Project Management Software Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

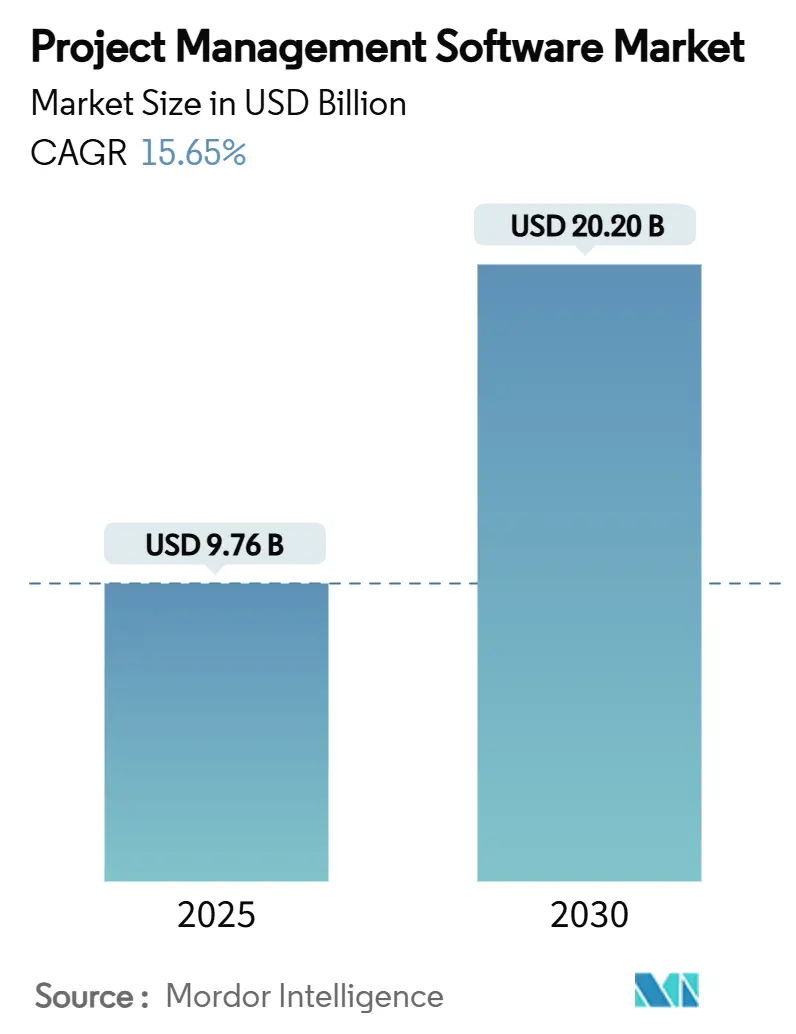

| Market Size (2025) | USD 9.76 Billion |

| Market Size (2030) | USD 20.20 Billion |

| Growth Rate (2025 - 2030) | 15.65% CAGR |

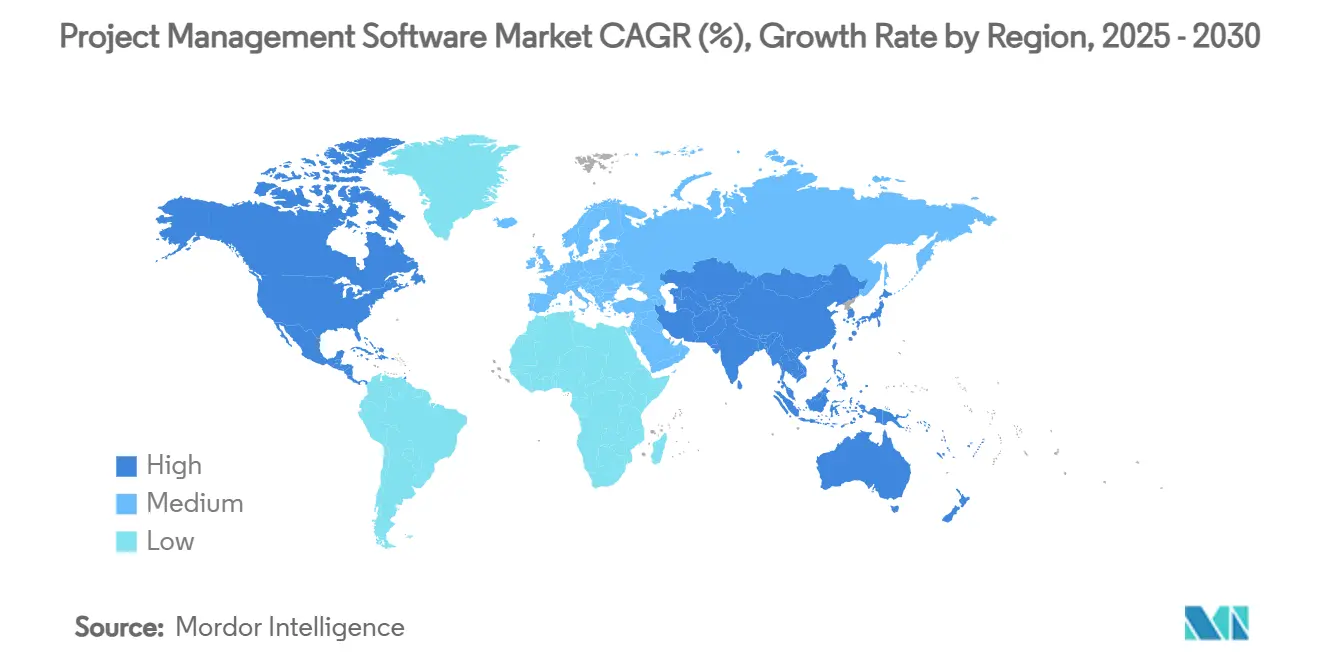

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

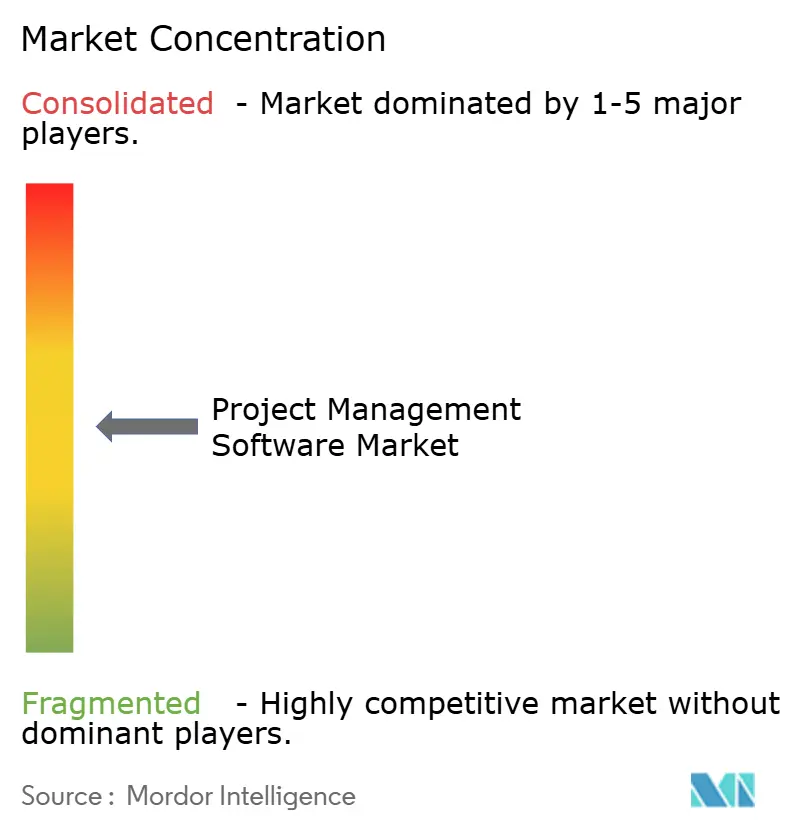

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Project Management Software Market Analysis by Mordor Intelligence

The project management software market stands at USD 9.76 billion in 2025 and is advancing at a 15.65% CAGR toward USD 20.20 billion by 2030. Expansion remains anchored in cloud-first deployment, low-code configurability, and predictive analytics that collectively upgrade project oversight from task tracking to strategic orchestration. Demand intensifies as distributed teams require real-time collaboration, and enterprises integrate project data with finance, HR, and customer systems for unified visibility. Hybrid deployment registers the fastest growth because regulated industries still need local data control. Small and medium enterprises (SMEs) accelerate adoption by bypassing traditional implementation hurdles, while AI-native features strengthen risk management and cost forecasting. Competitive intensity increases as vendors embed industry-specific workflows and open API ecosystems.

Key Report Takeaways

- By deployment, cloud services held 75% of the project management software market share in 2024, whereas hybrid models post the highest 18.4% CAGR through 2030.

- By organization size, large enterprises represented 61.1% of revenue in 2024, while SMEs expand at a 17.2% CAGR.

- By end-user industry, IT & Telecom led with 28.4% revenue in 2024; healthcare grows fastest at 16.1% CAGR to 2030.

- By subscription type, annual plans captured 53.2% of revenue in 2024, outpacing other contract options.

- By geography, North America commanded 36.5% of the project management software market share in 2024, but Asia-Pacific registers the strongest 15.3% CAGR through 2030.

Global Project Management Software Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-first adoption for remote and hybrid teams | +3.2% | North America, Europe | Short term (≤ 2 years) |

| Integration of PM platforms with SaaS stacks | +2.8% | North America, Asia-Pacific | Medium term (2-4 years) |

| SME uptake through low-code configurability | +2.1% | Asia-Pacific, Latin America | Medium term (2-4 years) |

| AI-driven predictive analytics | +1.9% | North America, Europe | Long term (≥ 4 years) |

| Vertical-specific PM suites | +1.4% | Global | Medium term (2-4 years) |

| ESG compliance reporting | +0.8% | Europe, North America | Long term (≥ 4 years) |

Source: Mordor Intelligence

Cloud-First Adoption for Remote and Hybrid Project Teams

Organizations report 54% faster task completion when shifting from desktop tools to cloud-native platforms[1]Dustin Moskovitz, “Work Innovation at Scale,” asana.com. The project management software market gains traction because real-time synchronization enables distributed teams to sustain momentum across time zones. IT departments prefer cloud scalability that removes capacity planning burdens. Hybrid models grow at 18.4% CAGR because regulated sectors balance accessibility with data control. Vendors respond by offering data-residency options that satisfy sovereignty mandates while keeping collaboration friction-free.

Integration of PM Platforms with Enterprise SaaS Stacks

Enterprises run an average of 976 applications, yet only 28% are meaningfully integrated, stalling project data flow. Modern platforms position themselves as integration hubs tied to finance, CRM, and HR systems, raising the project management software market relevancy in enterprise architecture. The SaaS integration segment is projected to exceed USD 15 billion by 2025, and firms that deploy comprehensive integration strategies report 30% productivity lifts. Cloud-native vendors gain an advantage through open APIs and pre-built connectors that curb expensive custom coding.

SME Uptake Boosted by Low-Code / No-Code Configurability

Low-code builders eliminate months-long implementations, allowing SMEs to launch in weeks and align spend with cash cycles. The shift democratizes advanced features once exclusive to large enterprises, propelling SME demand within the project management software market. Asia-Pacific SMEs adopt aggressively as manufacturing and services sectors digitize. Vendors streamline onboarding through guided templates that maintain enterprise-grade depth when required.

AI-Driven Predictive Analytics for Schedule and Cost Variance

Eighty-two percent of executives expect AI to reinvent project management within five years. Algorithms surface early-stage schedule slips and budget overruns so managers act proactively. Construction projects using AI cost tracking save 5-10% on materials by intercepting errors. Early deployments reside in North America and Europe because data quality and analytics talent are prerequisites, but broader adoption will follow as packaged AI modules reach mid-market buyers.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High migration and customization costs | -2.4% | Global | Short term (≤ 2 years) |

| Data-sovereignty and privacy constraints | -1.8% | Europe, Asia-Pacific | Medium term (2-4 years) |

| Feature commoditization and vendor lock-in | -1.1% | Global | Long term (≥ 4 years) |

| Change-management fatigue | -0.9% | North America, Europe | Medium term (2-4 years) |

Source: Mordor Intelligence

High Migration and Customization Costs for Legacy Estates

Enterprises face implementation bills that triple license fees because data mapping, validation, and user training are labor intensive. Migration overruns average 30% and can reach USD 15,000 per terabyte of archives. The hurdle delays refresh cycles and slows the project management software market uptake among incumbents with heavily customized workflows.

Data-Sovereignty and Privacy Concerns in Multi-Tenant Clouds

GDPR and region-specific localization rules complicate pure-cloud rollouts, especially in healthcare and finance. Hybrid deployments, therefore, persist as enterprises keep sensitive artifacts on-premise while benefiting from cloud collaboration. Compliance documentation and breach-response planning also raise operating overhead, tempering project management software market growth in regulated economies.

Segment Analysis

By Deployment: Hybrid Models Bridge Security Gaps

Cloud deployment held 75% of revenue in 2024, but hybrid configurations grow at 18.4% CAGR, signalling the strongest momentum inside the project management software market. Hybrid solutions synchronize local repositories with cloud workspaces; this duality attracts firms bound by data residency statutes. On-premise persists in government and defense, yet its share shrinks as security certifications for cloud zones tighten.

The hybrid rise reflects tools that now manage seamless offline sync, encrypted tunnels, and selective storage. Construction companies keep drawings on local servers yet share field updates through cloud dashboards[2]Autodesk Construction Cloud, “Hybrid Collaboration in Construction,” autodesk.com. Vendors differentiate by offering granular tenancy controls, creating upsell paths around compliance.

By Organization Size: SMEs Drive Market Democratization

Large enterprises controlled 61.1% of 2024 spend, but SMEs chart a 17.2% CAGR that reshapes the project management software market size trajectory. Growth centers on Asia-Pacific, where local governments fund digital upskilling grants. Japanese SMEs adopt AI-assisted scheduling to offset labor shortages. Pricing tiers remove user minimums, reducing the barrier to entry.

Enterprise growth plateaus in saturated regions, so vendors launch light editions and community events geared to smaller firms. Yet, multi-national corporations still anchor revenue with complex integrations and premium analytics bundles. Dual focus forces product teams to maintain scalability without complicating onboarding.

By End-User Industry: Healthcare Leads Vertical Specialization

IT and Telecom held 28.4% revenue in 2024, but healthcare posts the fastest 16.1% CAGR, leveraging compliance-ready templates for patient safety and capital projects. Construction follows, motivated by rising material volatility that raises demand for predictive costing. Hospitals deploy Procore to manage USD 3 billion programs and remove manual spreadsheets.

Specialization sparks new bundles: clinical trial tracking modules, Building Information Modeling (BIM) connectors, and ESG reporting dashboards. Vendors partner with regulatory bodies to certify workflows, giving them pricing power and stickier renewals within the project management software market.

By Subscription Type: Annual Models Dominate Enterprise Preferences

Annual contracts captured 53.2% of 2024 revenue, reflecting the CFO's preference for budget predictability in the project management software market. Monthly plans remain popular among startups that need staffing flexibility. One-time licenses fade as perpetual models clash with cloud updates.

Vendors test usage-based overlays that add AI credits or advanced analytics once consumption passes set thresholds. Monday.com grants 500 free credits each month to entice experimentation while preserving transparent add-on rates. Alignment of pricing to value achieved keeps churn low.

Geography Analysis

North America held 36.5% of the project management software market in 2024. Enterprises there leverage robust infrastructure and sizable IT budgets to roll out end-to-end project ecosystems. Microsoft recorded 16% revenue growth to USD 245 billion in 2024, supported by integrated project functions within Microsoft 365[3]Microsoft Corporation, “Annual Report 2024,” microsoft.com. Innovation hubs continue to pioneer AI modules, yet regional growth moderates as penetration nears saturation.

Asia-Pacific grows at 15.3% CAGR through 2030, the fastest across regions. China’s SaaS segment expands near 30% annually, with multinationals installing integrated Salesforce and Azure stacks to manage cross-border initiatives. India’s SaaS revenue is forecast to increase from USD 7.18 billion in 2023 to USD 62.93 billion by 2032, driven by cloud adoption and startup momentum. SMEs across Southeast Asia adopt local-language PM suites that embed regional compliance norms.

Europe posts steady gains as GDPR compels localization features, rewarding vendors offering EU data centers and advanced encryption. South America, and Middle East, and Africa now improve broadband and payment rails, nurturing cloud subscriptions previously held back by infrastructure gaps. Vendors anticipate double-digit uptake once connectivity costs fall further.

Competitive Landscape

The project management software market is moderately fragmented. Microsoft deploys ecosystem leverage across Office, Azure, and Teams. Asana reported USD 188.3 million Q4 2025 revenue and positive free cash flow after launching AI Studio that automates routine workflows. Monday.com focuses on modular AI Blocks and Digital Workforce capabilities aimed at scale deployments. Atlassian maintains dominance with developer-centric Jira integration.

Disruptors like ClickUp, valued at USD 4 billion, bet on unified workspaces that converge docs, chat, and goals. Celoxis introduced Lex, an AI assistant for proactive risk alerts. Specialist players target niches: Procore in construction, Pulsora in ESG data, Suits Inc. in Japan’s SME sector. Acquisition activity rises as incumbents buy vertical features or AI engines to keep pace.

Robust API ecosystems remain decisive because enterprises prize seamless data flow. Platforms with open standards outcompete feature-rich but closed suites, underlining integration as a differentiator in renewal cycles. Pricing innovation, especially consumption-based extensions, further defines competitive posture.

Project Management Software Industry Leaders

-

Microsoft Corporation

-

SAP SE

-

Broadcom Inc. (CA Technologies)

-

Oracle Corporation

-

ServiceNow Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Asana posted Q4 2025 revenue of USD 188.3 million, reflecting 10% year-over-year growth and expanding AI Studio uptake.

- February 2025: Monday.com unveiled its AI Vision roadmap, adding AI Blocks, Product Power-ups, and Digital Workforce features with 500 monthly free credits to spur adoption.

- February 2025: Celoxis released Lex, an AI project assistant that predicts schedule slips and resource needs.

- December 2024: Microsoft’s 2024 annual report showed 16% revenue growth to USD 245 billion, citing productivity cloud services as a key driver.

Global Project Management Software Market Report Scope

Project management software is software that is used for various purposes in a project, such as planning, scheduling, resource allocation, and change management. It allows project managers, stakeholders, and users to control costs and manage budgeting, quality management, and documentation. It can also be used as an administration system.

The market is segmented by Type of Deployment (Cloud-based, On-premises), End-user Vertical (Oil and Gas, IT and Telecom, Healthcare, Government, Other End-user Verticals), and Geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value in USD billion for all the above segments.

| By Deployment | Cloud | |||

| On-premise | ||||

| By Organization Size | Large Enterprises | |||

| Small and Medium Enterprises | ||||

| By End-user Industry | IT and Telecom | |||

| Healthcare | ||||

| Construction and Infrastructure | ||||

| BFSI | ||||

| Government and Public Sector | ||||

| Manufacturing | ||||

| Others | ||||

| By Subscription Type | Monthly Subscription | |||

| Annual Subscription | ||||

| One-time License | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| South America | Brazil | |||

| Argentina | ||||

| Rest of South America | ||||

| Europe | United Kingdom | |||

| Germany | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| Nordics | ||||

| Rest of Europe | ||||

| Middle East and Africa | Middle East | Saudi Arabia | ||

| United Arab Emirates | ||||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Egypt | ||||

| Nigeria | ||||

| Rest of Africa | ||||

| Asia-Pacific | China | |||

| India | ||||

| Japan | ||||

| South Korea | ||||

| ASEAN | ||||

| Australia | ||||

| New Zealand | ||||

| Rest of Asia-Pacific | ||||

| Cloud |

| On-premise |

| Large Enterprises |

| Small and Medium Enterprises |

| IT and Telecom |

| Healthcare |

| Construction and Infrastructure |

| BFSI |

| Government and Public Sector |

| Manufacturing |

| Others |

| Monthly Subscription |

| Annual Subscription |

| One-time License |

| North America | United States | ||

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordics | |||

| Rest of Europe | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

Key Questions Answered in the Report

What is the projected value of the project management software market by 2030?

The market is forecast to reach USD 20.20 billion by 2030.

Which deployment model is growing fastest?

Hybrid deployment is expanding at an 18.4% CAGR as firms balance cloud access with data sovereignty needs.

Why are SMEs adopting project management platforms more quickly than before?

Low-code configurability now lets non-technical teams deploy and tailor solutions in weeks, removing historical cost and complexity barriers.

Which industry vertical shows the highest growth through 2030?

Healthcare leads with a 16.1% CAGR due to stringent regulatory requirements and complex capital projects.

Page last updated on: July 10, 2025