Planar Solid Oxide Fuel Cell Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

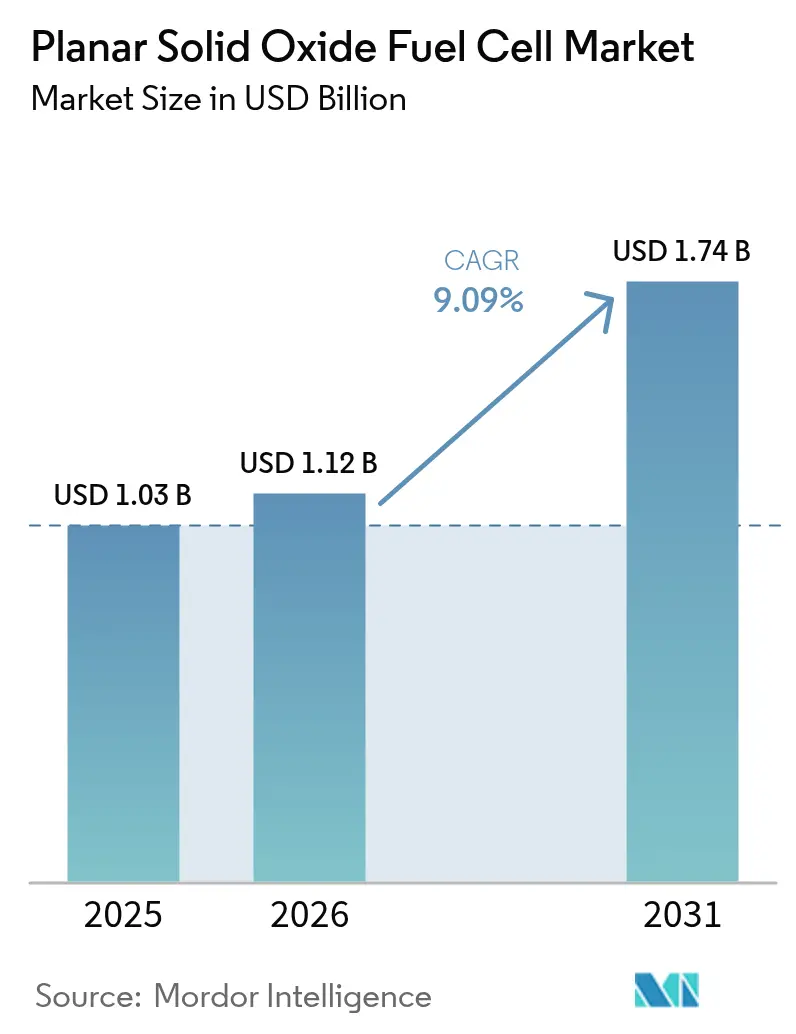

| Market Size (2026) | USD 1.12 Billion |

| Market Size (2031) | USD 1.74 Billion |

| Growth Rate (2026 - 2031) | 9.09% CAGR |

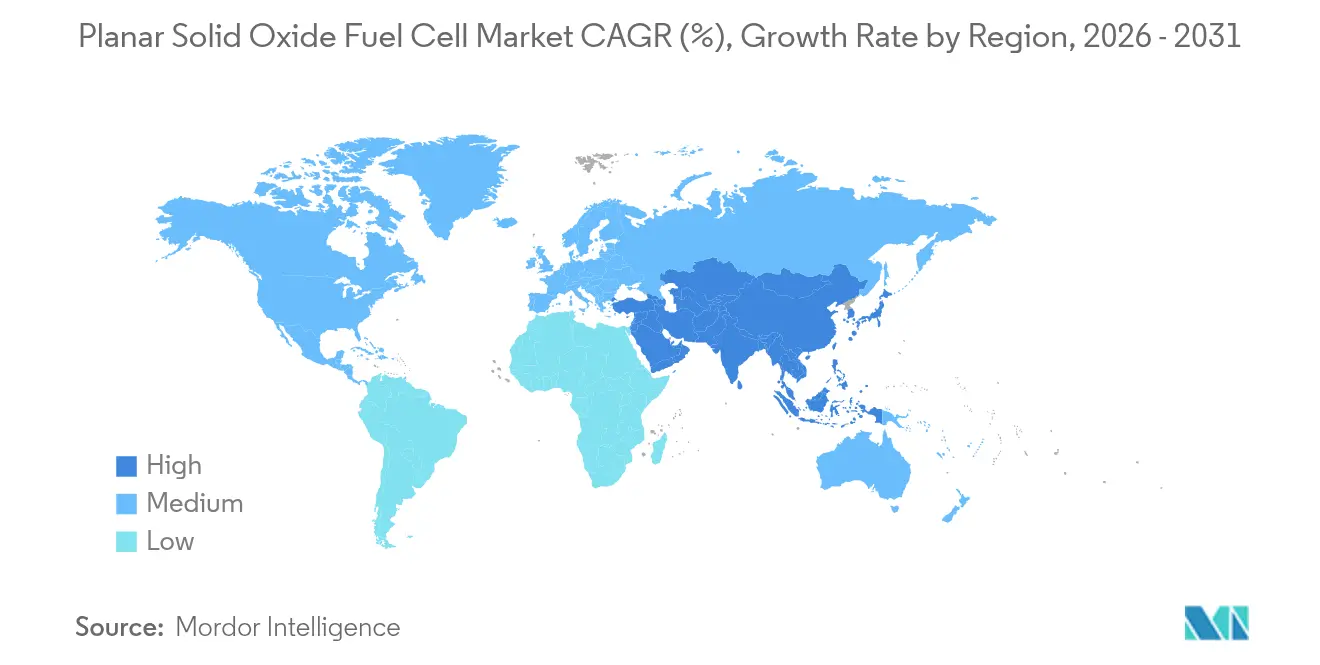

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

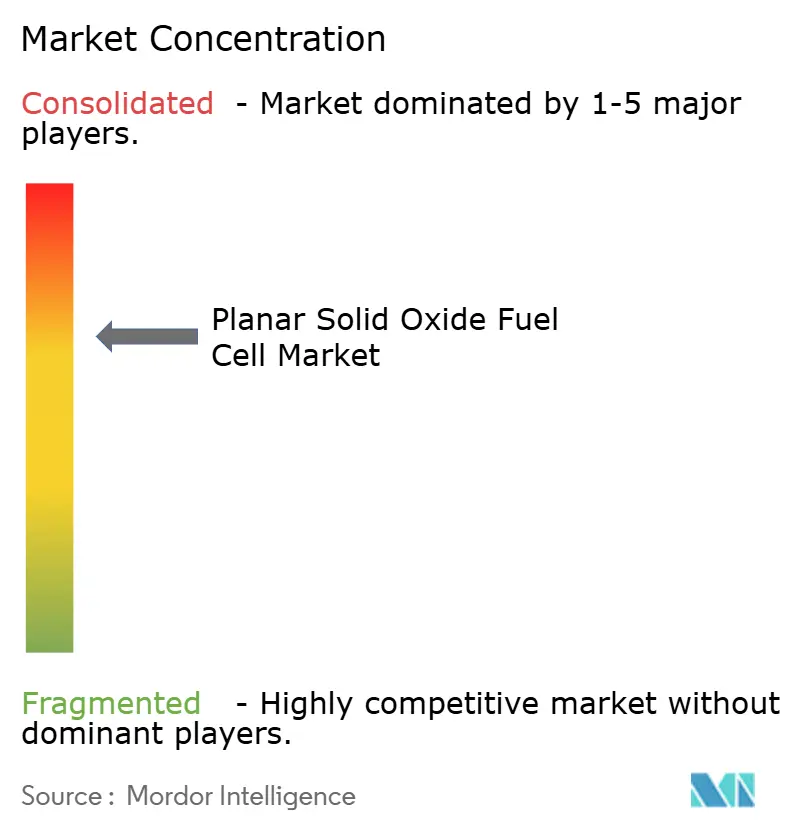

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Planar Solid Oxide Fuel Cell Market Analysis by Mordor Intelligence

The Planar Solid Oxide Fuel Cell market size is expected to grow from USD 1.03 billion in 2025 to USD 1.12 billion in 2026 and is forecast to reach USD 1.74 billion by 2031 at 9.09% CAGR over 2026-2031.

This upward trajectory is largely driven by government-backed hydrogen incentives, increasing data-center power requirements, and steady cost declines in planar solid oxide fuel cell stacks. Widespread policy support is catalyzing first-of-a-kind industrial deployments, while the technology’s 60% electrical efficiency and near-90% total system efficiency when paired with heat recovery position it as a prime replacement for diesel generation in mission-critical sites. Natural-gas fueled units dominate today’s installed base, yet hydrogen-ready designs are gaining ground as clean-fuel regulations tighten. Manufacturers are lowering stack costs through reduced-temperature sintering and increased cell throughput, and investors are responding by accelerating gigawatt-scale factory buildouts in Europe and Asia. Together, these factors underpin investor confidence that the planar solid oxide fuel cell market will remain a pivotal pillar of the global energy-transition toolkit.

Key Report Takeaways

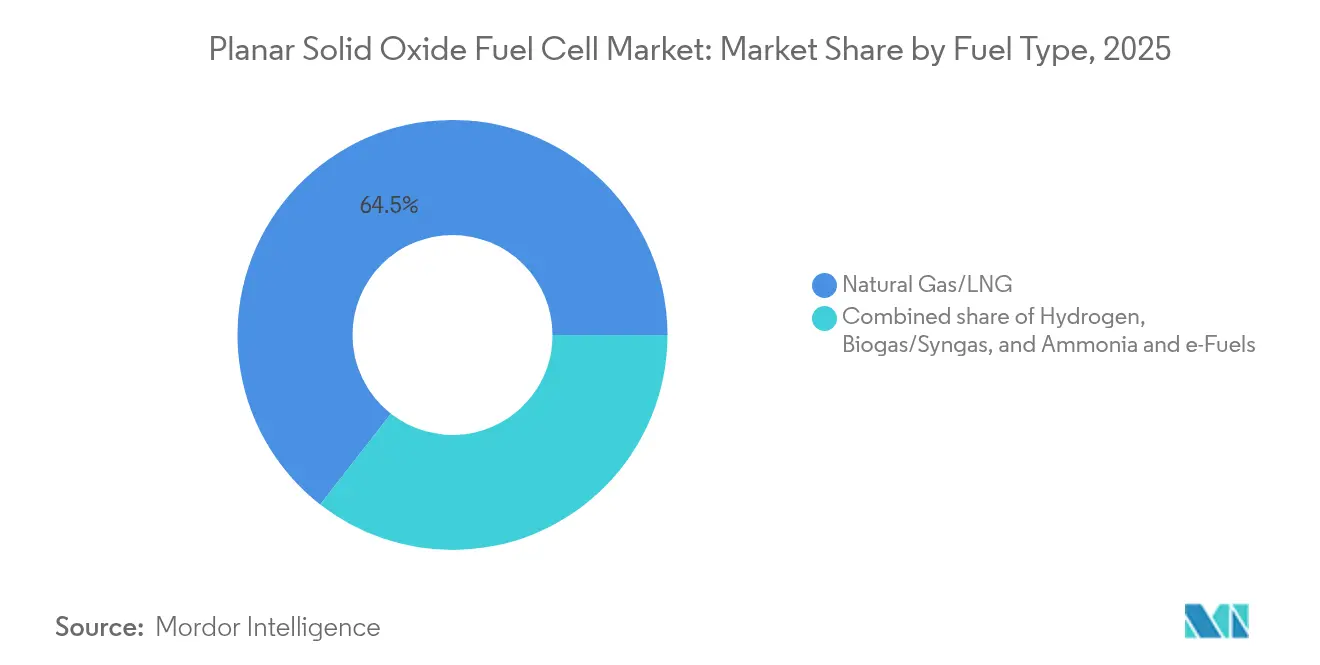

- By fuel type, natural gas/LNG accounted for 64.45% of the planar solid oxide fuel cell market share in 2025, while hydrogen applications are forecast to advance at a 12.35% CAGR through 2031.

- By electrolyte material, yttria-stabilised zirconia (YSZ) accounted for 66.80% of the planar solid oxide fuel cell market size in 2025, whereas lanthanum gallate-based (LSGM) is expanding at a 10.21% CAGR.

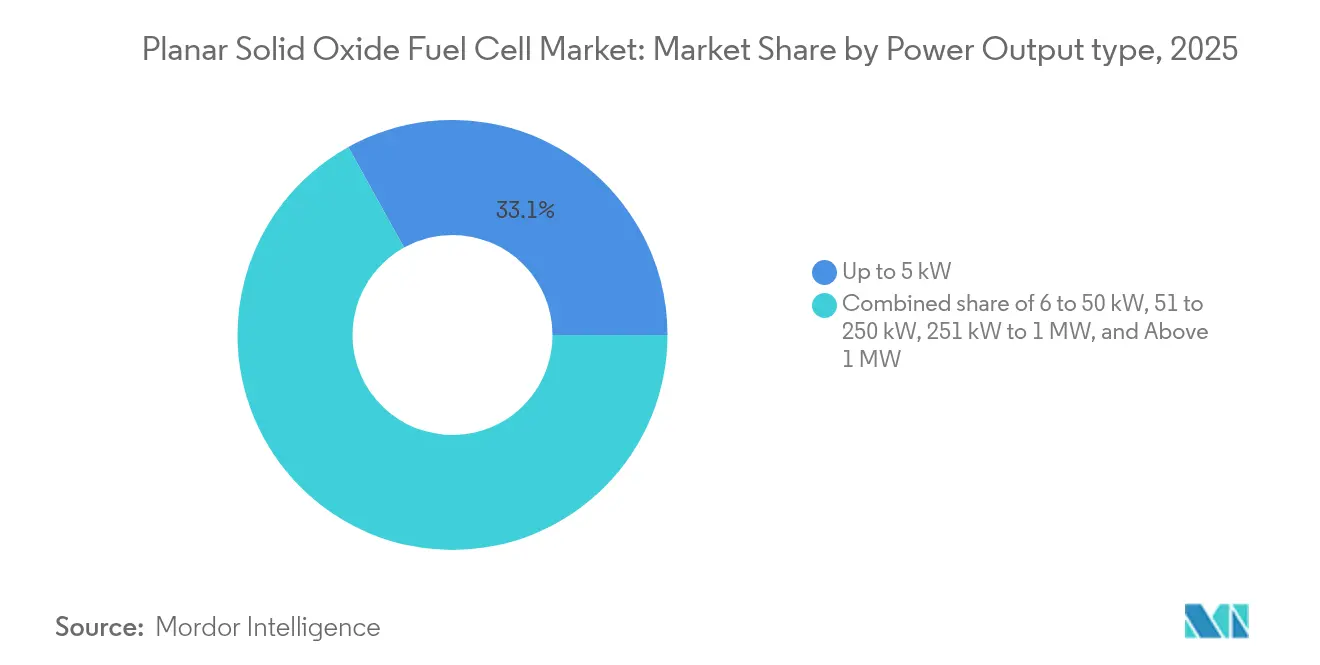

- By power output, the up to 5 kW segment held a 33.05% share of the planar solid oxide fuel cell market size in 2025, and above-1 MW systems are projected to grow at a 11.62% CAGR between 2026 and 2031.

- By application, stationary baseload generation captured a 39.20% share of the planar solid oxide fuel cell market size in 2025, whereas backup and prime-power units are poised to grow at a 9.86% CAGR through 2031.

- By geography, the Asia-Pacific region led with a 47.10% revenue share in 2025; North America is expected to expand at a 10.53% CAGR through 2031.

- Bloom Energy, Ceres Power, FuelCell Energy, and Mitsubishi Power collectively represented more than 55% of global shipments in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Planar Solid Oxide Fuel Cell Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government decarbonization targets & hydrogen incentives | +1.60% | Global (early momentum in North America, Europe, Asia-Pacific) | Medium term (2-4 years) |

| Demand for resilient power in data centres & C&I sites | +2.10% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Advances in planar SOFC manufacturing lower system CAPEX | +1.80% | Global | Medium term (2-4 years) |

| High electrical efficiency & multi-fuel flexibility | +1.40% | Global | Long term (≥ 4 years) |

| Reversible planar SOFCs for on-site green-H₂ production | +1.20% | Europe, North America (spill-over to Asia-Pacific) | Long term (≥ 4 years) |

| CCUS-ready planar SOFC hybrid pilots boost utility uptake | +0.90% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government decarbonization targets & hydrogen incentives

Governments worldwide are pairing climate-neutrality goals with generous fiscal measures that directly benefit the planar solid oxide fuel cell market. The U.S. Inflation Reduction Act offers up to USD 3 per kg in clean-hydrogen production tax credits, Canada applies a 15-40% Clean Hydrogen Investment Tax Credit, and Germany is channeling EUR 4.6 billion into 23 IPCEI Hydrogen Programme projects. Australia’s planned AUD 8 billion hydrogen-production incentive begins in 2027, and the UK’s Gas Shipper Obligation is designed to narrow the cost gap between low-carbon hydrogen and fossil fuels.(1)K&L Gates, “Australia’s Hydrogen Production Incentive,” klgates.comThese incentives cut payback periods for new installations, stimulate local supply chains, and accelerate large-scale manufacturing commitments in Europe and Asia. The alignment of fiscal tools, carbon pricing, and permitting reforms is now translating into bankable project pipelines that will propel the planar solid oxide fuel cell market over the next decade.(2)Federal Government of Germany, “National Hydrogen Strategy Update,” bundesregierung.de

Demand for resilient power in data centres & C&I sites

Explosive growth in generative AI and high-performance computing is doubling the electricity consumption of global data-center clusters, forcing operators to rethink their reliance on standby diesel. Planar solid oxide fuel cell systems achieve 60% net electrical efficiency and can exceed 90% total system efficiency when integrated with chilled-water loops, making them a compelling fit for hyperscale campuses.(3)Microgrid Knowledge, “SOFCs as Prime Power for AI Data Centres,” microgridknowledge.com Recent 9.75 MW installations across Belgian commercial estates and pending 20 MW deployments in California show buyers favoring modular SOFC arrays that can be sited without extensive grid-interconnection upgrades. In commercial and industrial estates, the same technology enables firms to hedge outage risk, monetize waste heat, and meet ESG metrics without sacrificing uptime. The trend is expected to drive multi-megawatt orders and keep data-center operators among the fastest-growing end-users of the planar solid oxide fuel cell market.

Advances in planar SOFC manufacturing lower system CAPEX

Manufacturers are steadily eroding stack costs by shortening sintering dwell times, switching to lower-temperature co-firing, and optimizing cell geometry. Laboratory evidence indicates that co-firing at 1,250 °C, utilizing Fe₂O₃ sintering aids, reduces energy consumption and preserves mechanical integrity compared to 1,550 °C. Tri-layer ceria-zirconia-ceria designs achieve 1.2 W cm-² at 650 °C while retaining large-format manufacturability. Cold-isostatic pressing has delivered dense bilayer electrolytes at 1,250 °C with power densities of 1.251 W cm-². The U.S. Department of Energy targets system-level costs of USD 900 kW⁻¹ by 2025, and analysts expect sub-USD 800 kW⁻¹ beyond 2030 as automated sealing, thinner interconnects, and larger cell footprints are adopted. As high-volume plants transition from pilot to commercial production, these innovations reduce capital cost premiums and expand the addressable market for planar solid oxide fuel cell solutions.

High electrical efficiency & multi-fuel flexibility

Planar SOFC technology achieves over 60% electrical efficiency in standalone mode and approximately 85% in combined heat and power service, surpassing competing combustion and PEM pathways. Internal reforming enables the direct use of natural gas, biogas, syngas, and even ammonia without the need for complex upstream processing. Demonstrations of 100 kW direct-ammonia stacks for maritime power show peak densities exceeding 1,000 mW cm-², while biogas-SOFC coupling achieves a total system efficiency of 70.88% and yields attractive revenue streams for waste management. The ability to operate on today’s pipeline gas and convert to green-hydrogen feedstock tomorrow provides asset owners with future-proofed flexibility, a key selling point in sectors facing decarbonization mandates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital cost vs. conventional generators | –1.5% | Global | Short term (≤ 2 years) |

| Thermal durability & long-term degradation issues | –1.1% | Global | Medium term (2-4 years) |

| Rival PEMFC & battery solutions in low-power range | –0.8% | North America, Europe | Short term (≤ 2 years) |

| Nickel price volatility impacting anode supply chain | –0.6% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High upfront capital cost vs. conventional generators

Planar SOFC systems still command USD 5,000–10,000 kW⁻¹ in the 100 kW to multi-MW range, well above diesel or gas turbines. Small 1–10 kW models can reach USD 30,000 kW⁻¹, a hurdle that suppresses residential adoption. Levelized-cost studies show hydrogen-fueled units at GBP 0.527 kWh⁻¹, triple the natural-gas equivalent, underscoring the premium for zero-carbon operation. Economics improve in regions with high retail electricity prices and supportive feed-in tariffs, but global parity hinges on mass production. Industry roadmaps indicate that stack costs could decrease from USD 500 kW⁻¹ to under USD 100 kW⁻¹ when volumes exceed several hundred megawatts annually, a tipping point that would significantly reduce the price gap.

Thermal durability & long-term degradation issues

Repeated thermal cycling can degrade cell interfaces at a rate of 0.5–1.5% per 1,000 hours, eroding efficiency and shortening maintenance intervals. Interface delamination between cathodes and metallic interconnects remains a primary failure mechanism, with early-life degradation rates peaking at 0.89% per cycle during the first 34 on-off sequences [SCiencedirect.com]. Post-operational examinations of stacks surpassing 100,000 hours reveal chromium poisoning and anode fragmentation, although electrolytes generally remain intact. Research into cobalt-embedded gadolinia-doped ceria nanocatalysts has yielded 30% performance gains in fuel-cell mode and 60% gains in electrolysis mode, paving the way for longer service life at lower temperatures. Continued materials innovation will be vital in achieving the sub-0.25% degradation rate benchmarks demanded by long-term financiers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Type: Hydrogen Drives Decarbonization Transition

Natural gas/LNG retained 64.45% of the planar solid oxide fuel cell market share in 2025, buttressed by existing gas grids and the architecture’s built-in steam reforming capacity. Hydrogen projects, however, are advancing at a 12.35% CAGR and are expected to narrow the gap sharply after 2027 as green-hydrogen costs fall and carbon pricing widens. Biogas-syngas integrations bolster circular-economy economics by monetizing landfill or agricultural waste streams, while ammonia and e-fuel pilots serve heavy-transport niches seeking zero-carbon alternatives. Reversible SOFC modules that switch between fuel-cell and electrolysis modes enable industrial sites to generate hydrogen during low-demand periods and export power at peak tariff hours, unlocking additional revenue. Carbon-capture-compatible stack designs further expand the addressable market among refineries and steel mills pursuing net-zero pathways.

Hydrogen’s advance will continue to pull the planar solid oxide fuel cell market size toward zero-carbon applications through 2031. With governments earmarking tens of billions of dollars for electrolyzer tax credits, plant developers are opting for dual-mode SOFC/SOEC lines that hedge against future commodity price fluctuations. The combination of hydrogen readiness, future fuel flexibility, and falling stack prices positions SOFC arrays as a central solution for industrial decarbonization strategies worldwide.

By Electrolyte Material: YSZ Dominance with LSGM Innovation

Yttria-stabilized zirconia (YSZ) commanded a 66.80% share of the planar solid oxide fuel cell market in 2025, due to its robust ionic conductivity within the 700–800 °C operating window and a mature supply base. Lanthanum gallate (LSGM) is expanding at a 10.21% CAGR as developers seek intermediate-temperature options that alleviate mechanical stress and reduce balance-of-plant costs. Gadolinium-doped ceria meets the niche demand for residential and light-commercial units that require quick ramp rates.

Tri-layer ceria-zirconia-ceria builds boost area-specific resistance to just 0.01 Ω cm², achieving over 1.2 W cm-² at 650 °C, while bilayer YSZ–GDC configurations produced via cold-isostatic pressing reach 1.251 W cm-² at the same temperature. Interface engineering, such as nano-web cathodes, helps curb chromium poisoning and enhances oxygen-reduction kinetics. These electrolyte innovations should preserve YSZ’s lead over the forecast horizon while allowing LSGM hybrids to capture a high-growth share in the portable and mCHP segments.

By Power Output: Megawatt Systems Lead Growth

Units up to 5 kW delivered 33.05% of 2025 shipments, serving residential micro-cogeneration and telecommunication sites. Above-1 MW systems will surge at a 11.62% CAGR as utilities, refineries, and data-center operators standardize multi-megawatt blocks. Bloom Energy’s recent 20 MW contract highlights the scalability of modular planar stacks for grid-interactive microgrids, while Hope Gas’s 7,250-unit residential rollout in West Virginia demonstrates the credibility of the consumer market. Manufacturing-cost models indicate large-format lines could reach USD 370/kW direct costs at high volumes, narrowing the gap with reciprocating engines and accelerating adoption in the >1 MW bracket.

Commercial traction in the 51–250 kW cohort remains strong among retail chains and hospitals seeking resilient on-site generation with combined heat capacities. Meanwhile, 251 kW–1 MW systems bridge corporate campuses and small industrial loads, often configured as fuel-neutral generators that can switch seamlessly between LNG and green hydrogen without requiring hardware replacement.

By Application: Backup Power Emerges as Growth Driver

Stationary baseload plants held a 39.20% share in 2025 and will continue to be the cornerstone of industrial SOFC deployment, delivering critical electricity and high-grade heat. Backup and prime-power units are poised for a 9.86% CAGR as weather-related outages push hospitals, airports, and distribution hubs toward low-emission alternatives to diesel sets. Healthcare installations, such as Klickitat Valley Health's 100 kW hydrogen system, illustrate early momentum, while universities adopt planar SOFC cogeneration to meet net-zero commitments.

Off-grid and auxiliary power markets, including maritime and remote defense posts, are increasingly relying on ammonia- and LPG-fueled stacks to extend mission range without incurring carbon penalties. The cumulative demand from these niches continues to reinforce the planar solid oxide fuel cell market's position as a diversified, multi-application platform.

By End-User: Data Centers Drive Market Expansion

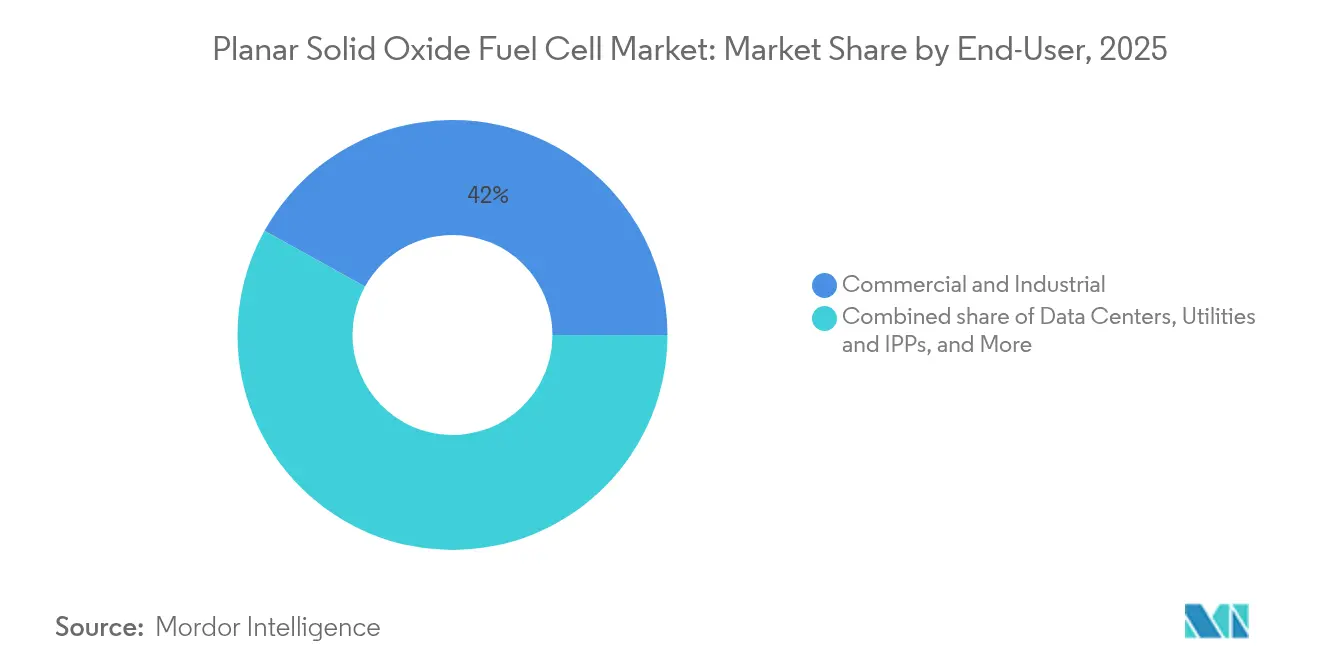

Commercial-industrial buyers represented 41.95% of the 2025 planar solid oxide fuel cell market; however, data-center operators are expected to post a 12.12% CAGR through 2031 as AI workloads increase. Microsoft, Equinix, and CoreWeave are piloting SOFC arrays to displace diesel generators, citing lower Scope 1 emissions and higher fuel efficiency. Utilities are next-tier adopters, integrating multi-megawatt SK Eternix-Bloom Energy blocks into capacity-constrained feeders. Defense agencies are field-testing hydrogen nanogrids that pair planar stacks with renewable energy sources for silent surveillance and perimeter security, demonstrating the technology's versatility across various mission profiles.

Geography Analysis

Asia-Pacific retained a 47.10% share of 2025 shipments on the back of China’s hydrogen-fuel-cell market jump from CNY 1.63 billion in 2019 to CNY 3.93 billion in 2023, with 2024 spend forecast at CNY 5.99 billion. Japan and South Korea continue to invest in both SOEC and SOFC platforms. Korea’s 8 kW electrolyzer stack, which produces 5.7 kg of H₂ per day, is the country’s largest to date. The region’s deep component supply chains and aggressive hydrogen road-maps ensure steady demand for planar solid oxide fuel cell market solutions.

North America is the fastest-growing territory at a 10.53% CAGR. The Inflation Reduction Act’s production credits, combined with DOE research grants and the expanding data center footprint, are propelling orders for multi-megawatt fuel cell parks. Canada’s 15–40% Clean Hydrogen Investment Tax Credit and a CAD 1.5 billion Clean Fuels Fund reinforce continental momentum. Residential adoption is also advancing, highlighted by the WATT HOME program in West Virginia.

Europe’s strategy centers on pairing heavy industry with CCUS. Germany’s 10 GW electrolysis target and EUR 4.6 billion IPCEI outlays, the UK’s Gas Shipper Obligation, and Topsoe’s EUR 94 million EU-funded SOEC gigafactory cement the region’s supply-side capacity. Belgium’s 9.75 MW SOFC deployment signals commercial viability in northern Europe, while broader EU markets benefit from 41 operational CCUS sites and 392 projects in development, providing a ready tie-in for carbon-capture-compatible SOFC hybrid plants.

Competitive Landscape

The planar solid oxide fuel cell market is moderately concentrated, with the top five suppliers accounting for approximately 55% of shipments in 2024. Bloom Energy leverages a vertically integrated stack and balance-of-plant design to win multi-megawatt data center and utility contracts, including the world’s largest fuel cell installation with SK Eternix. Ceres Power follows a capital-light licensing model, granting OEM partners manufacturing rights that accelerate regional scale-up in Asia and Europe. FuelCell Energy is narrowing its focus on distributed generation and large-scale electrolyzers after a 15% cost-reduction restructuring.

Mitsubishi Power is positioning reversible SOFC/SOEC units for industrial hydrogen hubs, while Doosan Fuel Cell plans to commercialize a transportation-focused planar stack in 2025. Maritime applications are a burgeoning white space, as evidenced by Alma Clean Power’s 100 kW ammonia-fueled prototype, which meets strict marine safety codes. Competitive strategy centers on cost leadership, fuel flexibility, and turnkey microgrid solutions, with cross-licensing deals and joint ventures serving as preferred entry points into newly liberalized hydrogen markets.

Planar Solid Oxide Fuel Cell Industry Leaders

Bloom Energy Corp.

Aisin Seiki Co Ltd

POSCO Energy Co. Ltd.

FuelCell Energy Inc

Doosan Fuel Cell Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: FuelCell Energy and Malaysia Marine & Heavy Engineering have initiated a feasibility study for a low-carbon fuel plant that leverages solid oxide electrolysis in Southeast Asia.

- February 2025: Bloom Energy and Sembcorp announced the deployment of SOFCs in Singapore, aligning with the nation’s Green Data Centre Roadmap.

- February 2025: Bloom Energy has secured a 20 MW utility order from FPM Development to deploy its fuel cell technology in Los Angeles, aiming to enhance grid resilience in California.

- January 2025: The U.S. Army has introduced its first hydrogen-powered nanogrid at the White Sands Missile Range in New Mexico. This innovative system, developed by the U.S. Army Engineer Research and Development Center (ERDC), utilizes renewable energy to replace traditional diesel generators for remote, off-grid operations.

Global Planar Solid Oxide Fuel Cell Market Report Scope

The planar solid oxide fuel cell market report include:

| Natural Gas/LNG |

| Hydrogen |

| Biogas/Syngas |

| Ammonia and e-Fuels |

| Yttria-stabilised Zirconia (YSZ) |

| Gadolinium-doped Ceria (GDC/CGO) |

| Lanthanum Gallate-based (LSGM) |

| Others (ScSZ, Composite) |

| Up to 5 kW |

| 6 to 50 kW |

| 51 to 250 kW |

| 251 kW to 1 MW |

| Above 1 MW |

| Stationary Power |

| Combined Heat and Power (mCHP) |

| Backup and Prime Power (Data Centres, Telecom) |

| Auxiliary and Off-grid Units |

| Commercial and Industrial |

| Utilities and IPPs |

| Data Centres |

| Military and Defense |

| Manufacturing |

| Others (Residential, Education, Healthcare) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Fuel Type | Natural Gas/LNG | |

| Hydrogen | ||

| Biogas/Syngas | ||

| Ammonia and e-Fuels | ||

| By Electrolyte Material | Yttria-stabilised Zirconia (YSZ) | |

| Gadolinium-doped Ceria (GDC/CGO) | ||

| Lanthanum Gallate-based (LSGM) | ||

| Others (ScSZ, Composite) | ||

| By Power Output | Up to 5 kW | |

| 6 to 50 kW | ||

| 51 to 250 kW | ||

| 251 kW to 1 MW | ||

| Above 1 MW | ||

| By Application | Stationary Power | |

| Combined Heat and Power (mCHP) | ||

| Backup and Prime Power (Data Centres, Telecom) | ||

| Auxiliary and Off-grid Units | ||

| By End-User | Commercial and Industrial | |

| Utilities and IPPs | ||

| Data Centres | ||

| Military and Defense | ||

| Manufacturing | ||

| Others (Residential, Education, Healthcare) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the planar solid oxide fuel cell market?

The market was valued at USD 1.12 billion in 2026 and is forecast to reach USD 1.74 billion by 2031.

How fast is the planar solid oxide fuel cell market expected to grow?

Industry revenues are projected to rise at a 9.09% compound annual growth rate through 2031.

Which fuel type holds the largest share of installed planar SOFC capacity today?

Natural-gas and LNG-fueled systems commanded 64.45% of global shipments in 2025.

Why are data-center operators adopting planar solid oxide fuel cells?

The technology delivers 60% electrical efficiency, approaches 90% total system efficiency with heat recovery and offers a cleaner alternative to standby diesel generators.

Which region is expanding the quickest?

North America leads in growth momentum with a forecast 10.53% CAGR, driven by policy incentives and hyperscale data-center construction.

What is the main cost barrier facing wider deployment?

Capital costs still range from USD 5 000 to 10 000 per kW for larger systems, although high-volume manufacturing could drive stack prices below USD 100 per kWe over the next decade.

Page last updated on: