Prefabricated Building System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

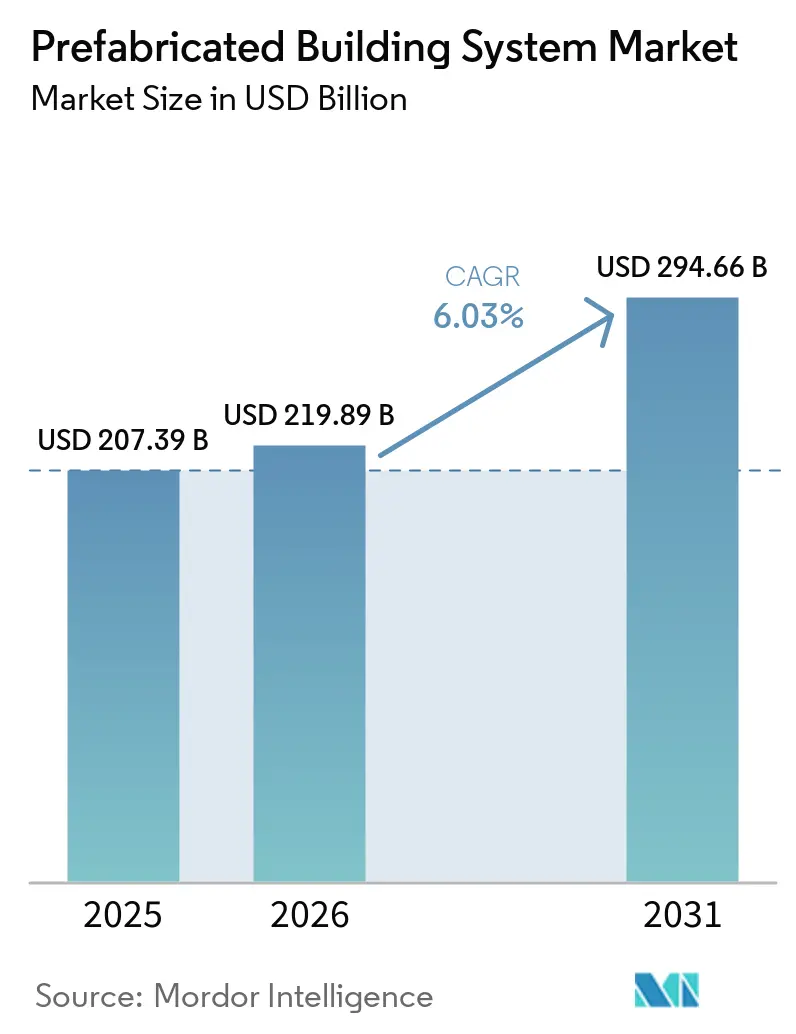

| Market Size (2026) | USD 219.89 Billion |

| Market Size (2031) | USD 294.66 Billion |

| Growth Rate (2026 - 2031) | 6.03% CAGR |

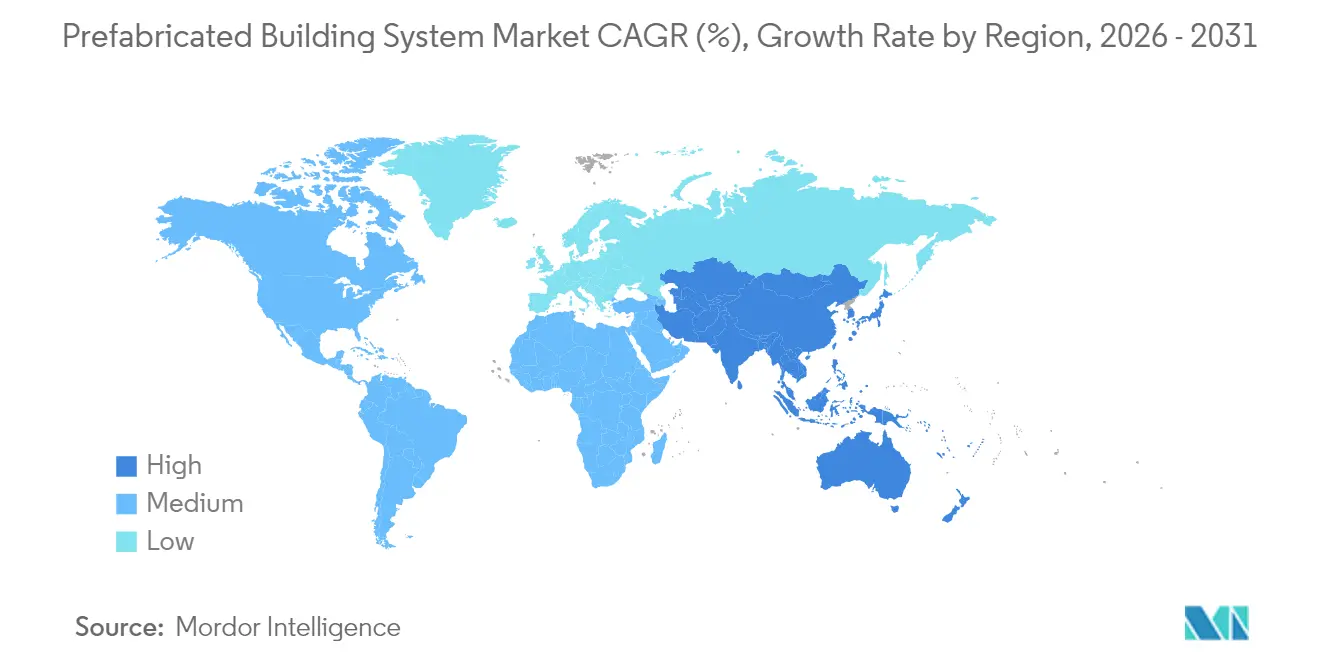

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Prefabricated Building System Market Analysis by Mordor Intelligence

The Prefabricated Building System market size is expected to grow from USD 207.39 billion in 2025 to USD 219.89 billion in 2026 and is forecast to reach USD 294.66 billion by 2031 at 6.03% CAGR over 2026-2031. Current expansion is underpinned by labor shortages, policy incentives, and technology that delivers factory-level precision at construction-site scale. Rising urban household formation, worsening housing affordability, and mandatory green-building codes are pushing public agencies and private developers toward off-site manufacturing solutions that cut on-site work by more than 50%. Consolidation is intensifying as leading suppliers integrate design, production, and assembly to capture margin across the value chain. Logistics optimization, fire-safety code harmonization, and continued material innovation remain decisive levers for sustaining growth momentum within the prefabricated building systems market.

Key Report Takeaways

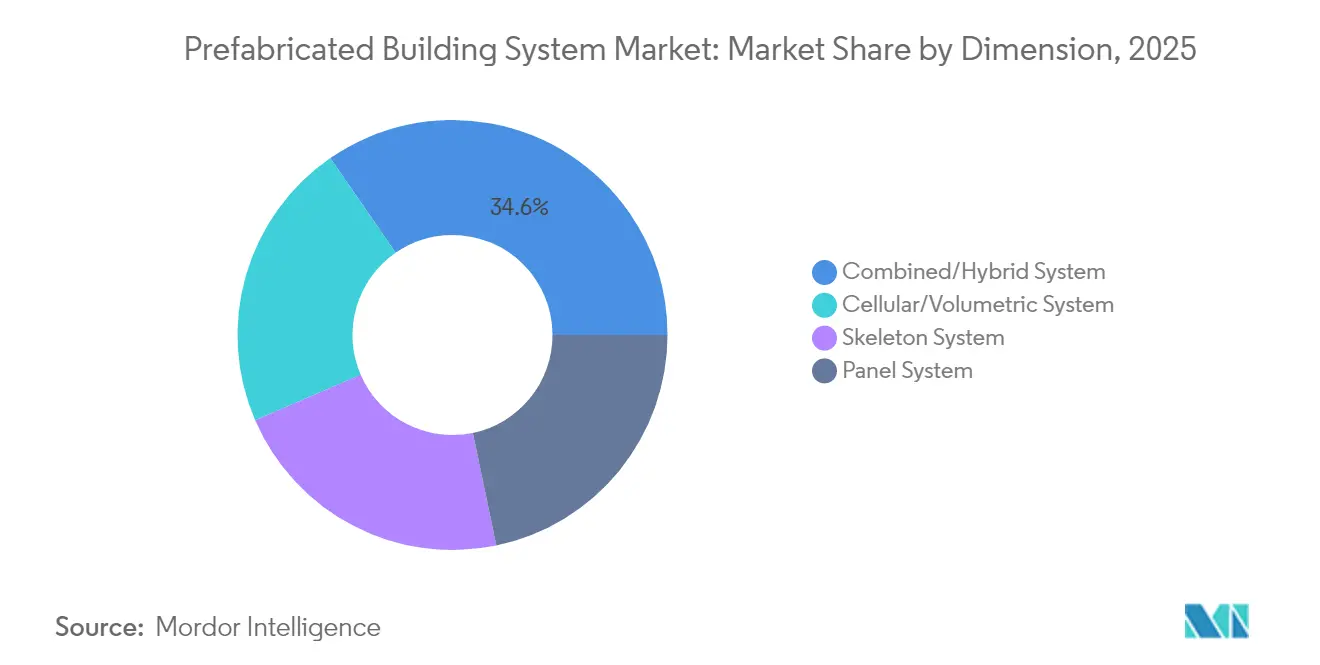

- By dimension, combined systems led with 34.62% revenue share of the prefabricated building systems market in 2025; the category is expanding at a 7.22% CAGR through 2031.

- By material, concrete accounted for 49.02% of the prefabricated building systems market size in 2025, whereas timber is advancing fastest at a 7.08% CAGR to 2031.

- By construction method, 2-D panelised solutions captured 49.58% of the prefabricated building systems market share in 2025, while 3-D volumetric modules are projected to grow at a 7.55% CAGR.

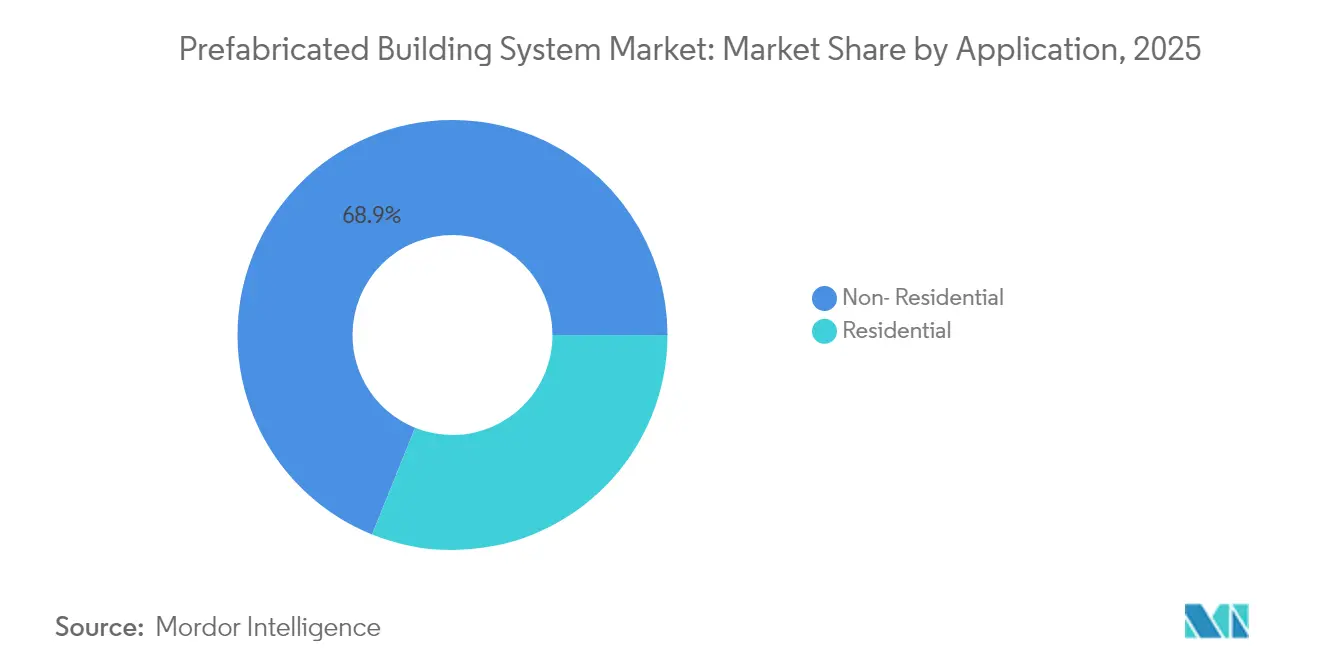

- By application, non-residential projects represented 68.90% of the prefabricated building systems market size in 2025; residential applications are set to climb at a 6.88% CAGR.

- By geography, Asia Pacific commanded 48.60% of global revenues in 2025 and is forecast to log a 6.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Prefabricated Building System Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating urbanization and housing shortages | +1.8% | Global, with concentration in APAC and North America | Long term (≥ 4 years) |

| Government incentives and green building mandates | +1.2% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Labor shortage and rising wages in construction | +1.5% | Global, most acute in developed markets | Short term (≤ 2 years) |

| Carbon-credit monetization for timber modules | +0.7% | North America and EU, pilot programs in APAC | Long term (≥ 4 years) |

| Climate-resilient rapid-deployment housing demand | +0.9% | Global, priority in disaster-prone regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Urbanization and Housing Shortages

Urban centers are swelling, with ASEAN cities expected to absorb 90 million additional residents by 2030, outpacing traditional construction capacity[1]OECD, “Urbanisation in Southeast Asia: Key Trends,” oecd.org . National programs such as Australia’s pledge to deliver 1.2 million new homes by 2029 rely heavily on imported modular components that speed project cycles by up to 40%. Large-scale migration is forcing developers to embrace standardized floor plates and repeatable modules that reduce permitting complexity and enable parallel manufacturing. Modular factories can operate around the clock, bringing predictable output that aligns with monthly housing delivery schedules. Consequently, the prefabricated building systems market is evolving from a niche alternative into a primary housing supply channel for high-growth urban corridors.

Government Incentives and Green-Building Mandates

Canada’s federal Build Canada Homes plan reserves more than USD 25 billion for builders deploying prefabricated techniques, creating a clear procurement preference for off-site manufacturing. In the United States, the Section 45L tax credit provides up to USD 5,000 per dwelling for energy-efficient homes, a threshold easily met by factory-produced envelopes with verified airtightness[2]U.S. Department of Energy, “45L Tax Credit Guidance,” energy.gov. The U.S. Department of Energy’s Zero Energy Ready Home guidelines further reinforce performance benchmarks that favor modular assemblies with integrated HVAC, insulation, and rooftop solar. Across the EU, 2025 revisions to Energy Performance of Buildings regulations require life-cycle carbon accounting, positioning factory-controlled production as the lowest-waste delivery model. These converging policies guarantee multi-year demand visibility for the prefabricated building systems market.

Labor Shortage and Rising Wages in Construction

Construction employment has contracted sharply since 2020, with job vacancy rates doubling in major economies. Wage escalation, overtime premiums, and training bottlenecks lift total site labor costs by double-digit percentages. Off-site manufacturing addresses scarcity by shifting work to climate-controlled plants where output per worker can be 2-3 times higher than on-site. Standardized tasks boost safety compliance and reduce rework, enabling contractors to meet deadlines despite lean site crews. Manufacturing wages remain competitive yet predictable, stabilizing bid prices and improving margin performance. These dynamics continue to draw capital toward automated production lines, reinforcing prefabricated building systems market growth.

Carbon-Credit Monetization for Timber Modules

Cross-laminated timber can sequester 0.38 tCO₂e per square meter, unlocking valuable offsets in voluntary and compliance carbon markets. Stora Enso’s Helsinki headquarters stores 6,000 tonnes of CO₂ while cutting emissions by 35% relative to concrete, showcasing scalable climate impact. Verified Environmental Product Declarations now allow developers to monetize stored carbon, delivering new revenue streams that can reduce net construction cost. High-rise timber prototypes across Europe demonstrate fire safety compliance through encapsulation and sprinkler integration, clearing regulatory barriers. These advances cement timber’s role as the fastest-growing material segment within the prefabricated building systems market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High logistics costs/size constraints | -1.1% | Global, most acute in regions with limited transport infrastructure | Short term (≤ 2 years) |

| Fragmented high-rise fire codes for modular buildings | -0.8% | North America and EU, emerging in APAC | Medium term (2-4 years) |

| Integration with Traditional Construction | -0.6% | Global, most pronounced in markets with established construction practices | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Logistics Costs and Size Constraints

Moving volumetric units requires wide-load permits, escort vehicles, and carefully sequenced delivery windows that can push transport charges to USD 25,000 per single-family module. Cost-to-weight ratios remain unfavorable because finished modules contain large volumes of air yet occupy entire truck-beds. Bridge clearances, turning radii, and axle-weight limits often dictate smaller module footprints, leading to additional onsite stitching that erodes factory efficiency. Investing in regionally distributed micro-factories can mitigate distance penalties but raises capital intensity. Overcoming these constraints will determine how broadly the prefabricated building systems market can penetrate low-density or infrastructure-constrained territories.

Fragmented High-Rise Fire Codes for Modular Buildings

Local authorities interpret fire-performance criteria inconsistently, forcing manufacturers to engineer to the strictest global standard or customize designs for every jurisdiction. The United Kingdom’s mandate for dual staircases in buildings over 18 meters exemplifies sudden rule changes that trigger redesigns and schedule slippage. Divergent requirements for gypsum thickness, joint protection, and sprinkler spacing add testing cycles that inflate soft costs. Harmonized codes or mutual recognition agreements would unlock scale economies for module producers. Until then, compliance complexity remains a friction point that tempers the long-term CAGR of the prefabricated building systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dimension: Integrated Combined Systems Reshape Project Delivery

Combined systems accounted for a 34.62% share of the prefabricated building systems market in 2025 while registering the leading 7.22% CAGR. Developers favor integrated skeleton-plus-panel platforms that deliver structural integrity alongside rapid enclosure, reducing trade handovers and compressing critical path schedules. These hybrid assemblies simplify cross-border sourcing because steel or concrete frames can be fabricated locally while façade and interior panels ship globally.

Demand is especially strong in mixed-use towers where open spans at podium levels transition into repetitive residential modules above. As Building Information Modeling gains traction, designers specify optimal mixes of volumetric cores, paneled façades, and steel megaframes to balance speed, cost, and architectural expression. The prefabricated building systems market benefits as bundled offerings provide one-stop procurement, mitigating interface risk that typically burdens conventional subcontracting.

By Material: Concrete Holds Scale while Timber Accelerates on Climate Credentials

Concrete held 49.02% of the prefabricated building systems market share during 2025, drawing strength from mature supplier networks and proven durability under diverse loading conditions. Automation of reinforcement placement, 3-D-printed formwork, and ultra-high-performance mixes are lowering unit costs and enabling thinner panels, expanding concrete’s design latitude. Yet the segment faces mounting embodied-carbon scrutiny, pressing producers to adopt low-clinker cement and recycled aggregates to protect market position.

Timber posted the fastest 7.08% CAGR and is commanding premium valuations in jurisdictions offering carbon credits or expedited permitting for biogenic materials. Engineered wood panels, dowel-laminated slabs, and hybrid timber-steel connectors now achieve 18-story height approvals, erasing historic limitations.

By Construction Method: Volumetric Modules Gain Traction against Panelised Mainstay

2-D panelised assemblies retained 49.58% of the prefabricated building systems market size in 2025 by combining flat-pack logistics with straightforward onsite craning. Panels expedite weather-tight closure and allow follow-on trades to operate within days of foundation completion. However, 3-D volumetric units are growing at a commanding 7.55% CAGR as robotic welding, high-precision jigs, and plug-and-play MEP integration drive cost parity. Complete room pods arrive with finishes, fixtures, and even appliances installed, enabling 70% of project value to be realized off-site and compressing commissioning timelines.

By Application: Residential Uptick Complements Established Non-Residential Dominance

Non-residential contracts delivered 68.90% of 2025 revenue, supported by repeatable building types such as data centers, warehouses, and healthcare facilities that justify capital-intensive production lines. Government stimulus for social infrastructure upgrades adds predictable order flow, enabling factories to maintain high utilization. Repeat clients value guaranteed opening dates and predictable cost metrics that prefabrication consistently delivers.

Residential demand is advancing at a 6.88% CAGR as municipalities seek rapid, code-compliant solutions to chronic affordability gaps. Factory-built homes can be installed on infill plots without extended street closures, minimizing neighbor disruption. Developers are adopting standardized floor plans that allow buyers to personalize finishes without changing structural layouts, increasing throughput across marketing, permitting, and production. Forward-looking jurisdictions streamline approvals for modular housing, shortening pre-construction phases. Together, these factors enlarge the addressable market and accelerate growth for the prefabricated building systems market.

Geography Analysis

Asia Pacific controlled 48.60% of 2025 turnover, buoyed by China’s USD 1 trillion Special Economic Zone investments that finance extensive modular factory rollouts and by Singapore’s 90% adoption rate for high-rise prefabrication. Regional governments couple industrial policy with urban housing targets, ensuring continuous project pipelines that lock in long-term plant capacity. The prefabricated building systems market size in Asia Pacific is on track for a 6.94% CAGR, reflecting both intra-regional trade and rising domestic content requirements that foster indigenous technology maturation.

North America is propelled by the USD 50 million Regional Homebuilding Innovation Initiative in Canada and supportive zoning reforms in the United States that classify modular units as permanent real property. Momentum is further sustained by stringent building-energy standards that favor tightly sealed factory-produced envelopes. The regional share is expected to edge higher as inland logistics corridors improve, reducing cost penalties for cross-border volumetric shipments.

Europe continues its steady advance on the back of labor shortages, aging housing stock, and Green Deal directives mandating whole-life carbon disclosure. Progressive municipalities, notably in the Nordics and the Netherlands, now include off-site construction criteria in public tenders. Mid-sized producers cluster near high-speed rail corridors, enabling overnight delivery across multiple capital cities.

Competitive Landscape

The competitive field remains moderately fragmented. Technological alliances are multiplying. CSCEC Modular leverages parent-company financing to win turnkey export contracts, including a recent multi-tower medical campus in the Gulf region that uses seismic-rated steel pods. Start-ups deploy computer-vision-guided robotics for panel finishing, shaving hours off manual sanding and reducing silica dust exposure. Timber specialists partner with forest managers to secure long-term feedstock at certified-sustainable yields, protecting margins as carbon valuation rises. Regional expansion strategies intensify rivalry. Chinese volumetric suppliers license designs to local partners in the United States to circumvent import duties and qualify for domestic content incentives.

Prefabricated Building System Industry Leaders

CSCEC Modular (China State Construction)

Laing O’Rourke

Red-Sea International

Sekisui House

Skyline Homes

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: EVStudio partnered with Vederra Modular to deliver affordable wood-frame housing, combining design expertise with regional factory capacity.

- February 2024: MMY US announced its first modular-housing plant in Louisville’s Parkland district, promising home delivery within 16 weeks.

Global Prefabricated Building System Market Report Scope

The building and construction industry uses prefabricated building systems, which are modular constructions or assemblies of parts and components. Typically, these systems are created and put together in factories before being delivered to the construction site, where they are installed or used to create structures. These systems are made from a variety of materials, including metal, wood, glass, plastic, concrete, etc. The prefabricated building system market is segmented based on dimensions, application, and geography. The market is segmented by dimensions into skeleton, panel, cellular, and combined systems. By application, the market is segmented into residential and non-residential. The report offers market sizes and forecasts for 18 countries across major regions. For each segment, market sizing and forecasts have been done on the basis of value (USD) for all the above segments.

| Skeleton System |

| Panel System |

| Cellular/Volumetric System |

| Combined/Hybrid System |

| Concrete |

| Steel |

| Timber |

| Others (Aluminium, Composites) |

| 2-D Panelised |

| 3-D Volumetric |

| Hybrid (2-D + 3-D) |

| Residential | |

| Non- Residential | Infrastructure |

| Commercial | |

| Industrial/Institutional |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN | |

| Rest of Asia Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIAC | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Egypyt | |

| South Africa | |

| Nigeria | |

| Rest of Middle-East and Africa |

| By Dimension | Skeleton System | |

| Panel System | ||

| Cellular/Volumetric System | ||

| Combined/Hybrid System | ||

| By Material | Concrete | |

| Steel | ||

| Timber | ||

| Others (Aluminium, Composites) | ||

| By Construction Method | 2-D Panelised | |

| 3-D Volumetric | ||

| Hybrid (2-D + 3-D) | ||

| By Application | Residential | |

| Non- Residential | Infrastructure | |

| Commercial | ||

| Industrial/Institutional | ||

| By Geography | Asia Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIAC | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Egypyt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the prefabricated building systems market?

The market reached USD 219.89 billion in 2026 and is projected to climb to USD 294.66 billion by 2031 on a 6.03% CAGR trajectory.

Which region holds the largest prefabricated building systems market share?

Asia Pacific leads with 48.60% of 2025 global revenue and maintains the highest regional CAGR at 6.94% through 2031.

Why are combined prefabricated systems gaining popularity?

Integrated skeleton-plus-panel platforms deliver structural strength, faster enclosure, and reduced trade interfaces, driving 34.62% market share and the top 7.22% CAGR among dimension categories.

How do logistics affect modular construction costs?

Wide-load permits, escort vehicles, and route restrictions can add up to USD 25,000 per residential module, making proximity to project sites a key cost variable.

What role do carbon credits play in timber prefabrication?

Verified carbon storage in cross-laminated timber unlocks offset revenues, improving project economics and assisting developers in meeting net-zero commitments.

Page last updated on: