Porcelain Insulators Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 9.87 Billion |

| Market Size (2030) | USD 13.43 Billion |

| Growth Rate (2025 - 2030) | 6.36% CAGR |

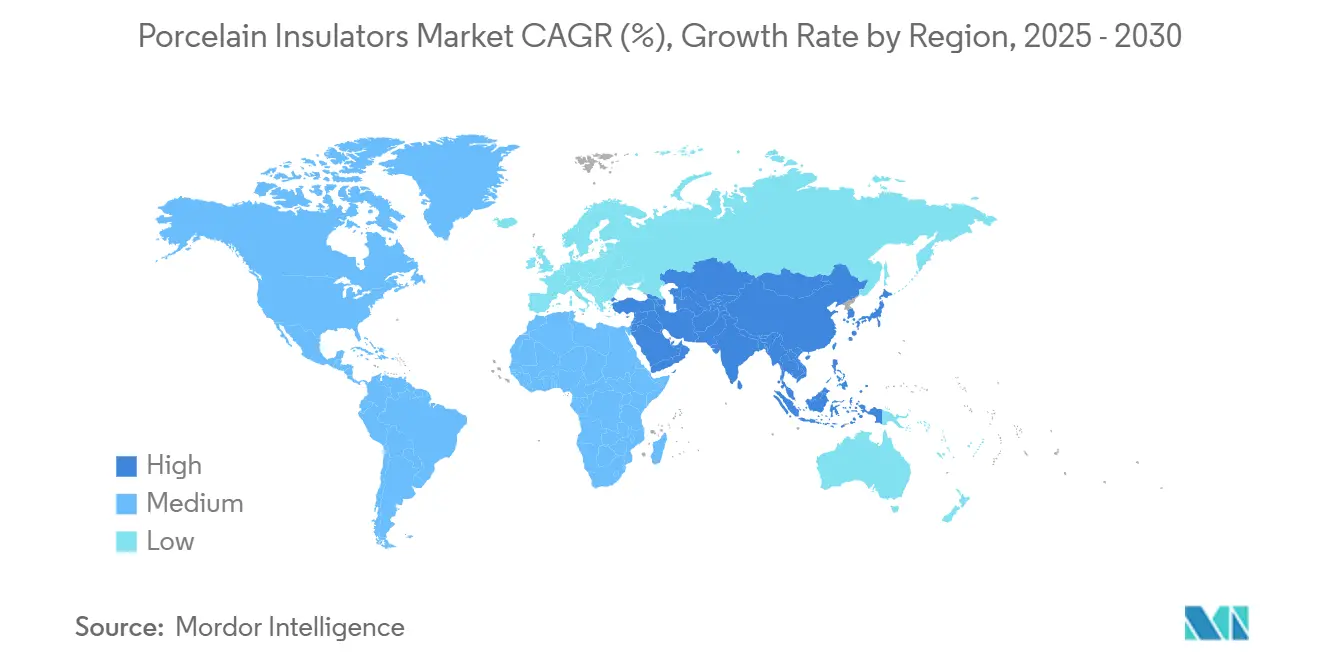

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Porcelain Insulators Market Analysis by Mordor Intelligence

The Porcelain Insulators Market size is estimated at USD 9.87 billion in 2025, and is expected to reach USD 13.43 billion by 2030, at a CAGR of 6.36% during the forecast period (2025-2030).

Momentum comes from grid-modernization cycles, ultra-high-voltage (UHV) transmission buildouts, and policy-driven domestic sourcing mandates. Utilities are accelerating replacement of aging hardware in the OECD, while Asia-Pacific drives green-field demand through renewable integration and rural electrification projects. Price-sensitive distribution networks continue to weigh polymer alternatives, yet porcelain retains an edge in mechanical strength, dielectric performance, and long service life. Manufacturers that blend raw-material integration with advanced coatings capture value in premium applications where reliability outweighs initial cost.

Key Report Takeaways

- By product type, suspension insulators led with 48.2 % revenue share in 2024; strain designs are projected to expand at a 7.8 % CAGR through 2030.

- By voltage rating, applications above 69 kV accounted for 54.8 % of the porcelain insulators market share in 2024 and are progressing at a 6.7 % CAGR to 2030.

- By installation environment, overhead lines captured 62.5 % of the porcelain insulators market size in 2024, while substation placements recorded the fastest 7.4 % CAGR.

- By end user, utilities commanded 69.1 % of 2024 demand and continue at a 6.5 % CAGR as asset-management budgets prioritize reliability upgrades.

- By geography, Asia-Pacific held 49.0 % of revenue in 2024; the region exhibits a 6.9 % CAGR on the back of Chinese UHV expansion and India’s Make in India local-content regime.

Global Porcelain Insulators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of HV transmission corridors | +1.80% | Asia-Pacific core, spillover to MEA | Long term (≥ 4 years) |

| Grid refurbishment in OECD economies | +1.50% | North America & EU | Medium term (2-4 years) |

| Rural electrification roll-outs | +1.20% | ASEAN, India, Bangladesh | Medium term (2-4 years) |

| Rail-traction electrification surge | +0.90% | Global, concentration in Europe & China | Short term (≤ 2 years) |

| Adoption of hydrophobic nano-coated strings | +0.60% | Global, early adoption in harsh environments | Long term (≥ 4 years) |

| Local-content mandates | +0.40% | India, China, Brazil | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of HV transmission corridors in Asia & Africa

State Grid Corporation’s 600 billion yuan 2024 capex program, including the 1,901 km Sichuan-Tibet UHVDC line, underscores how large-scale corridors boost premium demand for porcelain strings engineered for extreme altitude, contamination, and icing. ASEAN’s Power Grid masterplan adds another USD 100 billion through 2045, requiring insulators with superior mechanical strength for 500 kV and above.(1)Source: Asian Development Bank, “ASEAN Power Grid Vision 2045,” adb.org Porcelain’s higher mass is offset by proven field performance and compatibility with conventional hardware, creating a durable specification advantage that suppliers leverage by bundling long-term service warranties.

Grid refurbishment programs in OECD economies

North American and European utilities are replacing 1960s-era hardware to meet reliability indices and renewable-integration targets. The International Energy Agency estimates annual transmission investments must average USD 140 billion through 2027, funneling steady orders toward insulators that drop into existing steelwork without redesign [IEA.ORG]. Lifecycle assessments reveal porcelain units offer predictable aging profiles, letting asset managers time replacements around outage windows. Sediver’s U.S. laboratory initiative exemplifies service-based value propositions aimed at refurbishment budgets.(2)Source: Sediver, “U.S. Test Laboratory Opening,” sediver.com

Rural electrification roll-outs (South & SE Asia)

IEA modelling shows Southeast Asia will absorb more than 25 % of incremental global electricity demand by 2035, translating into dense 11-kV and 33-kV feeder programs in Indonesia, Vietnam, and the Philippines. Governments prefer established ceramic supply chains to minimize project delays, while India’s 50 % local-content rule locks in domestic sourcing for Class I bids. Despite price competition, these factors safeguard porcelain volumes in the 1-69 kV bracket.

Rail-traction electrification surge

Europe’s Trans-European Transport Network and China’s freight-rail decarbonization push require insulators certified for dynamic loading, vibration, and thermal cycling. Porcelain’s thermal stability and long fatigue life meet rail standards such as EN 50119, ensuring continued selection even when polymers dominate static structures. OEM partnerships around pantograph assemblies elevate specification stickiness and support price premiums.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid shift toward composite & polymer units | -1.40% | Global, acceleration in seismic zones | Short term (≤ 2 years) |

| Volatile alumina/kaolin input prices | -0.80% | Global, highest impact in Asia-Pacific | Short term (≤ 2 years) |

| PFAS-linked glazing restrictions | -0.50% | North America & EU regulatory jurisdictions | Medium term (2-4 years) |

| Counterfeit units in price-sensitive markets | -0.30% | Emerging markets, notably South Asia & Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid shift toward composite & polymer insulators

Seismic design codes in Japan, Chile, and California award higher points for lighter assemblies, accelerating polymer adoption. Yash Highvoltage’s product roadmap now allocates 60 % of new R&D to silicone housings, signaling supply-side momentum. Yet long-term field data show glass-filled composites experience higher leakage current in high-pollution corridors, preserving a porcelain niche in coastal and desert zones.

Volatile alumina/kaolin input prices

Spot alumina rose 22 % between Q1-Q4 2024 on energy-cost spikes, squeezing smaller Asian kilns that buy on short contracts. Integrated players such as NGK hedge exposure by co-owning bauxite mines and using captive power, cushioning margins.(3)NGK Insulators, “Annual Report 2023,” ngkinsulators.co.jp Volatility encourages supply-chain consolidation, raising barriers for new entrants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Suspension Dominates Transmission Applications

Suspension units owned 48.2 % of 2024 revenue in the porcelain insulators market, benefiting directly from the 5,373 km of new UHV corridors energized in China during the year.(4)State Grid Corporation of China, “2024 UHV Line Statistics,” sgcc.com.cn Long string assemblies cope with conductor sag, aeolian vibration, and ice load, ensuring low line losses at 800 kV and beyond. Manufacturers differentiate via double-glazing and zinc-sleeve pin designs that resist interface corrosion across 40-year lifecycles.

Strain designs, though smaller in volume, post a robust 7.8 % CAGR to 2030 as catenary-support and renewable interconnection sites demand high mechanical ratings. Hydrophobic nano-coatings and forged steel end-fittings allow strain sets to match 300 kN ultimate tensile loads, positioning suppliers for rail electrification roll-outs. Pin and shackle formats in rural 11 kV networks remain cost-driven; nonetheless, steady public funding in ASEAN village electrification maintains baseline orders. Specialty glaze lines targeting 145° contact angles help premium products undercut polymer encroachment in desert and coastal feeders.

By Voltage Rating: High Voltage Segment Drives Premium Growth

Applications above 69 kV generated 54.8 % of 2024 sales and carry a 6.7 % forecast CAGR, underpinning the porcelain insulators market size for premium designs. UHV projects in China, India, and the East Africa Power Pool require 800 kV and 1,100 kV strings where dielectric and mechanical safety factors exceed 2.5. Porcelain’s homogeneous crystalline structure offers crack-propagation resistance absent in filament-wound composites.

Medium-voltage strings dominate volume but face margin compression as polymers capture pole-top replacements in suburban feeders. Nevertheless, United States data-center buildouts and grid-hardening funds drive a 10.5 % CAGR for medium-voltage switchgear, sustaining porcelain bushings and post units. Low-voltage demand is steady yet commoditized; growth prospects hinge on renovation subsidies in Europe’s building stock.

By Installation Environment: Overhead Applications Maintain Structural Advantage

Overhead lines secured 62.5 % of 2024 revenue, reflecting porcelain’s resistance to UV degradation and its ability to carry 4-tonne conductor loads without creep. Utilities renew conductor bundles with higher amperage aluminum-steel composite cores, necessitating heavier insulators that polymers cannot match mechanically.

Substation applications, rising at a 7.4 % CAGR, pivot on space-saving designs and seismic-rated pedestals. Post insulators using porcelain-glass hybrids meet IEEE C57.19.00 criteria for transformer bushings, underpinning adoption in North American and European retrofit projects. Transit rolling-stock demand, though niche, captures downstream value due to certifications and after-sales maintenance contracts linked to rail operators’ thirty-year asset schedules.

By End User: Utilities Drive Infrastructure Investment Cycles

Utilities accounted for 69.1 % of 2024 spending, validating a procurement culture that values total lifecycle cost over first-price bids. Asset-management models run 45-year depreciation curves; porcelain’s proven mean-time-to-failure outweighs light-weight polymers in critical nodes. NGK’s 2023 revenue uplift to JPY 578.9 billion stemmed largely from U.S. and Australian utility orders for high-voltage strings.

From metals smelters to semiconductor fabs, industrial users favor standardized 15-35 kV porcelain bushings that withstand corrosive atmospheres. Commercial facilities adopt porcelain posts in mission-critical substations serving airports and hospitals, while residential uptake is limited to legacy overhead suburbs. Hubbell’s 2024 report notes 65 % of its sales come from reliability-enhancing products that directly align with utility grid-resilience KPIs.

Geography Analysis

Asia-Pacific’s 49.0 % share underscores the structural weight of Chinese, Indian, and ASEAN grid projects. The State Grid UHVDC corridor, completed in January 2025, spans 1,901 km and moves 40 billion kWh annually while demanding insulators rated for 4,000 kN mechanical load. Parallel Make in India rules force 50 % local-content thresholds, channeling spending to domestic clay-rich belts. Vietnamese and Indonesian rural electrification allocates sovereign bonds toward 22 kV feeders, generating high-volume orders for pin and shackle formats with simplified end fittings.

North America and Europe rely on asset-replacement cycles. The United States DOE’s Grid Resilience and Innovation Partnership (GRIP) program released USD 3.5 billion in grants, unlocking orders for 69-230 kV porcelain posts that retrofit into existing steel poles. Europe’s Ten-Year Network Development Plan (TYNDP) allocates EUR 300 billion to cross-border interconnectors, and standards bodies emphasize SF6-free apparatus, thereby reinforcing demand for porcelain bushings that perform under alternative gases.

Emerging regions—South America, the Middle East, and Africa—absorb around 14 % of global spend yet exhibit double-digit growth as interconnection projects tap resource deserts for solar exports. The East Africa Power Pool’s 400 kV Ethiopia-Kenya line and Brazil’s Belo Monte HVDC scheme highlight how multilateral lenders fund infrastructure that specifies ceramic hardware due to long-term reliability records. Supply-chain localization remains a barrier; thus, multinational producers cooperate with state-owned ceramics firms to meet local-value mandates and offset import duties.

Competitive Landscape

The porcelain insulators market presents moderate fragmentation: the top five suppliers account for roughly 38 % of global revenue, while regional specialists dominate domestic tenders. NGK leverages kiln technology and raw-material integration to maintain margins amid alumina volatility. It reported FY 2023 sales of JPY 578.9 billion, buoyed by U.S. and Australian grid programs.

Asian incumbents exploit scale and proximity to kaolin basins. Liling Huaxin Ceramics expanded output 12 % in 2024 after adding tunnel kilns with 25 % lower gas intensity, reinforcing cost leadership in 11-66 kV ranges. Western OEMs counter via technology: Hubbell’s hydrophobic coatings reduce washing intervals by 50 % in coastal substations, securing premium contracts despite higher unit prices.

Strategic plays coalesce around three axes. First, vertical integration: players such as PPC Insulators invest in alumina refineries to stabilize input costs. Second, horizontal M&A: TE Connectivity’s 2024 acquisition of a Czech bushing maker broadens voltage portfolios. Third, R&D differentiation: manufacturers collaborate with universities to tailor nano-frits that cut leakage currents under salt fog. The fragmentation invites consolidation pressure on mid-tier firms lacking a local-content advantage or technology depth.

Porcelain Insulators Industry Leaders

Seves Group

NGK Insulators Ltd.

MacLean Power Systems

PPC Insulators

Aditya Birla Insulators Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Hitachi Energy committed an additional USD 250 million to scale transformer-component and insulation capacity, addressing a global shortage and boosting porcelain demand for 145-800 kV bushings.

- January 2025: China energized the world’s highest UHVDC project, a 1,901 km link delivering 40 billion kWh annually, equipped with custom porcelain strings rated for 4,000 kN.

- September 2024: Hitachi Energy injected USD 155 million into North American factories in Reynosa, South Boston, and Mount Pleasant, expanding high-voltage switchgear and insulator lines.

- July 2024: State Grid Corporation announced 600 billion yuan 2024 transmission capex, a 60 % hike centered on UHV corridors that specify porcelain units for 800 kV AC service.

- July 2024: .India’s DPIIT revised procurement policy, reclassifying Production Linked Incentive products under Class II unless 50 % local content is met, steering porcelain contracts to domestic plants

Global Porcelain Insulators Market Report Scope

| Pin |

| Suspension |

| Strain |

| Shackle |

| Low (Below 1 kV) |

| Medium (1 to 69 kV) |

| High (Above 69 kV) |

| Overhead |

| Substation |

| Transit and Rolling Stock |

| Utilities |

| Industrial |

| Commercial |

| Residential |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Product Type | Pin | |

| Suspension | ||

| Strain | ||

| Shackle | ||

| By Voltage Rating | Low (Below 1 kV) | |

| Medium (1 to 69 kV) | ||

| High (Above 69 kV) | ||

| By Installation Environment | Overhead | |

| Substation | ||

| Transit and Rolling Stock | ||

| By End User | Utilities | |

| Industrial | ||

| Commercial | ||

| Residential | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What CAGR is projected for porcelain insulators between 2025 and 2030?

The market is forecast to grow at a 6.36% CAGR over the 2025-2030 period.

Which region contributes the largest revenue?

Asia-Pacific generated 49.0% of 2024 sales and is the fastest-growing region at 6.9% CAGR.

Why do utilities still prefer porcelain over polymer designs?

Utilities value porcelain’s proven 40-year service life and compatibility with existing hardware, reducing total ownership cost despite higher initial price.

Which product type shows the fastest growth?

Strain insulators post the highest 7.8% CAGR, driven by rail-traction and renewable interconnection projects.

How are local-content rules shaping sourcing decisions?

Policies in India and Brazil mandate 50 % domestic content, compelling multinationals to establish joint ventures or local plants to access tenders.

What is the main restraint for porcelain demand?

Rapid adoption of lighter composite units in seismic and offshore applications trims the CAGR by an estimated 1.4 percentage points.

Page last updated on: