emirates" industrialisation push raises industrial-oil demand

The ICV framework, which reached 86% in 2023, awards procurement preference to domestically blended lubricants, bolstering demand for turbine, transformer and metal-working fluids in aluminum, steel and chemicals plants at KIZAD. ADNOC Distribution’s specialty lineup now includes FDA-grade white oils and ISO 22241 diesel exhaust fluid, meeting the needs of food processing and SCR-equipped power gensets.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of counterfeit lubricants in grey markets | -0.4% | UAE (Ajman, Sharjah free zones), with cross-border flows from South Asia | Short term (≤ 2 years) |

| Rising base-oil freight rates from Asia | -0.3% | UAE import terminals (Jebel Ali, Fujairah), affecting blenders dependent on Singapore/South Korea supply | Short term (≤ 2 years) |

| Carbon-tax considerations inflating re-refined base-oil competitiveness | -0.4% | UAE, affecting the manufacturing of re-refined base oils and influencing prices | Medium term (>2 to 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Counterfeit Lubricants in Grey Markets

Despite ESMA’s tamper-evidence rules, seizures worth AED 7.46 million in 2024 underscore ongoing counterfeit activity in Ajman and Sharjah. Sub-specification base stocks shorten engine life and jeopardize warranties, prompting ENOC to roll out blockchain-linked QR codes and ADNOC Distribution to leverage its 551-station network to assure authenticity[2]ENOC, “Anti-Counterfeit Packaging Press Release, Dec 2024,” enoc.com .

Rising Base-Oil Freight Rates from Asia

South Korean and Singapore refiners diverted capacity to gasoil in early 2025, lifting Group I SN150 to USD 810 per tonne CFR UAE. Each USD 50-per-tonne freight increase adds roughly 6% to finished-product cost for import-dependent blenders, eroding margins in marine and industrial segments that rely on bright stock and cylinder oils.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Industrial Engine Oil Moves Ahead of Automotive

Industrial engine oil demand is poised to outgrow automotive counterparts at a 3.65% CAGR as gas-turbine, marine and upstream compressors consume higher‐viscosity formulations. The automotive category is maturing as extended-drain synthetics and growing EV penetration trim per-vehicle oil volume, yet it still retained 33.35% of the UAE lubricants market share in 2025. Turbine, hydraulic and metal-working fluids enjoy policy tailwinds from the “Make it in the Emirates” program, while specialty greases serve quarrying and agriculture in the Northern Emirates. Export approvals such as Siemens Energy for Voyager turbine oil and WinGD for marine cylinder oils reinforce brand credibility abroad. The UAE lubricants market size tied to transmission and gear oils is also expanding due to construction equipment that operates under severe thermal cycles.

Hydraulic fluids used in aluminum smelters, steel rolling mills, and plastic-molding lines benefit from Group II oxidation resistance, supporting up-time in continuous processes. Turbine oils with ≥ 10,000-hour stability are being specified for combined-cycle and solar-hybrid plants that make up the UAE’s new-build generation mix. Meanwhile, brake fluids, though low volume, remain essential for both automotive safety and heavy-equipment hydraulics and are widely retailed through ADNOC’s 157 oil-change centers.

By End-User Industry: Infrastructure Spend Lifts Industrial Growth

Automotive end users commanded 53.12% of the UAE lubricants market size in 2025 across passenger cars, commercial vehicles and two-wheelers. However, industrial users—power generation, metallurgy and petrochemicals—are projected to grow 3.55% per year through 2031. Passenger cars are shifting to 0W-20 low-SAPS formulations, while heavy trucks on the Dubai-Abu Dhabi corridor rely on 15W-40 CK-4 oils that balance cost and protection. Two-wheeler demand, although modest, is supported by JASO-approved oils for wet-clutch scooters popular with last-mile delivery fleets.

On the industrial side, turbine and transformer oils serve expanding generation and grid assets, whereas metal-working fluids lubricate CNC machining centers that supply downstream fabrication for construction and renewables projects. Marine lubricants supplied 54,711 m³ through Fujairah in 2025—critical for vessels navigating the Strait of Hormuz—and are moving toward Environmentally Acceptable Lubricants for compliance in protected waters. Aerospace remains a white space requiring MIL-PRF approvals, while heavy equipment in quarrying and agriculture continues to consume EP gear oils.

By Base Stock Type: Bio-Based Leads Growth, Mineral Still Dominant

Mineral oils retained 67.78% volume share in 2025, but OEM endorsements for bio-based hydraulics and marine oils are driving the fastest 4.09% CAGR. ADNOC’s Voyager PX Green, already exported to 46 markets, showcases an early-mover advantage, and PANOLIN-branded products from Shell broaden the sustainable portfolio. Synthetic PAO and ester oils, including Shell’s Helix Ultra Lightning and ExxonMobil’s Mobil 1 SuperSyn, capture the premium passenger-car niche. Semi-synthetic blends bridge cost and performance for mid-tier fleets, and the local supply of Group III from Ruwais blurs the line between traditional mineral and near-synthetic performance. Re-refined base oils are gaining policy interest as GCC carbon-tax debates intensify, with lifecycle studies showing up to 81% lower greenhouse-gas emissions versus virgin production.

Geography Analysis

Abu Dhabi anchors industrial demand with Ruwais’s 600,000-ton Group III complex and the KIZAD cluster that houses aluminum, steel, and chemical plants consuming transformer, turbine, and gear oils. ADNOC Distribution’s dense retail and logistics network underpins brand penetration and authentication, limiting counterfeit risk. Dubai operates as the re-export hub of the UAE lubricants market, hosting international majors in Jebel Ali Free Zone and capturing high-end passenger-car and marine segments. Construction projects and aviation maintenance at Dubai International and Al Maktoum airports create demand for synthetic ATF and specialty aerospace fluids. Fujairah, the world’s third-largest bunkering port, sold over 54,700 m³ of marine lubricants in 2025, reinforcing its strategic role for cylinder oils that meet IMO 2020 sulfur rules.

Sharjah and Ajman, part of the Northern Emirates, house mid-sized blenders such as SHARLU and United Grease & Lubricants with export footprints that reach Africa and South-East Asia. Weaker customs oversight, however, has encouraged counterfeit inflows, prompting brand owners to invest in anti-tamper packaging and dealer education. Ras Al Khaimah and Umm Al Quwain add incremental demand from quarrying and light industry, rounding out a national profile in which the UAE lubricants market benefits from deep-water ports, free-zone incentives, and fast customs clearance that support re-export into Oman, Saudi Arabia, and East Africa.

Competitive Landscape

The UAE lubricants market remains moderately consolidated. ADNOC draws advantage from captive Group III supply, enabling it to price synthetics competitively and extend Voyager exports. ENOC’s blockchain-secured packaging and SKF-based RecondOil service underline a technology-led push to extend drain intervals and reduce waste. Local independents such as Dana Lubricants, SHARLU, and Universal target price-sensitive commercial and industrial sectors with API-compliant products at double-digit discounts, often winning tenders that emphasize up-front cost. White-space opportunities in aerospace and biodegradable lubricants are attracting early investment; Voyager PX Green and Shell’s PANOLIN address sustainability mandates, while MIL-PRF certifications remain scarce among domestic players. Digital disruption is emerging through on-demand services; partnerships reminiscent of ExxonMobil’s mobile-app oil-change pilot overseas are influencing strategy discussions among UAE incumbents seeking to defend share.

UAE Lubricants Industry Leaders

Abu Dhabi National Oil Company (ADNOC) P.J.S.C.

Emirates National Oil Company (ENOC)

Shell plc

BP p.l.c.

ExxonMobil Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: ADNOC Distribution reported that Ruwais Group III output hit nameplate capacity, enabling full substitution of imported Group III in Voyager blends.

- December 2025: Shell introduced Helix Ultra Lightning, a GTL-derived synthetic carrying multiple European OEM approvals, at an Abu Dhabi launch event.

UAE Lubricants Market Report Scope

Lubricants, including oils, greases, and specialized fluids, play a critical role in optimizing machinery performance. By reducing friction, heat, and wear between moving surfaces, they enhance operational efficiency. Additionally, lubricants form a protective barrier that prevents corrosion, blocks contaminants, and extends the lifespan of mechanical components, ensuring long-term reliability and functionality.

The UAE lubricant market is segmented by product type, end-user industry, and base stock type. By product type, the market is segmented into automotive engine oil, industrial engine oil, transmission, fluids, gear oil, brake fluids, hydraulic fluids, greases, process oil (including rubber process oil and white oil), metalworking fluids, turbine oil, transformer oil, and other product types. By end-user industry, the market is segmented into automotive (passenger vehicles, commercial vehicles, and two-wheelers), marine, aerospace, heavy equipment (construction, mining, and agriculture), and industrial (power generation, metallurgy and metalworking, textiles, oil and gas, and other end-use industries). By base stock type, the market is segmented into mineral oil-based lubricants, synthetic lubricants, semi-synthetic lubricants, and bio-based lubricants.

By Product Type

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

By End-user Industry

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-Use Industries |

By Base Stock Type

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-Use Industries | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

Key Questions Answered in the Report

How large will the UAE lubricants market be by 2031?

Volume is forecast to reach 212.64 million liters by 2031, reflecting a 3.54% CAGR over 2026-2031.

Which segment grows fastest between 2026 and 2031?

Industrial engine oil is projected to expand at 3.65% per year, outperforming other product categories.

What drives demand for bio-based lubricants in the UAE?

OEM approvals for hydraulic and marine applications and corporate sustainability mandates are pushing bio-based volumes, which grow at a 4.09% CAGR.

How are Euro-5 and Euro-6 standards affecting lubricant formulations?

The regulations are accelerating a shift toward low-SAPS 0W-20 and 5W-30 synthetics that protect particulate filters and improve fuel economy by up to 3%.

Which companies dominate retail channels?

ADNOC Distribution, ENOC and Emarat collectively control about 63% of retail and commercial outlets through integrated fuel stations and blending plants.

Why are base-oil freight rates a risk factor?

Gas-oil margins in Asia reduced base-oil output, lifting freight costs and tightening imports, which raise finished-lubricant prices for UAE blenders that lack a captive supply.

Page last updated on: