Pine Chemicals Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

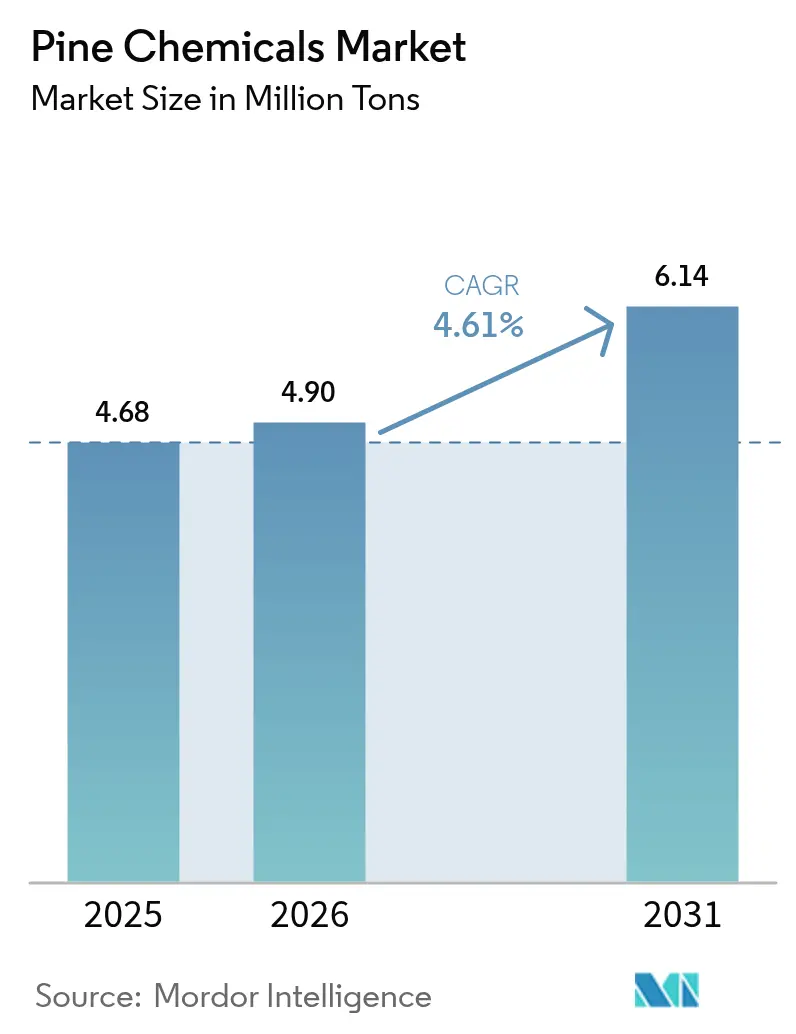

| Market Volume (2026) | 4.9 Million tons |

| Market Volume (2031) | 6.14 Million tons |

| Growth Rate (2026 - 2031) | 4.61% CAGR |

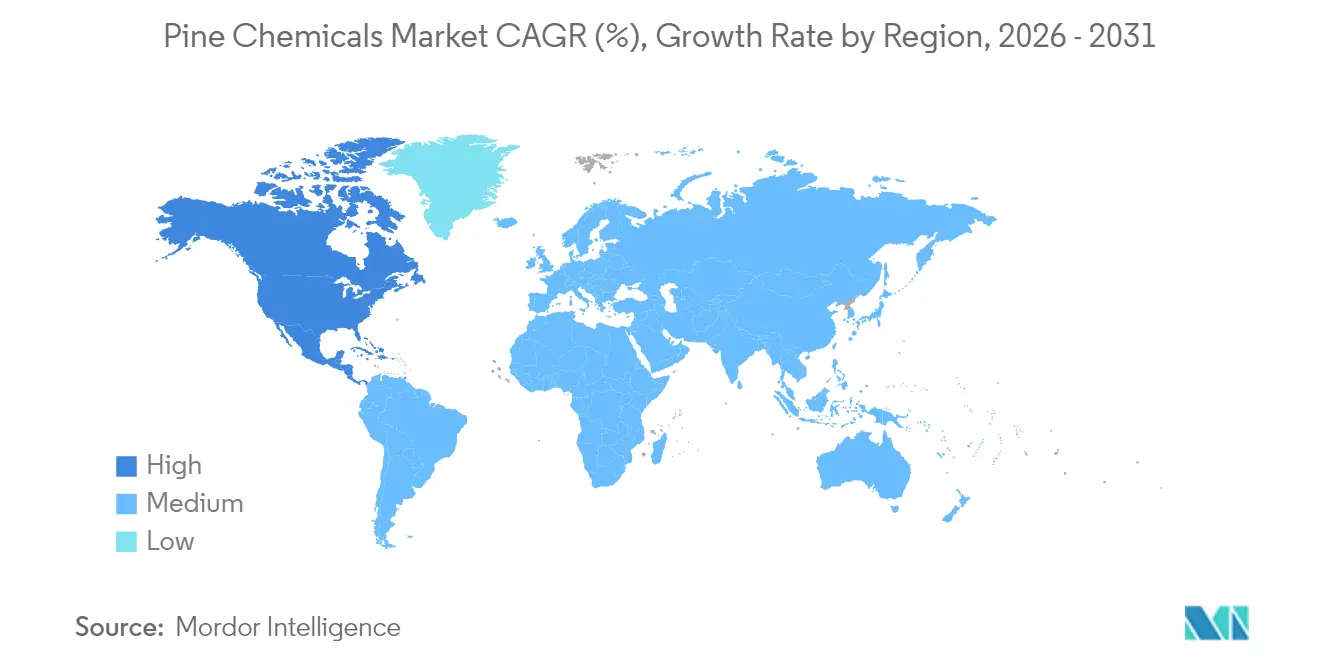

| Fastest Growing Market | North America |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pine Chemicals Market Analysis by Mordor Intelligence

Pine Chemicals market size in 2026 is estimated at 4.9 million tons, growing from 2025 value of 4.68 million tons with 2031 projections showing 6.14 million tons, growing at 4.61% CAGR over 2026-2031. The shift is most visible in adhesives, coatings, and lubricants, where rosin esters and tall-oil derivatives replace hydrocarbon tackifiers and mineral oils to lower emissions and improve traceability. Europe dominates demand today because its kraft-pulping base yields abundant crude tall oil, but North America is scaling fastest as supply-chain localization incentives encourage new refining capacity. Feedstock competition with renewable diesel refiners remains the single largest risk, yet it also underpins pricing power for vertically integrated players who can secure long-term CTO offtake. Innovation in terpene chemistry, from high-purity α-pinene for fragrance intermediates to rosin-based epoxies for EV composites, keeps the pipeline of high-margin specialties expanding, moderating the impact of cyclical swings in commodity adhesives.

Key Report Takeaways

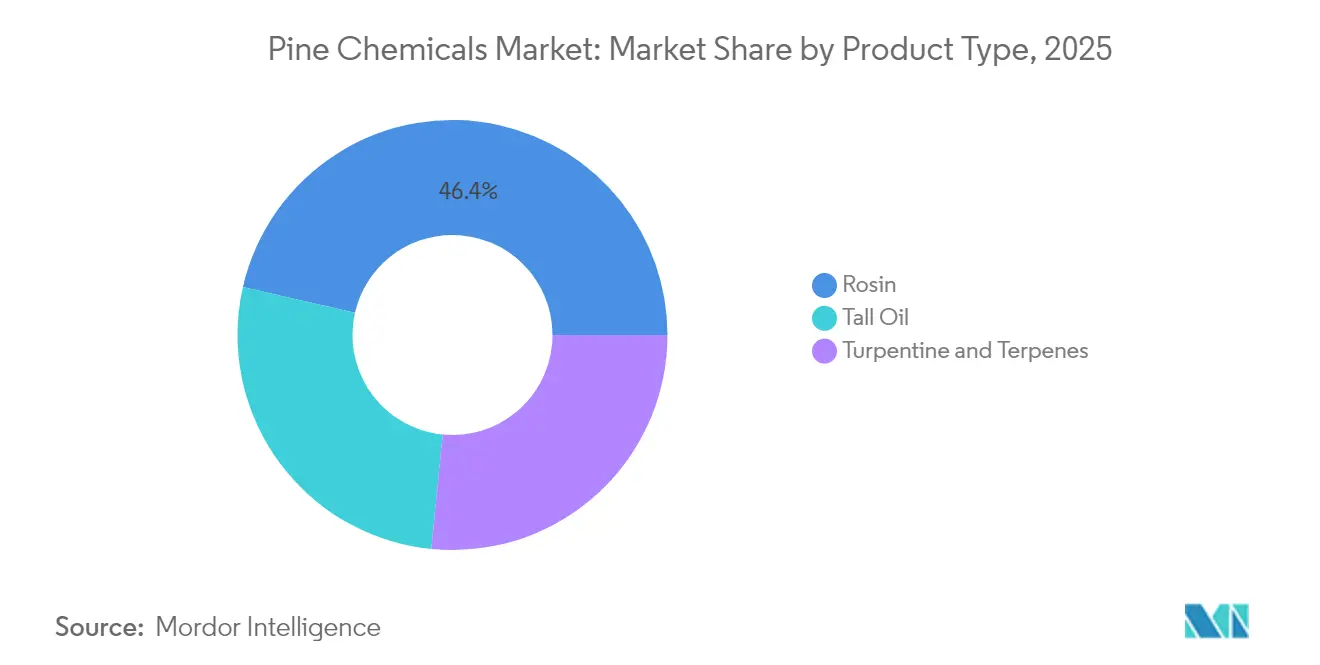

- Rosin held 46.42% of the 2025 product share and is expected to advance at a 4.88% CAGR through 2031.

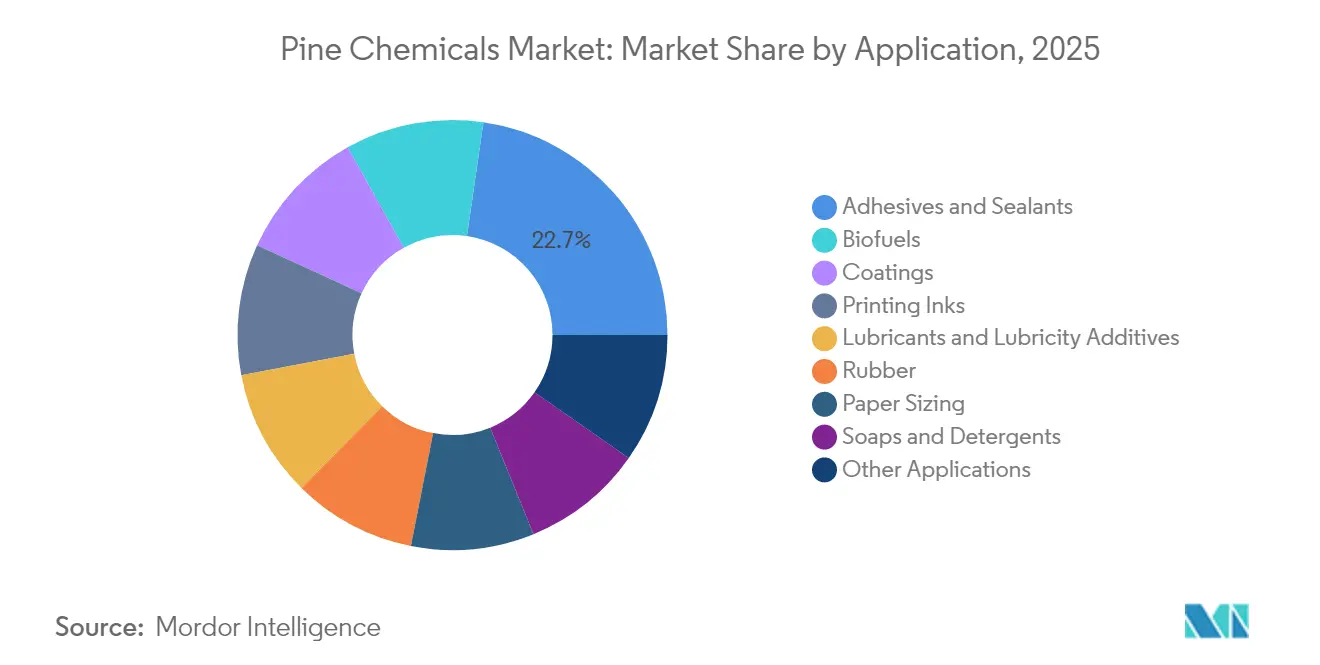

- Adhesives and sealants accounted for 22.70% of the 2025 application share, representing the fastest-growing use case with a 5.26% CAGR to 2031.

- Europe led with 41.92% of 2025 volume, while North America shows the top regional growth rate at 5.01% CAGR for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pine Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand spike from mining flotation and lubricants | +0.8% | APAC, South America | Medium term (2-4 years) |

| Growth of pine-based flavours and fragrances | +0.6% | North America, Europe, emerging APAC | Long term (≥ 4 years) |

| Stricter VOC rules favouring bio-adhesive tackifiers | +1.2% | Europe, North America, spill-over to APAC | Short term (≤ 2 years) |

| Adhesive converters’ shift to rosin esters in EV lightweighting | +0.9% | North America, Europe, China | Medium term (2-4 years) |

| Supply-chain localisation incentives in the United States and European Union | +0.7% | United States, European Union | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Demand Spike From Mining Flotation And Lubricants

Pine oil remains a preferred frother in the flotation of copper, lead, zinc, and iron sulfide because of its partial collecting ability, which stabilizes bubbles and improves concentrate recovery. Declining ore grades in Chile, Peru, Australia, and China raise reagent consumption per ton, lifting incremental pine-oil demand. Parallel growth is achieved through the incorporation of tall-oil fatty acids into metalworking fluids and greases, where biodegradability or bio-content mandates are applicable. As Latin American and Australian mines commit to scope 3 carbon targets, they favor tall-oil–based collectors with lower life-cycle emissions. This pull remains largely insensitive to adhesive-sector cycles, offering volume stability when construction demand softens. Integration between pulp mills and reagent formulators shortens supply chains and secures feedstock in regions distant from pine forests.

Growth Of Pine-Based Flavours And Fragrances

Terpenes distilled from gum or wood turpentine supply α-pinene, β-pinene, limonene, and linalool, all of which are valued as natural aroma molecules for personal care and household cleaners. Consumer preference for clean-label products drives formulators to replace synthetic limonene with traceable, low-contaminant turpentine fractions. Photodegradation studies on pine-resin–treated wine highlight the need for protective packaging to maintain aroma stability, spurring demand for higher-purity terpene streams. North American flavor houses are seeking ISCC-PLUS certification, which rewards suppliers who document sustainable forestry practices. Rising disposable income across ASEAN economies adds incremental demand in mass-market cosmetics. Although supply is concentrated in China, India, and Southeast Asia, traceability premiums support export flows to Europe and North America even when freight costs are elevated.

Stricter VOC Rules Favouring Bio-Adhesive Tackifiers

EU REACH and the Green Deal cap permissible VOC emissions, prompting converters to switch from hydrocarbon tackifiers to rosin esters, which can reduce formulated adhesive emissions. Kraton’s USDA-certified 97% bio-based REvolution grades exemplify the push toward high-bio-content drop-ins. North American EPA limits on architectural coatings reinforce this shift, while export-oriented Asian converters adopt EU-aligned specifications to retain market access. Unlike petroleum resins, rosin esters are readily biodegradable, supporting brand owners' circular economy claims. As regulatory reviews are tightened every three years, converters that pre-qualify their rosin-based systems avoid costly reformulation. This durable tailwind keeps the pine chemicals market outpacing GDP even when macro cycles soften.

Adhesive Converters’ Shift To Rosin Esters In EV Lightweighting

Electric vehicle OEMs rely on structural adhesives to bond multi-material bodies without rivets, saving weight and extending range. Rosin-based epoxy resins synthesized with bio-epichlorohydrin reach near-100% bio-carbon content while meeting mechanical benchmarks for composite panels. UV-curable rosin resins, produced via Michael-addition, show high crosslink density and rapid cure, making them suitable for 3D-printed brackets used in battery enclosures. North American and European OEMs pilot these materials to fulfill scope 3 reporting. The specialty nature of EV adhesives yields above-average margins, cushioning suppliers from volatility in commodity hot-melt pricing. Because certification cycles for automotive parts span three to five years, adoption locks in multi-year demand for qualified rosin ester and epoxy suppliers.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CTO diversion into renewable diesel | −1.3% | Europe, United States, spill-over to Canada | Short term (≤ 2 years) |

| Cheaper C-5/C-9 petroleum resins eroding rosin demand | −0.9% | Global, acute in APAC | Medium term (2-4 years) |

| Seasonal labour shortages in gum-resin belts | −0.6% | China, India, Indonesia, Vietnam, Brazil | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

CTO Diversion Into Renewable Diesel

Refiners aggressively bid for crude tall oil (CTO) when prices for renewable identification numbers surge, as CTO is recognized as an advanced feedstock under both RED III and the U.S. RFS. The EU's anti-dumping duties on Chinese biodiesel will eliminate low-cost imports, tightening the supply of CTO in Europe and driving up prices for adhesive producers. Rosin ester and TOFA manufacturers, lacking long-term contracts, face margin compression as biofuel producers outbid them. Given that CTO constitutes a significant portion of rosin ester costs, even slight price increases can affect adhesive pricing within a quarter. Although some chemical users are investigating synthetic alternatives, gaps in performance and VOC compliance hinder widespread adoption, leaving the pine chemicals market susceptible to fluctuations in biofuel policies.

Cheaper C-5/C-9 Petroleum Resins Eroding Rosin Demand

When crude oil prices soften or petrochemical utilization peaks, C-5 and C-9 petroleum resins undercut rosin esters, tempting price-sensitive hot-melt adhesive and ink converters in China and Southeast Asia. Rosin producers respond by promoting hydrogenated grades that offer superior color stability and UV resistance, attributes that petroleum resins struggle to match in food-contact packaging. Specialty rosin esters thus gain share in regulated niches even as commodity volumes migrate to cheaper petro-resins. This price dance has persisted for two decades and will likely continue, capping upside for pine chemicals market share in bulk packaging adhesives. Technical differentiation and bio-content certification remain the primary shields against petro-resin encroachment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rosin Retains Primacy As Tall Oil Faces Biofuel Pull

Rosin controlled 46.42% of the 2025 volume, and its share of the pine chemicals market is expected to expand 4.88% through 2031, as adhesive and coating converters value its low-VOC profile and drop-in compatibility. Tall-oil rosin dominates bulk tackifier production because kraft-pulping yields ample, consistent feedstock, whereas gum rosin commands price premiums in food-contact and pharmaceutical uses for its lighter color and lower metal content. Gum-rosin supply volatility, tied to seasonal labor and weather fluctuations, prompts high-volume users to shift toward tall-oil derivatives despite looming biofuel diversion. Turpentine fractions provide α-pinene and β-pinene for aroma chemicals, and innovation in pinene-derived methacrylates opens new revenue streams in high-Tg coatings.

Tall-oil fatty acid (TOFA) refineries now pivot between chemical and biofuel contracts, creating allocation tension that cascades into the availability of distilled tall oil (DTO) and tall-oil pitch (TOP). CTO feedstock premiums during high RIN price periods squeeze margins for alkyd-resin and lubricant makers who rely on TOFA’s greater than 90% oleic acid content. In response, integrated pulp-paper groups sign multiyear deals with specialty chemical buyers, ensuring steady offtake and stabilizing the pine chemicals market size allocated to value-added derivatives. Wood rosin from aged stumps holds niche appeal where sustainable forestry certifications align with local procurement, but its slow extraction cycle limits scalability.

By Application: Adhesives Lead While Biofuels Compete For Feedstock

Adhesives and sealants accounted for 22.70% of 2025 demand, the highest among all end uses, and are forecast to grow at a 5.26% CAGR to 2031, maintaining their leadership within the pine chemicals market. Rosin-ester tackifiers deliver optimal peel and shear balance in pressure-sensitive labels and hygiene disposables, while hydrogenated grades serve clear hot melts in electronics packaging. Coatings follow as the second-largest outlet, where rosin-modified phenolics enhance gloss and corrosion resistance in marine and architectural films. Printing inks utilize rosin esters for viscosity control in flexographic processes, which dominate the food packaging industry, an area where migration limits drive demand for low-odor grades.

CTO diversion into renewable diesel creates direct competition with biofuels, which already absorb TOFA and TOP volumes for HVO production. The pine chemicals market share allocated to traditional chemical users thus hinges on policy-driven demand for biofuels. Lubricants benefit from TOFA-based esters that enhance biodegradability in metalworking fluids, particularly for applications subject to stringent wastewater regulations in Europe and North America. Paper sizing demand closely tracks kraft pulp production cycles, providing a steady yet mature outlet. Rubber compounders use rosin acids as tackifiers in tire carcasses, though competition from petroleum-resin alternatives intensifies during oil price downturns.

Geography Analysis

Europe accounted for 41.92% of the 2025 volume, primarily driven by the softwood pulp mills in Scandinavia, which supply crude tall oil and crude sulfate turpentine. The implementation of RED III triples biofuel targets by 2030, diverting more CTO into HVO and SAF, which constrains chemical feedstock and increases rosin prices. Anti-dumping duties on Chinese biodiesel enacted in August 2025 intensify the squeeze, incentivizing European mills to install upgraded extractors to maximize tall-oil recovery. Strong VOC regulations and brand-owner sustainability pledges maintain resilient demand, although high electricity costs erode competitiveness compared to North American suppliers.

North America is projected to record the highest regional CAGR at 5.01% between 2026 and 2031, driven by federal incentives that reward domestic bio-based output and penalize imported high-carbon materials. North America's pine chemicals market is poised for growth, bolstered by estimates suggesting that logging residues could soon be funneled into new facilities, pending the activation of preprocessing depots. In a strategic move underscoring industry consolidation, a major acquisition has been made to secure a steady supply of CTO and enhance fractionation technology. In a nod to the Buy-American clauses tied to public infrastructure projects, regional adhesive manufacturers are increasingly entering into multi-year offtake agreements.

The Asia-Pacific, South America, the Middle East, and Africa collectively supply most gum rosin and absorb growing volumes of rosin ester imports for packaging and construction. China leads gum-resin tapping, but seasonal labor constraints cap output growth, prompting exporters to blend gum and tall-oil rosin to meet color specs. India and Indonesia expand plantations yet face logistics hurdles that limit premium-grade exports. Brazil’s southern states utilize Pinus elliottii for gum rosins, which are used domestically in rubber and cleansing agents, with any surplus directed to Europe. South Africa’s modest tall-oil output serves the domestic adhesives markettheir sourcing, elevating the relevance of North American and European suppliers, while Gulf countries remain net importers. Supply-chain disruptions during pandemic lockdowns prompted many Asian converters to diversify sourcing, elevating North American and European suppliers’ relevance despite longer transit times.

Competitive Landscape

The pine chemicals market is moderately consolidated. Companies are investing in technology to improve purity and yield from variable CTO streams. Supercritical CO₂ extraction reduces energy use and removes sulfur traces that shorten catalyst life in hydrogenated grades. Blockchain-enabled digital traceability systems facilitate the verification of the chain of custody, a crucial requirement for EU eco-label approvals. Market leaders differentiate with hydrogenated rosin esters for electronics adhesives, focusing on color stability and low odor. Terpene distillers are expanding their high-purity α-pinene capacity to meet flavor and fragrance specifications, supported by joint ventures with aroma-chemical firms. Biofuel refiners are emerging as a competitive force. Their willingness to pay CTO premiums when RIN values rise increases chemical feedstock costs, making renewable diesel policies a key factor in pine chemical margins. Chemical producers counter by lobbying for CTO carve-outs or marketing low-carbon intensity scores to secure feedstock. Companies with reliable CTO sourcing and diverse portfolios, from commodity tackifiers to high-margin specialties, gain the most advantage.

Pine Chemicals Industry Leaders

Kraton Corporation

Ingevity Corporation

DRT (Dérivés Résiniques et Terpéniques)

Harima Chemicals Group Inc.

Forchem Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Kraton announces a general price increase of up to 25% on turpentine-refined products and derivatives, effective April 1, 2025.

- March 2024: The Brazilian pine chemicals group agrees to take over Pinopine, Portugal, a producer of gum rosin derivatives. Grupo Resinas Brasil (RB), one of the largest Brazilian producers of pine chemicals, acquires a majority stake in Pinopine, a derivatives producer based in Portugal.

Global Pine Chemicals Market Report Scope

Pine chemicals are a group of organic compounds derived from pine trees, primarily extracted from the resin or sap of pine species. These chemicals include rosin, tall oil, turpentine, and their derivative. They find a wide range of applications due to their adhesive, tackifying, solvency, fragrance, and other functional properties. The pine chemicals market is segmented by product type, application, and geography. By product type, the market is segmented into tall oil, rosin, and turpentine and terpenes. By application, the market is segmented into adhesives and sealants, coatings, printing inks, lubricants and lubricity additives, biofuels, paper sizing, rubber, soaps and detergents, and other applications (oil field chemicals, chemical additives, chewing gum, and food additives). The report also covers the market size and forecasts for pine chemicals in 22 countries across major regions. For each segment, market sizing and forecasts are based on volume (tons).

| Tall Oil | Crude Tall Oil (CTO) |

| Tall Oil Fatty Acid (TOFA) | |

| Distilled Tall Oil (DTO) | |

| Tall Oil Pitch (TOP) | |

| Rosin | Tall Oil Rosin (TOR) |

| Gum Rosin | |

| Wood Rosin | |

| Turpentine and Terpenes | Gum/Wood Turpentine |

| Crude Sulphate Turpentine | |

| Other Turpentines |

| Adhesives and Sealants |

| Coatings |

| Printing Inks |

| Lubricants and Lubricity Additives |

| Biofuels |

| Paper Sizing |

| Rubber |

| Soaps and Detergents |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Tall Oil | Crude Tall Oil (CTO) |

| Tall Oil Fatty Acid (TOFA) | ||

| Distilled Tall Oil (DTO) | ||

| Tall Oil Pitch (TOP) | ||

| Rosin | Tall Oil Rosin (TOR) | |

| Gum Rosin | ||

| Wood Rosin | ||

| Turpentine and Terpenes | Gum/Wood Turpentine | |

| Crude Sulphate Turpentine | ||

| Other Turpentines | ||

| By Application | Adhesives and Sealants | |

| Coatings | ||

| Printing Inks | ||

| Lubricants and Lubricity Additives | ||

| Biofuels | ||

| Paper Sizing | ||

| Rubber | ||

| Soaps and Detergents | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the pine chemicals market in 2026?

The pine chemicals market size is projected to be 4.9 million tons by 2026.

What is the expected growth rate through 2031?

The market is forecast to post a 4.61% CAGR, reaching 6.14 million tons by 2031.

Which product category holds the largest share?

Rosin leads with 46.42% of 2025 volume and continues to gain ground.

Why is North America the fastest-growing region?

Federal localization incentives and renewable diesel mandates drive demand, resulting in a 5.01% CAGR for 2026-2031.

Which end-use shows the highest growth?

Adhesives and sealants expand at a 5.26% CAGR on the back of bio-based, low-VOC demand in packaging, construction, and EV assembly.

Page last updated on: