Power Cutter Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 20.27 Billion |

| Market Size (2031) | USD 29.06 Billion |

| Growth Rate (2026 - 2031) | 7.47% CAGR |

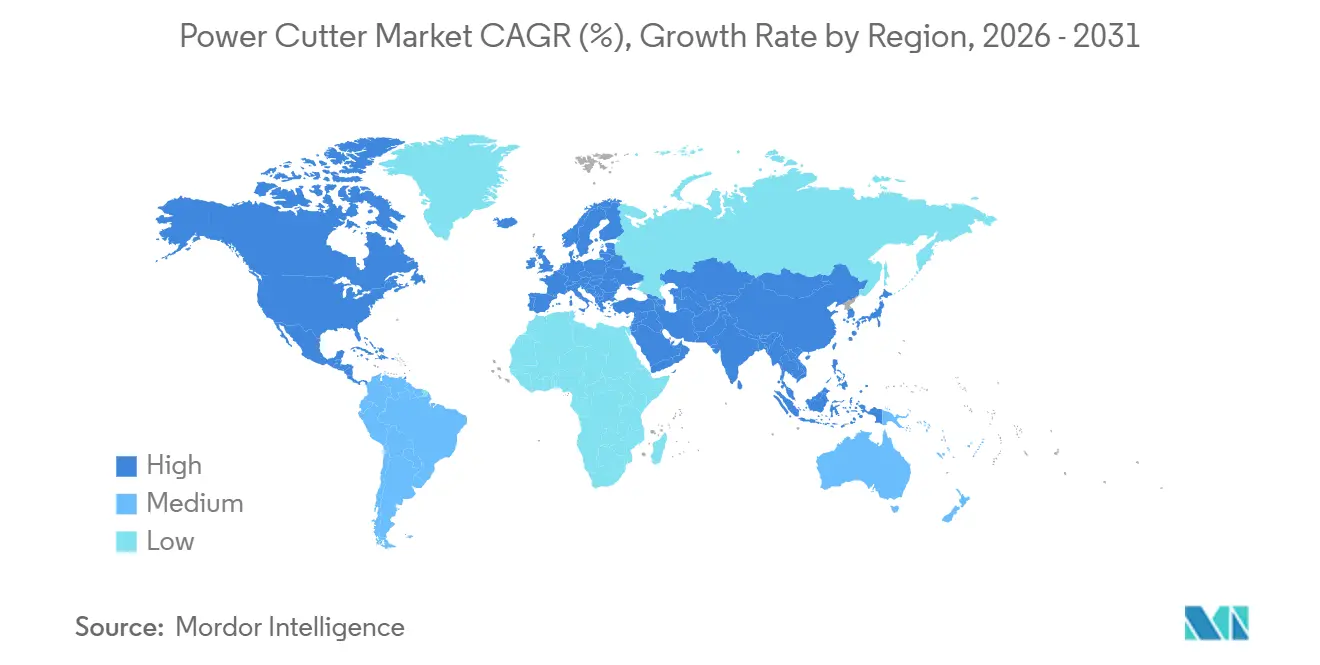

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Power Cutter Market Analysis by Mordor Intelligence

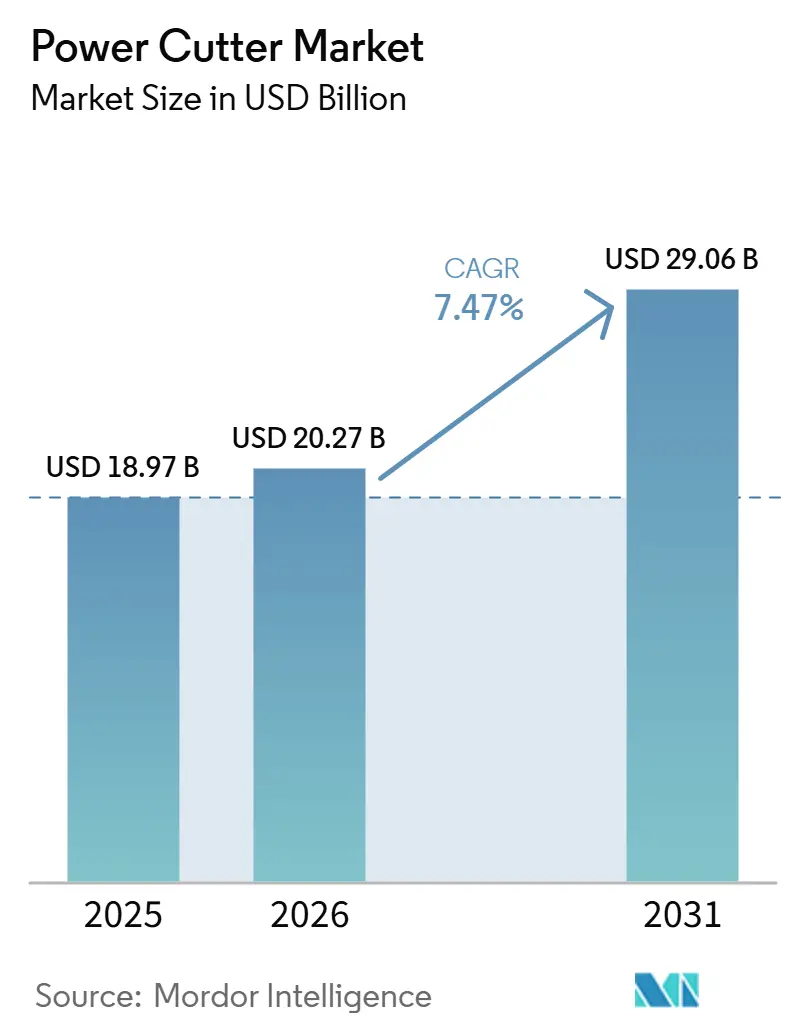

The Power Cutter Market size is projected to be USD 18.97 billion in 2025, USD 20.27 billion in 2026, and reach USD 29.06 billion by 2031, growing at a CAGR of 7.47% from 2026 to 2031.

Growth in the power cutter market reflects steady infrastructure renewal, the electrification of portable equipment, and the integration of connected diagnostics for fleet management across public safety and municipal buyers. Weber Rescue Systems’ SMART-FORCE platform highlights how connected battery telemetry and cloud tracking are now expected features for rescue-focused cutters used by civil-defense agencies. Battery-platform scale and accessory ecosystems are shaping competitive behavior as brands seek long-term lock-in across handheld and walk-behind categories in the power cutter market, supported by rapid product cycles and field-service programs. Hilti’s 2026 Nuron expansions and Bosch’s 2026 product wave illustrate how premium players are moving to standardize on single-voltage ecosystems that can serve both light and heavy-duty tasks. At the same time, advances in diamond coatings, such as BALDIA VARIA, underscore how material science continues to extend blade life in composite-heavy applications that are expanding across aerospace and medical manufacturing.

Key Report Takeaways

- By product type, handheld cut-off saws led with 53.5% of the power cutter market share in 2025; handhelds are forecast to expand at a 9.1% CAGR to 2031.

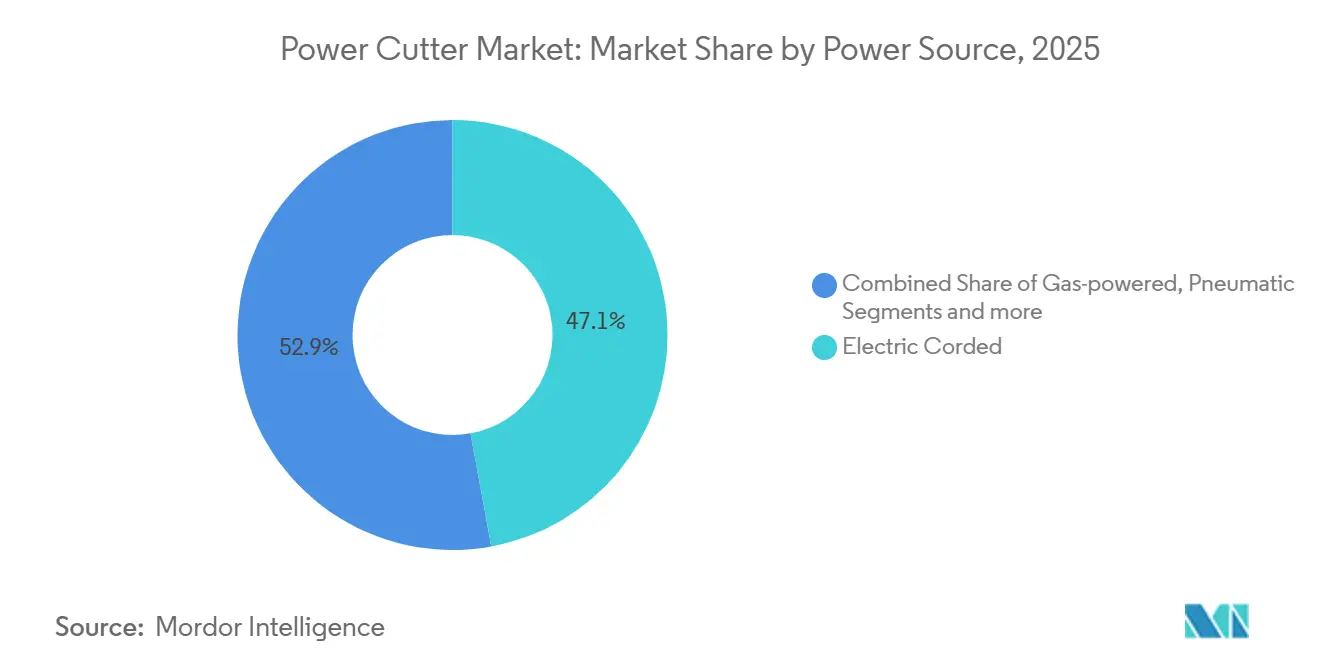

- By power source, electric-corded models held 47.1% share in 2025; battery-powered handhelds record the fastest projected 8.8% CAGR through 2031.

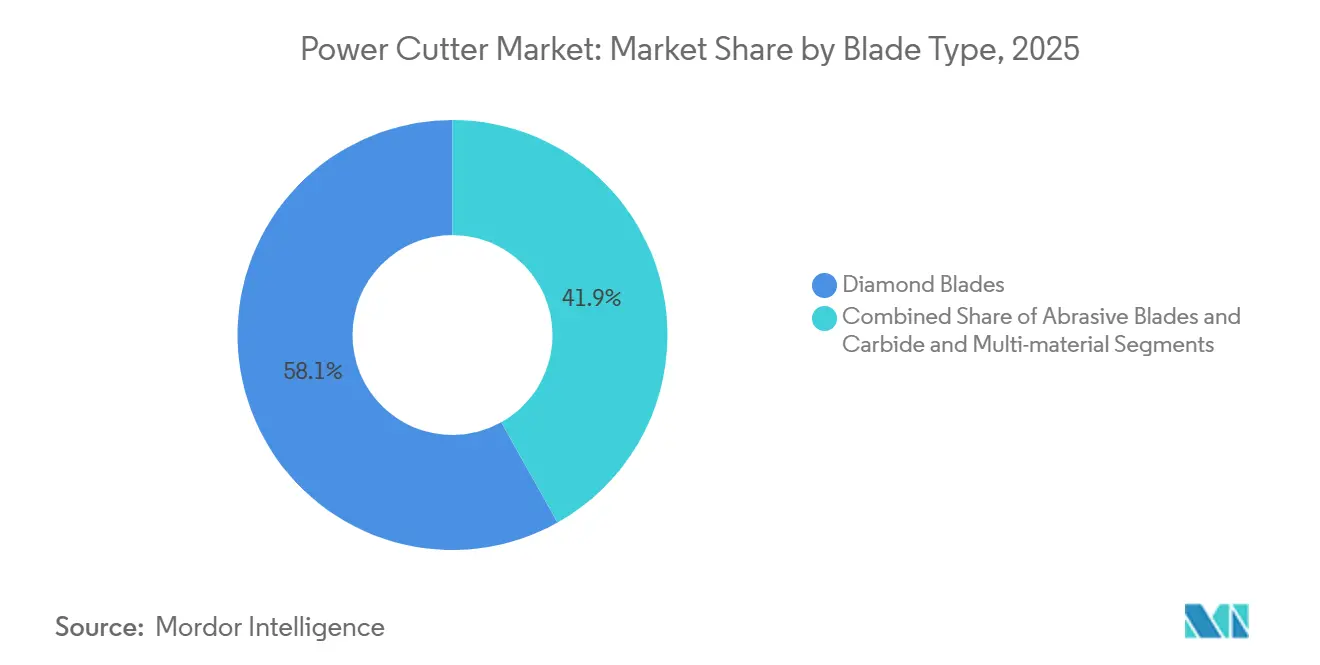

- By blade type, diamond blades commanded 58.1% of the power cutter market share in 2025; carbide and multi-material blades are set to grow at 7.7% CAGR to 2031.

- By end-user industry, construction and demolition accounted for 53.1% of 2025 demand; general manufacturing, metalworking, and fabrication are advancing at an 8.1% CAGR to 2031.

- By geography, Asia-Pacific captured 38.4% share in 2025; the region is projected to grow at 8.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Power Cutter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption in Emergency Rescue and Disaster Response Operations | +0.9% | Global, with early gains in EU, North America, GCC | Medium term (2-4 years) |

| Growing Renovation and Remodeling Activities | +1.2% | North America, Western Europe, urban India | Short term (≤ 2 years) |

| Expansion of Road Construction and Maintenance Programs | +1.5% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Growth in DIY and Professional Landscaping Services | +0.6% | North America, Australia, urban China | Short term (≤ 2 years) |

| Increasing Preference for Cordless and Battery-Powered Models | +2.1% | Global | Short term (≤ 2 years) |

| Mining and Quarrying Industry Expansion | +0.7% | South America, Sub-Saharan Africa, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption in Emergency Rescue and Disaster Response Operations

Emergency services are integrating connected power cutters into their standard operating kits due to the rise of composite materials and high-strength steels in modern vehicles. Real-time battery diagnostics, usage logs, and location tracking in platforms like Weber Rescue Systems’ SMART-FORCE improve readiness verification and asset control across multi-station fleets[1]Staff Reporter, “Compact and connected: From cutters to cloud, inside WEBER RESCUE SYSTEMS’ digital rescue push,” International Fire & Safety Journal, internationalfireandsafetyjournal.com. Compact form factors and specialty attachments support confined-space operations, including rapid access cuts in mass transit and multi-vehicle incidents. These capabilities reduce the risk of on-scene tool downtime and streamline mutual-aid recoveries after cross-jurisdictional deployments. As zero-emissions vehicles proliferate, responders need non-sparking diamond-blade solutions with reliable braking and dust control, which strengthens the case for premium cordless platforms in the power cutter market. Connectivity and battery management also help departments plan life-cycle replacement and training, which tightens procurement alignment with operational demands.

Growing Renovation and Remodeling Activities

Sustained home renovation and light commercial remodeling keep demand high for portable cutters that can handle porcelain, tile, masonry, and light metal tasks. Homeowners and small contractors combine continuous-rim diamond blades for clean tile cuts with segmented blades for faster concrete work, which reduces changeover time on multi-material projects. Water-suppression and dust-shroud accessories have become standard choices for indoor tasks where compliance and neighbor comfort matter. Rental programs extend access to higher-end cutters for weekend projects where purchase does not pencil out. In parallel, contractors standardize on cutters that integrate easily with vacuums and water kits to manage dust and debris on occupied sites. This activity sustains a broad base of users in the power cutter market as property owners prioritize upgrades over new builds when financing conditions are tight.

Expansion of Road Construction and Maintenance Programs

Public investment in roads, bridges, and transit corridors is translating into steady orders for walk-behind saws, joint cutters, and depth-controlled machines. Large regional transit corridors, such as India’s Sarai Kale Khan–Shahjahanpur-Behror RRTS segment commencing in August 2026, will require tight-tolerance cuts along extensive alignments and stations through to project completion in 2031[2]Staff Correspondent, “‘Power tools segment likely to more than double to $3.8 billion by 2035 at CAGR of 7.8%,’” The Hindu, thehindu.com. Municipal specifications increasingly reference precise depth and kerf quality, which favors models with laser alignment, telemetry, and robust water delivery. Emissions rules in Europe push agencies and contractors toward electric alternatives where diesel restrictions apply in dense urban areas. IoT-enabled usage tracking also gives owners improved visibility into contractor compliance on cut depth and linear meters delivered against plan. As fleets turn over, procurement preferences lean toward cutters that can operate in mixed asphalt and concrete environments with minimized blade wear.

Growth in DIY and Professional Landscaping Services

Landscaping and hardscaping workstreams are adopting cordless cutters to avoid emissions and noise restrictions in residential neighborhoods. Product families now span from pole saws and trimmers to grinders and cut-off saws on shared battery systems, which lowers ownership costs through energy and charger commonality. Bosch’s 2026 launches reflect this unification of chemistries across categories that previously required gas or grid connections. Contractors favor compact 9-inch cordless cut-off saws that eliminate cords and reduce setup time on rooftops, courtyards, and small-footprint jobs. Multi-tool battery compatibility in pro-grade ecosystems helps small crews manage full-day workloads without added fuel logistics. These patterns sustain a dense long tail of users in the power cutter market, especially during peak landscaping seasons.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety Hazards and Operator Injury Risks | -0.6% | Global, concentrated in North America and EU due to litigation exposure | Medium term (2-4 years) |

| Frequent Blade Replacement and Consumable Costs | -0.4% | Global | Short term (≤ 2 years) |

| Seasonal Demand Fluctuations in Construction Activity | -0.3% | Temperate climates: North America, Northern Europe, temperate Asia | Short term (≤ 2 years) |

| Physical Strain and Ergonomic Challenges | -0.5% | Global, with heightened focus in EU and North America under OSHA/ISO frameworks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Safety Hazards and Operator Injury Risks

Rotating-blade tools present inherent risks that include kickback, binding, and debris ejection, and job sites often operate under variable conditions that can amplify these hazards. Manufacturers have responded with enhanced blade guards, electronic brakes, and intelligent motor controls that cut power during binding events. As more cutting shifts are being performed indoors or into enclosed spaces, water-suppression systems and dust shrouds are also being standardized to manage silica exposure. Portable units without cords reduce trip hazards around crowded work areas and improve setup discipline. Buyers in the power cutter market increasingly assess tools by their integrated safety stack, from braking times to dust mitigation, due to regulatory and liability pressures. Wider adoption of sensor-rich and brake-equipped models can reduce incident severity and downtime on professional crews.

Frequent Blade Replacement and Consumable Costs

Consumables weigh on the total cost when cutting abrasive materials or steel-reinforced structures. A 14-inch segmented diamond blade for concrete cutting can command USD 100–500, and the lifecycle is sensitive to feed pressure, cooling, and substrate. Premium formulations promise longer life and more consistent kerf quality, which reduces rework on high-spec projects. Manufacturers also use blade-venting and segment geometry to keep temperatures in check and limit wobble at speed, improving cut accuracy and life. Rental programs sometimes bundle a blade with the tool to simplify billing, though frequent users typically secure discounts through fleet or palletized purchases. Managing blade costs remains a practical constraint that buyers in the power cutter market factor into bid estimates and fleet budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Source: Corded Electric Anchors Present, Battery Platforms Redefine Tomorrow

Electric corded models held 47.1% share in 2025, reflecting value in continuous torque delivery on multi-hour cutting tasks where battery-swap cycles could disrupt workflow. This position aligns with use on slab cuts, rebar sections on high-rise decks, and stationary fabrication stations where uninterrupted duty cycles are critical. Battery-powered handhelds show the fastest expansion at 8.8% CAGR through 2031 as platform-scale, cooling, and charging improvements narrow performance gaps with corded baselines. Brands emphasize single-ecosystem coverage so one charger and a few packs sustain multiple categories, which increases utilization and lowers fleet complexity. Electronic braking and overload protection features help cordless units meet safety expectations that once favored fixed installations. Platform lock-in has become a strategic factor in the power cutter market as contractors extend battery investments across hundreds of compatible tools. Procurement also reflects dust-control and vibration demands that are often easier to implement on designs without engine emissions systems in urban or enclosed environments.

Corded units eliminate upfront battery costs and reduce weight relative to onboard energy storage, which helps in tight spaces and repetitive cutting sequences. Gas-powered cutters still serve remote and disaster-response roles where refueling remains faster than charging, especially on sustained high-output cycles, although emissions policies in dense cities limit their use. Hydraulic systems continue to occupy a specialized niche for demolition and subsurface utility work where torque density is paramount, though hoses and auxiliary packs limit mobility. Pneumatic solutions are retreating as cordless options remove compressor infrastructure and airline maintenance. As cordless ecosystems mature, owners in the power cutter industry expect better integration with dust shrouds, water systems, and vacuums to deliver holistic compliance. Buyers weigh all-in system costs, not just tool-only price, which supports broader adoption of premium cordless solutions in the power cutter market when productivity gains and safety features offset initial investment.

By Product Type: Agile Handhelds Drive Volume, Walk-Behinds Command Project Premium

Handheld cut-off saws captured 53.5% of 2025 revenue, and this category also leads growth at 9.1% CAGR to 2031 as cordless models expand job-site flexibility for interior, rooftop, and enclosed projects. These tools enable fast substrate switching across masonry, rebar, steel tube, and composite panel tasks within remodeling and light commercial work. Stationary cut-off machines remain fixtures in fabrication shops that require repeatable 90-degree and miter cuts with clamps for a one-operator workflow. Walk-behind units serve expansion joints, utility trenches, and apron repairs where straightness, controllable depth, and millimeter-level expectations are common in municipal contracts. Ride-on saws address large-area removal and preparation, but their capital cost limits are used for specialized contractors and high-throughput scenarios. In the power cutter market, modular accessories, interchangeable guards, and universal arbor adapters help inventories pivot quickly from one substrate to another. Buyers also evaluate the ease of integrating dust and water controls so crews can move indoors without reconfiguring equipment.

Guard design remains a focal point for safety teams and inspectors because guards must cover the blade and retract appropriately to expose only the kerf during a cut. Manufacturers enhance braking to reduce post-trigger coasting and extend electronic controls to detect binding events. New cordless table saws and concrete-focused grinders hint at the migration of tabletop features into portable platforms that could absorb some walk-behind use cases where portability is a key advantage. As battery energy density continues to rise, handhelds will carry more of the heavy-duty work that previously belonged to gas equipment. Edge quality, kerf precision, and dust suppression increasingly differentiate product families as contracts tighten tolerances and documentation requirements. These product-level advances shape brand preference in the power cutter market, where professional users balance speed, control, and compliance.

By Blade Type: Diamond's Longevity Premium Justifies Cost, Carbide Versatility Gains Share

Diamond blades held 58.1% of 2025 blade-type revenue as contractors select longevity and cut quality for reinforced concrete, stainless steel, and fiber-reinforced plastics. Segmented-rim designs provide debris evacuation on aggregate-heavy concrete and asphalt, while turbo rims blend faster feed rates with acceptable finish for mixed jobs. Pricing tires reflects diameter, bond hardness, and segment height, and lifecycle depends on feeding pressure and cooling. Advanced coatings such as Oerlikon’s BALDIA VARIA address composite stacks that blunt conventional tooling, and progressive wear modes support more predictable change-outs on critical parts. Carbide and multi-material blades are growing at 7.7% CAGR as crews adopting mixed-substrate workflows reduce changeovers, especially where steel, cured concrete, and conduit align in one shift. Abrasive wheels retain an entry price advantage but remain labor-intensive due to shorter life and inconsistent kerf finish, which can raise rework time.

Geometry and thermal management are now core differentiators as vendors tune gullets, vents, and segment profiles for cooler and cleaner cuts. Milwaukee employs diamond vents to cool blades and minimize wobble, which helps crews maintain line control during long cuts[3]Product Page, “Diamond Blades and Cup Wheels,” Makita, makitatools.com. Makita’s battery-optimized diamond blades with thinner kerf and Turbo U-Notch segments reduce drag to extend cordless runtime, tightening the battery math for long indoor jobs. As ISO and CE requirements reinforce traceability and performance verification, procurement for public projects increasingly specifies certified suppliers, which supports established brands with in-house testing. In the power cutter market, blade reliability, certification, and predictable life are central to total cost calculations, especially on contracts with strict penalties for cut quality or dust control violations. The scaling of synthetic diamond production complements this dynamic and may reduce price gaps at mid-tier diameters over time.

Geography Analysis

Asia-Pacific accounted for 38.4% of 2025 revenue and is projected to grow at 8.5% CAGR through 2031, anchored by data-center construction, national infrastructure programs, and large transit corridors. China’s 2021 construction-equipment sales and excavator volumes signal sustained complementary demand for cutters across concrete, rebar, and asphalt use cases. India’s National Infrastructure Pipeline totals INR 100 trillion (USD 1.2 trillion), reinforcing multi-year demand for cutting equipment across highways and transit centers (USD 1.2 trillion). The Regional Rapid Transport System segment from Sarai Kale Khan to Shahjahanpur-Behror kicks off in August 2026 and is expected to be completed by November 2031, which implies sustained needs for joint, trench, and station cuts over the timeline. Urban emissions and noise policies in Tokyo, Seoul, Singapore, and Hong Kong steer buyers toward electric options for indoor and nighttime work. Localized OEM investments, including capacity decisions affecting South Korea, improve supply resilience and lead times.

North America and Europe together hold roughly the remaining half of global revenue, with premium pricing, codified training, and advanced compliance ecosystems. Funding visibility for United States infrastructure contributes to stable tool budgets among contractors that prioritize uptime and support. European regulations on emissions, silica dust, and hand-arm vibration continue to lift baseline specifications, which support integrated systems that combine cutters, vacuums, and water kits. CE marking and EN standards reinforce procurement preferences for documented performance and traceable materials. Training credentials for walk-behind saw operators in markets like Germany further formalize tool selection and usage. As cordless platforms improve, indoor and enclosed-space tasks shift away from gas equipment to meet local rules without specialized ventilation.

South America and the Middle East & Africa contribute to the balance of demand. Mining and quarrying across Brazil, Chile, and Peru sustain orders for heavy-duty cutters used in core trimming and rock processing. Large-scale construction in Gulf Cooperation Council markets produces episodic surges tied to mega-project phases. In Africa, road connectivity and port expansions add incremental growth as industrialization advances in select economies. Currency volatility and uneven enforcement of standards influence channel strategies, with international contractors often specifying premium brands for safety and quality consistency. Across these regions, rental plays an important role as contractors align tool access with project schedules and cash-flow planning. The power cutter market benefits from this flexibility, which expands access to premium platforms where outright purchase is deferred.

Competitive Landscape

The market remains fragmented overall, although premium segments are increasingly influenced by ecosystem-driven competition among leading global brands. Competition is shaped by platform breadth, safety features, service density, and accessory ecosystems that elevate switching costs. Hilti’s Nuron 22V expansion in 2026, including heavy-duty breakers and a cordless table saw, aims to consolidate buyer preference on one voltage family that covers light and heavy tasks with rapid charging. Bosch’s 2026 set of launches extends platform compatibility across concrete and outdoor tools, which makes battery logistics simpler for mixed crews. Oerlikon’s BALDIA VARIA coating shows that consumable innovation is a parallel competition vector as composite machining expands. Vendors with in-house certification and testing also respond faster to evolving standards, which shortens time-to-market for updated models in the power cutter market.

Digital features now extend beyond theft deterrence to usage analytics that support predictive maintenance and fleet optimization. Milwaukee’s emphasis on intelligent controls and braking capabilities illustrates how electronics raise tool safety as well as performance. Large customers often negotiate direct fleet agreements that bundle service, training, and consumables for consistent uptime. This favors brands that can deliver fast parts logistics and accredited training programs across major metros. As a result, aftermarket-service density weighs heavily in share shifts, with brand preference driven as much by support as by peak performance specifications.

Supply-chain decisions are also strategic. Investments that balance production among North America, Europe, and Asia aim to reduce lead times and tariff exposure, which matters for municipal buyers with specific funding windows. As cordless gains continue, brands differentiate with complete systems that include dust, water, and storage solutions tuned to their cutters, which eases compliance and transport. This system's view improves bid competitiveness on public works that require documentation and safety validation. The power cutter market remains dynamic as platform lock-in, consumable R&D, and service scale create durable advantages for multi-category leaders.

Power Cutter Industry Leaders

Husqvarna Group

Stihl Holding AG & Co. KG

Makita Corporation

Hilti Corporation

Bosch Power Tools (Robert Bosch GmbH)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Bosch Power Tools unveiled a broad set of new products at World of Concrete 2026, including the EXPERT 18V battery platform and expanded concrete and outdoor equipment families designed to deliver corded-like performance while unifying chemistries.

- January 2026: Hilti announced the largest expansion of its Nuron 22V platform to date, adding a first cordless table saw alongside heavy-duty breakers and high-capacity batteries, to consolidate professional buyers on a single ecosystem.

- November 2025: Volvo Construction Equipment selected Eskilstuna, Sweden, for a crawler excavator assembly plant investment, with groundwork starting in H1 2026 to support European production resiliency

Global Power Cutter Market Report Scope

The Power Cutter Market Report is Segmented by Power Source (Gas-Powered, Electric – Corded, and More), by Product Type (Handheld Cut-Off Saws, Walk-Behind Cutters, and More), by Blade Type (Abrasive Blades, Diamond Blades, and More), by End-User Industry (Construction & Demolition, Automotive, and More), and by Geography (North America, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value in USD Billion.

| Gas-powered |

| Electric – Corded |

| Pneumatic |

| Hydraulic |

| Battery-powered (hand-held) |

| Handheld Cut-off Saws |

| Walk-behind Cutters |

| Stationary Cut-off Machines |

| Abrasive Blades |

| Diamond Blades |

| Carbide & Multi-material Blades |

| Construction & Demolition |

| General Manufacturing, Metalworking & Fabrication |

| Automotive |

| Aerospace |

| Others (Consumer, DIY, Landscaping, Municipal, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Turkey | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Power Source | Gas-powered | |

| Electric – Corded | ||

| Pneumatic | ||

| Hydraulic | ||

| Battery-powered (hand-held) | ||

| By Product Type | Handheld Cut-off Saws | |

| Walk-behind Cutters | ||

| Stationary Cut-off Machines | ||

| By Blade Type | Abrasive Blades | |

| Diamond Blades | ||

| Carbide & Multi-material Blades | ||

| By End-user Industry | Construction & Demolition | |

| General Manufacturing, Metalworking & Fabrication | ||

| Automotive | ||

| Aerospace | ||

| Others (Consumer, DIY, Landscaping, Municipal, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and long-term growth outlook for the power cutter market?

The power cutter market size reached USD 18.97 billion in 2025 and is projected to reach USD 29.06 billion by 2031 at a 7.5% CAGR, supported by infrastructure renewal, electrification, and connected fleet management.

Which product type leads to demand, and which is growing the fastest?

Handheld cut-off saws led with 53.5% of 2025 revenue, and the same category is the fastest-growing at a 9.1% CAGR due to advances in cordless performance and job-site flexibility.

How is the regional mix shifting through 2031?

Asia-Pacific held 38.4% in 2025 and shows the fastest trajectory at an 8.5% CAGR through 2031, while North America and Europe maintain premium share positions with strong compliance and service ecosystems.

What are the top two factors accelerating cordless adoption?

Improved battery energy density with rapid charging and tighter on-site constraints around emissions, dust, and noise are pushing buyers toward cordless systems that deliver cord-like performance.

Which end users are driving sustained purchasing?

Construction and demolition account for 53.1% of 2025 demand, and general manufacturing, metalworking, and fabrication are growing at 8.1% CAGR as EV, aerospace, and semiconductor use cases expand.

What should buyers weigh when comparing blade options?

Diamond blades hold 58.1% share for durability and cut quality, while carbide and multi-material variants are growing at 7.7% CAGR; selection should consider substrate mix, water-suppression needs, and certified performance for public works.

Page last updated on: