POC Platform And Technology Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

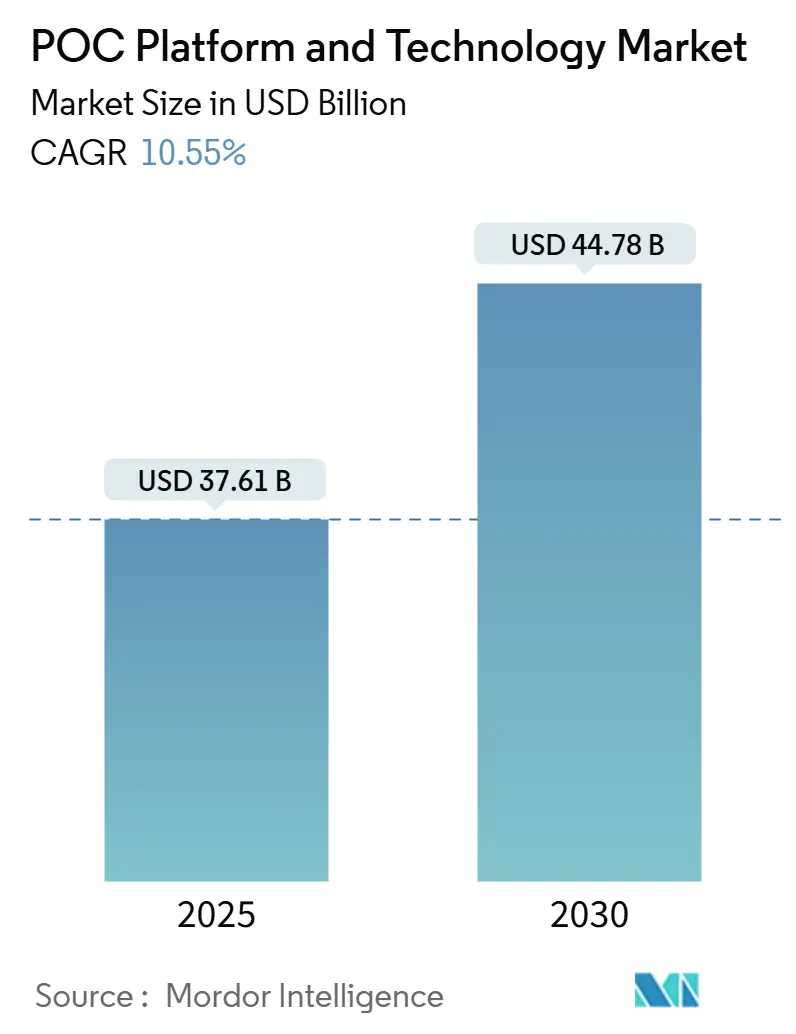

| Market Size (2025) | USD 37.61 Billion |

| Market Size (2030) | USD 44.78 Billion |

| Growth Rate (2025 - 2030) | 10.55% CAGR |

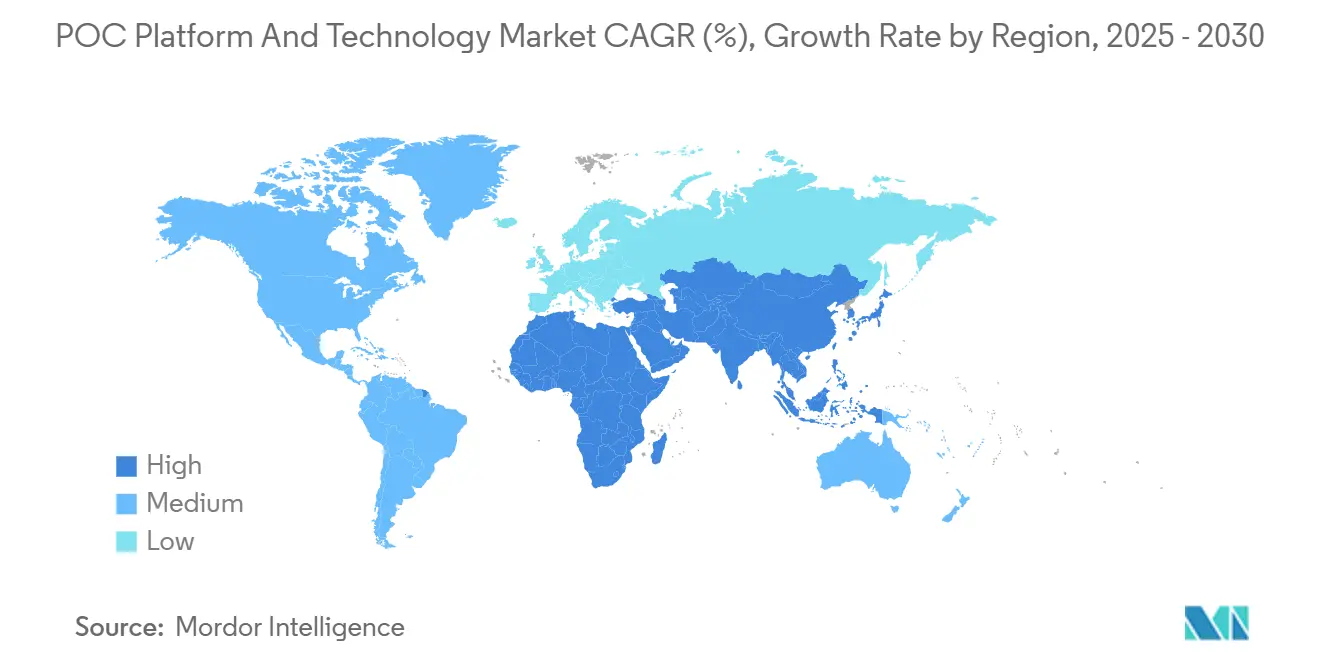

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

POC Platform And Technology Market Analysis by Mordor Intelligence

The global POC platform technology market size stands at USD 37.61 billion in 2025 and is projected to advance to USD 44.78 billion by 2030, reflecting a 10.55% CAGR. Continued miniaturization, pandemic-driven regulatory acceleration, and artificial-intelligence-enabled smartphone biosensing ecosystems underpin this growth trajectory. Heightened investments in infectious-disease surveillance, the push for decentralized chronic-disease care, and supply-chain resiliency strategies further strengthen demand. Competition centers on faster assay turnaround, cartridge affordability, and seamless cloud connectivity, while innovators leverage distributed manufacturing alliances and app-based analytics to reach under-served settings. Strategic partnerships between device majors and AI specialists create first-mover advantages in predictive clinical insights and workflow automation, positioning the POC platform technology market for sustained double-digit expansion.

Key Report Takeaways

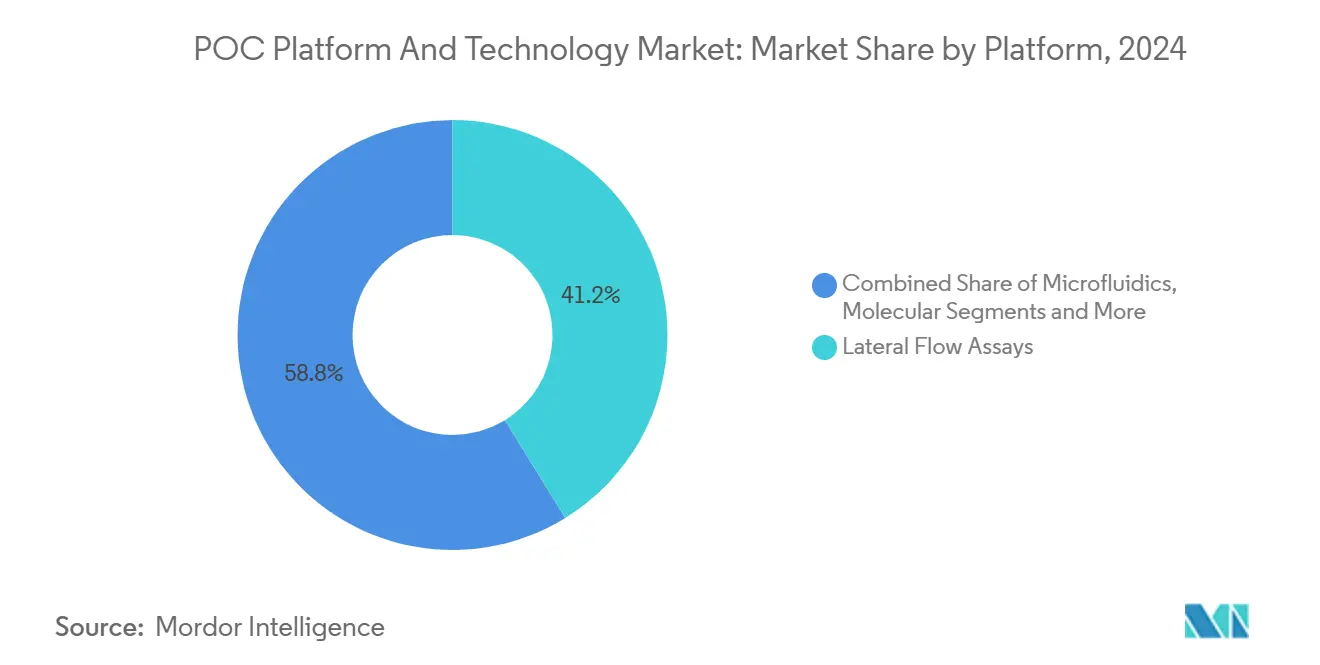

- By platform, Lateral Flow Assays led with 41.22% of POC platform technology market share in 2024; Molecular platforms are forecast to expand at a 14.36% CAGR through 2030.

- By application, Infectious Disease Testing accounted for 36.73% share of the POC platform technology market size in 2024 and is advancing at a 13.27% CAGR through 2030.

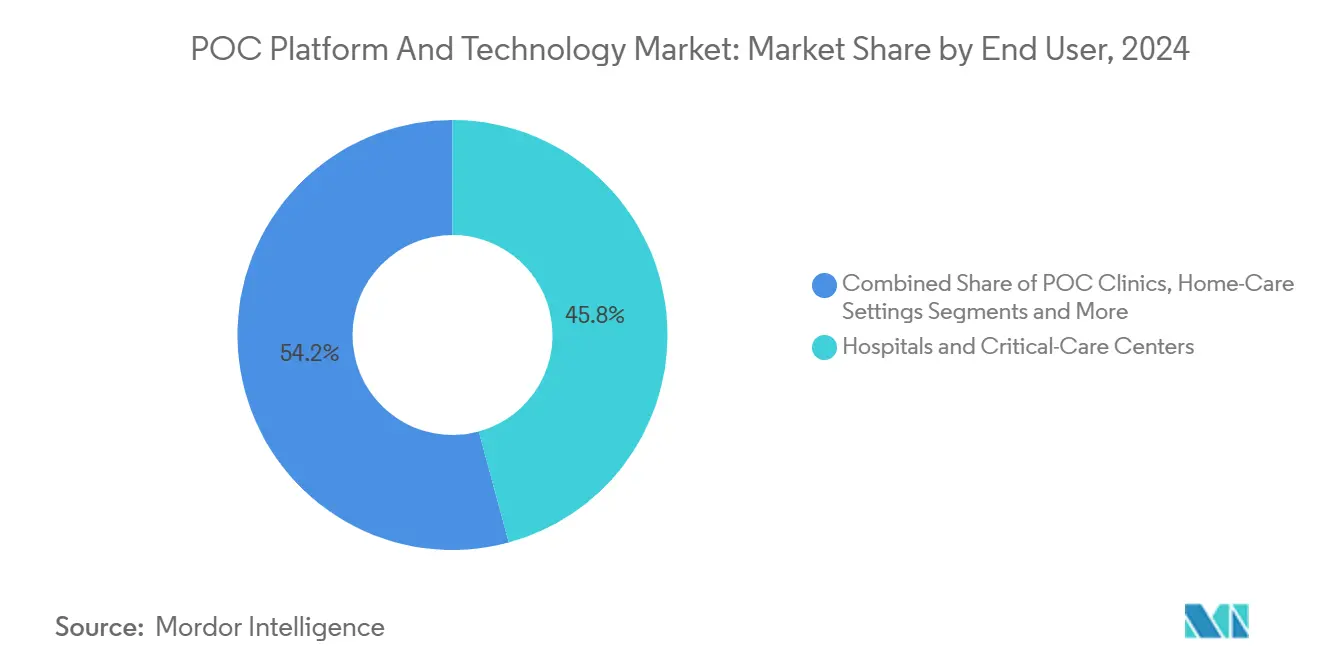

- By end-user, Hospitals & Critical-Care Centers held 45.79% of the POC platform technology market share in 2024, while Home-Care Settings record the highest projected CAGR at 12.69% through 2030.

- By mode of purchase, Prescription-Based channels dominated with 58.24% revenue share in 2024; OTC/Direct-to-Consumer sales are set to rise at a 14.79% CAGR to 2030.

- North America retained 39.68% of global revenue in 2024; Asia-Pacific is forecast to post a 12.48% CAGR, the fastest among regions.

Global POC Platform And Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Miniaturisation & Microfluidics-Driven Cost Reductions | + 2.1% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Pandemic-Accelerated Regulatory Fast-Track Pathways | + 1.8% | Global, led by FDA and EMA frameworks | Short term (≤ 2 years) |

| Shift To Home-Based Chronic-Disease Management | + 1.6% | North America & EU core, expanding to APAC | Long term (≥ 4 years) |

| Decentralized Cartridge-Manufacturing Partnerships | + 1.4% | Global supply chain optimization | Medium term (2-4 years) |

| Convergence With Smartphone Biosensing Ecosystems | + 1.2% | APAC leadership, global adoption | Short term (≤ 2 years) |

| AI-Enabled Multiplex Analytics For Antimicrobial Stewardship | + 0.9% | Global, with healthcare system integration focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Miniaturization & microfluidics-driven cost reductions

Shrinking channel geometries cut reagent use and sample volumes, lowering per-test expenses while preserving sensitivity. TE Connectivity’s ISO 13485-certified Denver site illustrates industrial-scale microfluidic cartridge output, featuring closed-loop inspection that keeps defect rates below 1%. Smartphone-linked immunosensing systems now match ELISA accuracy for cancer biomarkers at a fraction of cost, and roll-to-roll nanoimprint lines boost lateral-flow throughput to millions of strips per day. These advances democratize access, especially in resource-constrained clinics where capital budgets are limited.

Pandemic-accelerated regulatory fast-track pathways

The FDA’s Commissioner’s National Priority Voucher program compresses standard review cycles from ten months to as little as eight weeks, institutionalizing emergency-era speed.[1]Food and Drug Administration, “FDA to Issue New Commissioner’s National Priority Vouchers,” U.S. Food and Drug Administration, fda.gov Draft guidance on immediate public-health response allows validated devices to reach field use before formal 510(k) clearance when a Section 564 declaration is absent. Similarly, China’s 24-measure reform sets 45-day lot-release clocks for seasonal flu vaccines, signaling long-term political will to expedite innovative POC approvals. Firms able to navigate these channels secure earlier revenue capture and competitive lead.

Shift to home-based chronic-disease management

Cardinal Health projects robust uptake of self-testing as patients seek convenient monitoring of diabetes, cardiac risk, and infectious threats. Abbott data show HIV initiation times shorten by 130 days when POC devices guide therapy start compared with centralized labs. Roche’s CE-marked Accu-Chek SmartGuide couples predictive algorithms with continuous glucose sensors, giving prescribers early warnings of hypoglycemia events. Rising user familiarity with app-linked diagnostics cements home settings as a core care venue.

Decentralized cartridge-manufacturing partnerships

Global supply-chain shocks sparked modular clean-room deployments closer to demand centers. bioMérieux’s EUR 111 million deal for SpinChip Diagnostics integrates on-site cartridge molding with cloud-connected benchtop readers able to deliver whole-blood immunoassay results in 10 minutes. Continuous and single-use processes trim change-over time, while localizing capacity mitigates customs delays and currency fluctuations. The model supports pandemic surge manufacturing without overbuilding centralized plants.

Convergence with smartphone biosensing ecosystems

Ubiquitous cameras, LED flashes, and processors transform phones into optical spectrometers, fluorescence readers, and AI inference engines. A Nanobiotechnology study demonstrated breast-cancer BRCA-1 detection at picomolar limits using a silver-plated substrate and hairpin amplification read through a handset display.[2]Zan Yu, Wenxin Liu, and Lei Wang, “A Smartphone-Colorimetric Dual-Mode Diagnosis Method for Breast Cancer Detection of BRCA-1 Gene,” Journal of Nanobiotechnology, biomedcentral.com Bluetooth-enabled capillary electrophoresis modules extend assays to heavy-metal screening, widening the application palette. Such consumer hardware co-option slashes bill-of-materials and accelerates global reach.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Privacy Hurdles In Cloud-Connected POCT | -1.3% | Global, with GDPR and regional privacy regulations | Short term (≤ 2 years) |

| Batch-To-Batch Variability Of Lateral-Flow Reagents | -0.8% | Global manufacturing quality control | Medium term (2-4 years) |

| Reimbursement Mis-Alignment For Digital POCT Kits | -0.7% | North America & EU healthcare systems | Long term (≥ 4 years) |

| Skilled-Operator Gaps In Low-Resource Settings | -0.5% | APAC, MEA, and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-privacy hurdles in cloud-connected POCT

The FDA’s June 2025 cybersecurity guidance requires detailed software bill-of-materials tracking, penetration-test evidence, and over-the-air patch plans before clearance. Harmonizing these demands with GDPR’s right-to-erasure mandates burdens smaller manufacturers. Hospitals face rising insurance premiums tied to breach exposure, prompting lengthier procurement vetting and slowing new-device roll-outs.

Batch-to-batch variability of lateral-flow reagents

Twenty-year quality-assurance data highlight persistent sensitivity swings across lots, with only 79% pass rates in a global biomarker proficiency program.[3]Marcel Kremser, Nathalie Weiss, Anne Kaufmann-Stoeck, Laura Vierbaum, Silke Kappler, Ingo Schellenberg, Andreas Hiergeist, Volker Fingerle, Michael Baier, and Udo Reischl, “Longitudinal Analysis of 20 Years of External Quality Assurance Schemes,” Frontiers in Molecular Biosciences, frontiersin.org While roll-to-roll imprinting lifts capacity, surface-chemistry inconsistency can alter antibody binding. Added validation protocols inflate cost and time-to-market, challenging start-ups that lack in-house GMP expertise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Molecular Diagnostics Accelerate Beyond Established Immunoassays

Lateral Flow Assays delivered 41.22% of 2024 revenue, underscoring entrenched infrastructure and low consumable costs within the POC platform technology market. The FDA’s approval of the Shield blood test for colorectal cancer detection showcased molecular platforms’ leap in sensitivity, pushing the segment toward a 14.36% CAGR through 2030 as clinicians favor NAAT and CRISPR workflows for early-stage disease confirmation. The POC platform technology market size for Molecular solutions is projected to widen rapidly as decentralized oncology screening moves into primary care. Microfluidics readers piggyback on smartphone optics to offer disposable cartridges below USD 1, reinforcing price competitiveness. Biosensor-based platforms capitalize on integrated AI image processing for automated result calls, reducing human-interpretation error rates.

Technological convergence drives platform choices across economic strata. Polymedco’s Pathfast high-sensitivity cardiac troponin I assay furnishes 17-minute rule-out capability for emergency departments, accelerating throughput and cutting bed occupancy. The Dragonfly portable LAMP platform pairs power-free extraction with lyophilized reagents, sustaining 96.1% sensitivity for orthopoxvirus detection without cold-chain logistics. Dipsticks and manual immunoassay readers retain niche appeal where electricity and connectivity infrastructure remain sparse, preserving access equity.

By Application: Infectious Disease Testing Retains Dual Leadership

Infectious Disease Testing represented 36.73% of total 2024 billings and is predicted to pace the field at a 13.27% CAGR. Recurrent mpox flare-ups and looming influenza variants keep stockpiling budgets elevated. Cardiometabolic Monitoring captures lifestyle-disease momentum as continuous glucose sensors pair with predictive apps, while Oncology & Tumor Marker assays ride the molecular wave for liquid biopsy-based monitoring. Prenatal & Fertility kits reach broader audiences via privacy-centric OTC channels backed by accurate smartphone readers.

Regulators expedite novel respiratory panels for home collection, as illustrated by the Monkeypox PCR Test Home Collection Kit EUA. Toxicology screening maintains employer-driven demand, and microfluidic platelet-function tests meet cardiovascular intervention timing needs. Smartphone urinalysis apps supplant visual strip interpretation, enabling cloud-stored trend analysis.

By End-User: Home-Care Settings Catalyze the Next Adoption Curve

Hospitals & Critical-Care Centers accounted for 45.79% revenue in 2024, supported by integrated procurement and reimbursement pathways. Yet the POC platform technology market now crescendos in living rooms, where Home-Care Settings are forecast to grow 12.69% annually as patients gain confidence in guided self-testing. Professional Diagnostic Labs pivot to hybrid models, validating remote-sample workflows while offering specialized confirmatory testing. Decentralized clinics employ walk-in models to capture consumer traffic, and Assisted-Living Facilities adopt on-site panels for timely medication adjustments.

Consumer comfort with finger-stick blood collection, affirmed by BD’s MiniDraw parity study, accelerates the displacement of venipuncture. Community-health-worker pilots confirm that rapid CRP triage lowers antibiotic abuse without compromising safety, signaling broader potential across low-resource geographies.

By Mode of Purchase: OTC Expansion Democratizes Access

Prescription channels preserved 58.24% 2024 share, but OTC/Direct-to-Consumer kits headline growth at 14.79% CAGR as regulators trust lay-user competence. The First To Know Syphilis Test broke ground as the first rapid syphilis OTC assay, addressing surging U.S. incidence.

The FDA’s Digital Diagnostics initiative supports app-linked readers that log results to electronic health records, bridging consumer autonomy with clinician oversight. Payers negotiate coverage as economic models quantify avoided office visits and earlier intervention outcomes.

Geography Analysis

North America held 39.68% of 2024 billings, buoyed by high per-capita spend and mature private insurance that reimburses advanced panels. FDA leadership on cybersecurity and fast-track approvals sets tone for global harmonization. Canada and Mexico expand adoption through telehealth investments and cross-border supply agreements.

Asia-Pacific is the fastest riser at 12.48% CAGR. China’s regulatory overhaul, including 45-day vaccine batch releases, persuades multinationals to site R&D hubs locally. Japan’s precision-machining sector and South Korea’s digital-health subsidies aid technology diffusion. Indian cost-effectiveness studies find rural HbA1c POC screening delivers USD 185/QALY gains, justifying government tenders.Australia leverages international-standard convergence to import next-generation cartridges swiftly.

Europe grows steadily under single-payer purchasing power and GDPR-driven data-security supremacy, giving regional vendors an edge in privacy-sensitive deployments. Germany and France integrate AI-ready readers into hospital procurement pipelines, while the U.K. fosters home-diagnostic pilots via NHS Digital. The Middle East and Africa benefit from donor-funded infectious-disease initiatives, and South America scales through Brazil’s public-health build-out coupled with private hospital adoption in Argentina and Chile.

Competitive Landscape

The POC platform technology market remains moderately fragmented. Top-tier incumbents combine immunoassay lineage with acquisitions in molecular and AI analytics to secure end-to-end portfolios. The bioMérieux-SpinChip union melds cartridge innovation with global sales channels, promising 10-minute whole-blood panels that rival central-lab precision. BD charts a 2026 spin-off to sharpen focus on a USD 22 billion diagnostics and biosciences addressable market, signaling confidence in segment-specific growth trajectories.

New entrants center strategy on smartphone dependability and localized manufacturing. Low-CAPEX nanoimprint lines and cloud-first result dashboards grant agile players priceroom against conglomerates. Partnerships with AI algorithm houses such as Prenosis bolster sepsis-prediction differentiators within Roche’s navify suite. Regulatory mastery—510(k) dossiers and ISO 13485 frameworks—remains a barrier that entrenched firms exploit, yet venture-backed start-ups increasingly recruit seasoned quality-systems talent to bridge gaps.

POC Platform And Technology Industry Leaders

Abbott Laboratories

F. Hoffmann-La Roche Ltd

Siemens Healthineers

Danaher (Cepheid)

Becton, Dickinson and Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Royal Philips introduced the Flash Ultrasound System 5100 POC, engineered for anesthesia, emergency, and MSK imaging workflows.

- May 2025: Oracle Health, Cleveland Clinic, and G42 unveiled a joint AI-based healthcare platform aimed at nation-scale data analytics and secure care delivery.

- February 2025: Avitia launched with USD 5 million seed funding to deploy on-site AI-driven molecular cancer mutation testing for remote laboratories.

Global POC Platform And Technology Market Report Scope

| Lateral Flow Assays |

| Microfluidics |

| Molecular (NAAT, CRISPR) |

| Biosensor-Based |

| Others (Dipsticks, Immunoassay Readers) |

| Infectious Disease Testing |

| Cardiometabolic Monitoring |

| Oncology & Tumor Markers |

| Prenatal & Fertility |

| Drugs-of-Abuse & Toxicology |

| Hematology & Coagulation |

| Urinalysis |

| Hospitals & Critical-Care Centers |

| Professional Diagnostic Labs |

| Decentralised/POC Clinics |

| Home-Care Settings |

| Assisted-Living Facilities |

| Prescription-Based |

| OTC / Direct-to-Consumer |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Platform | Lateral Flow Assays | |

| Microfluidics | ||

| Molecular (NAAT, CRISPR) | ||

| Biosensor-Based | ||

| Others (Dipsticks, Immunoassay Readers) | ||

| By Application | Infectious Disease Testing | |

| Cardiometabolic Monitoring | ||

| Oncology & Tumor Markers | ||

| Prenatal & Fertility | ||

| Drugs-of-Abuse & Toxicology | ||

| Hematology & Coagulation | ||

| Urinalysis | ||

| By End-User | Hospitals & Critical-Care Centers | |

| Professional Diagnostic Labs | ||

| Decentralised/POC Clinics | ||

| Home-Care Settings | ||

| Assisted-Living Facilities | ||

| By Mode of Purchase | Prescription-Based | |

| OTC / Direct-to-Consumer | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the POC platform technology market in 2025?

The POC platform technology market size is valued at USD 37.61 billion in 2025 with a 10.55% CAGR forecast to 2030.

Which platform grows fastest through 2030?

Molecular diagnostics (NAAT and CRISPR) lead growth at a 14.36% CAGR, propelled by high sensitivity and regulatory traction.

Why is infectious-disease testing dominant?

It combines the largest 2024 revenue share at 36.73% with a 13.27% CAGR, fueled by pandemic preparedness and emerging-pathogen surveillance funding.

What drives OTC diagnostic uptake?

FDA approvals like the First To Know Syphilis Test and smartphone-guided workflows support OTC kits, giving the channel a 14.79% CAGR.

Which region offers the strongest growth potential?

Asia-Pacific posts the fastest regional CAGR at 12.48% owing to China’s regulatory reforms and expanding healthcare infrastructure.

How do AI tools improve antimicrobial stewardship?

Systems such as UTI Smart reduce antibiotic mismatches by 37.4% by combining rapid POC results with patient-specific resistance analytics.

Page last updated on: