Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

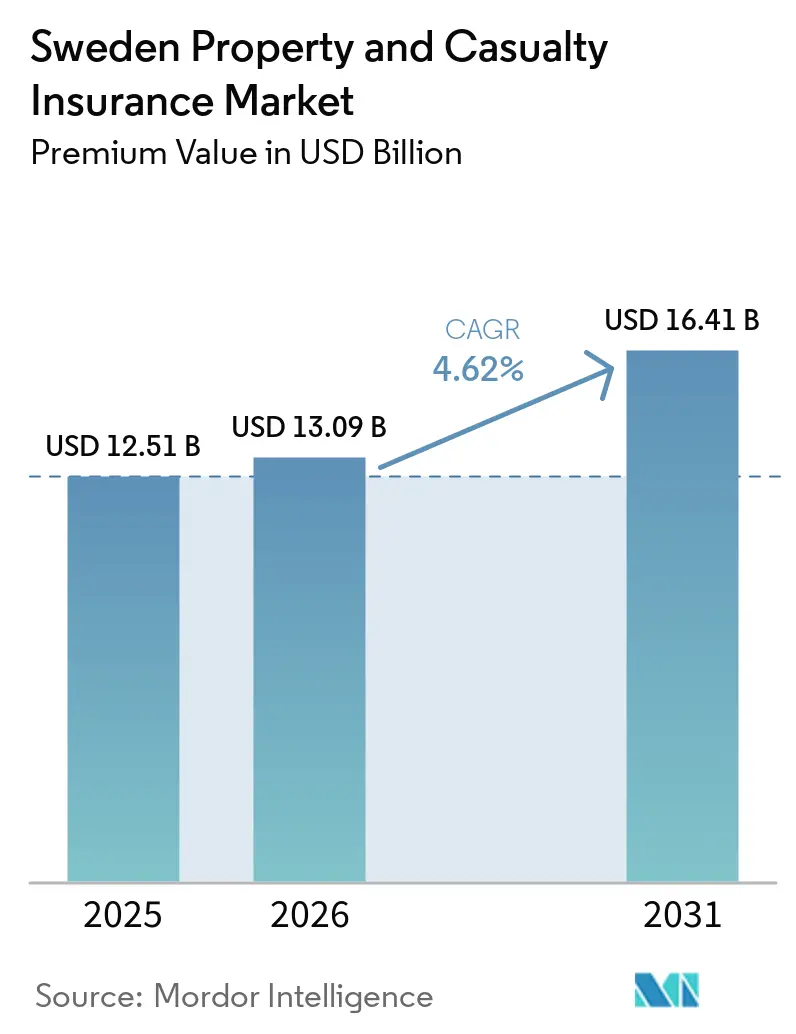

| Base Year Market Size (2025) | USD 12.51 Billion |

| Market Size (2026) | USD 13.09 Billion |

| Market Size (2031) | USD 16.41 Billion |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sweden Property and Casualty Insurance Market Analysis by Mordor Intelligence

The Sweden Property And Casualty Insurance Market size in terms of premium value is expected to grow from USD 12.51 billion in 2025 to USD 13.09 billion in 2026 and is forecast to reach USD 16.41 billion by 2031 at 4.62% CAGR over 2026-2031.

Digital distribution, telematics-driven auto pricing, and climate-adaptation coverage collectively underpin near-term revenue expansion. Insurers also benefit from robust household balance sheets and sustained mortgage origination that lift property sums insured. At the same time, mandatory traffic insurance sustains auto premium volumes while micro-mobility liability rules unlock incremental business. However, claims inflation linked to advanced vehicle parts and rising cyber-loss severity continues to squeeze technical margins, prompting greater focus on cost-efficient operating models and data-driven underwriting.

Key Report Takeaways

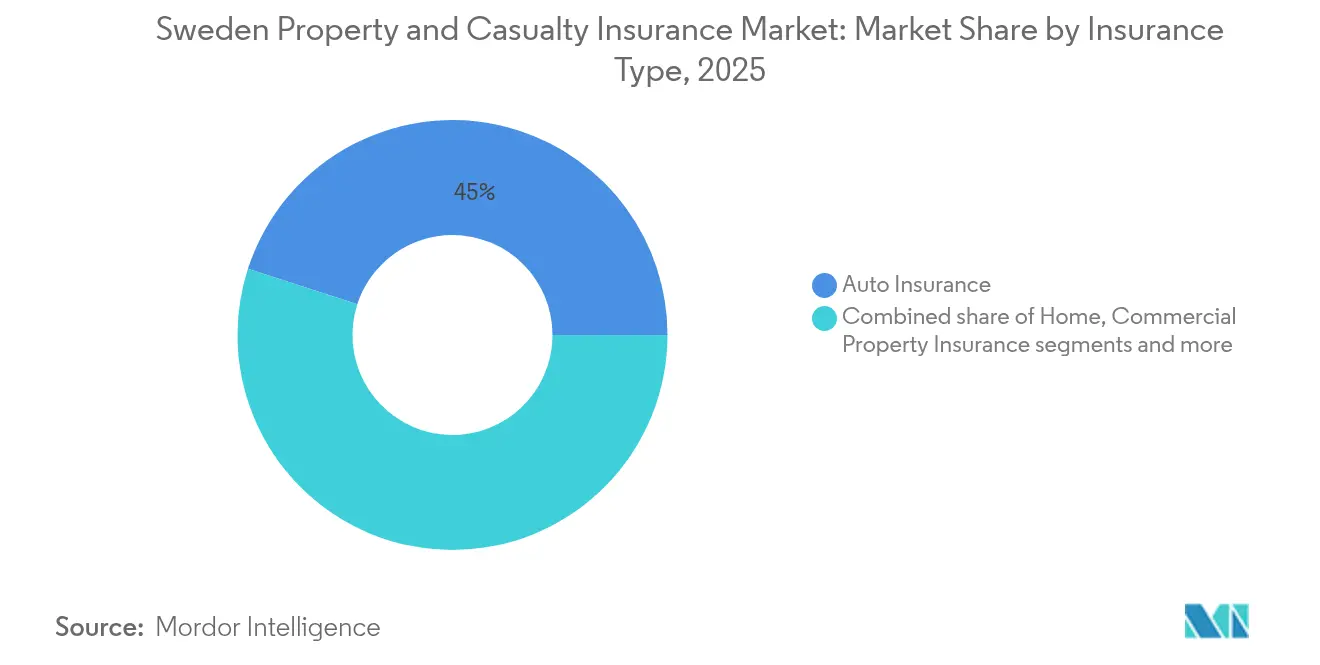

- By insurance type, auto insurance led with 45.02% of Sweden property and casualty insurance market share in 2025; liability insurance is forecast to advance at a 6.05% CAGR through 2031.

- By distribution channel, the direct segment controlled a 52.74% share of the Sweden property and casualty insurance market size in 2025 and is growing at a 7.14% CAGR.

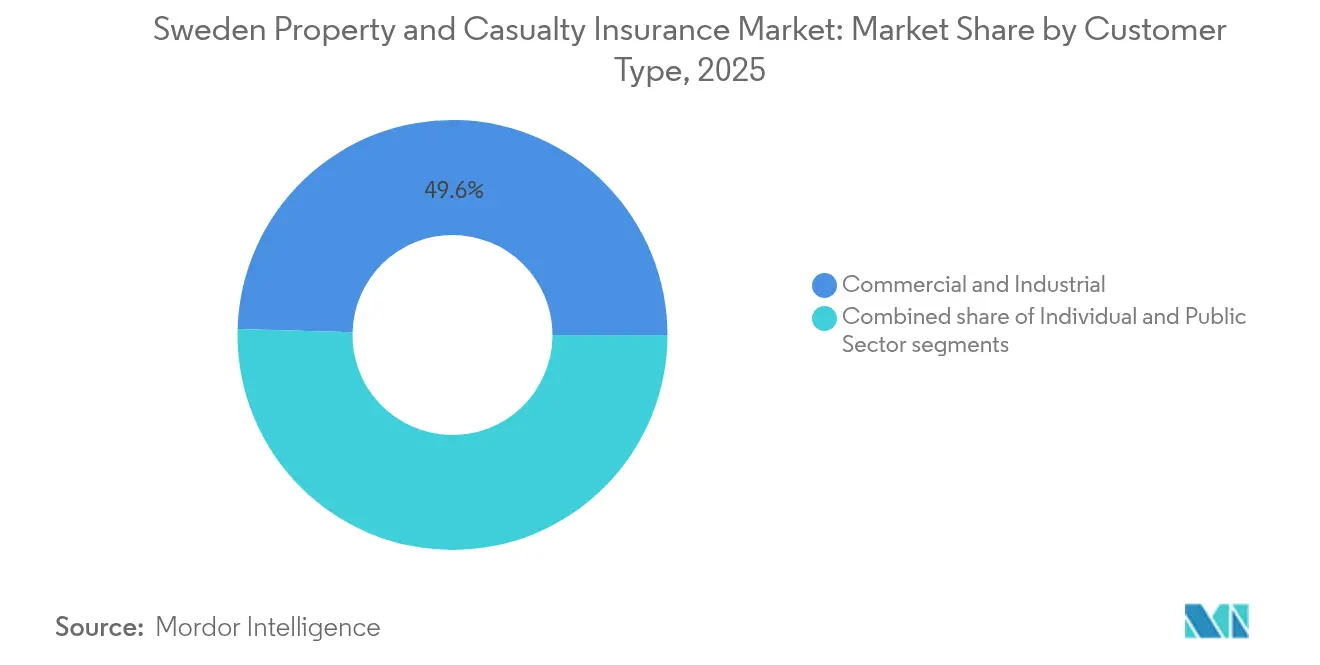

- By customer type, commercial & industrial clients accounted for a 49.55% share of the Sweden property and casualty insurance market size in 2025, while the Individual segment is expanding at a 5.18% CAGR.

- By region, Svealand captured 35.08% of Sweden property and casualty insurance market share in 2025; Götaland is the fastest-growing region at a 4.11% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Sweden Property and Casualty Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in telematics-based auto insurance | +1.2% | National; early gains in Stockholm, Göteborg, Malmö | Medium term (2-4 years) |

| Climate-adaptation renovations | +0.9% | National; coastal and northern regions | Long term (≥4 years) |

| Compulsory liability for micro-mobility | +0.3% | Urban centers: Stockholm, Göteborg, Malmö | Short term (≤2 years) |

| Digital distribution platforms expansion | +0.8% | National; higher uptake in metropolitan areas | Medium term (2-4 years) |

| Strong household balance sheets & mortgages | +0.7% | Svealand and Götaland | Medium term (2-4 years) |

| Increasing frequency of extreme weather | +0.6% | Northern and coastal regions | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Surge in Telematics-Based Auto Insurance Adoption

EU data-access rules now let drivers share vehicle telemetry directly with insurers, removing long-standing manufacturer bottlenecks and catalyzing the adoption of usage-based policies that cut premiums for safe, low-mileage users[1]Allianz SE, “EU Data Act Opens New Horizons for Usage-Based Insurance,” allianz.com.. Insurers add smartphone-driven scoring apps and on-board plug-ins that provide granular feedback on acceleration, braking, and cornering, nudging safer driving habits that lower accident frequency and claims costs. Larger carriers integrate telematics feeds with claims triage engines that trigger towing, medical, and repair workflows within minutes, shrinking loss-adjuster expenses and boosting customer retention. Competitive pricing pressure intensifies because granular risk segmentation shrinks cross-subsidies that once allowed broader premium bands. Digital-first entrants exploit over-the-air firmware access to iterate scoring models every quarter and at a tempo that traditional players struggle to match. The cumulative benefits strengthen the Sweden property and casualty insurance market by improving profitability even as policy counts rise.

Climate-Adaptation Renovations Boosting Property Premiums

Severe storms and shifting snow-load patterns over 2019-2024 pushed reinsurer deductibles higher, prompting Swedish homeowners to elevate foundations, install back-flow valves, and switch to Class B roofing tiles with higher wind-resistance ratings[2]European Investment Bank, “EIB Climate Survey 2024—Sweden Results,” eib.org. Insurers respond by embedding “green rebuild” clauses that pay for heat pump installations and recycled insulation, lifting reinstatement values by double-digit percentages, and immediately expanding written premiums. Further tying claim payouts to eco-certified materials via If P&C's sustainable building module would encourage contractors to adopt circular-economy standards and reduce long-run loss ratios through improved durability. Mortgage lenders increasingly demand proof of flood-risk mitigation before approving loan disbursements, indirectly forcing insurance uptake on previously under-insured coastal cottages. Swedish municipalities also tighten building codes, raising average replacement costs per square meter and thereby contributing additional premium volume. These converging forces reinforce the Sweden property and casualty insurance market as adaptation spending continues through the decade.

Compulsory Liability for Micro-Mobility Vehicles

Urban e-scooter fleets logged a surge in pedestrian injuries, prompting regulators to extend the Traffic Injuries Act provisions to all motorized devices exceeding 20 km/h in public areas[3]Transportstyrelsen, “Traffic Injuries Act: Insurance Rules for Micro-Mobility,” transportstyrelsen.se. Fleet owners must now hold blanket liability policies that cover bodily injury and property damage, and devices must display unique ID stickers linked to a central coverage registry, simplifying enforcement checks by police. Pricing models resemble commercial auto fleets, with per-unit premiums flexing on mileage and accident history captured via integrated accelerometers. Consumers using privately owned e-bikes purchase low-tier traffic cover bundled into renters’ or homeowners’ policies, raising penetration across personal lines. Brokers report that municipalities also buy umbrella policies to cover shared-mobility pilots on city sidewalks, adding another revenue layer. Early evidence suggests annualized loss ratios remain below 60%, given lower average claim severity, offering a profitable niche that enlarges the Sweden property and casualty insurance market.

Digital Distribution Platforms Expansion

Comparison platforms and insurer-owned portals cut acquisition costs by up to 50%, allowing smaller brands to reach national audiences without brick-and-mortar branches. AI chatbots pre-fill quote journeys using bank-ID credentials, slashing drop-off rates among time-pressed consumers in Stockholm and Göteborg. Embedded APIs inside mortgage, car-leasing, and travel-booking flows add contextual cross-sell moments; lifting attach rates on ancillary lines such as gadget cover and voluntary deductibles. Data-sharing consents now last 12 months under the Swedish Privacy Act, meaning insurers can periodically refresh coverage recommendations without additional paperwork, deepening client stickiness. Despite the digital push, complex marine and engineering lines still rely on face-to-face broking, preserving multi-channel relevance. The interplay between digital speed and human advisory breadth drives balanced growth for the Sweden property and casualty insurance market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price pressure from comparison portals | -0.4% | Urban areas | Short term (≤2 years) |

| Claims inflation from advanced vehicle parts | -0.6% | Metropolitan markets | Medium term (2-4 years) |

| Stricter capital rules under Solvency II | -0.3% | National | Long term (≥4 years) |

| Cyber-risk accumulation limits underwriting | -0.2% | Commercial segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Pressure from Comparison Portals

Instant quote algorithms strip away product-feature mystique, forcing carriers into visible price wars on standardized auto and content policies. Smaller firms leverage nimble operating models to cut overhead and underbid incumbents, yet often lack claims-service depth, pushing discerning customers back toward established brands. To defend margins, larger insurers roll out tiered cover, bronze, silver, and gold, so that headline prices stay competitive while upsell options preserve revenue. Loyalty rebates, carbon offset perks, and multi-product discounts add non-price levers that temper churn. Regulators watch for “price walking” but currently view transparent comparison tools as consumer-friendly, limiting the scope for intervention. Sustained down-pricing trims earned-premium growth by 0.4% points, modestly softening the Sweden property and casualty insurance market outlook.

Claims-Inflation from Advanced Vehicle Parts

The average cost to replace a single bumper on an ADAS-equipped EV now exceeds USD 2,500, three times the 2019 figure, because embedded radar modules require post-repair calibration. Semiconductor shortages lengthen repair times, generating higher rental-car indemnity claims. Preferred-repairer agreements cap labor rates, but OEM part prices remain largely inelastic, forcing carriers to negotiate bulk-buy contracts directly with suppliers. Telematics helps flag low-speed collisions where sensor wrists reset without full replacement, allowing remote advice to drivers and mitigating small claims. Reinsurers encourage the adoption of salvage-parts programs, yet consumer resistance remains strong for near-new vehicles. The net effect is a 0.6% point drag on the compound growth of underwriting profits within the Sweden property and casualty insurance market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Type: Auto Dominance Faces Liability Surge

In 2025, auto insurance accounted for 45.02% of Sweden property and casualty insurance market, driven by mandatory traffic coverage and a growing adoption of telematics, which aligns premiums with actual driving behavior. The increasing integration of telematics helps insurers assess risk more accurately and also incentivizes safer driving habits among policyholders. Liability insurance, spurred by mandates in micro-mobility and increased demand for professional indemnity, boasts a 6.05% CAGR, marking it as the fastest-growing segment among major lines. This growth reflects the evolving risk landscape and the rising need for tailored insurance solutions.

As electric vehicle (EV) adoption rises, repair costs surge, straining auto-combined ratios. The complexity of EV repairs, coupled with the higher cost of specialized parts and labor, further amplifies this pressure. This trend underscores the urgency for data-driven pricing and strategic repair partnerships to manage costs effectively. Meanwhile, liability lines are expanding due to emerging risk classes like e-scooters and indemnities for the gig economy. These developments highlight the industry's ability to adapt to new risks and consumer needs, broadening Sweden property and casualty insurance market. Both home and commercial property insurance remain steadfast revenue sources, buoyed by climate-resilient upgrades that elevate insured sums and spur premium growth. Investments in climate-proofing properties, such as flood defenses and energy-efficient retrofits, are driving incremental premium increases while ensuring long-term sustainability for insurers.

By Distribution Channel: Direct Surge Reshapes Market Access

The Direct channel captured 52.74% of Sweden property and casualty insurance market share by 2025, building on consumer trust in Bank-ID authentication that simplifies digital onboarding. Real-time underwriting enables instant motor and home cover issuance at the point of car purchase or real-estate closing, turning distribution timing into a critical differentiator. AI-powered advisors within portals explain deductible trade-offs, increasing average deductibles chosen, and lowering future claims frequency. Data analytics personalize renewal messages, flagging life events such as moving or adding a family member that warrant coverage updates, and reducing lapse rates by 300 basis points year on year.

Agencies still retain footholds in personal-line bundles for retirees who value relationship continuity and in large commercial accounts where risk engineering site surveys remain essential. Bancassurance thrives on cross-selling mortgage-linked property policies and payment-protection add-ons, representing 11.72% of the Sweden property and casualty insurance market. Digital brokers blend algorithmic comparison with optional human chat, capturing mid-complexity personal lines such as high-value content and leisure craft. Affinity deals with trade unions and sports federations to create captive pools whose claims experience trends below market average, delivering profitable loss ratios that subsidize competitive pricing on other portfolios. Combined, this multi-channel ecosystem underpins steady growth for the Sweden property and casualty insurance market despite margin compression in fully commoditized products.

By Customer Type: Commercial Strength Meets Individual Growth

Commercial & Industrial policies contributed 49.55% of Sweden property and casualty insurance market share in 2025, reflecting Sweden export-heavy economy, where machinery breakdown, cargo, and business interruption covers carry large limits. Mid-cap manufacturers now buy cyber-extension riders as supply-chain digitization exposes them to ransomware threats capable of halting production. Renewable-energy developers in Norrland seek specialized construction-all-risk and operational-phase covers for wind and hydro projects, injecting new premium flows into commercial books. Overall, the segment’s technical profitability remains strong owing to a professional risk-management culture and lower claims frequency relative to personal lines.

Individual customers, while smaller ticket per policy, outpace commercial growth at a 5.18% CAGR, bolstered by rising housing values, personal-electronics cover, and hybrid working, which increases work-from-home equipment insured under contents extensions. Telematics-enabled auto policies attract younger demographics historically priced out of the market, expanding penetration among first-car owners. E-commerce boom fuels demand for in-transit cover on high-value parcels, bundled as micro-policies at checkout, further widening the Sweden property and casualty insurance market footprint. Combined multiproduct discounts cultivate stickiness, evidenced by cross-sell ratios rising to 2.7 policies per retail customer. The shift signals a strategic imperative: aggregate small but numerous personal accounts to diversify revenue against large-loss volatility in commercial lines.

Geography Analysis

Stockholm's concentration of affluent households and corporate headquarters enables Svealand to command a dominant 35.08% share of Sweden property and casualty insurance market. The city's mortgage expansion and robust household net worth bolster property premiums by ensuring a steady demand for property insurance products. Meanwhile, Stockholm's burgeoning tech ecosystem is fast-tracking the digital adoption of policy purchases and claims servicing, enabling insurers to streamline operations and enhance customer experiences.

Götaland, with the highest regional CAGR of 4.11% projected through 2031, is witnessing a surge in demand for product liability, cargo, and business interruption coverage. This uptick is largely fueled by automotive, aerospace, and logistics clusters forming around Göteborg, which are driving industrial growth and increasing the need for comprehensive insurance solutions. Additionally, concerns over coastal flooding have led to climate-adaptation endorsements, further boosting the region's insured property sums. These developments are significantly contributing to the expansion of the local size of Sweden property and casualty insurance market.

While Norrland may be the smallest market, its mining, renewable energy, and infrastructure projects are in dire need of specialized commercial coverage. The region's challenges, from extreme snowfall to changing precipitation patterns, demand updated risk modeling, which in turn affects rating factors and product design. These tailored insurance products are crucial for mitigating risks associated with the region's unique environmental and industrial conditions. Digital channels and the efforts of cooperative insurers ensure even the most sparsely populated areas are being reached, ensuring that inclusive growth remains a cornerstone of Sweden property and casualty insurance landscape.

Competitive Landscape

The Sweden property and casualty insurance market remains moderately concentrated, with P&C Insurance reporting USD 6.4 billion in premiums across 4 million Nordic customers, and is leveraging its scale to invest in omnichannel platforms and sustainable claims processes.

Länsförsäkringar’s regional cooperatives maintain high customer loyalty through local presence and digital innovation, while Folksam strengthens affinity alliances with trade unions.

Customer-experience surveys place Svedea atop vehicle insurance satisfaction at 82.1 points, highlighting service quality as a key differentiator even in a price-competitive environment. Dina Försäkringar achieves similar recognition in property lines, reflecting community-focused claims handling that builds trust. Sustainability credentials also shape brand equity; Länsförsäkringar and Svedea received top environmental ratings in a 2024 market study, illustrating how ESG performance supports retention and acquisition in the Sweden property and casualty insurance market.

Digital-native challengers and comparison portals intensify pressure on legacy carriers. Swedbank’s adoption of Akur8’s AI pricing platform exemplifies the pivot toward advanced analytics that shortens time-to-market and refines risk segmentation. UNIQA, joining the Eurapco network alongside Länsförsäkringar, facilitates cross-border knowledge transfer on digital transformation and climate risk underwriting, elevating competitive benchmarks.

Sweden Property and Casualty Insurance Industry Leaders

Länsförsäkringar Alliance

If Skadeförsäkring AB

Folksam Ömsesidig Sakförsäkring

Trygg-Hansa (Codan Forsikring)

Dina Försäkringar

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: UNIQA Insurance Group joined the Eurapco Alliance, expanding collaboration on digital and sustainability initiatives across 35 countries, XPRIMM.

- January 2025: Insurely partnered with Länsförsäkringar Älvsborg to launch an AI-powered Advisor Dashboard for real-time policy comparison.

- July 2024: A global IT outage caused USD 10 billion-USD 15 billion in damages and USD 1.5 billion in insured losses, spotlighting cyber-risk accumulation in International Insurance.

- March 2024: Swedbank deployed Akur8’s cloud pricing tool to improve the predictive modeling accuracy of Akur8.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Sweden's property & casualty (non-life) insurance market as the gross written premiums generated within Sweden for motor, home, commercial property, liability, travel, pet, and other miscellaneous covers sold to individuals, businesses, and public-sector entities in Swedish-regulated paper or under EU freedom-of-services provisions.

Reinsurance flows, life, accident & health lines, and policies written on overseas risks are outside scope.

Segmentation Overview

- By Insurance Type

- Home Insurance

- Auto Insurance

- Commercial Property Insurance

- Liability Insurance

- Travel Insurance

- Pet Insurance

- By Distribution Channel

- Direct

- Agencies

- Banks

- Digital Brokers

- Affinity Partnerships

- By Customer Type

- Individual

- Commercial & Industrial

- Public Sector

- By Region

- Götaland

- Svealand

- Norrland

Detailed Research Methodology and Data Validation

Primary Research

Interviews and structured questionnaires with underwriters, MGA executives, brokerage heads, and regulatory advisers across Stockholm, Gothenburg, and Malmö help us verify retention ratios, embedded-insurance uptake, and expected catastrophe loadings. Responses also calibrate the discount rate and expense assumptions used in our premium models.

Desk Research

Mordor analysts first screen government and trade datasets such as Insurance Sweden's quarterly premium bulletins, Finansinspektionen solvency filings, Statistics Sweden macro tables, and Eurostat household spending series. We widen context using OECD insurance indicators, Swiss Re sigma market briefs, and peer-reviewed papers on Nordic climate-related loss trends. Company 10-Ks, investor slides, and press releases then anchor recent pricing cycles, while news aggregation from Dow Jones Factiva supplies event chronologies. These sources establish historical premium pools and stress points; yet they are neither exhaustive nor the only repositories we interrogate for validation.

Further depth is achieved through our paid access to D&B Hoovers for carrier financials and Questel patent analytics that shed light on telematics and cyber-risk product launches. This mosaic provides the secondary framework, though numerous additional outlets inform finer checks.

Market-Sizing & Forecasting

A top-down and bottom-up hybrid begins with 2024 gross written premium totals from Insurance Sweden, rebased into USD and trended forward by inflation-adjusted motor, property, and liability premium indices. Results are cross-checked against sampled carrier roll-ups and average price-per-policy times in-force policy counts drawn from survey returns. Key variables include new-vehicle registrations, dwelling completions, SME formation rates, severe-weather claim frequencies, and average court-awarded liability settlements. Forecasts apply a multivariate regression where premium growth is explained by GDP, consumer price inflation, and EV penetration, with scenario analysis around climate-loss volatility. Data gaps, such as opaque affinity-channel volumes, are bridged using conservative ratio benchmarks validated during interviews.

Data Validation & Update Cycle

Outputs run through variance checks against historic loss ratios and foreign exchange trends, followed by peer review by a senior analyst panel. Models refresh each year or sooner should statutory rule changes or large-loss events move the baseline materially.

Why Mordor's Sweden Property & Casualty Insurance Baseline Earns Trust

Published figures often diverge because firms pick different premium definitions, exchange rates, and refresh cadences.

By anchoring on audited Swedish filings and layering them with real-time carrier insight, Mordor delivers a figure clients can confidently reference.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 12.51 bn (2025) | Mordor Intelligence | - |

| USD 11.0 bn (2023) | Regional Consultancy A | Excludes affinity bundles; converts EUR at historic average, not year-end rate |

| USD 9.7 bn (2022) | Trade Journal B | Uses net premiums after reinsurance; older base year |

| USD 11.7 bn (2022) | Industry Association C | Includes accident & health lines and applies constant 2020 FX assumptions |

Taken together, the comparison shows that scope selection, currency timing, and premium basis easily swing totals by billions. Mordor's disciplined variable set, annual refresh, and open-book assumptions therefore provide the most reliable baseline for strategic planning.

Key Questions Answered in the Report

What is the current size of the Sweden property and casualty insurance market?

It is valued at USD 13.09 billion in 2026 and is projected to reach USD 16.41 billion by 2031.

Which insurance line dominates the Sweden property and casualty insurance market?

Auto Insurance holds the top position with a 45.02% share in 2025 due to mandatory traffic coverage.

How fast is the liability segment growing in Sweden?

Liability Insurance is the fastest-growing line, expanding at a 6.05% CAGR through 2031.

Which sales channel is growing quickest?

Direct digital distribution is expanding at 7.14% CAGR and already commands a 52.74% market share.

Which Swedish region offers the strongest growth prospects?

Götaland is forecast to grow at a 4.11% CAGR, outpacing other regions through 2031.

How are insurers addressing claims inflation from high-tech vehicle repairs?

Carriers develop preferred repair networks, promote aftermarket parts, and refine telematics-based pricing to manage rising costs associated with advanced vehicle components.

Page last updated on: