Post Traumatic Stress Disorder Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

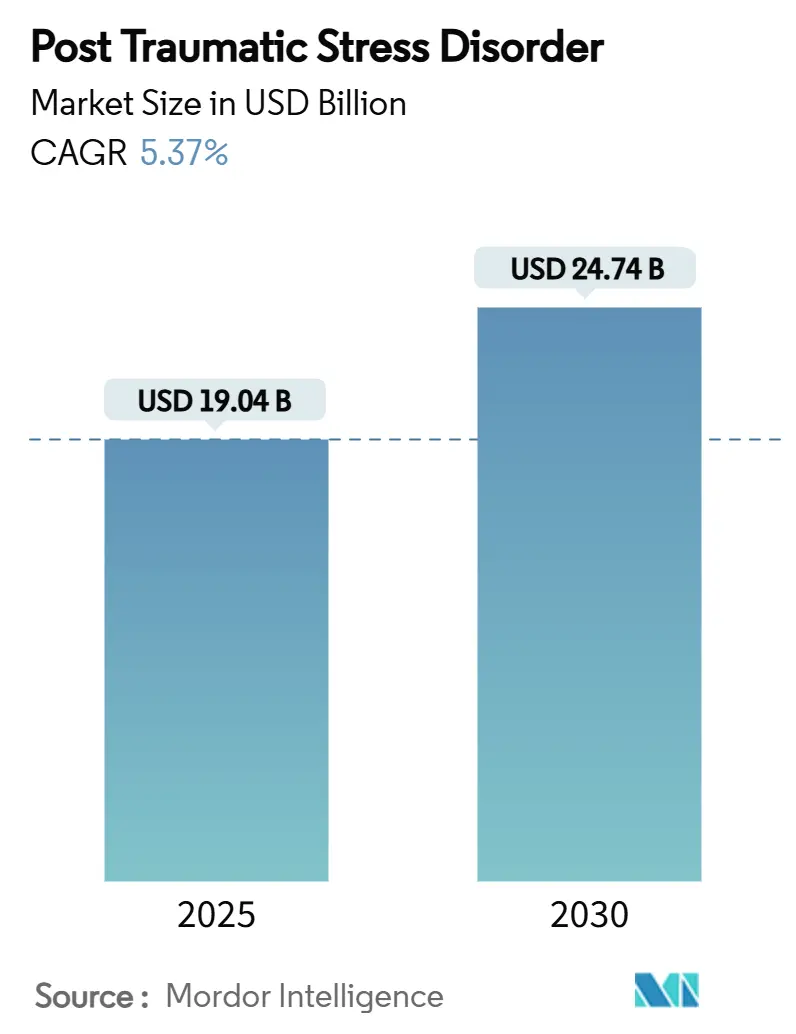

| Market Size (2025) | USD 19.04 Billion |

| Market Size (2030) | USD 24.74 Billion |

| Growth Rate (2025 - 2030) | 5.37% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Post Traumatic Stress Disorder Market Analysis by Mordor Intelligence

The PTSD therapeutics market is valued at USD 19.04 billion in 2025 and is forecast to reach USD 24.74 billion by 2030, advancing at a 5.37% CAGR. The current expansion is anchored in the steady uptake of selective serotonin re-uptake inhibitors (SSRIs), the widening clinical footprint of psychedelic-assisted regimens, and the rapid commercialization of FDA-cleared digital therapeutics. Regulatory actions—most notably the August 2024 FDA rejection of MDMA therapy—have redirected capital toward combination pharmacology and software-as-a-medical-device solutions, preserving momentum despite setbacks. Companies are also leveraging AI-driven drug-repurposing engines to shorten development timelines while payers expand reimbursement for tele-psychiatry, widening access to underserved cohorts and reinforcing overall growth in the PTSD therapeutics market.

Key Report Takeaways

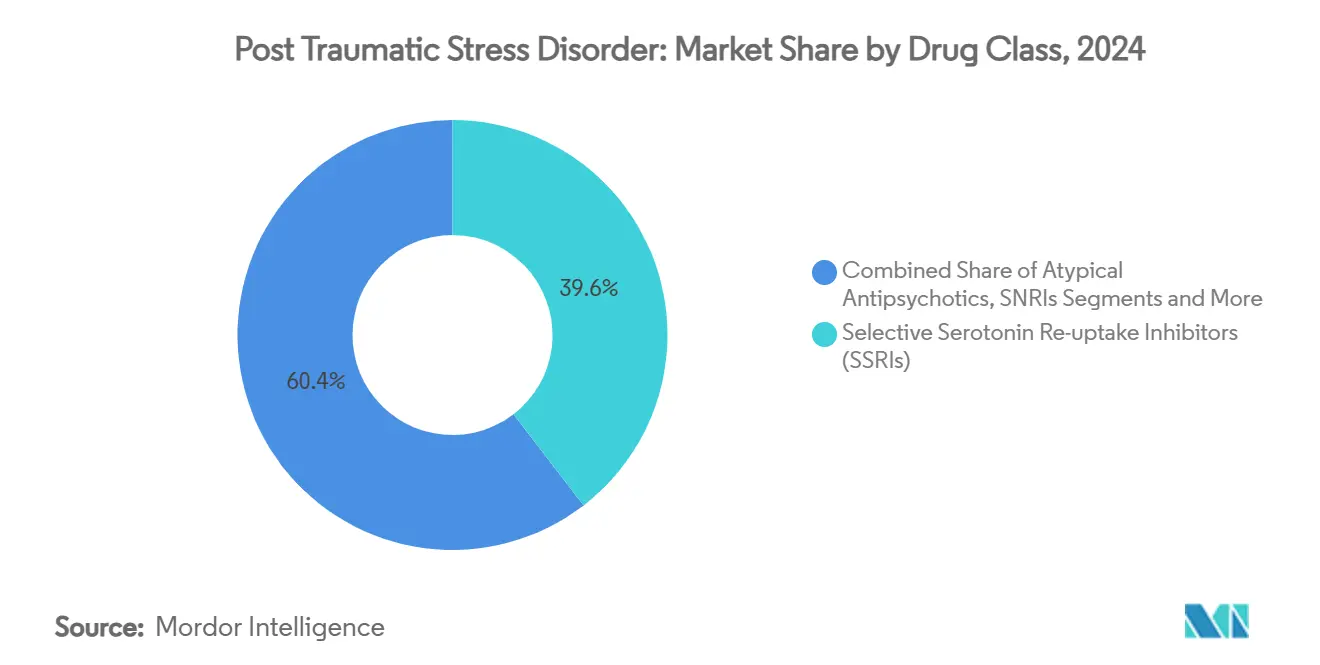

- By drug class, SSRIs led with 39.56% of PTSD therapeutics market share in 2024, while psychedelic-assisted therapies are projected to rise at an 8.89% CAGR through 2030.

- By patient type, adults accounted for 81.78% of the PTSD therapeutics market size in 2024 and children & adolescents are expected to grow at 7.67% CAGR to 2030.

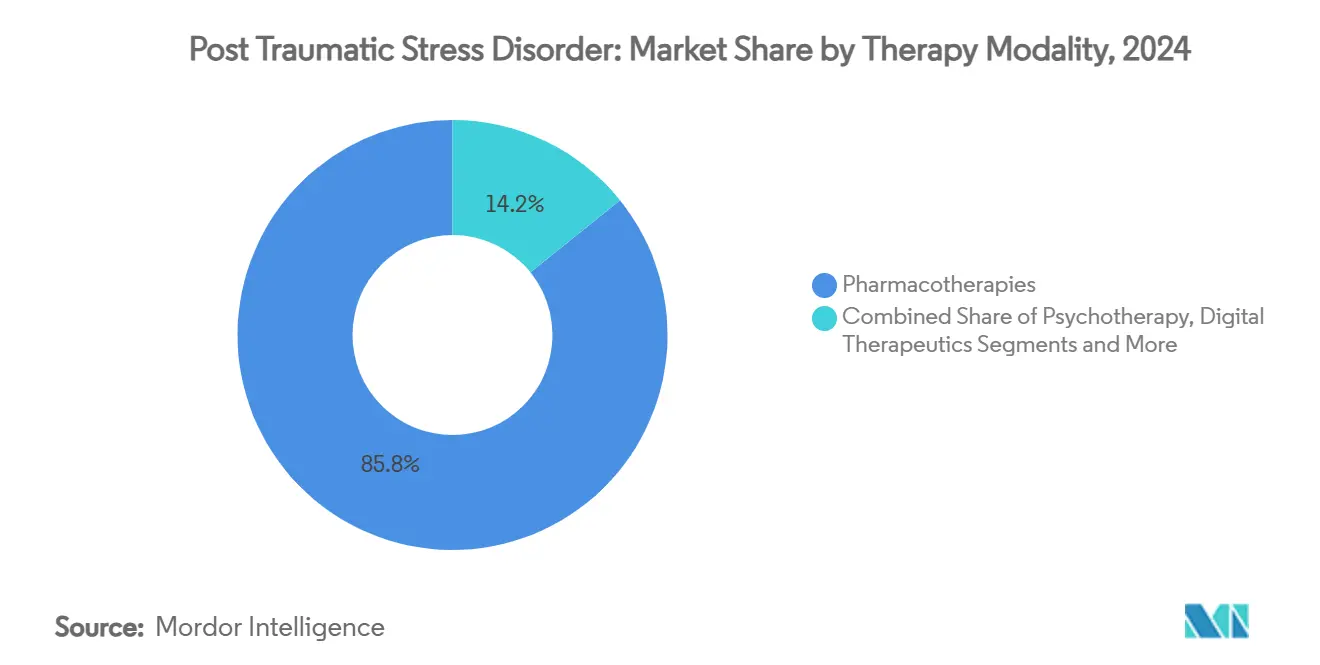

- By therapy modality, pharmacotherapy held 85.79% share of the PTSD therapeutics market size in 2024, whereas digital therapeutics are advancing at a 9.56% CAGR over the same period.

- By distribution channel, hospital pharmacies commanded 47.34% share in 2024; digital and tele-prescription platforms record the highest projected CAGR at 9.87% through 2030.

- By geography, North America led with 36.47% revenue share in 2024, while Asia-Pacific is forecast to expand at a 7.13% CAGR to 2030.

Global Post Traumatic Stress Disorder Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing global PTSD prevalence and diagnosis rates | +1.2% | North America & Europe highest | Medium term (2-4 years) |

| Accelerating late-stage clinical trials for novel agents | +0.8% | North America & EU core, spill-over to APAC | Short term (≤ 2 years) |

| Expedited FDA breakthrough & fast-track designations for psychedelic-assisted therapies | +0.6% | North America, spill-over to Australia & Europe | Long term (≥ 4 years) |

| AI-driven drug-repurposing platforms uncovering PTSD indications | +0.4% | US & Japan early adopters | Medium term (2-4 years) |

| Government and payer uptake of digital therapeutics for post-deployment mental health | +0.7% | North America & EU expanding to APAC | Short term (≤ 2 years) |

| Expansion of tele-psychiatry increasing prescription reach | +0.5% | Rural North America & emerging APAC markets | Medium term (2-4 years) |

Source: Mordor Intelligence

Growing Global PTSD Prevalence and Diagnosis Rates

Improved screening protocols are unveiling sizeable patient cohorts among women veterans and civilian trauma survivors who were historically under-diagnosed. The Odisha train disaster illustrated how mass trauma events trigger systematic PTSD assessments, with prevalence among survivors ranging from 19% to 59.4%.[1]Nilamadhab Kar, “Anatomy of a Catastrophe: Managing Psychosocial Consequences of the 2023 Odisha Train Accident,” Industrial Psychiatry Journal, journals.lww.comStates such as Texas now pilot psychedelic therapy programs for veterans after budget cuts to conventional care, further enlarging the treated population. The resulting rise in prescriptions keeps the PTSD therapeutics market on a steady growth trajectory and pushes developers to address therapy-resistant subgroups.

Accelerating Late-Stage Clinical Trials for Novel Agents

Pipeline density is the highest in two decades, with Otsuka and Lundbeck reporting a mean CAPS-5 improvement of 5.59 points for brexpiprazole-sertraline vs. placebo in two positive Phase 3 studies.[2]Lori L. Davis et al., “Brexpiprazole and Sertraline Combination Treatment in Posttraumatic Stress Disorder: A Phase 3 Randomized Clinical Trial,” JAMA Psychiatry, jamanetwork.com Compass Pathways achieved clinically sustained benefits from a single 25 mg psilocybin dose backed by psychological support. The FDA’s clearance for a 320-patient cannabis study underscores the wider regulatory appetite for diversified modalities.

Expedited FDA Breakthrough & Fast-Track Designations for Psychedelic-Assisted Therapies

While the agency issued a complete response letter on MDMA, it asked for an additional trial rather than rejecting the class outright, signaling a conditional openness. Breakthrough status for digital solutions tackling PTSD nightmares further highlights the regulator’s willingness to accelerate innovative tools.

AI-Driven Drug-Repurposing Platforms Uncovering PTSD Indications

Companies such as Alto Neuroscience use machine learning to match neurobiologic markers with existing CNS drugs, yielding ALTO-100 for PTSD with promising Phase 2 data. Dual-loop neuromodulation systems combining implants and AI wearables exemplify how technology can personalize interventions beyond symptom clusters.[3]Min Zuo, “When Neural Implant Meets Multimodal LLM: A Dual-Loop System for Neuromodulation and Naturalistic Neuralbehavioral Research,” arXiv, arxiv.org

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety & abuse-liability concerns around psychedelic compounds | -0.9% | North America & EU highest | Long term (≥ 4 years) |

| High placebo responses in PTSD trials | -0.6% | Global | Medium term (2-4 years) |

| Limited biomarker-based patient stratification | -0.4% | North America & EU | Long term (≥ 4 years) |

| Stigmatization and under-reporting of symptoms | -0.3% | Global, culturally variable | Long term (≥ 4 years) |

Source: Mordor Intelligence

Safety & Abuse-Liability Concerns Around Psychedelic Compounds

FDA advisers voted 10-1 against MDMA in August 2024, citing functional unblinding and therapist misconduct. Schedule I status triggers stricter REMS, elevating cost and limiting distribution channels in the PTSD therapeutics market. Specialized therapist training and controlled settings remain prerequisites, restraining near-term adoption despite strong clinical demand.

High Placebo Responses in PTSD Trials Complicate Regulatory Approvals

Placebo arms in pivotal MDMA studies posted 32% and 48% response, narrowing the efficacy margin needed for approval. Intensive psychotherapeutic support embedded in trials acts as an active treatment, skewing results and forcing sponsors to run larger, longer studies—raising development costs and delaying launches across the PTSD therapeutics market.

Segment Analysis

By Drug Class: SSRIs Steady, Psychedelics Surge

SSRIs retained a 39.56% slice of the PTSD therapeutics market in 2024 due to broad familiarity among prescribers and favorable safety records. Yet psychedelic-assisted approaches exhibit an 8.89% CAGR outlook, encouraged by adaptive trial designs and optimized safety protocols after the MDMA setback. Established SNRIs continue to serve treatment-resistant cases, and atypical antipsychotics such as brexpiprazole gain traction as combination agents.

The rise of NMDA receptor modulators, including esketamine approved in China, spotlights a shift toward glutamatergic pathways. Alpha-1 adrenergic antagonists and AI-identified repurposed drugs are also entering trials, enabled by faster de-risking. Developers able to integrate pharmacology with digital support will capture outsized value in the PTSD therapeutics market.

Note: Segment shares of all individual segments available upon report purchase

By Patient Type: Adults Dominate, Pediatric Pipeline Accelerates

Adults contributed 81.78% of PTSD therapeutics market size in 2024 thanks to veteran and first-responder demand. Department of Veterans Affairs backing for psychedelic services further entrenches adult volume. Nonetheless, the pediatric cohort, while smaller, leads growth at 7.67% CAGR as early-intervention studies such as Tonix’s OASIS trial gain traction.

Digital platforms designed for youth engagement and caregiver oversight extend reach where in-person therapy is scarce, aligning with tele-health reimbursement reforms. Ethical barriers and smaller trial pools still temper near-term penetration, but tailored products will eventually lift pediatric uptake within the PTSD therapeutics market.

By Therapy Modality: Pharmacotherapy Holds Ground, Digital Outpaces

Legacy pharmacotherapy stood at an 85.79% share in 2024, underscoring entrenched prescribing behaviors and established reimbursement. However, digital therapeutics grow fastest at 9.56% CAGR, powered by devices like Freespira and game-based neurofeedback systems that achieve FDA clearance.

Combination platforms coupling medication with software and psychotherapeutic coaching are emerging as the optimal model to tackle the disorder’s multi-faceted symptom clusters. As insurer coverage expands, integrated offerings will re-shape revenue mix inside the PTSD therapeutics market.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Hospitals First, Virtual Scripts Rising

Hospital pharmacies processed 47.34% of prescriptions in 2024, reflecting the high acuity of initial PTSD presentations. Retail and specialty outlets continue serving refill demand, yet digital and tele-prescription portals are forecast to post a 9.87% CAGR through 2030.

DEA telemedicine reforms and partnerships such as NRx with Conversio Health for IV ketamine underscore the channel shift. Real-time safety checks embedded in e-prescribing platforms bolster compliance and extend market reach, fueling incremental gains for the PTSD therapeutics market.

Geography Analysis

North America led the PTSD therapeutics market with a 36.47% revenue share in 2024, supported by extensive clinical trial infrastructure, the largest veteran population, and progressive reimbursement for both drugs and software-as-medical-devices. The February 2025 FDA target date for brexpiprazole-sertraline approval and CMS reimbursement codes for digital PTSD tools position the region to remain the primary innovation hub.

Asia-Pacific is the fastest-growing territory, set to register a 7.13% CAGR to 2030. Japan’s clearance of smartphone-delivered cognitive therapy and China’s esketamine nod illustrate a regulatory climate increasingly receptive to novel modalities. Government programs that address mental-health stigma and invest in tele-health infrastructure will amplify patient reach in populous emerging economies, further expanding the PTSD therapeutics market.

Europe shows steady but evolving demand, with policymakers crafting frameworks for psychedelic adoption after Australia’s MDMA and psilocybin rollout. Pan-EU harmonization efforts aim to streamline approvals while maintaining stringent evidence thresholds. Fragmented local regulations still challenge market entry, but rising digital-therapy adoption and robust generic SSRI uptake keep the PTSD therapeutics market resilient across the continent.

Competitive Landscape

The PTSD therapeutics market remains moderately fragmented but is coalescing around three pillars: conventional pharma firms refining combination regimens, software companies securing 510(k) or De Novo clearances, and psychedelic developers navigating Schedule I hurdles. Pfizer and GSK maintain baseline revenue through generic SSRI portfolios, while Otsuka and Lundbeck pursue differentiated dual-agent offerings.

Strategic collaborations accelerate platform approaches: AbbVie’s USD 2 billion deal with Gilgamesh targets neuroplastogens that divorce efficacy from hallucinogenic effects, anticipating payer hesitancy over high-touch psychedelic protocols. AI specialists like Alto Neuroscience integrate biomarker-guided selection to boost trial success rates, creating a precision-medicine edge inside the PTSD therapeutics market.

Barriers to entry rise as stakeholders build controlled-setting infrastructures and specialized therapist networks. Intellectual-property filings—such as Lykos’s MDMA particle-size patents—underline the role of IP in securing competitive moats. Overall, sustainable leadership will hinge on offering cohesive solutions that fuse pharmacology, software, and psychotherapeutic services.

Post Traumatic Stress Disorder Industry Leaders

-

Pfizer Inc.

-

GlaxoSmithKline plc.

-

Otsuka Pharmaceutical

-

Jazz Pharmaceuticals

-

Teva Pharmaceutical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Tonix Pharmaceuticals dosed the first patient in the Phase 2 OASIS trial evaluating TNX-102 SL for acute stress reaction; the study is backed by a USD 3 million Department of Defense grant.

- January 2025: The final Medicare physician fee schedule expands coverage for FDA-cleared digital PTSD therapies, broadening psychologist participation.

- December 2024: JAMA Psychiatry published positive Phase 3 data for Otsuka/Lundbeck brexpiprazole-sertraline; FDA decision expected February 2025.

- November 2024: FDA authorized a 320-patient Phase 2 trial of inhaled THC cannabis for veterans with moderate-to-severe PTSD.

Global Post Traumatic Stress Disorder Report Scope

As per the scope of the report, post-traumatic stress disorder (PTSD) is referred to as a mental health condition that's triggered by a terrifying event, either experiencing it or witnessing it. The treatment of PTSD includes the use of certain medications. The Post Traumatic Stress Disorder Treatment market is segmented by Drug Class (Antidepressants, Anti-anxiety drugs, Antipsychotics, and Other Drug Classes), By Patient (Adult and Children), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Other Distribution Channels) and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| By Drug Class | Selective Serotonin Re-uptake Inhibitors (SSRIs) | ||

| Serotonin-Norepinephrine Re-uptake Inhibitors (SNRIs) | |||

| Atypical Antipsychotics | |||

| Alpha-1 Adrenergic Antagonists | |||

| NMDA Receptor Modulators | |||

| Psychedelic-assisted Therapies (MDMA, Psilocybin, LSD) | |||

| Other Classes (Beta-blockers, Benzodiazepines, Anticonvulsants) | |||

| By Patient Type | Adults | ||

| Children & Adolescents | |||

| By Therapy Modality | Pharmacotherapy | ||

| Psychotherapy | |||

| Digital Therapeutics | |||

| Combination Therapy | |||

| By Distribution Channel | Hospital Pharmacies | ||

| Retail & Specialty Pharmacies | |||

| Digital / Tele-prescription Platforms | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Selective Serotonin Re-uptake Inhibitors (SSRIs) |

| Serotonin-Norepinephrine Re-uptake Inhibitors (SNRIs) |

| Atypical Antipsychotics |

| Alpha-1 Adrenergic Antagonists |

| NMDA Receptor Modulators |

| Psychedelic-assisted Therapies (MDMA, Psilocybin, LSD) |

| Other Classes (Beta-blockers, Benzodiazepines, Anticonvulsants) |

| Adults |

| Children & Adolescents |

| Pharmacotherapy |

| Psychotherapy |

| Digital Therapeutics |

| Combination Therapy |

| Hospital Pharmacies |

| Retail & Specialty Pharmacies |

| Digital / Tele-prescription Platforms |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

Key Questions Answered in the Report

1. What is the current size of the PTSD therapeutics market?

The PTSD therapeutics market is valued at USD 19.04 billion in 2025 and is projected to reach USD 24.74 billion by 2030.

2. Which drug class holds the largest PTSD therapeutics market share?

SSRIs led with a 39.56% PTSD therapeutics market share in 2024.

3. Which therapy modality is growing fastest?

Digital therapeutics are forecast to expand at a 9.56% CAGR between 2025 and 2030.

4. Why did the FDA reject MDMA therapy for PTSD?

Regulators cited safety concerns and functional unblinding, requesting an additional Phase 3 trial before reconsideration.

5. Which region is expanding most rapidly?

Asia-Pacific is expected to register a 7.13% CAGR, driven by regulatory modernization and growing mental-health awareness.

6. How are tele-prescription platforms impacting the PTSD therapeutics industry?

DEA telemedicine reforms and new Medicare codes allow controlled PTSD medications and digital therapies to be prescribed virtually, supporting a 9.87% CAGR in the channel.

Page last updated on: July 4, 2025