Germany Out Of Home Delivery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

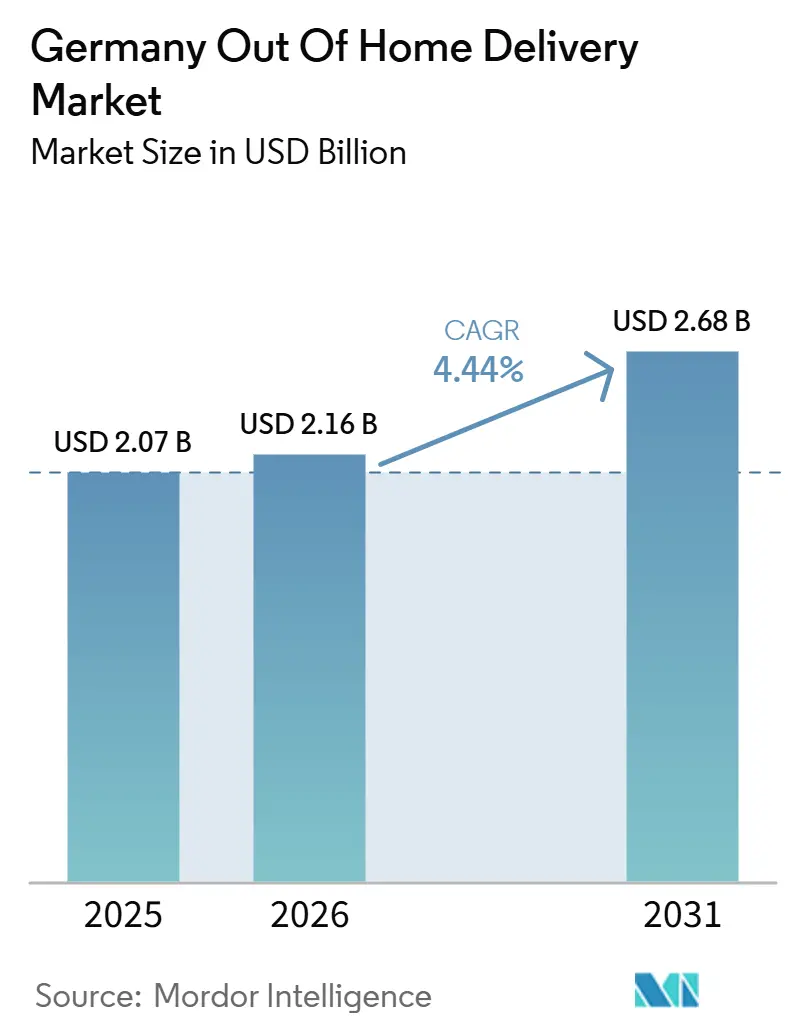

| Base Year Market Size (2025) | USD 2.07 Billion |

| Market Size (2026) | USD 2.16 Billion |

| Market Size (2031) | USD 2.68 Billion |

| Growth Rate (2026 - 2031) | 4.44% CAGR |

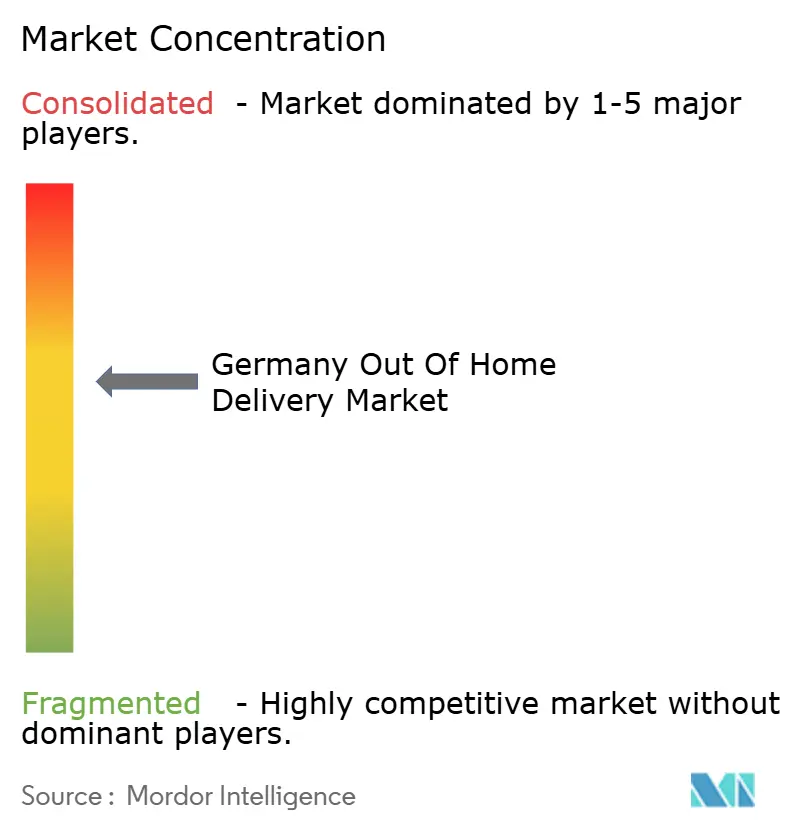

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Out Of Home Delivery Market Analysis by Mordor Intelligence

The Germany out-of-home (OOH) delivery market size was valued at USD 2.07 billion in 2025 and is estimated to grow from USD 2.16 billion in 2026 to USD 2.68 billion by 2031, registering a CAGR of 4.44% over the same period.

The Germany out-of-home (OOH) delivery market is moving forward because parcel operators are steering more volume toward self-service collection, and Germany’s collection point usage ratio rose from 9.35% in Q1 2025 to 14.10% in Q2 2025. The Germany out-of-home (OOH) delivery market also benefits from the scale of DHL’s Packstation estate, which exceeded 15,500 units in 2025 and placed 90% of residents within 10 minutes of a location. Shared infrastructure is widening the addressable opportunity, with DPD and GLS launching inboxx in 2026 and targeting 20,000 shared OOH points by the end of 2027, while myflexbox continues to expand carrier-neutral access. Labor shortages, rising wage pressure, and persistent return volumes are making consolidated drop-off and pickup models more attractive to carriers seeking to protect driver productivity and service quality. At the same time, municipal permitting friction and long-standing consumer preference for free home delivery continue to slow the pace at which Germany's out-of-home (OOH) delivery market can translate demand into dense national infrastructure.

Key Report Takeaways

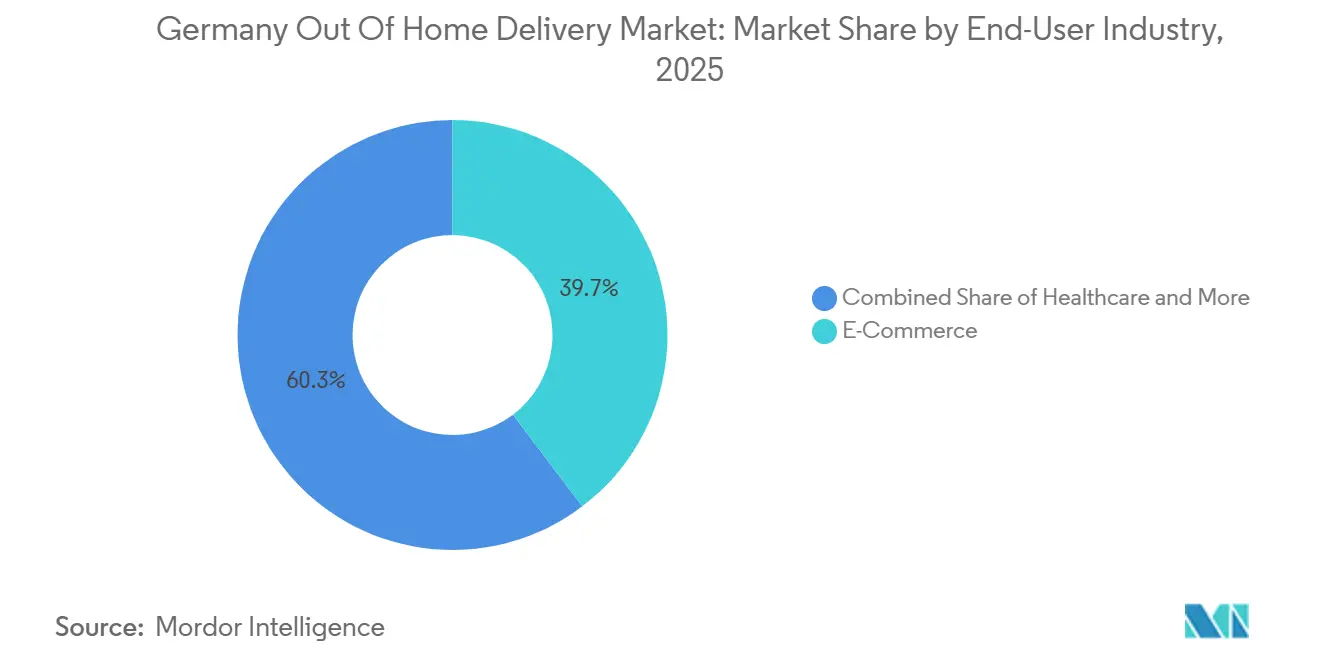

- By end-user industry, e-commerce accounted for 39.68% of the Germany out-of-home (OOH) delivery market share in 2025 and is also projected to record the fastest CAGR of 4.75% through 2031.

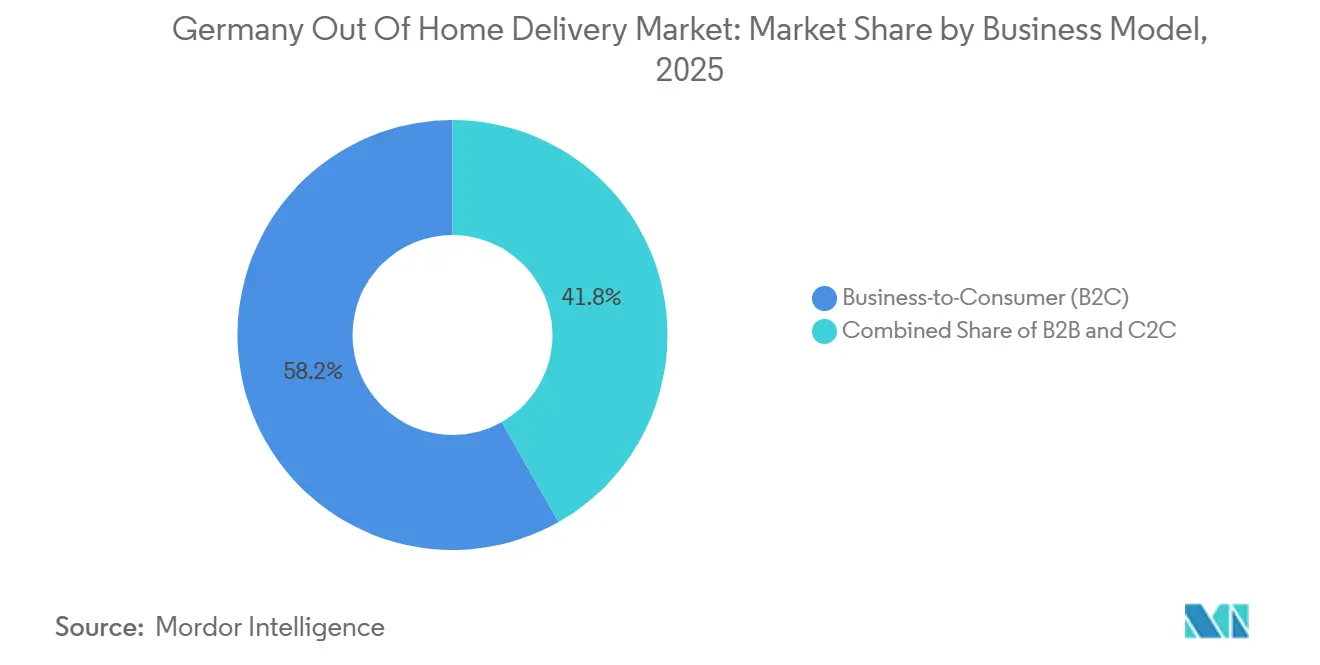

- By business model, B2C accounted for 58.21% of the Germany out-of-home (OOH) delivery market size in 2025, while C2C is projected to post the fastest 6.14% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Out Of Home Delivery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Unrivaled Consumer Adoption of APMs Led by Early Packstation Penetration Severe Logistics | +1.2% | National, with highest density in Munich, Berlin, Hamburg, Frankfurt Rhine-Main | Long term (≥ 4 years) |

| Labor Shortages (Fachkräftemangel) Forcing Carrier Consolidation | +0.6% | National, acute in Rhine-Ruhr conurbation and Greater Berlin | Medium term (2-4 years) |

| Exceptionally High Apparel Return Rates Favoring Frictionless PUDO Drop-Offs | +0.4% | National, with higher intensity in cities with large fashion e-commerce hubs | Short term (≤ 2 years) |

| Expansion of Carrier-Agnostic and Shared Open Locker Networks | +0.8% | National, concentrated rollout in North Rhine-Westphalia, Baden-Württemberg, Bavaria | Medium term (2-4 years) |

| Strict Environmental Zones (Umweltzonen) in Urban Centers Favoring OOH Hubs | +0.3% | Major city centers, including Munich, Berlin, Cologne, Düsseldorf, Frankfurt | Medium term (2-4 years) |

| B2B and Night-Time Express Lockbox Growth for Technical Services | +0.2% | National, concentrated in automotive and industrial clusters, including Stuttgart, Munich, Rhine-Ruhr | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Unrivaled Consumer Adoption of APMs Led by Early Packstation Penetration Severe Logistics

The German out-of-home (OOH) delivery market retains a structural advantage from the early normalization of parcel lockers in daily consumer routines. DHL reported that its Packstation network exceeded 15,500 units in 2025, and that footprint placed 90% of German residents within 10 minutes of a unit[1]DHL Group, “Post & Parcel Germany Division Overview,” DHL Group, group.dhl.com. That level of proximity matters because repeated exposure makes lockers a default collection option rather than an occasional fallback in dense urban and suburban areas. DHL also began a registration-free Packstation pilot in July 2025, working with 20 retail partners, including CEWE, to reduce the remaining barrier for first-time users. The pilot broadens access for shoppers who had not enrolled in DHL’s system, thereby expanding the user base without waiting for a major hardware change. As that habit base grows, the German out-of-home (OOH) delivery market becomes harder for late entrants to disrupt, because consumer familiarity and nearby locations matter as much as installed locker count.

Labor Shortages (Fachkräftemangel) Forcing Carrier Consolidation

Labor scarcity is reinforcing the case for delivery consolidation across the German out-of-home (OOH) delivery market. Stepstone Group found that demand for parcel deliverers in Germany rose 815% between 2019 and 2024, while demand for warehouse logistics specialists rose 479% over the same period. Pressure is even broader in transport, with the BGL reporting a shortfall of 120,000 truck drivers and public reporting noting that 4 in 10 active drivers are nearing retirement[2]Tagesschau, “Logistikbranche: 120.000 Lkw-Fahrer Fehlen,” Tagesschau, tagesschau.de. Wage pressure is also moving in the same direction, with the statutory minimum wage for CEP workers rising from EUR 9.50 (USD 11.17) per hour in 2021 to EUR 12.82 (USD 15.08) per hour in 2025, while political discussion has centered on EUR 15 (USD 17.64) per hour. When labor is constrained and wages are rising, each locker bank and each efficient PUDO stop helps carriers protect route density and reduce repeated door-to-door handling. That is why the German out-of-home (OOH) delivery market is not only a convenience story, because it is also a workforce productivity response to persistent delivery labor scarcity.

Exceptionally High Apparel Return Rates Favoring Frictionless PUDO Drop-Offs

Return logistics continue to support the German out-of-home (OOH) delivery market, especially where fashion volumes dominate e-commerce order flow. In 2025, 550 million return parcels were reported in Germany, up from 530 million in 2024, keeping reverse logistics under constant pressure[3]Forschungsgruppe Retourenmanagement, “Neuer Rekord – 2025 Voraussichtlich 550 Millionen Retourenpakete in Deutschland,” Forschungsgruppe Retourenmanagement, retourenforschung.de. The fashion channel remains central to this pattern because multi-size and multi-color ordering still leads to a predictable drop-off in activity after delivery. Self-service PUDO returns remove the need for courier pickup scheduling, shorten handover time for consumers, and allow carriers to pool reverse flows with forward parcel movements at the same network nodes. That operating model is especially valuable when consumers want flexibility, but carriers need a lower-cost collection process that fits routine store visits and neighborhood travel patterns. For the German out-of-home (OOH) delivery market, sustained return intensity means locker and PUDO infrastructure is becoming a durable part of retail logistics rather than a short-term add-on.

Expansion of Carrier-Agnostic and Shared Open Locker Networks

The German out-of-home (OOH) delivery market is entering a new phase in which shared infrastructure is eroding the advantage once held by closed, proprietary networks. DPD Deutschland GmbH and GLS Germany GmbH formally launched inboxx in March 2026 as an open, jointly branded parcel locker network, and the companies set a target of 20,000 shared OOH points, including up to 6,000 lockers, by the end of 2027[4]GLS Group, “GLS and DPD Launch inboxx as Their Shared Open Parcel Locker Brand,” GLS Group, gls-group.eu. In the same month, myflexbox expanded its cooperation with DPD through a long-term fixed-compartment rental agreement, deepening access to carrier-neutral lockers in German locations. This model lowers entry barriers for carriers that cannot justify a national proprietary locker rollout on their own balance sheets. It also widens the use case beyond standard parcel collection, as returns, B2B spare parts flows, and overnight technical service deliveries can fit more easily into open networks. As these networks spread, the German out-of-home (OOH) delivery market is shifting its competition toward software integration, consumer interface quality, and partner access rather than pure ownership of steel hardware.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Municipal Permitting (Sondernutzungserlaubnis) for Street-Level APMs | -0.7% | National, acute in Munich, Berlin, Hamburg | Medium term (2-4 years) |

| Deeply Entrenched Historical Expectation of Free Home Delivery | -0.5% | National | Long term (≥ 4 years) |

| Space Constraints in High-Density Retail for Expanding PUDO Footprints | -0.3% | Urban core areas, including Munich, Berlin, Hamburg, Cologne | Medium term (2-4 years) |

| Interoperability Resistance from Dominant Incumbent Networks | -0.2% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Municipal Permitting (Sondernutzungserlaubnis) for Street-Level APMs

Permitting remains the clearest near-term brake on faster densification in the Germany out-of-home (OOH) delivery market. DHL board member Nikola Hagleitner said in 2025 that the permit process for new Packstations can be as complex as construction approval, and the company linked that burden to slower progress against an installation ambition of up to 3,000 lockers per year. The problem is not a lack of national demand; the delay stems from municipal variation in processes, documentation, public-space rules, and approval timing. BPEX argued in June 2025 that German cities need to integrate logistics planning into new district development if OOH infrastructure is to be rolled out on a more predictable schedule. That means deployment economics are affected not only by parcel demand and site quality, but also by local administrative capacity and willingness to treat lockers as essential urban logistics assets. Until those local processes become more consistent, the Germany out-of-home (OOH) delivery market will keep facing a slower conversion of investment intent into installed capacity.

Deeply Entrenched Historical Expectation of Free Home Delivery

Consumer expectations built around free home delivery continue to limit the pace of change in the Germany out-of-home (OOH) delivery market. Large e-commerce platforms have long trained shoppers to see standard residential delivery as the default, which makes OOH collection feel like a trade-off unless the checkout clearly explains its value. DHL eCommerce reported in 2025 that 41% of European consumers redirect parcels to OOH locations, yet Germany still trails markets such as Poland and France, where OOH has been framed more strongly around convenience and choice. This matters because network expansion alone does not guarantee use if the checkout path still presents home delivery as the most familiar and frictionless option. The shift depends on incentives, clearer customer communication, and broader acceptance that pickup and drop-off can fit regular shopping and commuting behavior. As long as that expectation gap remains, the Germany out-of-home (OOH) delivery market will expand steadily, but it will not unlock its full efficiency potential as quickly as infrastructure providers would prefer.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: E-Commerce Anchors Demand While Healthcare Adds Premium Growth Depth

E-commerce held 39.68% of the German out-of-home (OOH) delivery market share in 2025 and is projected to expand at a 4.75% CAGR through 2031, making it both the largest and fastest-growing end-user segment. With German e-commerce penetration at 87%, the volume story has moved beyond simply adding new online shoppers and now centers more on how efficiently parcels and returns are handled. DHL’s July 2025 registration-free Packstation pilot reflects that shift, because it is designed to capture shoppers who still default to home delivery and bring them into a locker flow without prior registration. The same logic is reinforced by the scale of reverse logistics, with return parcel volumes projected at 550 million in 2025 and creating a steady stream of drop-off interactions that support locker and PUDO usage beyond new orders alone. In practical terms, this means the German out-of-home (OOH) delivery industry is gaining most where retail logistics needs a repeatable, lower-friction consumer handover model.

Healthcare is drawing more strategic attention than its current revenue base alone would suggest in the Germany out-of-home (OOH) delivery market. The BPEX KEP Study 2025 identified healthcare as one of the few end-user groups expected to show sustained shipment volume growth in 2025 even as manufacturing and industrial activity remained weak. DHL reinforced that priority in May 2025 by expanding its Life Sciences and Healthcare campus in Florstadt to 100,000 sqm with capacity for more than 140,000 pallets of pharmaceutical and medical products. BFSI contributes more measured volumes through secure document and equipment movements, while manufacturing, primary industry, and offline wholesale and retail trade add steadier but slower-moving B2B collections that often fit shared PUDO and corporate lockbox use. Together, these smaller end-user groups do not displace e-commerce, but they deepen the Germany out-of-home (OOH) delivery market by broadening the mix of use cases and supporting higher-value service layers.

By Business Model: B2C Provides the Foundation While C2C Drives the Growth Urgency

B2C held 58.21% share in 2025, giving it the largest base within the Germany out-of-home (OOH) delivery market size by value. That position reflects the direct link between dense e-commerce parcel volumes and the cost advantages of consolidating final delivery and returns through PUDO points and lockers. As shared networks spread, B2C benefits from a wider selection of pickup options without requiring every carrier to build a proprietary national estate, which makes retail-adjacent and commute-adjacent locations more valuable. The February 2026 DPD and GLS partnership with ECE to equip up to 50 shopping center parking garages with parcel stations demonstrates how major retail properties are being turned into structured last-mile infrastructure for daily consumer use. Germany’s high return parcel volume also supports this model, as B2C shoppers often need both delivery collection and reverse drop-off within the same neighborhood network.

C2C is projected to record the fastest 6.14% CAGR through 2031, which gives it the strongest growth role inside the Germany out-of-home (OOH) delivery market. The rise of peer-to-peer resale platforms is a key reason, because casual sellers need low-friction label creation and nearby drop-off options rather than formal business shipping relationships. That makes lockers and parcel shops well suited to C2C flows, where shipments tend to be lightweight, lower value, and highly sensitive to convenience at the point of dispatch. B2B remains smaller in volume but adds value depth through time-critical flows, and myflexbox’s cooperation with Night Star Express shows how open locker networks are being used for urgent items in technical service chains. The result is a business-model mix in which B2C anchors current scale, C2C supplies the urgency of future growth, and B2B improves monetization through specialized service needs.

Geography Analysis

The Rhine-Ruhr conurbation, Greater Berlin, Greater Munich, Frankfurt Rhine-Main, and Hamburg remain the strongest demand zones because parcel density, retail co-location, and sortation proximity align more favorably there. POI Data counted 16,064 verified package locker locations across Germany in May 2026, confirming that the installed base is already meaningful at a national scale, even before the next major wave of shared-network rollout. Even so, the urban-rural divide remains clear, because major cities can support faster utilization and higher stop productivity than rural areas with weaker daily footfall. BPEX projected that OOH could account for 25% to 30% of urban deliveries by 2030, suggesting the next major adoption step will be led by metropolitan corridors rather than uniform national expansion.

The geography story is also shaped by Germany’s 16 federal states and the local rules within them. Munich updated its ninth Luftreinhalteplan in October 2025, introducing new diesel access restrictions within the Mittlerer Ring and pressuring carriers to reduce repeated van movements through more consolidated delivery models. Germany still had 35 active Umweltzonen as of late 2025, which means low-emission logistics planning remains relevant across a broad set of urban centers. Baden-Württemberg, Bavaria, and North Rhine-Westphalia continue to attract disproportionate infrastructure attention because their commercial density gives operators a stronger case for absorbing permitting effort and installation cost. That state-level variation means the Germany out-of-home (OOH) delivery market advances through clusters first, then broadens more gradually across secondary cities and lower-density districts.

Germany’s medium-term opportunity comes from how much new density is still scheduled rather than from the current network base alone. DHL has set a target of 30,000 Packstations by 2030, which indicates that the national incumbent still sees substantial room for further penetration. inboxx is targeting 20,000 shared OOH points by the end of 2027, and myflexbox continues to scale carrier-neutral access across German sites. This combination suggests that the Germany out-of-home (OOH) delivery market will become denser through a mix of incumbent expansion and open-network rollout, with the largest gains likely to emerge where permitting, footfall, and multi-carrier demand line up most clearly.

Competitive Landscape

The Germany out-of-home (OOH) delivery market remains moderately concentrated, because one national postal incumbent still controls the most visible proprietary locker brand while several international and regional challengers are building scale through shared infrastructure. DHL retains a strong installed base and a wide consumer reach through Packstation, but the competitive setting is no longer defined only by closed networks and single-operator ecosystems. The March 2026 launch of inboxx by DPD and GLS marks the most visible coordinated challenge to that structure, because it formalizes a carrier-neutral platform with national rollout ambitions rather than a limited bilateral cooperation. myflexbox is also important in this context, because its carrier-neutral model gives multiple operators access to an open locker layer without waiting for proprietary build-out. The Germany out-of-home (OOH) delivery market is therefore moving from brand-led exclusivity toward a hybrid structure in which incumbent scale and shared-network interoperability compete side by side.

Three broad strategic postures are visible across the field. One is the cost-and-consolidation approach, where carriers use OOH infrastructure to reduce the handling of repeated home deliveries and defend margins in a wage-sensitive operating environment. Another is the partnership-and-scale approach, and the February 2026 DPD and GLS agreement with ECE to equip up to 50 shopping center parking garages illustrates how location hosts are becoming part of competitive positioning. A third is the niche-vertical model, where open lockers are integrated into urgent B2B technical service flows, as shown by Night Star Express using myflexbox for urgent items. These postures can coexist, but they reward different strengths, including route economics, partner access, software orchestration, and specialization by use case.

Company actions in 2025 and 2026 show how quickly positions are being adjusted. DHL used service design as a competitive lever with its registration-free Packstation pilot, which aimed to remove onboarding friction and widen first-time user conversion. DPD and GLS used shared rollout to gain reach faster, first through inboxx and then through site partnerships that connect locker infrastructure to existing retail parking assets. On the parcel shop side, Hermes entered a period of structural change after Advent International agreed in November 2025 to sell its 25% minority stake back to Otto Group, closing a five-year partnership and signaling further repositioning around the carrier’s delivery economics. The competitive result is a Germany out-of-home (OOH) delivery market where the leading players are not standing still, because they are actively changing network access, asset strategy, and location partnerships to defend or improve their position.

Germany Out Of Home Delivery Industry Leaders

DHL Paket GmbH

Hermes Germany GmbH

DPD Deutschland GmbH

GLS Germany GmbH & Co. OHG

United Parcel Service Deutschland S.à r.l. & Co. OHG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: DPD Deutschland GmbH and GLS Germany GmbH formally launched "inboxx," their jointly branded open, carrier-neutral parcel locker network targeting 20,000 shared OOH points, including up to 6,000 lockers, by the end of 2027, representing the largest coordinated open-access OOH infrastructure commitment in Germany's parcel sector history.

- February 2026: DPD Deutschland GmbH and GLS Germany GmbH signed a partnership with ECE Marketplaces to equip up to 50 ECE-operated shopping center parking garages across Germany with carrier-agnostic parcel stations by mid-2026, marking the first time a major retail property operator has partnered with parcel services for structured last-mile OOH deployment at scale.

- November 2025: Advent International entered into an agreement to divest its 25% minority stake in Hermes Germany GmbH back to the Otto Group, concluding a five-year strategic partnership.

- May 2025: DHL Group completed the expansion of its Life Sciences & Healthcare campus in Florstadt near Frankfurt, Germany, growing the site to 100,000 sqm with capacity for over 140,000 pallets of pharmaceutical and medical products, transforming it into a European pharma logistics hub serving biopharma, specialty pharma, medical technology, and clinical research sectors.

Germany Out Of Home Delivery Market Report Scope

| E-Commerce |

| Financial Services (BFSI) |

| Healthcare |

| Manufacturing |

| Primary Industry |

| Wholesale and Retail Trade (Offline) |

| Others |

| Business-to-Business (B2B) |

| Business-to-Consumer (B2C) |

| Consumer-to-Consumer (C2C) |

| By End-User Industry | E-Commerce |

| Financial Services (BFSI) | |

| Healthcare | |

| Manufacturing | |

| Primary Industry | |

| Wholesale and Retail Trade (Offline) | |

| Others | |

| By Business Model | Business-to-Business (B2B) |

| Business-to-Consumer (B2C) | |

| Consumer-to-Consumer (C2C) |

Key Questions Answered in the Report

What is the expected size of Germany out-of-home (OOH) delivery by 2031?

The Germany out-of-home (OOH) delivery market is forecast to reach USD 2.68 billion by 2031 from USD 2.16 billion in 2026, at a 4.44% CAGR over 2026-2031.

Which end-user segment leads demand in Germany?

E-commerce is the leading end-user segment, holding 39.68% share in 2025 and also posting the fastest 4.75% CAGR through 2031.

Which business model is growing fastest in Germany OOH delivery?

B2C remains the largest model with 58.21% share in 2025, while C2C is projected to grow fastest at a 6.14% CAGR through 2031.

Why are parcel lockers and PUDO points expanding in Germany?

Expansion is being supported by consumer adoption, open-network rollout, labor shortages, and high return parcel volumes, with collection point usage rising from 9.35% in Q1 2025 to 14.10% in Q2 2025.

What is slowing rollout across German cities?

The main constraint is municipal permitting for street-level lockers, which DHL described as highly complex and inconsistent across municipalities.

Which companies are shaping competitive activity in 2026?

DHL, DPD, GLS, myflexbox, and Hermes remain central to current positioning, with inboxx and ECE-based rollout standing out among the major 2026 moves.

Page last updated on: