Poland Out Of Home Delivery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.26 Billion |

| Market Size (2026) | USD 1.31 Billion |

| Market Size (2031) | USD 1.57 Billion |

| Growth Rate (2026 - 2031) | 3.78% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Poland Out Of Home Delivery Market Analysis by Mordor Intelligence

The Poland out-of-home (OOH) delivery market size was valued at USD 1.26 billion in 2025 and is estimated to grow from USD 1.31 billion in 2026 to USD 1.57 billion by 2031, registering a CAGR of 3.78% over the same period.

The market is undergoing a structural reset in last-mile delivery, as automated parcel machines and staffed pickup or drop-off points have already displaced home delivery as the default fulfillment option for a large share of Polish online consumers. That shift is now reinforcing carrier investment decisions, platform pricing strategy, and network design across the Poland OOH delivery market, with operators focusing less on proving adoption and more on improving utilization, service breadth, and route economics. The competitive setup is also changing at the ownership level, as a consortium led by FedEx Corporation and Advent International launched a recommended all-cash offer for InPost S.A. in May 2026[1]InPost S.A., “IS Iris Lux Bidco Launches All-Cash Offer for InPost Shares,” InPost, inpost.eu. The transaction matters because it would place the country’s largest APM network within a global express logistics system, while Allegro, ORLEN Paczka, DPD Polska, DHL Parcel Polska, and convenience-led PUDO operators are all trying to defend relevance through scale, access, or technology.

Key Report Takeaways

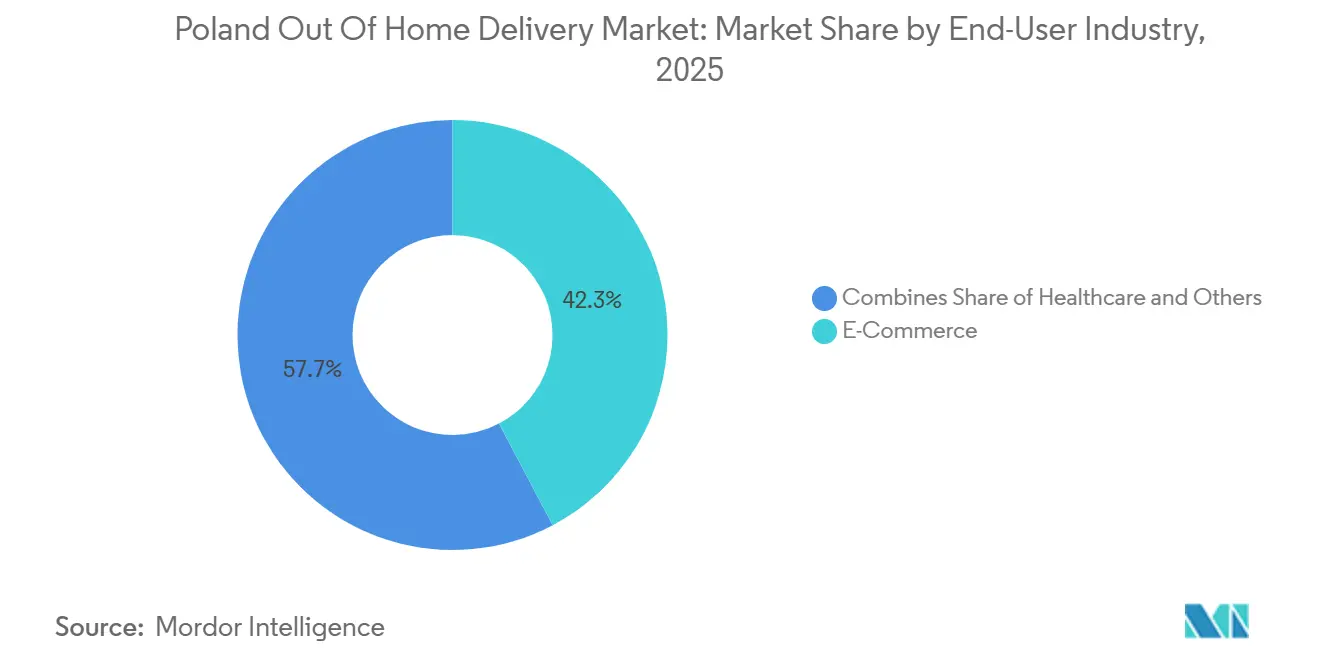

- By end-user industry, e-commerce accounted for 42.29% of the Polish OOH delivery market size in 2025 and is expected to record the highest growth at a 4.32% CAGR through 2031.

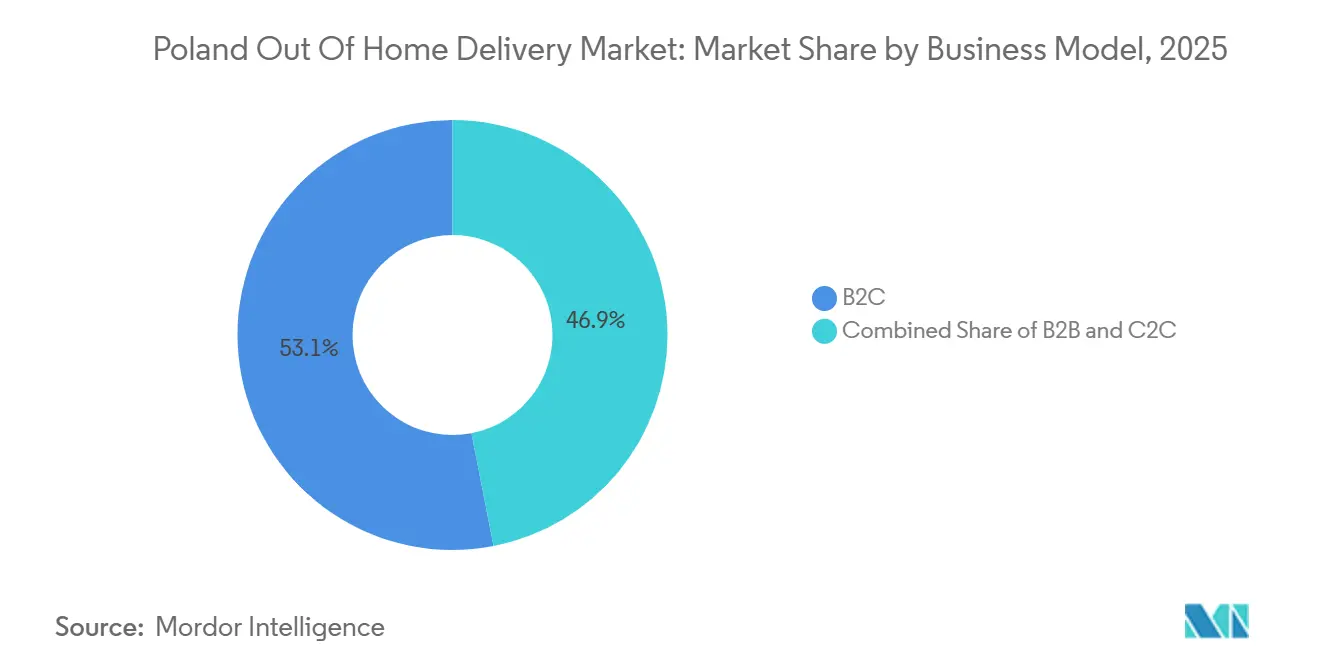

- By business model, B2C accounted for 53.06% of the Polish OOH delivery market share in 2025 and is expected to record the highest growth at a 4.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Poland Out Of Home Delivery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyper-Adoption of Automated Parcel Machines by Polish Consumers | +1.5% | National, with peak density in Warsaw, Kraków, Wrocław, and Łódź | Short term (≤ 2 years) |

| E-commerce Platform Rivalries Subsidizing OOH Delivery | +1.2% | National, strongest in metro and mid-tier cities | Medium term (2-4 years) |

| High Density of PUDO Networks in Convenience Retail | +0.9% | National, with stronger effect in suburban and semi-rural areas | Medium term (2-4 years) |

| Carrier Cost Reduction and Route Optimization in Urban Hubs | +0.7% | Urban cores including Warsaw, Kraków, Trójmiasto, and Wrocław | Short term (≤ 2 years) |

| Eco-Friendly Consumer Shift Toward Consolidated Drop-Off | +0.5% | National, strongest in large urban centers | Long term (≥ 4 years) |

| Cross-Border E-commerce Expansion into CEE Markets | +0.8% | National, especially corridors linked to Czech Republic, Slovakia, Hungary, and Romania | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hyper-Adoption Of Automated Parcel Machines By Polish Consumers

InPost stated that 87% of its Polish users chose Paczkomat as their preferred delivery method in 2025, which shows that the Poland OOH delivery market is now being shaped by habit rather than by one-time discounts or trial offers. This matters because growth after 2026 is less dependent on adding machines at the same pace and more dependent on improving how each installed unit is used across the day and across parcel types. The next wave is centered on AI-based slot allocation, residential building integration, and broader platform interoperability, all of which expand effective throughput without demanding the same amount of new street-level real estate. That shift changes the commercial logic of the Poland OOH delivery market, as monetization can come from premium convenience, subscription layers, and merchant data services rather than relying solely on rising parcel counts. It also makes established operators harder to displace, since consumers who already organize deliveries around nearby lockers have little reason to switch back to less predictable home-drop models.

E-Commerce Platform Rivalries Subsidizing OOH Delivery

Competition in the Poland OOH delivery market is being pushed by marketplace logistics programs that lower the consumer and merchant cost of OOH fulfillment without relying on direct carrier price wars alone. Allegro Delivery combines several carrier networks under one logistics umbrella, allowing platform economics to absorb part of the delivery cost and keeping APM-based fulfillment attractive even when smaller carriers cannot match the per-parcel rate on their own. Allegro’s One Box network passed 8,500 machines in Poland by the end of 2025, and the company is installing another 3,500 to 4,000 units in 2026, including off-grid models that can be placed where a standard electrical connection is a barrier[2]Allegro.eu, “Allegro Delivery Zwiększy Tempo Rozwoju Dzięki Nowej Generacji One Boxów,” Allegro Media, media.allegro.pl. Each new installation in a high-traffic residential zone forces nearby operators to protect their fill rates, collection speed, and merchant relationships, because the risk is no longer limited to parcel loss and now includes ecosystem migration. The result is a capacity race in which infrastructure is often added before demand fully catches up, keeping the Poland OOH delivery market on a build-first path rather than a wait-for-volume one. Over time, that rivalry is likely to favor operators that can pair physical reach with software tools that improve slot turnover, returns handling, and consumer retention within a single app environment.

High Density Of PUDO Networks In Convenience Retail

Convenience retail has become one of the most efficient access layers in the Poland OOH delivery market, because carriers can leverage existing footfall, staffing, and leased space rather than bear those fixed costs themselves. Żabka’s network of more than 8,400 stores serves 15.5 million consumers within 500 meters and handles close to 3 million daily visits, which makes it a ready-made PUDO substrate with national reach and strong local familiarity. FedEx formalized its partnership with Żabka in January 2026, adding more than 12,000 new service points and lifting its Polish network to more than 16,000 locations, instantly changing its position in domestic consumer and returns traffic[3]FedEx Corporation, “FedEx and Żabka Offer Convenient Package Drop-off and Pickup Solutions,” FedEx Newsroom Europe, newsroom.fedex.com. This model matters because PUDO access in convenience stores reduces the siting risk associated with dense urban locker build-outs and provides suburban and semi-rural zones with a practical collection option without waiting for every carrier to install its own machine. Returns are especially important here because consumers can combine multiple drop-offs into a single store visit, strengthening the retail host's bargaining position and raising the strategic value of open-access networks.

Cross-Border E-Commerce Expansion Into CEE Markets

Cross-border demand is widening the addressable base of the Poland OOH delivery market, because foreign merchants entering Poland often prefer a last-mile model that reduces failed deliveries and simplifies returns. The share of Polish consumers shopping internationally online rose from 15% in 2024 to 39% in 2025, and cross-border e-commerce accounted for 18% to 20% of the country’s online retail market in the same period[4]Ecommerce Europe, “Growth of Polish E-commerce Driven by Omnichannel, Mobile, and Cross-Border Shopping,” Ecommerce Europe, ecommerce-europe.eu. That increase supports carriers with established APM and PUDO infrastructure, since lockers and collection points let overseas sellers offer a predictable local handoff model without replicating full domestic courier density from the start. Packeta Poland’s cooperation with ORLEN Paczka in 2025 enabled Polish e-stores to use lockers as first-mile collection points for shipments moving into nearby Central and Eastern European markets, thereby shortening the operational gap between domestic dispatch and regional fulfillment. The corridor effect also supports specialized operators serving bilateral flows, especially where language, migrant communities, and repeat consignment needs make a standard parcel service less effective than a tailored cross-border network.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| APM Saturation in Tier-1 and Tier-2 Cities | -0.8% | Warsaw, Kraków, Wrocław, Łódź, Gdańsk, and Poznań | Short term (≤ 2 years) |

| Municipal Aesthetic Regulations and Residential Resistance | -0.5% | Urban residential districts, especially Tier-1 cities | Medium term (2-4 years) |

| Grid Connection Constraints for High-Density Smart Lockers | -0.4% | Suburban growth corridors and secondary cities | Medium term (2-4 years) |

| Rural Viability and Infrastructure Gaps | -0.9% | Gminas with fewer than 10,000 inhabitants, especially in eastern and northeastern Poland | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

APM Saturation In Tier-1 And Tier-2 Cities

The largest cities still drive parcel volumes, but they also show where the Poland OOH delivery market is reaching practical limits on how many proprietary machines can be added to the same neighborhoods. InPost already operates more than 28,000 APMs in Poland, while DPD Polska ended 2025 with 9,000 parcel lockers, and Allegro’s One Box network moved beyond 8,500 units, which means several scaled operators are now competing for many of the same urban catchments. In this setting, an additional installation no longer guarantees the same economic return as it did during the earlier roll-out phase, because the next machine is often placed near an existing one rather than serving a truly uncovered zone. That is why carriers are shifting their attention to utilization, slot management, and shared-access models that extend the value of existing infrastructure rather than repeating capital-intensive expansion in saturated districts. ORLEN Paczka’s open-access approach illustrates the direction of travel, as multi-carrier use can keep an asset productive even when standalone ownership would no longer justify a new placement.

Rural Viability And Infrastructure Gaps

The Poland OOH delivery market remains uneven outside major urban clusters, because low density and weaker infrastructure make standard APM economics harder to sustain. A 2025 study of the Poznań agglomeration found that 3.8% of residents had no viable OOH access even by bicycle, while rural areas were served by close to 6 APMs per 10,000 inhabitants versus 14 in core urban zones. Those figures show that network presence is not the same as practical accessibility, especially in peripheral communities where longer travel distances reduce the time and cost advantage of locker pickup. Allegro’s off-grid One Box format helps address the electricity barrier in newer or less fully served areas, but it does not remove the underlying issue that sparse demand weakens the return on each installed point. Poczta Polska’s universal presence helps preserve a baseline of postal access, yet commercial OOH choice is still materially thinner in many rural areas than in the country’s main city clusters. This gap limits how evenly the Poland OOH delivery market can scale, and it keeps rural expansion tied to partnership models and hybrid access formats rather than to pure APM roll-out.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: E-Commerce Anchors the OOH Delivery Value Chain

E-commerce held 42.29% of the Poland OOH delivery market share in 2025 and is projected to expand at a 4.32% CAGR through 2031, which made it the largest end-user category and the clearest signal for where new capacity, software upgrades, and service experiments are most likely to be directed. This lead is important because the largest category in the Poland OOH delivery industry is also the one that most directly influences where carriers place lockers, how platforms negotiate rates, and which service windows consumers come to expect. Allegro’s same-day One Box delivery pilot in Warsaw, Kraków, and Poznań during 2025 narrowed the convenience gap between home delivery and OOH collection, which strengthens the case for even more e-commerce volume to move through locker-based routes. The category also gained a new layer of utility in December 2025, when Allegro launched a consumer-to-consumer shipping service through the One Box network without requiring a marketplace transaction or a printed label. That development matters because it extends usage beyond formal online retail while still relying on the same physical network, which keeps e-commerce-linked infrastructure productive across more parcel journeys.

Within the Poland OOH delivery industry, BFSI uses the network mainly for document, card, and secure parcel delivery, where handoff control and identity assurance matter more than raw volume. Healthcare is also becoming more relevant, because temperature-adapted PUDO points are increasingly suited to direct-to-patient pharmaceutical fulfillment and other regulated deliveries that benefit from controlled collection timing. Manufacturing and wholesale or retail trade generate lower volumes, yet their use case is still meaningful in spare parts movement and replenishment cycles where APM pickup can ease loading-dock pressure in industrial zones. The primary sector remains a smaller contributor, largely because rural access gaps still limit network convenience where agricultural consumables and related deliveries would otherwise fit a collection model. Across these smaller verticals, compliance needs tied to secure consignment, data handling, and software-level traceability favor operators with stronger IT infrastructure, which raises the service threshold for smaller OOH providers that want to move into higher-value segments.

By Business Model: B2C Volumes Set the Growth Cadence

The B2C segment held a 53.06% of the Poland OOH delivery market size in 2025 and is projected to grow at a 4.98% CAGR from 2026 to 2031. It is expanding fastest because it sits atop online retail growth, cross-border inflows, and a deeply established locker collection habit. In 2025, parcel machines were the preferred delivery option for most Polish online shoppers, keeping the B2C model structurally stronger in Poland than in many Western European markets, where OOH penetration remains much lower. That preference creates a self-reinforcing cycle, because denser APM networks make pickup easier, higher usage improves utilization data, and better data lowers the unit cost of each delivered parcel. Once that cycle is established, large operators gain a defensive edge through software and consumer familiarity as much as through physical scale. InPost’s Paczkomat+ proposition adds another layer to that model by tying usage to a subscription and app environment rather than to stand-alone parcel events, which could deepen B2C loyalty as the company's ownership structure changes.

B2B remains relevant in manufacturing, wholesale, and selected service verticals. Still, its structural share is lower because shipment weights, irregular dimensions, and time-sensitive collection needs are less naturally aligned with standard locker compartment design. Sensitive B2B flows in healthcare and financial services often lean toward staffed PUDO points rather than APMs, because documentation requirements and identity checks are easier to handle in a person-assisted environment. C2C is still the smallest business model category, yet its runway has improved after Allegro’s off-marketplace locker shipping launch in December 2025 and Meest Post’s partnership with Poczta Polska in February 2026 for international drop-off access. Packeta Poland also improved cross-border flexibility in February 2026 by allowing merchants to choose the carrier used for Poland-bound shipments, which makes OOH fulfillment more predictable for regional sellers serving Polish demand. Together, these moves show that the Poland OOH delivery market is still led by B2C behavior, but the adjacent B2B and C2C layers are adding depth to the network and broadening the economic use case of each collection point.

Geography Analysis

Warsaw, Kraków, Wrocław, and the Trójmiasto cluster account for the majority of Poland OOH delivery market volumes, which confirms that the largest urban zones remain the operational center of gravity. Warsaw carries a particularly large share of B2C OOH flows because it combines high disposable income, dense apartment living, and daily routines that make locker pickup more practical than waiting for home delivery. The city also benefits from a sizable Ukrainian diaspora, which supports bilateral parcel demand through operators focused on Poland-Ukraine flows and related cross-border traffic. Allegro’s same-day One Box service and its C2C parcel functionality have been concentrated in the most infrastructure-rich districts, which suggests that service differentiation now matters as much as pure access count in the country’s densest micro-markets. In these locations, the Poland OOH delivery market is moving from a presence race to a convenience race, where faster handoff, better app control, and flexible returns shape competitive position.

Mid-tier cities such as Rzeszów, Białystok, Lublin, and Szczecin are absorbing more of the next growth phase as expansion opportunities in the largest metros become harder to justify at the same intensity. These cities benefit from tier-down spillover, lower site congestion, and Poland’s role as a transit bridge between Western and Eastern Europe. Allegro’s off-grid One Box machines are especially relevant in suburban districts and new residential zones where construction has moved faster than local grid readiness. That hardware change opens sites that were previously hard to serve and gives operators a practical way to extend OOH access without waiting for a standard utility connection. The same geographic pattern supports broader adoption of the Poland OOH delivery market beyond the most mature urban cores while keeping deployment economics under better control.

Cross-border influence is also rising across Poland’s regional geography. In 2025, 39% of Polish consumers shopped internationally online, up from 15% in 2024, which widened demand for APM and PUDO handoff options in both large cities and secondary corridors. GLS Group stated that its OOH volumes more than doubled in 2025 versus 2024, with Poland, Germany, and the Czech Republic all recording growth above 100%, which shows how regional network scale can lift local throughput when cross-border trade accelerates. At the same time, the Poznań accessibility study showed that peripheral and rural areas still lag urban centers, so geographic growth in the Poland OOH delivery market remains strong but uneven.

Competitive Landscape

The Poland OOH delivery market has a split competitive structure, because the APM infrastructure layer is concentrated among a limited set of scaled operators, while the broader PUDO access layer is much more open and fragmented. The leading network still benefits from a classic density advantage, since each added locker increases the chance that a consumer lives or works close enough to treat OOH pickup as the simplest option. That network effect lowers infrastructure cost per parcel over time and makes it difficult for later entrants to catch up through capital spending alone. Secondary operators are responding by leaning harder into shared-access models, retail partnerships, and open network arrangements rather than copying the same proprietary APM strategy in every location. ORLEN Paczka’s multi-carrier positioning reflects this change, as the asset can remain relevant by serving multiple brands from a single footprint rather than requiring exclusive parcel flow from a single operator.

A second competitive axis is emerging around software, user experience, and app-level control. InPost’s patented slot-management approach and AI-enabled shopping support demonstrate that the battle is no longer limited to box count, as utilization, retention, and in-app behavior now directly affect network value. Allegro is making the same point from the platform side, with features that let users manage multiple pending locker parcels in one action and with service design that blends marketplace activity, C2C sending, and OOH collection into one ecosystem. These moves matter because the Poland OOH delivery market is becoming harder to win through access alone once consumers already have several nearby collection options. As a result, white space is more visible in heavy-consignment B2B shipments and in cross-border niche corridors than in standard urban B2C locker traffic, where scale leaders already hold a strong advantage. Smaller regional players can still compete, but they are doing so through corridor coverage and partnership density rather than through a direct attempt to match the leading domestic APM footprint.

Strategic moves in 2026 reinforce this picture. The recommended FedEx and Advent offer for InPost would connect Poland’s largest APM system to a global express network if it closes, which could alter the balance between domestic scale and international reach. ORLEN’s February 2026 confirmation that its planned consolidation route with Poczta Polska had ended leaves the field more open for commercially funded competition instead of a larger state-backed OOH combination. Polenergia’s renewable power agreement for InPost’s Polish APM fleet adds a separate point of competition, because sustainability disclosure and energy sourcing are becoming more visible operating requirements for major networks. Taken together, these moves show a Poland OOH delivery market that is not fully consolidated, yet is clearly moving toward stronger advantages for operators that combine network reach, technology control, and partnership flexibility.

Poland Out Of Home Delivery Industry Leaders

InPost S.A.

DPD Polska

DHL Parcel Polska

Poczta Polska S.A.

GLS Poland

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: InPost, FedEx, Advent, A&R, and PPF moved from agreement to a formal recommended all-cash offer for all InPost S.A. shares, valuing the company at EUR 7.8 billion (USD 9.2 billion). The acceptance window runs from May 26 to July 27, 2026, and the transaction requires at least 80% shareholder acceptance before an expected second-half 2026 close.

- March 2026: Allegro launched a new off-grid generation of One Box APMs that do not require a standard electrical grid connection. The company plans to add 3,500 to 4,000 new One Box units in 2026, with this format targeted at residential developments, suburban areas, and commercial zones that were previously harder to serve.

- February 2026: ORLEN S.A. announced the joint withdrawal from the September 2025 term sheet under which Poczta Polska was expected to acquire up to 100% of ORLEN Paczka.

- January 2026: FedEx Express Polska formalized its partnership with Żabka, which added more than 12,000 new PUDO locations and lifted FedEx’s Polish service-point network to more than 16,000. The agreement gives FedEx a much stronger position in consumer parcel and returns flows than its traditional express model could deliver on its own.

Poland Out Of Home Delivery Market Report Scope

| E-Commerce |

| Financial Services (BFSI) |

| Healthcare |

| Manufacturing |

| Primary Industry |

| Wholesale and Retail Trade (Offline) |

| Others |

| Business-to-Business (B2B) |

| Business-to-Consumer (B2C) |

| Consumer-to-Consumer (C2C) |

| By End-User Industry | E-Commerce |

| Financial Services (BFSI) | |

| Healthcare | |

| Manufacturing | |

| Primary Industry | |

| Wholesale and Retail Trade (Offline) | |

| Others | |

| By Business Model | Business-to-Business (B2B) |

| Business-to-Consumer (B2C) | |

| Consumer-to-Consumer (C2C) |

Key Questions Answered in the Report

What is driving growth in Poland OOH delivery through 2031?

Growth is being driven by strong parcel locker adoption, platform-led delivery subsidies, dense convenience-based PUDO access, and rising cross-border e-commerce demand. The market is expected to move from USD 1.31 billion in 2026 to USD 1.57 billion by 2031 at a 3.78% CAGR.

Why are parcel lockers so important in Poland?

Parcel lockers are already part of routine consumer behavior in Poland. InPost said 87% of its Polish users chose Paczkomat as their preferred method in 2025, which makes OOH pickup the default option for many online orders.

Which business model is expanding fastest in this space?

B2C is the fastest-growing business model, with a projected 4.98% CAGR from 2026 to 2031. Its strength comes from online retail growth, cross-border inflows, and the high acceptance of locker pickup among Polish shoppers.

Which end-user category currently leads demand?

E-commerce is the leading end-user category, with 42.29% share in 2025. This category has the strongest influence on new APM deployment, same-day pilots, and platform-linked service innovation.

What are the main limits on future expansion outside major cities?

The biggest limits are metro saturation and weaker rural economics. The Poznań agglomeration study showed that 3.8% of residents had no viable OOH access even by bicycle, and rural APM density remained well below urban levels.

How is competition changing in 2026?

Competition is shifting from pure network build-out to control over access, software, and partnerships. The proposed FedEx and Advent acquisition of InPost, Allegro’s off-grid roll-out, and FedEx’s Żabka partnership all show that scale and ecosystem control now matter more than box count alone.

Page last updated on: