Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

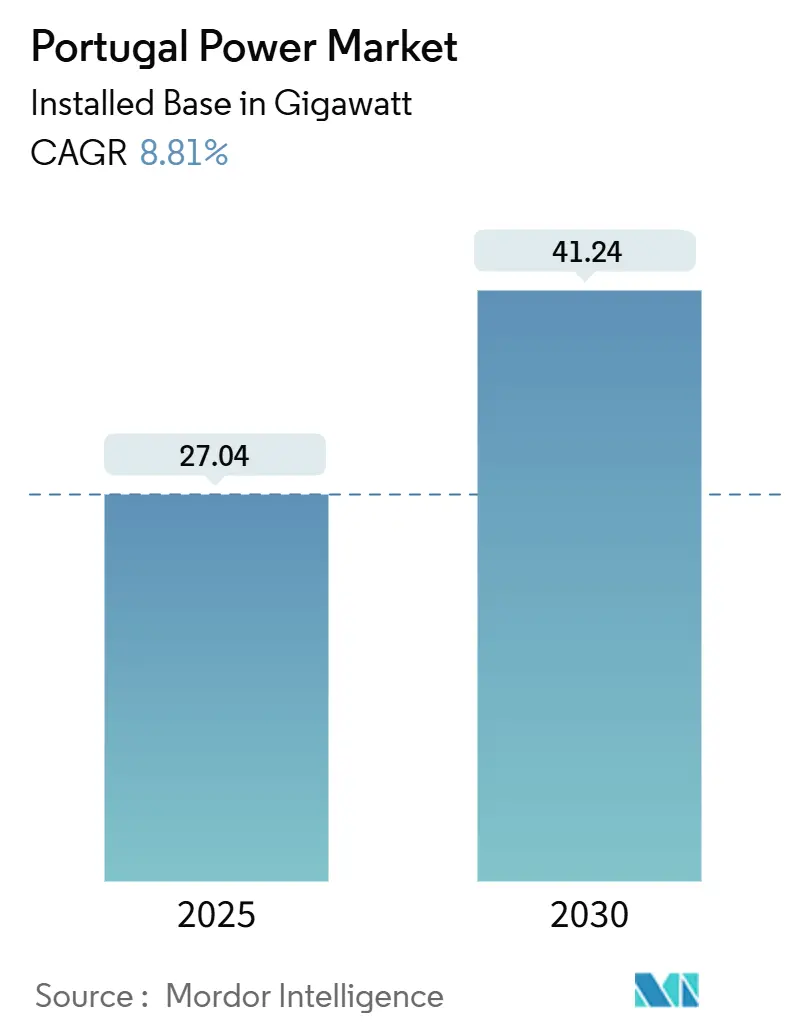

| Market Volume (2025) | 27.04 gigawatt |

| Market Volume (2030) | 41.24 gigawatt |

| Growth Rate (2025 - 2030) | 8.81% CAGR |

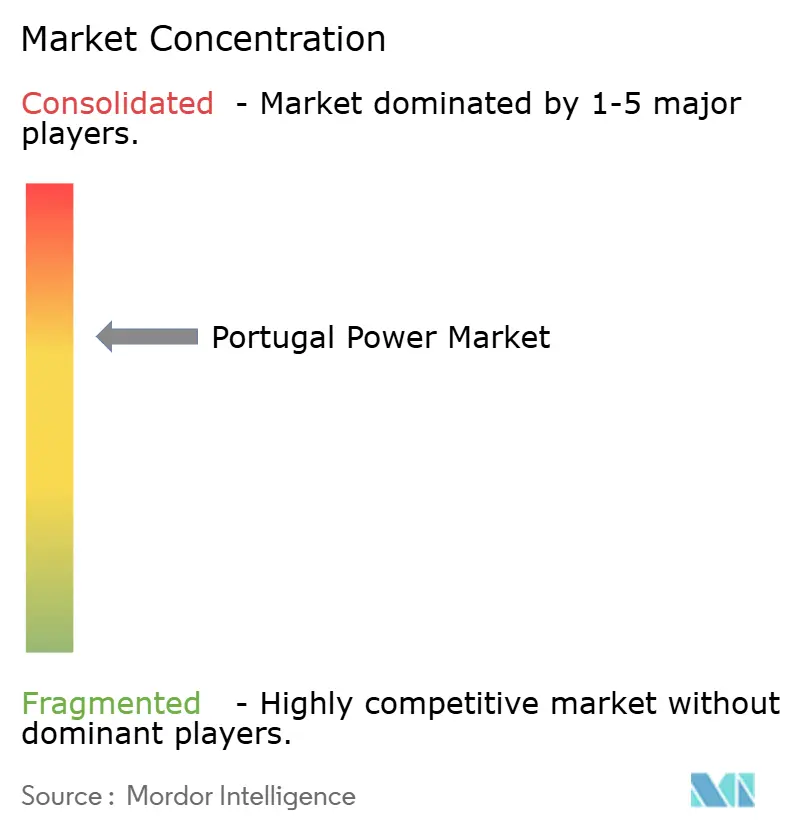

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Portugal Power Market Analysis by Mordor Intelligence

The Portugal Power Market size in terms of installed base is expected to grow from 27.04 gigawatt in 2025 to 41.24 gigawatt by 2030, at a CAGR of 8.81% during the forecast period (2025-2030).

Rapid scaling of solar photovoltaic (PV), steady hydro generation, and a 9.4 GW floating offshore wind pipeline underpin the headline numbers, while European Investment Bank (EIB)–backed transmission upgrades reinforce grid resilience. The National Energy and Climate Plan (NECP) 2030 targets, which aim to achieve an 80% renewable electricity share, serve as the central policy catalyst, supported by world-record auction tariffs that continue to attract international developers. Demand growth stems from large-scale data center and green hydrogen ventures along the Atlantic coast, prompting utilities to sign 24/7 clean power purchase agreements (PPAs) that bundle solar, wind, and storage. Hydropower’s dominant reservoir fleet supplies fast-ramping flexibility, whereas pumped-storage and battery systems mitigate curtailment risk as variable resources account for more than 70% of generation. Despite clear momentum, the Portuguese power market faces headwinds from permitting delays, rural network congestion, and limited cross-border interconnection with Spain, all of which may temper the short-term delivery of auctioned capacity.

Key Report Takeaways

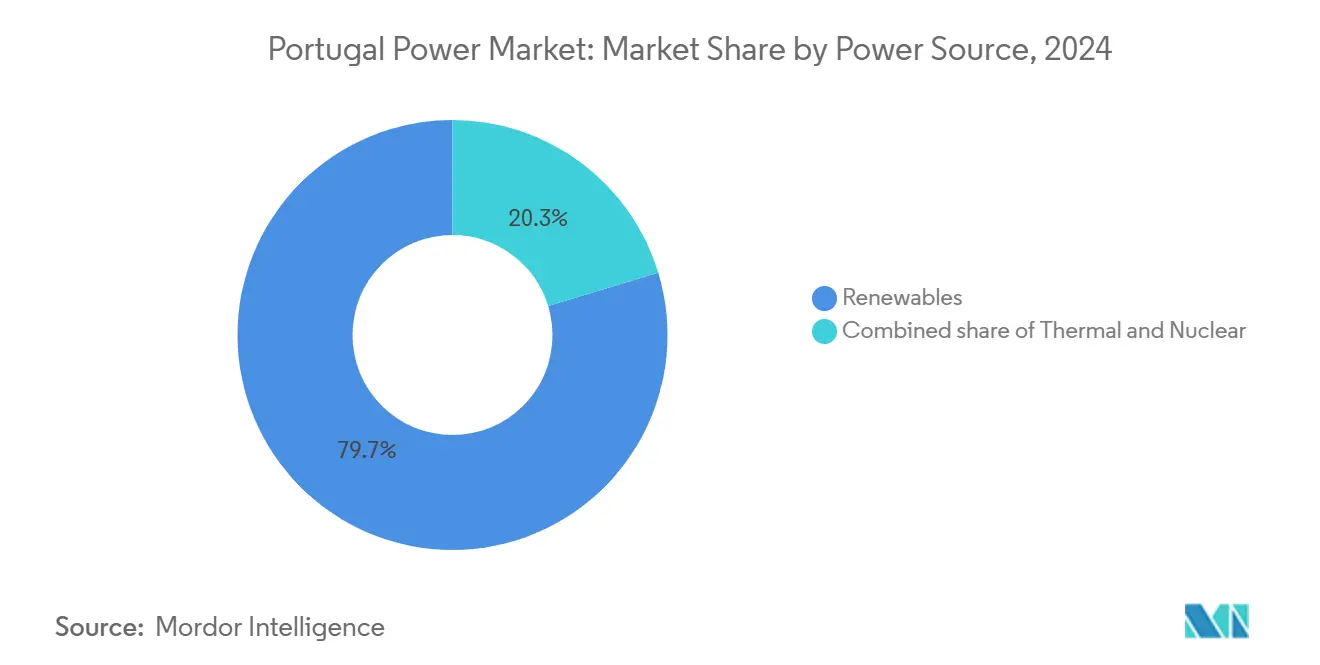

- By power source, renewables commanded 79.7% of Portugal's power market share in 2024, while solar PV is forecast to post a 10.7% CAGR between 2025-2030, the fastest among all technologies.

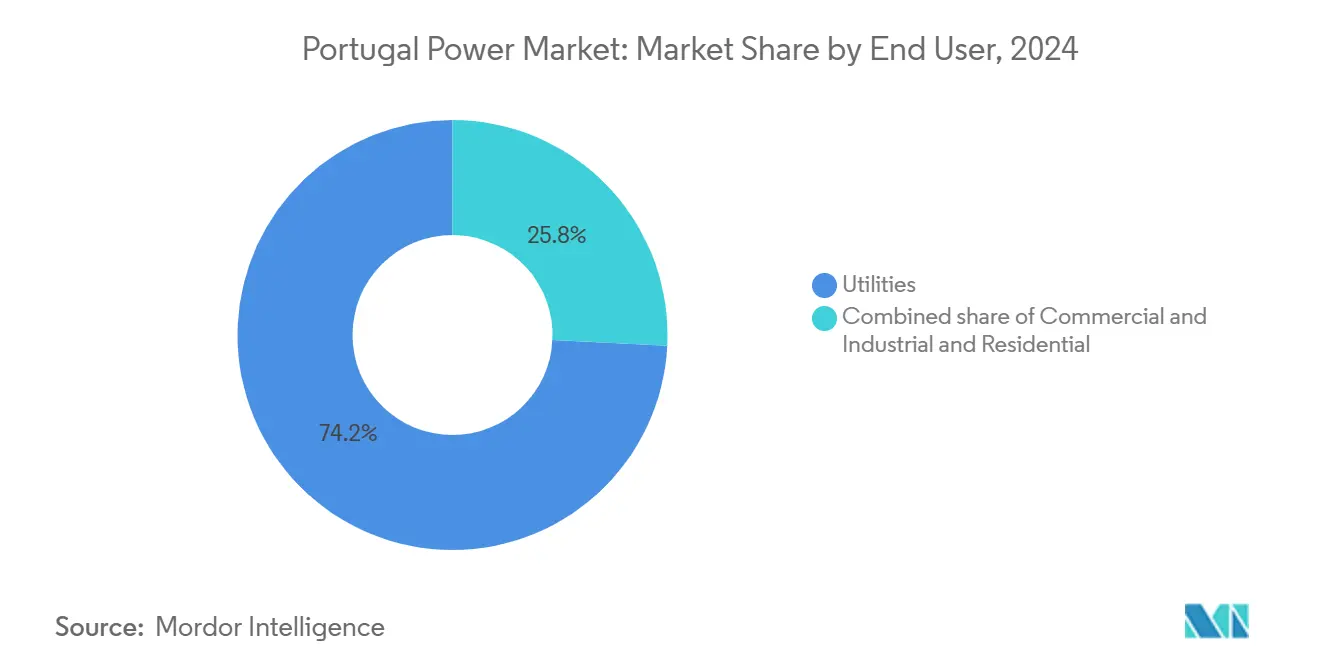

- By end user, utilities led with 74.2% of demand in 2024, whereas the residential segment is projected to expand at a 10.5% CAGR through 2030, driven by the adoption of distributed solar.

Portugal Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated renewable-auction pipeline to meet NECP 2030 targets | +2.1% | National, concentrated in Alentejo and Algarve | Medium term (2-4 years) |

| Rapid LCOE fall of Iberian solar PV & on-shore wind | +1.6% | National, with strongest impact in southern regions | Short term (≤ 2 years) |

| EU-funded grid reinforcement & Spain interconnection upgrades | +1.2% | National, with cross-border focus in northern regions | Long term (≥ 4 years) |

| Hybrid solar-plus-storage PPAs enabling 24/7 green power | +0.9% | National, early adoption in industrial zones | Medium term (2-4 years) |

| Data-center & green-hydrogen boom on Atlantic coast | +0.8% | Atlantic coast, concentrated in Sines and Porto regions | Medium term (2-4 years) |

| Upcoming floating offshore-wind auctions unlocking >10 GW pipeline | +0.7% | Coastal regions, primarily northern and central Atlantic | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Renewable-Auction Pipeline to Meet NECP 2030 Targets

Portugal’s solar tender in 2020 cleared at EUR 11.14/MWh, 25% below the prior global record, cementing the nation’s reputation for ultra-competitive auctions.[1]Government of Portugal, “New Solar Auction Guarantees Annual Savings of 372 Million to Consumers,” portugal.gov.pt Although deadline extensions, now seven since 2020, signal execution bottlenecks, the pipeline exceeds 10 GW of contracted capacity. Revised rules for the October 2025 offshore-wind auction aim to award 9.4 GW of floating sites, building on WindFloat Atlantic’s five-year performance. Auction momentum anchors the Portuguese power market as a prime destination for global infrastructure funds, provided grid connection queues and municipal approvals are streamlined.

Rapid LCOE Fall of Iberian Solar PV & On-Shore Wind

Solar modules now clear Iberian tenders at sub-EUR 20/MWh, reflecting low land-lease rates and abundant irradiation; 86% of 2024 renewable additions were. Neoen’s 272 MWp Azambuja complex exemplifies bankable megaprojects, while Iberdrola’s license for the nation’s largest onshore wind farm maintains wind’s relevancy. A 3.4% reduction in regulated retail tariffs confirms consumer pass-through of lower LCOE, even as grid-access fees create a premium tier for pre-permitted projects.

EU-Funded Grid Reinforcement & Spain Interconnection Upgrades

REN secured a EUR 450 million green loan from the EIB for its 2022-2026 expansion plan, which delivers 4.2 GW of additional transmission capacity.[2]European Investment Bank, “REN Green Loan Agreement,” eib.org A new 400 kV line, slated for completion by the end of 2025, will increase the exchange between Spain and Portugal by 1,000 MW, a step toward the EU's 15% interconnection goal. Complementary distribution-level automation and E-Redes flexibility auctions demonstrate early adoption of demand-response markets, reinforcing Portugal's power market's reputation as a test bed for smart grids.

Hybrid Solar-Plus-Storage PPAs Enabling 24/7 Green Power

Government grants of EUR 100 million in 2024 funded 43 battery projects totaling 500 MW, enabling hybrid plants that commit to round-the-clock delivery. EDP and Siemens Energy structured a 180 MW agreement for the SIN02 data center module, which combines PV, wind, and batteries into a single fixed-price agreement. Such structures boost offtake certainty and elevate the Portugal power market as an exporter of 24/7 green electrons to industrial clusters.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy environmental & municipal permitting process | -1.7% | National, most severe in protected areas | Short term (≤ 2 years) |

| Restricted cross-border capacity causing import dependence | -1.0% | National, with northern border focus | Medium term (2-4 years) |

| Rural MV network congestion in Alentejo/Algarve | -0.8% | Southern regions, concentrated in rural areas | Medium term (2-4 years) |

| Seasonal hydro-surplus curtailment risk | -0.5% | Northern and central regions with major dams | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lengthy Environmental & Municipal Permitting Process

The Ministério Público’s court case against Iberdrola’s 1,000-hectare solar plan, which would require felling 1.5 million trees, spotlights environmental scrutiny. EDP’s CEO labels red tape the top obstacle to EU clean-energy build-out, citing 89-month project cycles that undermine auction economics. Community objections in Alentejo and the mountainous north intensify the challenge, particularly for new offshore wind zones that must negotiate fishing and marine habitat interests.

Restricted Cross-Border Capacity Causing Import Dependence

Portugal's interconnection remains at 3% of installed capacity, one-fifth of the EU target, limiting export of surplus PV at midday. The April 2025 Iberian blackout, which occurred during 78% renewable penetration, underscored the system's vulnerability without external balancing.[3]Baker Institute, “Iberian Peninsula Blackout,” bakerinstitute.org Price spreads of EUR 1.34/MWh with Spain persist, reducing arbitrage and diluting investor returns, while French reluctance to endorse new Pyrenees lines restricts future capacity expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Source: Renewables Dominate Growth Trajectory

Renewables held 79.7% of Portugal's power market share in 2024, reflecting hydro reservoirs, mature onshore wind, and a rapidly growing solar fleet. Solar PV captured 86% of new builds and is on track for a 10.7% CAGR, ensuring it delivers the most incremental growth to the Portuguese power market through 2030. Wind contributes a steady 27% of green energy, with floating offshore prospects poised to unlock more than 10 GW of additional capacity by the next decade.

Hydropower remains crucial for inertia and peak shaving; the 2024 rainfall refilled reservoirs and boosted Alqueva operations. Pumped-hydro upgrades, such as the 520 MW Alqueva II extension, provide fast ramping to integrate surplus PV. Natural-gas plants now cover only 20.3% of installed capacity and increasingly provide peaking support rather than baseload. Biomass, waste-to-energy, and small-scale geothermal round out the mix, contributing a steady 6%, and reinforcing supply diversity in the Portuguese power market.

By End User: Utilities Lead While Residential Segment Accelerates

Utilities accounted for 74.2% of electricity demand in 2024, reflecting centralized dispatch and the capital intensity of large-scale assets held by EDP and REN. The residential segment, however, is projected to advance at a 10.5% CAGR, driven by rooftop-PV subsidies and energy-community models in Algarve municipalities.[4]European Parliament Think-Tank, “Briefing on Portugal Renewable Energy,” europarl.europa.eu Commercial and industrial load grows in tandem with data-center and hydrogen projects, exemplified by Start Campus’s 1.2 GW long-term PPA commitment.

Corporate offtakers increasingly prefer hybrid solar-plus-storage contracts that guarantee 24/7 clean energy supply, as evidenced by EDP’s 15 GW global PPA portfolio, which allocates over 20% to data center consumption. Residential customers benefit from a EUR 100 million storage-grant scheme that finances household batteries paired with PV, expanding prosumer participation and shifting peak-demand profiles in the Portugal power industry.

Geography Analysis

The Atlantic littoral enjoys premium solar irradiance and class II wind speeds, positioning Alentejo and Algarve as PV epicenters, anchored by Akuo’s 181 MW Santa array.[5]TaiyangNews, “Akuo Completes 181 MW Solar Plant,” taiyangnews.info Yet rural medium-voltage lines saturate quickly, compelling developers either to co-finance upgrades or to pivot toward onsite consumption. Northern river basins capture nearly half of hydropower output through 66 cascading plants on the Douro, granting proximity to Spanish interconnections that improve dispatch flexibility.

Sines has evolved into the transition nucleus, hosting Portugal’s primary LNG terminal and the SIN01-SIN05 data campus that will require 1.2 GW of renewable supply. The port’s deepwater draft and grid tie points attract electrolyzer consortia pursuing ammonia exports to Northwest Europe. Coastal municipalities are piloting energy communities, with seven Algarve councils pooling rooftop PV and storage to shave peaks during the tourism season.

Floating offshore wind resource mapping highlights the northern and central coastlines near Viana do Castelo, where 100-meter depths and 10 m/s winds intersect with grid landing points. These areas will host early auction rounds and establish Portugal as the Atlantic analogue to Scotland’s ScotWind cluster, further enhancing the geographical diversity of the Portugal power market.

Competitive Landscape

The Portuguese power market exhibits moderate concentration, with EDP holding 76% of the installed renewable capacity and REN operating the sole transmission concession. Iberdrola, Voltalia, Greenvolt, and Acciona Energía form a second tier of developers scaling solar, wind, and storage portfolios that chip away at incumbent share. Strategic partnerships flourish: Iberdrola invests venture funding in local clean-tech, while EDP leverages a EUR 700 million EIB loan to reinforce the grids of southern Europe.[6]Iberdrola, “Investment in Portuguese Start-Ups,” iberdrola.com

Technology adoption differentiates strategies. Incumbents leverage legacy hydro and substation assets to bundle pumped storage with PV, whereas new entrants focus on pure-play renewables, financed through asset-rotation models. Greenvolt's 2.6 GW battery pipeline exemplifies a shift toward monetizing grid services, thereby expanding the Portuguese power market's revenue base in ancillary services.

Regulatory complexity and scarce grid nodes favor experienced players, yet auction liberalization and corporate-PPA appetite lower entry barriers for niche specialists in floating foundations or electrolyzer integration. As offshore wind tenders commence, consortium configurations that include turbine OEMs, cable manufacturers, and port operators may outcompete single-utility submissions, reshaping the competitive equilibrium without upending incumbent vertical integration.

Portugal Power Industry Leaders

Acciona SA

Finerge SA

Iberdrola SA

Energias de Portugal

Aquila Capital

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Neoen has inaugurated a 272 MWp solar complex in Azambuja, Portugal, with 80% of its output being sold to the Portuguese government under two 15-year power purchase agreements (PPAs). The remaining 20% of the energy, along with its corresponding certificates of origin, is being marketed on the electricity market.

- May 2025: Start Campus launched the SIN01 data center module in Sines as part of an EUR 8.5 billion, 1.2 GW IT capacity campus.

- April 2025: Greenvolt divested its 83.2 MW Pelplin wind farm in Poland to Enea Nowa Energia for EUR 174.4 million. This sale is part of Greenvolt's strategy to monetize assets at the Ready-to-Build (RtB) or Commercial Operation Date (COD) stages, allowing them to reinvest in other projects, specifically in energy storage.

- March 2025: Greenvolt Group has signed an agreement with China’s BYD Energy Storage to develop up to 400 MW/1.6 GWh of battery energy storage system (BESS) projects in Poland. The agreement, led by the Greenvolt Power platform, covers the design and operation of BESS facilities at two locations -- Turosn Koscielna and Nowa Wies Elcka, each with a capacity of 200 MW/800 MWh.

- January 2025: The Ministry of Environment and Energy approved 43 storage schemes, totaling 500 MW, which are funded with EUR 100 million from the Recovery and Resilience Plan.

Portugal Power Market Report Scope

Power generation can be described as the production of electricity using various types of technology, including thermal, solar, wind, hydro, and nuclear. The Portugal power market report includes:

By Power Source

| Thermal (Coal, Natural Gas, Oil and Diesel) |

| Nuclear |

| Renewables (Solar, Wind, Hydro, Geothermal, Biomass & Waste, Tidal) |

By End User

| Utilities |

| Commercial and Industrial |

| Residential |

By Transmission & Distribution (Qualitative Analysis Only)

| High-Voltage Transmission (Above 230 kV) |

| Sub-Transmission (69 to 161 kV) |

| Medium-Voltage Distribution (13.2 to 34.5 kV) |

| Low-Voltage Distribution (<1 kV) |

| By Power Source | Thermal (Coal, Natural Gas, Oil and Diesel) |

| Nuclear | |

| Renewables (Solar, Wind, Hydro, Geothermal, Biomass & Waste, Tidal) | |

| By End User | Utilities |

| Commercial and Industrial | |

| Residential | |

| By Transmission & Distribution (Qualitative Analysis Only) | High-Voltage Transmission (Above 230 kV) |

| Sub-Transmission (69 to 161 kV) | |

| Medium-Voltage Distribution (13.2 to 34.5 kV) | |

| Low-Voltage Distribution (<1 kV) |

Key Questions Answered in the Report

How large is Portugal’s installed generation capacity in 2025?

The grid totals 27.04 GW, with expansion plans pushing toward 41.24 GW by 2030.

Which technology will add the most capacity by 2030 in Portugal?

Solar PV leads, poised for a 10.7% CAGR through 2030 thanks to record-low auction tariffs and rapid build schedules.

Why did Portugal experience the April 2025 blackout?

The event stemmed from 78% renewable penetration without adequate cross-border balancing or grid-stability services.

What drives residential electricity growth in Portugal?

Rooftop-PV subsidies, energy-community projects, and household battery grants accelerate residential adoption.

How much offshore-wind capacity is Portugal targeting?

Government auctions aim to allocate 9.4 GW of floating-offshore capacity by 2030, building on WindFloat Atlantic’s success.

Who dominates Portugal’s renewable generation market?

EDP controls 76% of installed renewable capacity and produced 91% renewable electricity in Q1 2025.

Page last updated on: