Market Overview

| Study Period | 2021 - 2031 |

|---|---|

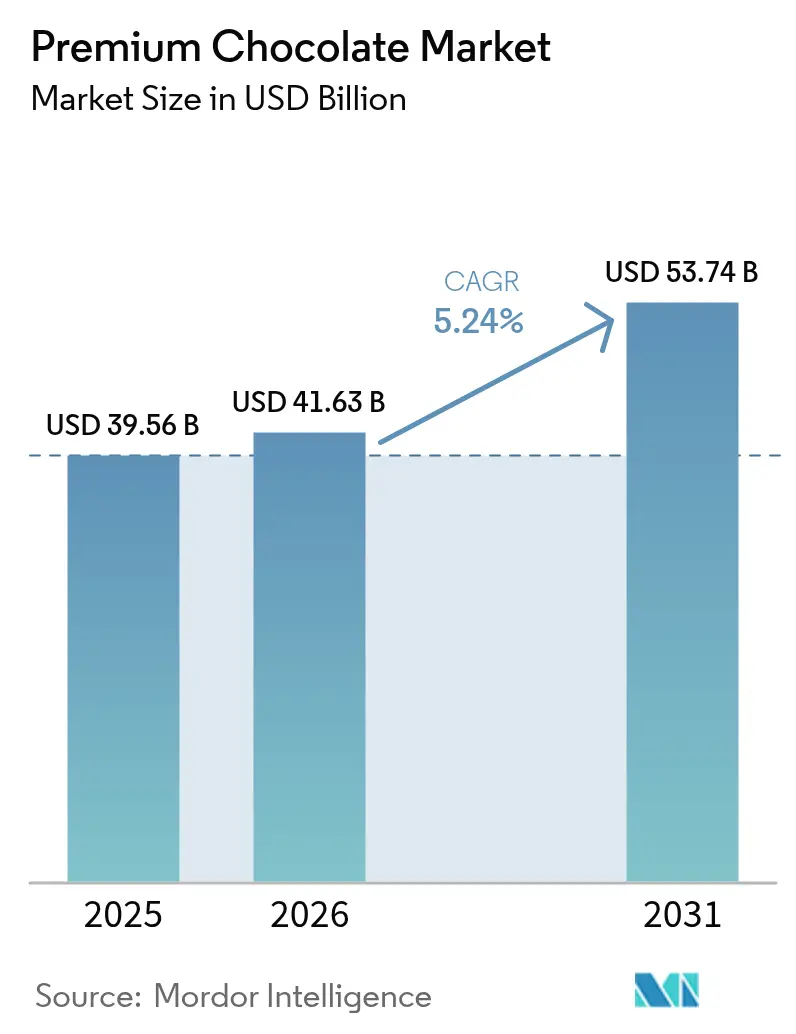

| Market Size (2026) | USD 41.63 Billion |

| Market Size (2031) | USD 53.74 Billion |

| Growth Rate (2026 - 2031) | 5.24% CAGR |

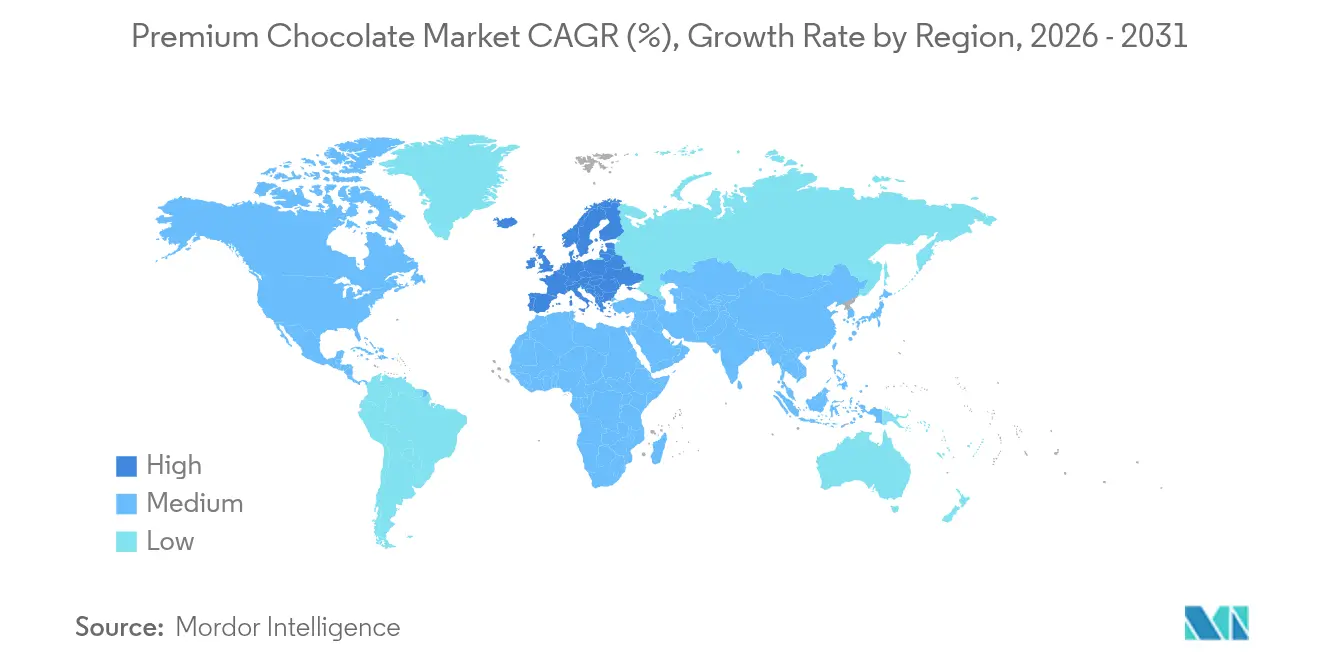

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

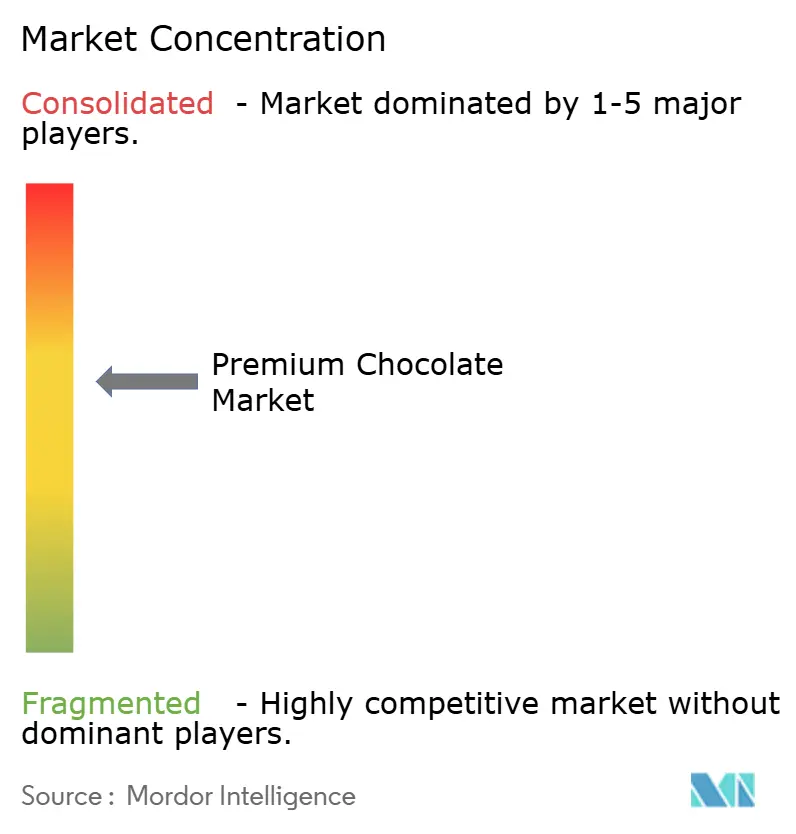

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Premium Chocolate Market Analysis by Mordor Intelligence

The premium chocolate market size is expected to grow from USD 39.56 billion in 2025 to USD 41.63 billion in 2026 and is forecast to reach USD 53.74 billion by 2031 at 5.24% CAGR over 2026-2031. This market is driven by increasing consumer demand for high-quality, artisanal, and ethically sourced chocolate products. Factors such as rising disposable incomes, growing awareness of premium product offerings, and the influence of gifting culture contribute significantly to the market's growth. Additionally, the trend of health-conscious consumers seeking dark chocolate for its perceived health benefits further supports market expansion. The premium chocolate market is also witnessing innovation in flavors, packaging, and sustainable sourcing practices, which are attracting a broader consumer base. These dynamics are expected to shape the market's trajectory during the forecast period.

Key Report Takeaways

- By product type, Premium Milk/White Chocolate led with 62.92% of premium chocolate market share in 2025; Dark Milk Chocolate is forecast to expand at a 7.05% CAGR through 2031.

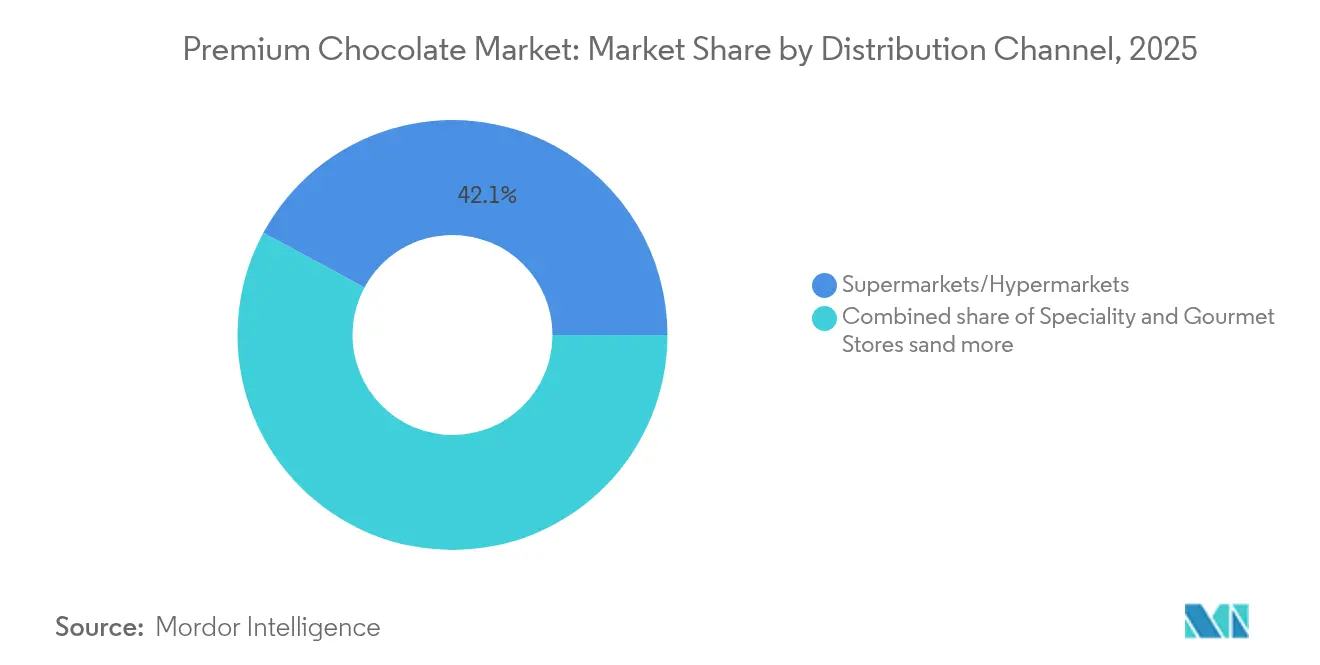

- By distribution channel, Supermarkets/Hypermarkets captured 42.12% of the premium chocolate market size in 2025, while Online Retail is projected to grow at an 7.94% CAGR between 2026-2031.

- By geography, Europe held 33.12% revenue share of the premium chocolate market in 2025; Asia-Pacific is advancing at a 6.92% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Premium Chocolate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization as "Affordable Luxury" post-pandemic | +1.2% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Rise of single-origin and bean-to-bar certifications | +0.8% | Europe and North America core, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Growing e-commerce penetration for gourmet gifting | +1.1% | Global, with early gains in Asia-Pacific and North America | Short term (≤ 2 years) |

| Functional and better-for-you formulations | +0.7% | North America and Europe, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Carbon-neutral product labels influencing purchase decisions | +0.6% | Europe core, expanding globally | Long term (≥ 4 years) |

| AI-enabled flavor innovation shortening research and development cycles | +0.4% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premiumization as "affordable luxury" post-pandemic

Post-pandemic, "affordable luxury" has emerged as the hallmark of premiumization, driving growth in the premium chocolate market. Consumers are increasingly seeking high-quality products that offer indulgence without being prohibitively expensive. This trend reflects a shift in purchasing behavior, where individuals prioritize value and experience, even in everyday treats. Premium chocolate brands are capitalizing on this demand by offering products that balance luxury and affordability, appealing to a broader audience. The emphasis on unique flavors, sustainable sourcing, and artisanal craftsmanship further enhances the appeal of premium chocolates as an accessible luxury option. Supporting this trend, Jordbruksverket reported that Sweden's per capita consumption of chocolate and confectionery increased to 16.4 kg in 2023, up from 15.8 kg in 2021 [1]Source: Jordbruksverket, "Per capita consumption of chocolate and confectionery in Sweden", statistik.sjv.se. This rise in consumption highlights the growing demand for chocolate products, including premium offerings, as consumers increasingly view chocolate as a means of affordable indulgence. The data underscores the expanding market potential for premium chocolate, driven by evolving consumer preferences for products that combine quality, taste, and an element of luxury.

Rise of single-origin and bean-to-bar certifications

Consumers increasingly demand transparency and authenticity in premium chocolate, making single-origin and bean-to-bar certifications vital differentiation tools. The European market drives this trend, with tree-to-bar products becoming the fastest-growing segment in premium chocolate. These products cater to discerning consumers who seek unique flavor profiles and ethical sourcing narratives [2]Source: Centre for the Promotion of Imports from Developing Countries (CBI), "Entering the European market for tree-to-bar chocolates", cbi.eu. This trend goes beyond marketing, prompting manufacturers to restructure supply chains fundamentally. They establish direct relationships with cocoa farmers to ensure quality control and traceability. This movement aligns with EUDR compliance mandates, blending regulatory requirements with consumer preferences for transparency. Bean-to-bar producers leverage their artisanal image to command premium prices and foster brand loyalty through compelling storytelling and exclusive limited-edition releases. The certification landscape continues to evolve, incorporating blockchain-based traceability systems. These systems enable real-time verification of origin claims, strengthening premium pricing strategies through authenticated legitimacy.

Growing e-commerce penetration for gourmet gifting

Premium chocolate is increasingly moving online, outpacing traditional retail channels. This shift is fueled by the ability to personalize offerings and foster direct relationships with consumers. Digital platforms are not just selling chocolates; they're crafting tailored gifting experiences and subscription models, boosting customer loyalty and lifetime value. Gourmet gifting has seen a pronounced shift online, with digital platforms offering better product curation, customizable packaging, and precise delivery timing than brick-and-mortar stores. This evolution in channels is reshaping competition, empowering smaller artisanal brands to tap into global markets without relying on conventional distribution partnerships. Furthermore, these digital platforms gather insights on consumer preferences, facilitating predictive inventory management and tailored product suggestions, which in turn, encourage repeat purchases. The trend is most evident in the Asia-Pacific and North America regions, bolstered by robust digital payment systems and logistics networks that ensure smooth e-commerce transactions for premium chocolates.

Functional and better-for-you formulations

Functional chocolate formulations are reshaping product development strategies across the premium segment by incorporating adaptogens, reduced sugar, and health-enhancing ingredients. These formulations reflect a growing wellness consciousness, with manufacturers including ingredients such as ashwagandha, collagen, and plant-based proteins while maintaining indulgent taste profiles. Balancing functional benefits with chocolate's traditional pleasure positioning poses a challenge, requiring manufacturers to use sophisticated ingredient technology and educate consumers. Premium brands are leveraging functional formulations to justify higher price points and attract health-conscious consumers who previously avoided chocolate categories. Research from ETH Zurich demonstrates scientific advancements in this area, showcasing cocoa gel alternatives that replace sugar while enhancing nutritional profiles. The functional chocolate segment is driving opportunities for cross-category partnerships with nutraceutical companies and positioning chocolate as a wellness product rather than purely an indulgent confection.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cocoa-price volatility | -1.8% | Global, with strongest impact in price-sensitive markets | Short term (≤ 2 years) |

| Counterfeit and diluted "premium" offerings eroding trust | -0.9% | Global, concentrated in emerging markets | Medium term (2-4 years) |

| Supply-chain traceability compliance costs (EU Deforestation Law) | -1.1% | Europe core, global supply chain impact | Short term (≤ 2 years) |

| Intensifying competition from artisanal local makers | -0.7% | North America and Europe, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cocoa-price volatility

Unprecedented cocoa price volatility poses the most significant threat to market stability, with prices fluctuating from USD 2,000 per ton in 2023 to peaks exceeding USD 12,000 in 2024 before declining over 30% in early 2025 [3]Source: Anadolu Ageny (AA), "Cocoa prices drop over 30% in 2025 after last year’s record high", aa.com.tr. This volatility creates operational challenges for premium chocolate manufacturers, who must balance cost pass-through with consumer price sensitivity while maintaining margin targets. Hershey's request for CFTC approval to purchase over 90,000 metric tons of cocoa demonstrates the extreme measures companies are taking to secure supply and manage price risk. The volatility stems from structural supply issues in West Africa, climate change impacts, and speculative trading activity that amplifies price movements beyond fundamental supply-demand dynamics. Premium brands face particular challenges as their positioning requires consistent quality and availability, making supply chain disruption more damaging than for mass-market products. The situation is forcing manufacturers to explore alternative ingredients and diversify sourcing strategies, potentially reshaping the fundamental composition of premium chocolate products.

Supply-chain traceability compliance costs

Smaller premium chocolate manufacturers, often resource-strapped, grapple with the EU Deforestation Regulation's stringent compliance demands. These requirements encompass geolocation data collection, risk assessments, and due diligence statements for each cocoa batch. Non-compliance could lead to hefty fines, capping at 4% of an entity's EU turnover. Set for a December 2024 rollout, the regulation's potential push to 2025 adds layers of uncertainty, muddling supply chain strategies and investment choices. Without the means to prove compliance, smaller premium brands risk being sidelined from EU markets. This scenario could pave the way for larger players, boasting robust traceability systems, to tighten their grip on market share. Compliance costs aren't limited to direct outlays; they ripple through the supply chain, necessitating farmer training and tech investments, often with delayed returns. Yet, brands that navigate these waters early stand to gain. By showcasing verified sustainability credentials, they can carve out a marketing edge, potentially recouping compliance costs through premium pricing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Milk Chocolate Dominates Despite Dark Innovation

In 2025, Premium Milk/White Chocolate holds a commanding 62.92% market share, highlighting its strong consumer preference for familiar and universally appealing flavor profiles. This segment's dominance is driven by its ability to cater to a broad demographic base, including children and adults, making it a staple choice in the premium chocolate market. The versatility of milk and white chocolate in various applications, such as gifting, celebrations, and everyday indulgence, further reinforces its market leadership. Additionally, its sweeter and creamier taste profile aligns with traditional consumer preferences, ensuring sustained demand across regions. However, the segment's growth trajectory indicates signs of maturation, as evolving consumer preferences and market saturation may limit its expansion potential in the coming years.

On the other hand, Premium Dark Chocolate is carving out a distinct niche, driven by increasing health consciousness and a demand for sophisticated flavor experiences. Dark Milk Chocolate, a subcategory within this segment, is emerging as the fastest-growing category with a projected CAGR of 7.05% during the forecast period (2026-2031). This growth is fueled by the intersection of wellness trends and indulgence, as dark chocolate's antioxidant properties provide a health-oriented justification for its premium pricing. The segment also benefits from a growing consumer base that values authenticity and craftsmanship, with single-origin and high-cacao content products gaining traction. Premium Dark Chocolate appeals to connoisseurs and health-conscious consumers alike, offering a balance of indulgence and perceived health benefits.

By Distribution Channel: Supermarkets/Hypermarkets Dominates, Online Retail Accelerates

In 2025, Supermarkets and Hypermarkets dominate the premium chocolate market's distribution channels, holding a significant 42.12% share. These outlets thrive on their ability to cater to established consumer shopping habits, where customers often prefer the convenience of purchasing a variety of products in one location. The strategic placement of premium chocolates near checkout counters or high-traffic areas within these stores plays a crucial role in driving impulse purchases, which are a key contributor to sales in this segment. Moreover, supermarkets and hypermarkets offer consumers the advantage of physically inspecting products, which is particularly important for premium chocolates, as buyers often seek to assess packaging, quality, and freshness before making a purchase. The availability of promotional discounts, bundled offers, and seasonal displays further enhances the appeal of these channels, making them a preferred choice for both regular and occasional buyers of premium chocolates.

Conversely, Online Retail is rapidly reshaping the premium chocolate market and is projected to grow at an impressive CAGR of 7.94% during the forecast period of 2026-2031. Digital platforms provide unparalleled convenience, allowing consumers to shop from the comfort of their homes while accessing a wide array of premium chocolate options, including niche and artisanal brands that may not be readily available in physical stores. The ability to offer personalized shopping experiences, such as tailored recommendations based on browsing history or preferences, sets online retail apart from traditional channels. Subscription-based models, which ensure regular delivery of premium chocolates, are gaining traction among consumers seeking convenience and exclusivity.

Geography Analysis

In 2025, Europe secures a commanding 33.12% share of the market, propelled by discerning consumers favoring premium chocolate and stringent regulations prioritizing quality over price. Europe's dominance is underscored by a rich cultural reverence for chocolate artistry, well-established distribution channels for premium offerings, and a consumer base willing to pay a premium for sustainability and quality assurances. The region enjoys proximity to traditional cocoa trading hubs and nurtured ties with West African suppliers, although evolving EUDR compliance mandates are altering these relationships. While Europe's mature market indicates tempered growth rates, its elevated per-capita consumption values bolster strategies centered on premium positioning.

Asia-Pacific stands out as the region with the most robust growth trajectory, boasting a 6.92% CAGR from 2026 to 2031. This surge is driven by increasing disposable incomes, a westernized palate, and a burgeoning appreciation for premium chocolate. As the third-largest cocoa producer, Indonesia holds a pivotal role, offering strategic benefits for the region's premium chocolate sector. This not only curtails supply chain expenses but also crafts distinctive narratives that set Asian premium brands apart. Within this landscape, China and India shine as the brightest prospects, buoyed by their swelling middle classes and heightened exposure to premium chocolate, thanks to global travel and digital platforms.

In North America, robust purchasing power and a trend towards premiumization bolster chocolate consumption. Yet, economic uncertainties are causing a rift, with consumers increasingly discerning between essential buys and luxury treats. The U.S. leads the regional consumption charge, while Canada and Mexico present fertile ground for growth, driven by their burgeoning middle classes and heightened encounters with premium chocolate. South America, straddling the line as both a cocoa producer and consumer, sees Brazil and Argentina spearheading the surge in premium chocolate consumption. Meanwhile, the Middle East and Africa are on the cusp of a chocolate renaissance, with the UAE emerging as a pivotal hub for premium chocolate distribution and consumption, buoyed by its affluent populace and global exposure.

Competitive Landscape

The premium chocolate market showcases a fragmented competition landscape that presents significant opportunities for strategic consolidation and niche positioning. Established multinational corporations such as Mars, Ferrero, and Hershey dominate the market by leveraging their scale advantages and extensive distribution networks. However, these large players face growing competition from artisanal local makers, who differentiate themselves through authenticity, sustainability, and personalized experiences. These attributes resonate strongly with a segment of consumers, creating a competitive dynamic where smaller players can carve out meaningful market share despite the dominance of larger corporations.

Strategic trends within the market reveal a clear bifurcation in approaches. On one hand, some companies focus on volume-driven efficiency strategies, aiming to maximize economies of scale and streamline operations. On the other hand, premium-focused differentiation strategies are gaining traction, with companies emphasizing high-quality ingredients, unique flavors, and luxury branding. Increasingly, successful players are adopting hybrid models that combine the strengths of both approaches. These models enable companies to manage costs effectively through scale while maintaining a premium brand image by offering targeted product lines and engaging directly with consumers through specialized channels.

Technology adoption has emerged as a critical factor in gaining a competitive edge within the premium chocolate market. Companies like Mondelez are at the forefront of this trend, investing in innovative solutions such as cultured cocoa biotechnology. Through partnerships with firms like Celleste Bio, Mondelez aims to address vulnerabilities in the supply chain while ensuring consistent product quality. This technological focus not only enhances operational resilience but also aligns with consumer demand for sustainable and ethically sourced products, further strengthening the competitive positioning of forward-thinking companies in the market.

Premium Chocolate Industry Leaders

-

Chocoladefabriken Lindt & Sprüngli AG

-

Ferrero International S.A.

-

Mondelēz International, Inc.

-

Nestlé S.A.

-

Mars, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Colombia's Cacao Hunters, the nation's most lauded premium chocolate brand, has officially debuted in the U.S. Celebrated for its single-origin chocolates and dedication to ethical sourcing, Cacao Hunters introduces a vibrant taste of South American artistry to American chocolate aficionados. U.S. shoppers can now explore Cacao Hunters' premium offerings, featuring dark and milk chocolate bars crafted from rare varietals, infused with distinctive regional flavors, all while upholding the highest standards of quality and ethics.

- October 2024: Godiva, the premium chocolate brand founded in Belgium, has unveiled its limited-edition Heritage Collection, marking its debut in the U.S. market. With nearly a century of history, Godiva has consistently made headlines in North America, especially as luxury products gain traction among consumers. The Heritage Collection features 12 distinct chocolate and confection pieces, all meticulously crafted in Brussels.

- January 2024: As part of its strategy to diversify product offerings, Mars, Incorporated has acquired Hotel Chocolat, a prominent premium chocolate brand in the UK. With this acquisition, Mars aims to bolster its foothold in the premium chocolate sector and capitalize on Hotel Chocolat's established brand recognition across Europe.

- January 2024: Haldiram's has introduced 'Cocobay,' a premium chocolate brand, to the Indian market. The brand asserts that all its offerings are made from 100% pure cocoa. The debut collection boasts distinct fruit and spice flavors, curated specifically for Indian palates.

Global Premium Chocolate Market Report Scope

Premium chocolates are typically high-quality chocolate variants compared to regular or mass-produced chocolate. It often involves the use of higher-quality cocoa beans with attention to detail in flavor, texture, and presentation.

The premium chocolate market is segmented based on product type, distribution channel, and geography. By product type, the market is segmented into dark and white and milk premium chocolates. The market is segmented by distribution channel into hypermarkets/supermarkets, convenience stores, online retail stores, and other distribution channels. By geography, the report analyzes established and emerging economies worldwide, including North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, market sizing and forecasts were made based on the value (USD million).

By Product Type

| Premium Dark Chocolate |

| Premium Milk/White Chocolate |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Specialty and Gourmet Stores |

| Online Retail |

| Other Distribution Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Rest of Middle East and Africa |

| By Product Type | Premium Dark Chocolate | |

| Premium Milk/White Chocolate | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty and Gourmet Stores | ||

| Online Retail | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the premium chocolate market in 2026?

The premium chocolate market size totals USD 41.63 billion in 2026.

What is the forecast CAGR for premium chocolate through 2031?

The sector is projected to grow at a 5.24% CAGR between 2026 and 2031.

Which product segment leads in revenue?

Premium Milk/White Chocolate holds 62.92% of premium chocolate market share in 2025.

Which sales channel is growing fastest?

Online Retail is expanding at an 7.94% CAGR during 2026-2031.

Which region offers the highest growth outlook?

Asia-Pacific shows a 6.92% CAGR, outperforming other regions through 2031.

Page last updated on: