Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

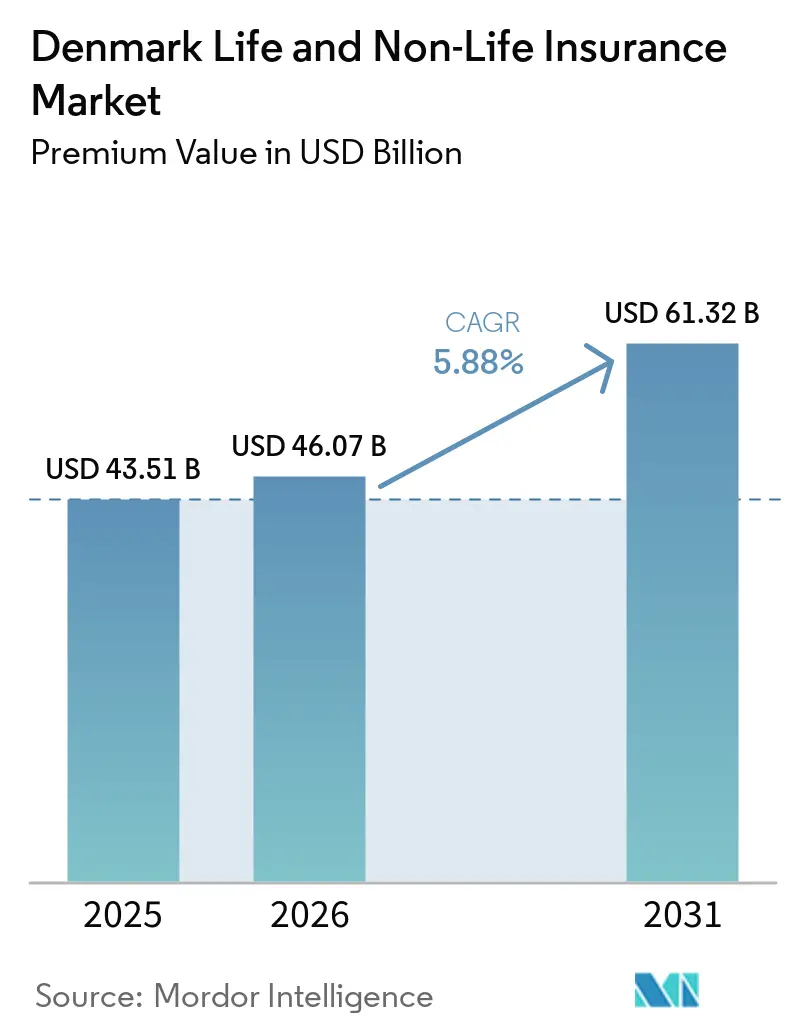

| Base Year Market Size (2025) | USD 43.51 Billion |

| Market Size (2026) | USD 46.07 Billion |

| Market Size (2031) | USD 61.32 Billion |

| Growth Rate (2026 - 2031) | 5.88% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Denmark Life and Non-Life Insurance Market Analysis by Mordor Intelligence

The Denmark Life And Non-Life Insurance Market size in terms of premium value is projected to be USD 43.51 billion in 2025, USD 46.07 billion in 2026, and reach USD 61.32 billion by 2031, growing at a CAGR of 5.88% from 2026 to 2031.

Solid household savings, mandatory occupational pensions, and the rapid digitalization of distribution have been the primary forces sustaining growth. The Denmark life and non-life insurance market continues to benefit from a structural pivot toward market-rate pension products that boost fee income while shifting investment risk to policyholders. At the same time, surging motor and property claims inflation is compelling insurers to pass through higher premiums, preserving underwriting discipline. Parametric flood solutions, catalyzed by escalating climate-risk exposure, are opening new premium pools, while compliance with EU DORA and CSRD is forcing technology upgrades that favor scale players able to amortize costs over larger books of business.

Key Report Takeaways

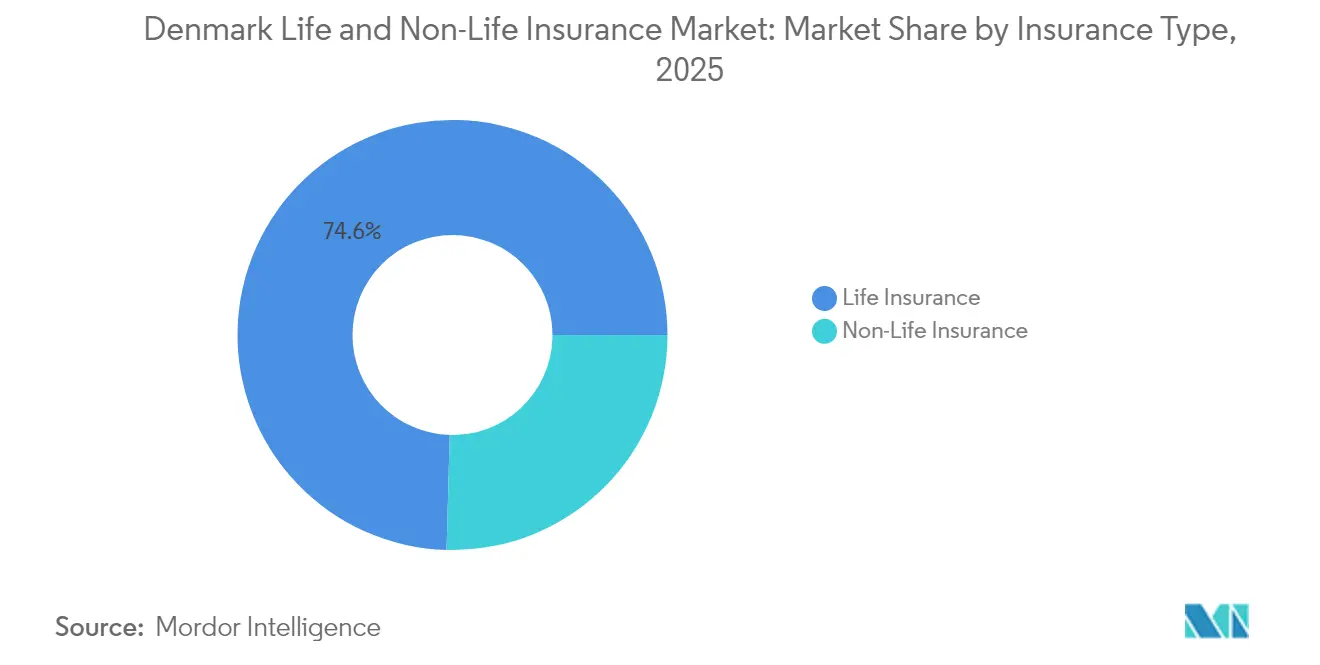

- By insurance type, life products led with 74.56% of Denmark life and non-life insurance market share in 2025; non-life lines are pacing the field with a 7.12% CAGR through 2031.

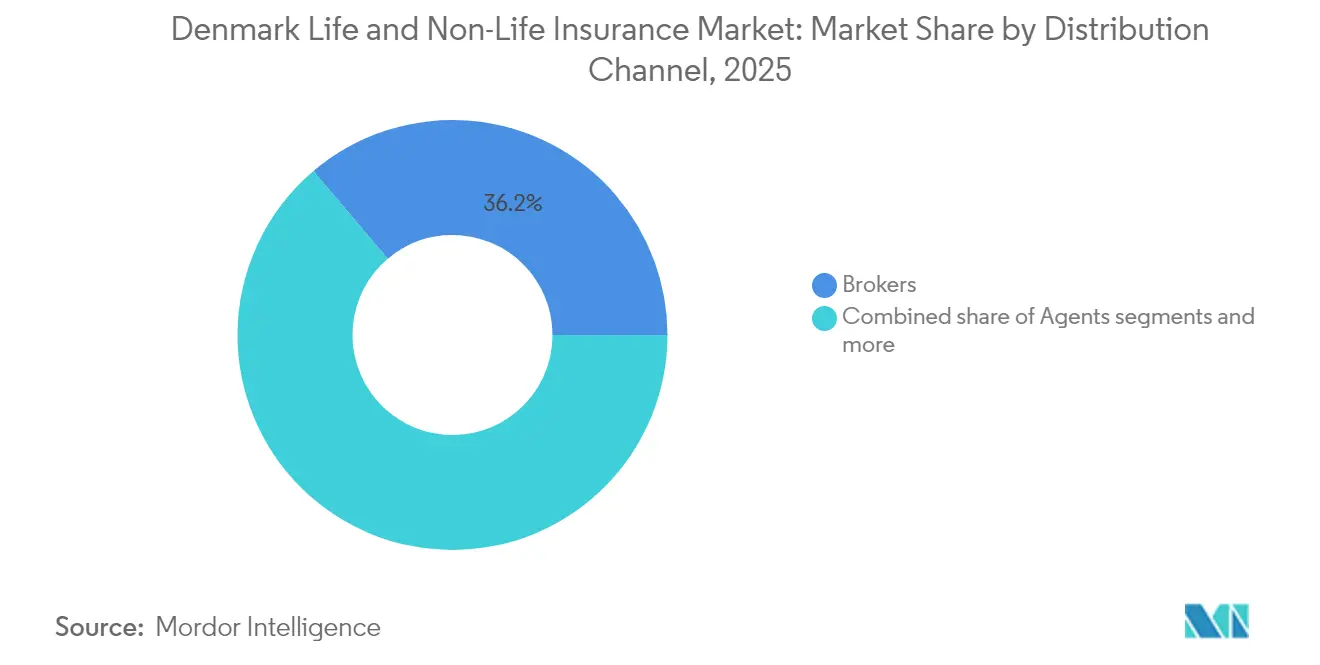

- By distribution channel, brokers captured a 36.20% share of the Denmark life and non-life insurance market in 2025, while direct digital sales are advancing at a 6.86% CAGR to 2031.

- By customer segment, retail policies generated 80.10% of the Denmark life and non-life insurance market size in 2025; corporate demand is expanding at a 6.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Denmark Life and Non-Life Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift from average-rate to market-rate pension products | + 1.8% | National, concentrated in the Capital Region and Central Denmark | Medium term (2-4 years) |

| Rising employer-funded health insurance penetration | +1.2% | National, with higher adoption in urban regions | Long term (≥ 4 years) |

| Digital & omni-channel distribution acceleration | +0.9% | National, with early gains in the Capital Region | Short term (≤ 2 years) |

| Motor premium growth amid claims-inflation pass-through | + 1.4% | National, with a higher impact in North Denmark and Region Zealand | Medium term (2-4 years) |

| Mandatory insurance enforcement in the Danish Straits boosts marine liability demand | +0.3% | Regional, focused on coastal areas and maritime corridors | Long term (≥ 4 years) |

| Parametric flood products leveraging Denmark's high climate-loss cover | +0.5% | National, with a concentration in coastal and low-lying areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shifts from Average-Rate to Market-Rate Pension Products

The transition away from guaranteed average-rate contracts toward market-rate pensions is reshaping the Denmark life and non-life insurance market. A state pension age rising to 70 by 2040 is lengthening contribution horizons, thereby enlarging investable assets[1]OECD, “Pensions at a Glance 2025 – Denmark,” oecd.org. . Danica Pension’s “Forward 28” program exemplifies carriers’ emphasis on higher-yielding investment‐linked offerings and digital self-service journeys to capture these flows. Larger insurers with multi-asset expertise are best positioned to harvest fee income while ceding longevity and investment risk to policyholders. Competitive intensity is accelerating as Topdanmark, PFA, and others roll out low-cost indexed funds inside market-rate wrappers

Rising Employer-Funded Health Insurance Penetration

Employer-paid health cover is spreading as companies vie for talent and seek to curb sick-leave costs despite Denmark’s robust public system. Reimbursement thresholds raised by Sygeforsikringen “Denmark” in 2025 for dental and physiotherapy services underscore employers’ appetite for supplementary benefits. Life-science and technology firms are especially active, with Novo Nordisk and other blue-chips offering executive wellness packages that bundle mental-health support. Group medical policies recorded premium growth nearing 8% in 2024, outpacing the broader Denmark life and non-life insurance market. Tax treatment remains a policy wildcard; however, current fiscal neutrality has sustained momentum.

Digital and Omni-Channel Distribution Acceleration

Near-universal broadband penetration and nationwide 5G coverage underpin the rapid emergence of digital self-service portals and embedded insurance propositions. Insurers have rolled out AI-assisted chatbots for first-notice-of-loss, while Tryg tested an injury-case documentation assistant in the Danish Financial Supervisory Authority’s sandbox[2]Tryg A/S, “AI Assistant Sandbox Project,” tryg.com. . Direct online premiums rose 7.3% in 2024, and the Denmark life and non-life insurance market is seeing up to 35% of new motor policies purchased via mobile apps. Compliance with GDPR and upcoming EU DORA rules is prompting heavy investment in cloud infrastructure, favoring carriers able to budget multi-million-USD upgrades. Over the short term, digital adoption is anticipated to boost market growth by 0.9% annually.

Motor Premium Growth Amid Claims-Inflation Pass-Through

Motor insurers are contending with 6% quarterly claims inflation driven by advanced driver-assistance systems, EV spare-part costs, and workshop labor rates. Carriers responded with double-digit premium hikes in 2024, with Gjensidige achieving a 90% pass-through rate. Telematics and usage-based pricing are helping segment risks and sustain underwriting margins. Danish regulators have backed actuarially sound rate increases, recognizing the need for solvency stability.

Restraints Impact Analysis*

| Restraint | % (~)Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low interest-rate compression on legacy life guarantees | -1.1% | National, with a higher impact on traditional life insurers | Long term (≥ 4 years) |

| Motor & property claims-cost inflation (spare parts, materials) | -0.8% | National, with regional variations in repair costs | Medium term (2-4 years) |

| EU DORA/CSRD compliance burden for small mutuals | -0.4% | National, disproportionately affecting smaller regional insurers | Short term (≤ 2 years) |

| Growth in class actions via litigation funding raises liability risk | -0.3% | National, with a concentration in commercial liability segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Low Interest-Rate Compression on Legacy Life Guarantees

Despite recent rate rises by Danmarks Nationalbank, yields on Danish sovereigns remain below the 3–4% guarantees embedded in legacy life books, squeezing spreads for traditional carriers[3]European Central Bank, “Solvency II and the Danish Compromise,” ecb.europa.eu.. The so-called “Danish compromise” offers some capital-relief flexibility, yet the negative carry persists. Firms must hold sizable capital buffers, diverting funds from growth initiatives to support guarantee run-off. New business is overwhelmingly market-rate, but the slow amortization of old blocks will weigh on sector profitability for at least another decade.

Motor & Property Claims-Cost Inflation

Escalating costs for EV battery packs, ADAS sensors, lumber, and skilled labor have pushed average repair bills well above consumer-price inflation [4]Statistics Denmark, “Repair Cost Index 2024,” dst.dk. . Even with higher premiums, combined ratios remain under pressure, especially for sub-scale regional carriers lacking procurement leverage. Larger insurers are tightening preferred-repair-shop agreements and deploying AI-driven parts-sourcing engines to mitigate expense drift. Nevertheless, lingering supply-chain bottlenecks suggest elevated claims severity will persist through at least 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Type: Life Dominance Amid Non-Life Acceleration

Life products retained 74.56% of Denmark life and non-life insurance market share in 2025, underpinned by compulsory occupational pension contributions and high household savings. Non-life premiums, however, are scaling faster at 7.12% CAGR, supported by 50% average motor-rate hikes, enforced marine liability in the Danish Straits, and growing employer-health uptake. Danica Pension’s shift to market-rate strategies is spurring an inflow of contributions to unit-linked accounts that charge asset-based fees, helping expand Denmark life and non-life insurance market size within the life bucket. On the non-life side, property lines are capitalizing on rising construction-value indices and increased take-up of climate-risk riders propelled by DTU flood-loss projections. Liability lines are also expanding as litigation funding makes class actions more viable, nudging corporates toward broader D&O and professional-indemnity limits.

Motor insurance remains the bellwether of non-life profitability; Gjensidige’s 83 combined ratio in 2024 showed that disciplined pricing and telematics segmentation can still deliver healthy margins. Health insurance premiums rose in tandem with employer benefits budgets, while the marine segment gained a boost from mandatory coverage rules that came into full enforcement in 2024. Carriers are using parametric structures in flood and crop lines to speed claims settlement, enhancing customer experience and reducing frictional costs. Over the forecast horizon, life products will continue to anchor Denmark life and non-life insurance market size, but non-life lines will drive incremental growth.

By Distribution Channel: Broker Networks Face Digital Disruption

Brokers controlled 36.20% of Denmark's life and non-life insurance market share in 2025, a testament to their advisory role in complex commercial placements. Yet direct digital channels are outpacing legacy intermediaries, expanding to 6.86% CAGR as consumers chase convenience and price transparency. Tryg’s 10% online discount has stimulated web-based conversions, while mobile in-app claims filing has slashed loss-adjustment expenses. Banks remain vital for life policies, leveraging bundled checking-pension propositions; Danske Bank’s integration with Danica exemplifies bancassurance collaborations that enhance Denmark's life and non-life insurance market size within the life sphere.

Regional agents still resonate in rural districts where digital uptake trails urban norms, illustrating that omnichannel strategies remain essential. Affinity and embedded offerings, such as appliance coverage bundled with electronics retailers, are emerging micro-channels that capitalize on Denmark’s e-commerce penetration. As EU DORA tightens cybersecurity mandates, carriers with robust data-governance frameworks will win trust and differentiate service quality, tilting share toward scale operators able to absorb compliance overhead.

By Customer Segment: Retail Dominance with Corporate Growth Acceleration

Retail policies generated 80.10% of Denmark's life and non-life insurance market size in 2025, supported by GDP growth of 3.0%, low unemployment, and stable disposable income. High mobile-banking usage has made digital onboarding friction-free, especially for simple term-life and motor covers. Mandatory occupational pensions guarantee a steady premium stream, while supplemental health and dental plans are climbing as public system wait times lengthen. The Denmark life and non-life insurance market continues to find depth in retail because consumer awareness of climate and cyber risks is fostering demand for broader household and personal cyber protection.

Corporate premiums are expanding to a 6.42% CAGR, propelled by elevated bankruptcy-rate memories and the need to shore up supply-chain resilience. SMEs, now subject to CSRD-linked sustainability disclosures, are purchasing environmental-liability riders. Renewable-energy pioneers like Topsoe secured technology-performance guarantees to derisk new hydrogen projects, underscoring the rising appetite for specialty covers. As firms digitize operations, cyber-risk awareness is driving take-up of network-interruption policies. Although corporate lines remain a smaller slice of Denmark's life and non-life insurance market share, their higher average premiums make them pivotal to the top-line trajectory.

Geography Analysis

The Capital Region captured an estimated 41.50% of Denmark's life and non-life insurance market size in 2025, reflecting Copenhagen’s concentration of corporate headquarters, high-value real estate, and affluent households. Headquarters of Danske Bank and other financial services majors anchor demand for complex liability and executive-risk solutions. Robust digital infrastructure accelerates the uptake of direct sales and embedded products, making the region a testbed for Insurtech pilots.

Central Denmark follows as the second-largest premium pool, buoyed by manufacturing and renewable-energy clusters around Aarhus. Topsoe’s SOEC factory inauguration in Herning in 2025 is likely to catalyze insurance demand for construction, operation-phase warranties, and environmental liability. Agricultural acreage in the hinterland is spurring crop-insurance experimentation with parametric rainfall triggers. These factors combine to give Central Denmark the fastest projected 7.22% CAGR through 2031.

Region Zealand and the Region of Southern Denmark exhibit balanced growth, mixing urban centers with agrarian districts. Both regions face notable flood exposure; DTU projects storm-surge damages of USD 34.7 billion (DKK 249 billion) over the next century, prompting homeowners and municipalities to seek higher climate-loss limits. North Denmark, though smaller in population, shows elevated marine-insurance density due to its proximity to the Danish Straits. Mandatory liability enforcement for transiting vessels has lifted premiums, cushioning regional market growth. Across all five regions, insurers that tailor distribution, blending local agents with digital self-service, will capture an outsized share of Denmark life and non-life insurance market expansion.

Competitive Landscape

Denmark’s insurance arena is moderately concentrated. Market leadership rests on multi-product breadth, brand equity, and economies of scale that help absorb regulatory tech spend. Tryg’s weather-claims tolerance of DKK 800 million annually (USD 116 million) and equal large-claims guidance signal disciplined risk appetite that smaller rivals struggle to match.

Consolidation remains a theme as mid-tier mutuals evaluate capital pressure from EU DORA and CSRD. Alm. Brand’s 2024 acquisition of Codan’s Danish personal-lines book sharpened focus on profitable niches, while Gjensidige’s 11% revenue surge and 83.3 combined ratio proved that cross-Nordic diversification plus precise pricing delivers robust margins. Codan has carved a distinct global niche in offshore-wind insurance, riding Denmark’s renewable-energy laurels to secure contracts from German and U.K. wind parks.

Strategic differentiation is now gravitating toward AI-enabled underwriting, embedded micro-covers, and climate-risk analytics. Carriers able to integrate real-time weather data into claims triage or to embed gadget insurance at e-retail checkout are seizing wallet share in the Denmark life & non-life insurance market. Legacy mutuals lacking digital scale are expected to partner with cloud providers or become acquisition targets, further tightening competitive intensity.

Denmark Life and Non-Life Insurance Industry Leaders

Tryg

Alm. Brand

Topdanmark

Gjensidige

If P&C Insurance

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Allianz, aligning with its strategy to bolster private credit capabilities, initiated early-stage discussions to acquire Capital Four. The Copenhagen-based European credit manager boasts over USD 23.9 billion (EUR 23 billion) in assets under management, including USD 8.3 billion (EUR 8 billion) in private credit, as reported by Insurance Business.

- February 2025: Denmark transposed forthcoming EU AI Act provisions, empowering national authorities to police prohibited AI use, a move that will broaden insurers’ compliance obligations around automated decision-making.

- January 2025: Topsoe partnered with New Energy Risk to underwrite technology-performance insurance for solid-oxide electrolyzer cells, covering commissioning through operations to enhance the bankability of Danish green-hydrogen projects.

- January 2025: Danske Bank unveiled Danica Pension’s “Forward 28” strategy, prioritizing digital engagement, healthcare add-ons, and attractive net returns to elevate customer experience by 2028.

Denmark Life and Non-Life Insurance Market Report Scope

Life insurance provides a lump sum amount of sum assured at the time of maturity or in case of death of the policyholder. Non-life insurance policies offer financial protection to a person for health issues or losses due to damage to an asset. Denmark life & non-life insurance market is segmented by insurance type (life insurance (individual and group), non-life insurance (motor, home, health, and other non-life insurances)), and by distribution channel (direct, agency, banks, online, and other distribution channels). The report offers market size and forecasts for Denmark's life & non-life insurance market in value (USD billion) for all the above segments.

By Insurance Type

| Life Insurance | |

| Non-Life Insurance | Motor Insurance |

| Health Insurance | |

| Property Insurance | |

| Liability Insurance | |

| Other Insurance |

By Customer Segment

| Retail |

| Corporate |

By Distribution Channel

| Brokers |

| Agents |

| Banks |

| Direct Sales |

| Other Channels |

| By Insurance Type | Life Insurance | |

| Non-Life Insurance | Motor Insurance | |

| Health Insurance | ||

| Property Insurance | ||

| Liability Insurance | ||

| Other Insurance | ||

| By Customer Segment | Retail | |

| Corporate | ||

| By Distribution Channel | Brokers | |

| Agents | ||

| Banks | ||

| Direct Sales | ||

| Other Channels | ||

Key Questions Answered in the Report

What is the current value of the Denmark life and non-life insurance market?

The market was worth USD 46.07 billion in 2026 and is set to reach USD 61.32 billion by 2031.

How fast is the sector expected to grow?

It is forecast to post a 5.88% CAGR between 2026 and 2031, led by non-life lines expanding at a 7.12% CAGR.

Which insurance type holds the largest share?

Life products dominate with 74.56% of total premiums, owing to compulsory occupational pension schemes.

Which distribution channel is gaining ground quickest?

Direct digital sales are growing at a 6.86% CAGR as consumers favor online purchasing pathways.

Page last updated on: