Portable Washing Machines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.92 Billion |

| Market Size (2031) | USD 2.69 Billion |

| Growth Rate (2026 - 2031) | 6.94% CAGR |

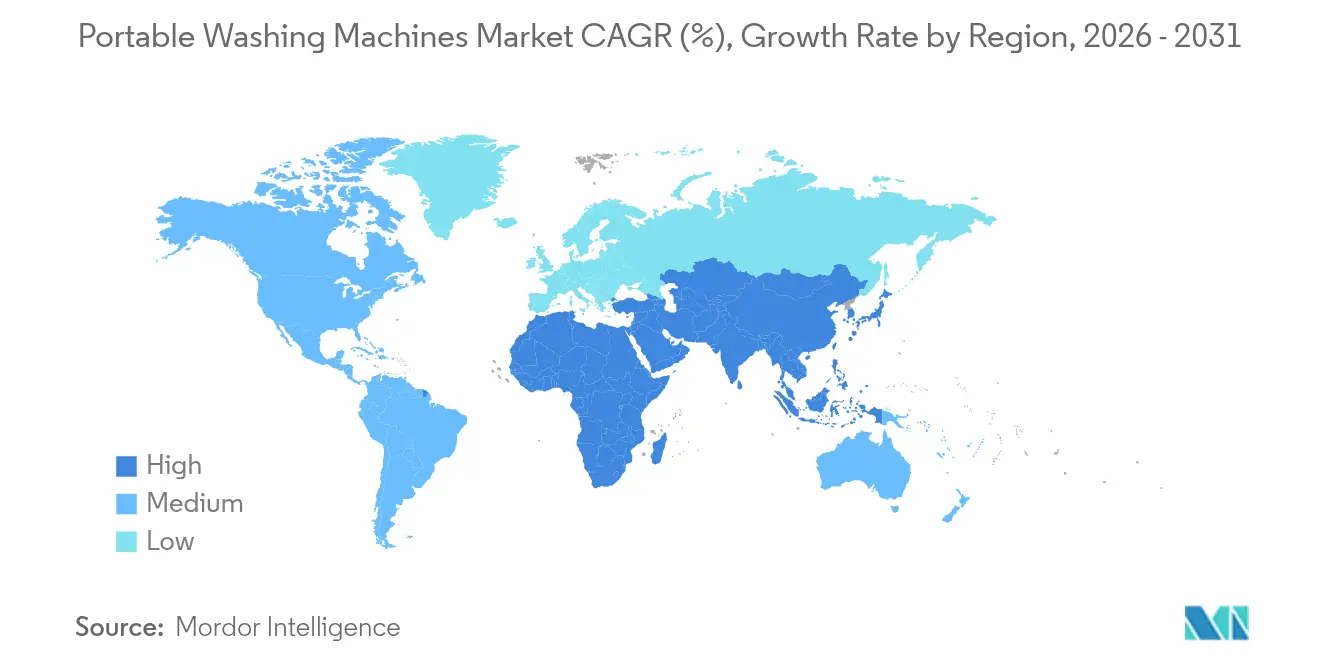

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

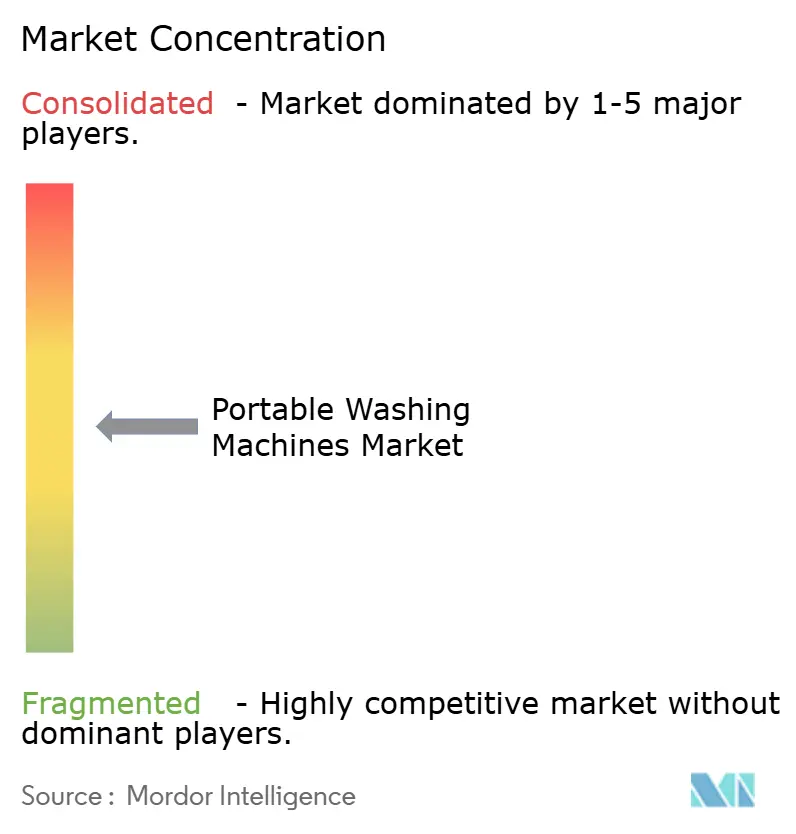

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Portable Washing Machines Market Analysis by Mordor Intelligence

Portable washing machines market size in 2026 is estimated at USD 1.92 billion, growing from 2025 value of USD 1.80 billion with 2031 projections showing USD 2.69 billion, growing at 6.94% CAGR over 2026-2031. Urbanization, shrinking living spaces, and rising disposable income push consumers toward compact laundry solutions that match full-size performance. Rapid progress in inverter motors, IoT connectivity, and water-saving programs keeps the portable washing machines market firmly aligned with new U.S. energy and water rules that take effect in 2028[1]Ministry of Energy, “Energy Conservation Program: Clothes Washer Standards,” energy.gov. Regional demand remains balanced against stricter eco-design laws, which favor brands able to meet higher Modified Energy Factor and lower Integrated Water Factor thresholds. Asia-Pacific’s dominance reflects strong middle-class growth, while e-commerce broadens access in North America and Europe. Producers that can localize final assembly, shorten lead times, and embed smart features are well placed to defend margins in an increasingly competitive field.

Key Report Takeaways

- By product type, top-load units led with 64.35% of the portable washing machine market share in 2025, while front-load machines are expanding at a 7.55% CAGR through 2031.

- By capacity, below 5 kg models dominated 2025 sales with a 54.20% revenue share; however, above 7 kg units are set to grow at 7.85% CAGR, the fastest among all capacities.

- By power source, electric models retained 89.20% of the portable washing machine market size in 2025; solar-ready machines are expected to expand at an 8.10% CAGR to 2031.

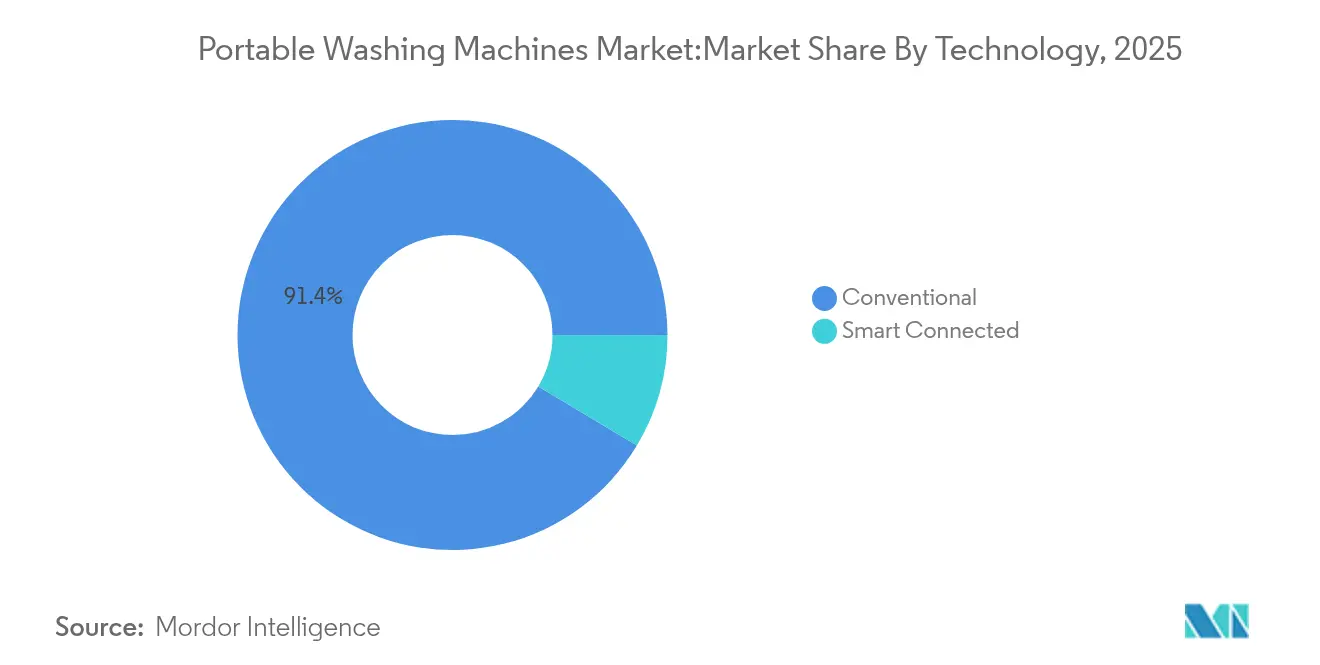

- By technology, conventional units held the greatest share of 91.40% in 2025, and Smart Connected adoption is forecast to keep pace at 8.45% CAGR.

- By end user, the residential buyers commanded 69.10% of the portable washing machine market size in 2025; the commercial segment is growing at a 6.95% CAGR.

- By distribution channel, B2C/retail held the top share of 80.90% 2025, and the online segment is scaling at 8.50% CAGR, reflecting stronger direct-to-consumer models.

- By geography, Asia-Pacific accounted for a 38.70% slice of the portable washing machine market share in 2025, and is advancing at a 7.45% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Portable Washing Machines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Disposable Income of Urban Micro-Households | +1.8% | Asia-Pacific core, spill-over to Latin America | Medium term (2-4 years) |

| Rapid Product Innovation (Inverter, IoT, Energy-Saving) | +1.5% | Global, early adoption in North America & the EU | Short term (≤ 2 years) |

| Expansion of E-Commerce Appliance Channels | +1.2% | Global, most pronounced in emerging markets | Short term (≤ 2 years) |

| Van-Life & Recreational Vehicle Boom Demanding Off-Grid Washing Solutions | +0.8% | North America & EU, niche Australia | Medium term (2-4 years) |

| Solar-Powered Humanitarian Housing Deployments | +0.4% | Africa, the Middle East, and disaster-prone regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Income of Urban Micro-Households

Urban micro-households are the fastest-growing buyer group for portable washers. Whirlpool and Hindustan Unilever promote first-time adoption in India through joint campaigns that couple stain-removal detergents with compact appliances. Better income prospects let entry-level consumers shift from hand washing to mechanized laundry without sacrificing floor space. Property developers continue to favor smaller apartments, which reinforces demand for compact formats. Add-on sales of detergents optimized for low-water cycles increase lifetime revenue per unit and deepen brand loyalty. This dynamic keeps the portable washing machines market firmly anchored to consumer buying power in large urban centers.

Rapid Product Innovation (Inverter, IoT, Energy-Saving)

Technological leapfrogging sits at the heart of market differentiation. Samsung extended its Bespoke AI range with a compact model that suggests the ideal cycle and flags maintenance needs[2]Samsung Newsroom Staff, “Samsung Unveils Bespoke AI Laundry Line,” news.samsung.com . LG and Samsung now battle in 25 kg combo machines that fold heat-pump drying into a small footprint, indicating engineering gains that spill into the portable segment. Compliance with 2025 DOE test methods pushes every brand to lift Modified Energy Factor scores, prompting broader use of inverter drives and low-noise pumps. Such enhancements unlock premium pricing, narrow the resource-efficiency gap with full-size washers, and widen the global appeal of the portable washing machines market.

Expansion of E-commerce Appliance Channels

Digital retail changes how shoppers research and buy appliances. Rich product pages outline unit dimensions, electrical needs, and installation steps that bricks-and-mortar stores cannot match at scale. Instant customer reviews build trust among buyers who lack product experience. Online sales shorten the path between factory and living room, trimming channel margins and fueling faster price discovery. Manufacturers also gain data on buyer behavior, guiding iterative design cycles that match emerging needs. These gains explain why the portable washing machines market registers the highest online growth rate among major household appliance categories.

Van-life & Recreational Vehicle Boom Demanding Off-Grid Washing Solutions

The rise of remote work and outdoor living turns vans and recreational vehicles into rolling homes. Demand centers on 12 V or solar-ready washers that handle light loads without straining battery banks. Brands incorporate collapsible tubs, fold-out handles, and onboard filtration to conserve water. Though niche, this customer base pays above-average prices for autonomy and low weight. Secondary demand stems from boat owners, disaster response teams, and mobile clinics, all of which need laundry in places without grid power. The segment raises overall average selling prices and opens fresh pockets of growth within the portable washing machines market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Abundant Laundromats & On-Demand Laundry Apps | -1.1% | Urban centers globally, strongest in North America & EU | Short term (≤ 2 years) |

| Limited Load Capacity vs. Conventional Washers | -0.9% | Global, particularly affecting larger households | Medium term (2-4 years) |

| Durability & Performance Perception Gaps | -0.7% | Emerging markets, price-sensitive segments globally | Medium term (2-4 years) |

| Tightening Small-Appliance Energy Regulations | -0.6% | North America, EU, with gradual expansion to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Abundant Laundromats & On-Demand Laundry Apps

Well-capitalized laundromat chains and mobile laundry platforms compete on convenience, especially in dense cities where apartment space is scarce. Pay-per-use pricing reduces upfront costs and appeals to travelers and students. App-based pickup services extend reach into premium neighborhoods, further eroding appliance ownership incentives. Markets that deregulate utility pricing may see commercial laundries gain further advantage through volume discounts. While this dynamic softens near-term growth, portable models still appeal to users who demand control over hygiene, fabric care, and operating schedules.

Limited Load Capacity versus Conventional Washers

Portable washers rarely exceed 7 kg per cycle, forcing larger families to split loads and consume more time. The gap widens as full-size machines stretch to 15 kg while raising per-cycle efficiency, making the larger format more economical per kilogram of laundry. Manufacturers respond by packing larger drums into slim cabinets and adopting more efficient motor layouts. Hisense’s 4-in-1 heat-pump model shows that technical ceilings continue to rise[3]China Daily Staff, “Hisense Debuts 4-in-1 Heat-Pump Washer,” chinadaily.com.cn. Yet capacity will remain a structural restraint until major breakthroughs in drum geometry emerge.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Front-Load Growth Reshapes the Mix

Top-load machines still dominate 2025 demand with 64.35% market share, especially among first-time buyers in price-sensitive regions where washer ownership remains below 35%. Simpler mechanics, familiar ergonomics, and easier maintenance protect this position. Bulk procurement by micro-finance programs further lifts volumes in Southeast Asia. Yet as smart displays, inversion motors, and precision dosing migrate across product lines, the front-load value proposition strengthens and shifts global buyer preference. This shift is instrumental in the 6.94% headline CAGR recorded for the portable washing machines market.

Front-load variants, though less familiar to legacy buyers, are expanding at a 7.55% CAGR and will keep rising their portion of the portable washing machines market share next to top-load leaders. Engineers cite lower water usage and gentler tumble action that meets new energy metrics. Early adopters view the frontal door and horizontal drum as premium cues that justify a higher price. Manufacturers streamline supply by adapting full-size front-load components to portable formats, lowering the incremental cost per unit. Enhanced wash quality also trims detergent use, a small but visible benefit to eco-aware households.

By Capacity: Polarized Preferences Guide Design Strategy

The below 5 kg class dominated 2025 sales with a 54.20% revenue share, supported by single-person flats, student dorms, and senior living complexes. Lower sticker prices, lighter shipping weight, and plug-and-play setup make these compact washers an easy upgrade from hand washing. Brands address noise and vibration, two key concerns in high-rise living, by adding suspension pads and variable-speed drums. At the opposite end, above 7 kg models are the fastest-growing slice, advancing at 7.85% CAGR through 2031 and steadily enlarging their slice of the portable washing machines market. Their broader drum size closes the performance gap with mid-size conventional units, making them popular in suburban homes, co-living spaces, and smaller hotels.

Between the two extremes lies the 5–7 kg tier, which serves couples and small families that want a versatile appliance while retaining a smaller footprint. Flexible dosing, custom soak programs, and steam cycles push the average selling price higher in this sub-segment. As inverter motors unlock greater torque within the same cabinet, all capacity tiers gain wash quality improvements without inflating energy bills. The resulting spectrum of drum sizes lets vendors tailor marketing messages to distinct micro-segments of the portable washing machines market rather than chase one “average” customer.

By Power Source: Electric Leads, while Solar Options Emerge

The power source, electric models, retained 89.20% of the portable washing machine market size in 2025.Plug-in electric models represent the mainstream of the portable washing machines market and will keep their lead for the forecast period. They link directly to household sockets and do not require auxiliary chargers, making them suitable for rental properties. Efficiency gains arrive via brushless direct-drive motors that cut stand-by consumption, while thermal sensors reduce overheating risk in tight cabinets. Brands with global footprints ship the same universal-voltage control boards worldwide, lowering cost and parts inventory.

The solar-ready machines are expected to expand at an 8.10% CAGR to 2031. Solar-ready DC units remain a single-digit niche today but answer the sustainability push in off-grid settlements, humanitarian camps, and remote lodges. Non-profit collaborations, such as Whirlpool Foundation’s support of The Washing Machine Project, distribute hand-crank and solar-enabled units in disaster relief zones. Technical hurdles include panel sizing, battery depth-of-discharge, and water storage. As lithium-ion prices fall, market penetration is expected to expand in Africa and island states, broadening the portable washing machines industry footprint. Manual washers will persist as ultra-low-cost choices where shipping power sources are impractical.

By Technology: Smart Features Transition from Novelty to Standard

Conventional non-connected units still led global volume in 2025, but Wi-Fi and Bluetooth modules are rapidly moving from premium add-ons to baseline expectations. BSH Home Appliances has begun shipping Matter-compatible units, paving the way for plug-and-play integration with third-party smart-home hubs. Remote monitoring of remaining cycle time and machine health reduces user anxiety about leaks in rented spaces. Brands also test subscription programs for firmware upgrades and performance analytics, opening new revenue lines beyond hardware.

Price used to be the chief obstacle for technology, yet the cost of cloud services per unit has fallen below USD 1 annually. Vendors collect anonymized run data that reveal regional washing habits, informing targeted detergent partnerships and future design tweaks. As these feedback loops tighten, the portable washing machines market gains a data-centric layer that lifts both margins and customer retention.

By End User: Residential Core with Expanding Commercial Horizons

Residential buyers account for 69.10% of the global revenue, while the commercial segment maintains a 6.95% CAGR. Smaller living units, flexible lease contracts, and high mobility drive demand for appliances that can roll into a closet at move-out time. College dormitories and micro-apartments install built-in kitchenettes but rarely provide shared laundry, steering tenants toward personal portable washers. In mature markets, homeowners purchase a portable machine as a secondary washer, reserved for delicate or specialty fabrics.

Commercial establishments form the fastest-emerging opportunity. Hostels, wellness clinics, and recreational camps adopt portable models to avoid major plumbing retrofits. After the Kahramanmaraş earthquake, relief agencies used compact washers to sanitize bedding in temporary shelters, underscoring resilience benefits. The mix of cyclical tourism and rising climate-related disruptions means authorities and NGOs will continue procuring mobile laundry infrastructure, a trend that lifts non-residential demand within the portable washing machines market.

By Distribution Channel: Digital Commerce Accelerates the Cycle

Online marketplaces command the leading share and a 8.50% CAGR. Brands control storefront aesthetics, publish video installation guides, and bundle extended warranties, building trust where hands-on experience is impossible. Return logistics improve yearly, lowering perceived risk for buyers. Electronic payment penetration in South and Southeast Asia unlocks new buyer pools, while buy-now-pay-later plans enable larger average order sizes.

Multi-brand physical stores still attract shoppers who want to test noise levels or inspect hose connectors. They remain critical in markets with limited home-delivery reliability. Exclusive brand outlets deliver curated experiences for premium lines, offering concierge installation and IoT onboarding. Direct B2B sales cover bulk orders for hotels, hostels, and healthcare facilities. This multi-channel matrix drives wide geographic coverage for the portable washing machines market, balancing margin and reach.

Geography Analysis

Asia-Pacific ranks first by revenue and posts a 7.45% CAGR through 2031. China’s domestic makers benefit from clustered supply chains, keeping average selling prices lower than Western equivalents. India’s household penetration level, still under 20%, sets a large runway for growth. Whirlpool and Hindustan Unilever’s joint promotion illustrates how detergent and appliance brands cooperate to convert first-time buyers. Rising urban wages and limited floor space keep consumers gravitating toward compact washers even as full-size ownership moves up the income curve.

North America registers mid-single-digit growth. The U.S. energy rule scheduled for 2028 pressures manufacturers to cut kilowatt-hour consumption, driving new model launches every 18 months. The van-life trend also fuels demand for 12 V and solar-capable washers that run in mobile dwellings. Mexico consolidates its role as a manufacturing hub, supplying the U.S. and Canada while building a domestic mid-tier consumer base. Online fulfilment hubs in California and Texas cut delivery times, reinforcing regional supply resilience within the portable washing machines market.

Europe maintains a low-to-mid single-digit CAGR. High urban density, stringent water tariffs, and mature online retail ease adoption. Government rebates support energy-efficient purchases, nudging consumers toward inverter-driven portable models. German-based BSH Home Appliances reported 4.1% North American growth in Laundry Care for 2024, proving that European engineering resonates abroad. Meanwhile, Eastern European countries with expanding middle classes display above-average take-up, closing the gap with Western peers.

Mordor Intelligence provides coverage of the portable washing machines market across other key regional markets, including Middle East, Europe, and Asia, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to United States incorporating local coverage and market participation, as required.

Competitive Landscape

The portable washing machines market shows moderate concentration. Haier, Midea, Samsung, LG, Whirlpool, Hisense, and BSH Home Appliances collectively control more than half of the global volume. Competitive differentiation now centers on water use, noise reduction, and smart-home pairing rather than simple cost. Samsung and LG spar over AI-driven cycle optimization in large-capacity washer-dryer portfolios, with lessons feeding back into smaller formats. Hisense’s heat-pump launch validates Chinese brands’ growing R&D depth.

Regional investments align with reshoring and near-shoring goals that cushion supply risk. North American makers expand U.S. and Mexican plants to limit trans-Pacific freight exposure. Component suppliers for pumps, valves, and PCBAs diversify across Vietnam and Indonesia, enhancing resilience. Collaboration remains pivotal: Whirlpool works with detergent brands for after-sales cross-promotion, while Bosch partners with connectivity alliances to future-proof interoperability. Such strategies foster stickier customer relationships and safeguard pricing power across the portable washing machines industry.

Portable Washing Machines Industry Leaders

LG Electronics

Whirlpool Corporation

Midea Group

Samsung Electronics

Haier Smart Home Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Hisense unveiled the world’s first 4-in-1 heat-pump washing and drying machine with three independent laundry compartments at the China Household Appliances and Consumer Electronics Expo.

- January 2025: The U.S. Department of Energy finalized updated test procedures for residential and commercial clothes washers, effective Jul 16, 2025, standardizing cloth bundles and statistical thresholds.

- June 2024: Whirlpool of India and Hindustan Unilever entered a marketing tie-up that pairs Surf Excel stain-removal claims with Whirlpool’s 6th Sense tech to attract first-time Indian washer buyers.

Global Portable Washing Machines Market Report Scope

A portable washing machine is a compact appliance that works the same way a full-size washing machine works, it has a tub with an agitator. A complete background analysis of the global portable washing machine market, which includes an assessment of the parental market, emerging trends by segments and regional markets, significant changes in market dynamics and market overview is covered in the report. The report also features the qualitative and quantitative assessment by analyzing data gathered from industry analysts and market participants across key points in the industry's value chain. Global Portable Washing Machines Market is segmented by Product Type(Top Load, Front Load), by End- User(Residential, Commercial), by Distribution Channel (Multi-Branded Stores, Specialty Stores, Online and Other Distribution Channels), and by Region (North America, Europe, Asia Pacific, South America, and Middle East & Africa). The market size and forecasts are provided in terms of value (USD billion) for all the above segments.

| Top Load |

| Front Load |

| Below 5 kg |

| 5–7 kg |

| Above 7 kg |

| Electric (AC) |

| Manual/Hand-Crank |

| Solar-Compatible DC |

| Smart Connected |

| Conventional |

| Residential |

| Commercial (e.g., Hostels, Clinics, Campgrounds) |

| B2C/Retail | Multi-brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| B2B/Directly from the Manufacturers |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Middle East And Africa | United Arab of Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Product | Top Load | |

| Front Load | ||

| By Capacity | Below 5 kg | |

| 5–7 kg | ||

| Above 7 kg | ||

| By Power Source | Electric (AC) | |

| Manual/Hand-Crank | ||

| Solar-Compatible DC | ||

| By Technology | Smart Connected | |

| Conventional | ||

| By End User | Residential | |

| Commercial (e.g., Hostels, Clinics, Campgrounds) | ||

| By Distribution Channel | B2C/Retail | Multi-brand Stores |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Directly from the Manufacturers | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Middle East And Africa | United Arab of Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the current value of the portable washing machines market?

The portable washing machines market size is USD 1.92 billion in 2026 and is expected to reach USD 2.69 billion by 2031.

Which region holds the largest share of global sales?

Asia-Pacific leads the portable washing machines market due to rapid urbanization, rising incomes, and dense living conditions that favor compact appliances.

What growth rate can the market expect through 2031?

The market is forecast to register a 6.94% CAGR during the 2026–2031 period.

Which product type is expanding the fastest?

Front-load portable washers post the highest growth, advancing at 7.55% CAGR as consumers seek superior water and energy efficiency.

How are online channels influencing sales?

Online platforms already capture the highest share and grow at 8.50% CAGR because they allow detailed product comparisons, flexible payment options, and direct deliveries that fit compact living scenarios.

What impact will new U.S. energy standards have on manufacturers?

Updated Department of Energy test procedures, effective in 2025 and stricter standards in 2028, compel brands to improve Modified Energy Factor and Integrated Water Factor scores, accelerating innovation in inverter motors and smart wash algorithms.

Page last updated on: