Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

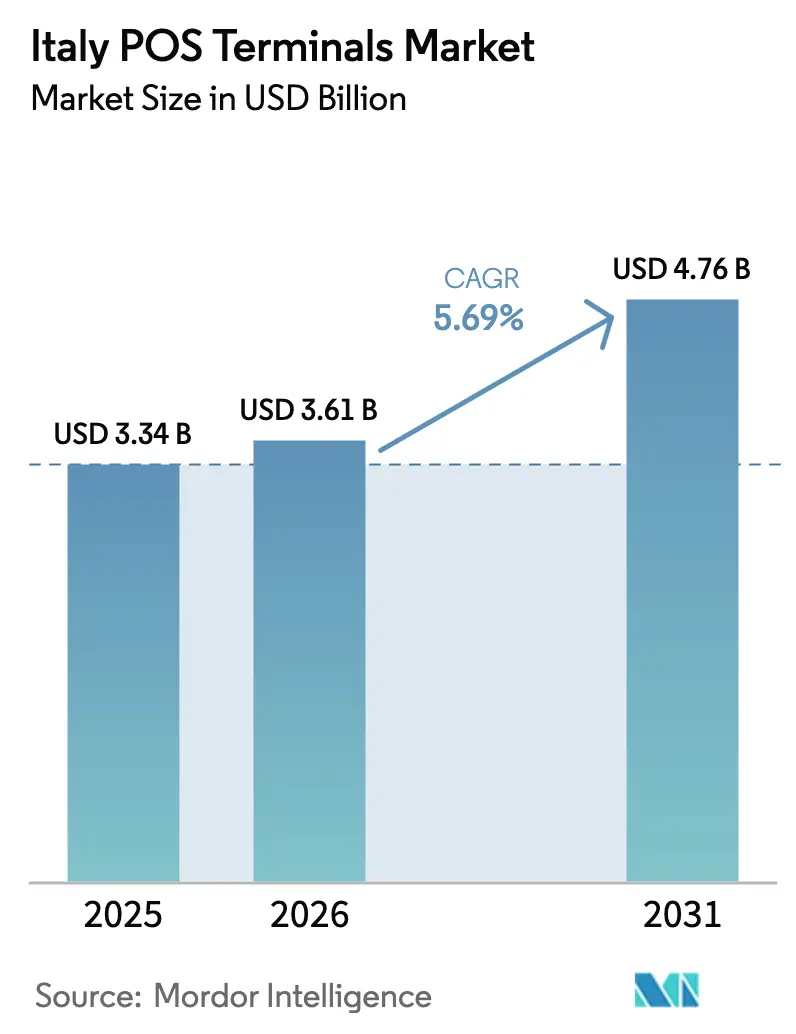

| Base Year Market Size (2025) | USD 3.34 Billion |

| Market Size (2026) | USD 3.61 Billion |

| Market Size (2031) | USD 4.76 Billion |

| Growth Rate (2026 - 2031) | 5.69% CAGR |

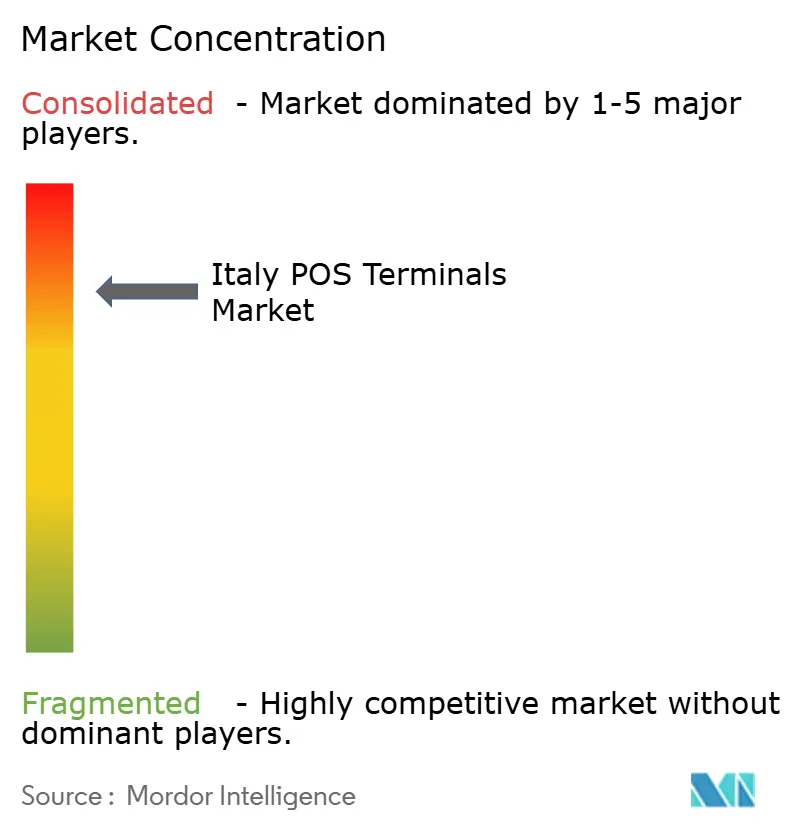

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy POS Terminals Market Analysis by Mordor Intelligence

The Italy POS terminals market size is expected to increase from USD 3.34 billion in 2025 to USD 3.61 billion in 2026 and reach USD 4.76 billion by 2031, growing at a CAGR of 5.69% over 2026-2031. Structural incentives rather than consumer hesitation now define demand: Rome’s 2026 rule that connects every POS device to a telematic cash register recasts fiscal compliance as a hard requirement, while the 30% tax credit on card-processing fees for merchants below EUR 400,000 (USD 452,000) in annual turnover transforms digital acceptance into a subsidized revenue stream. An 80% contactless penetration rate achieved in 2024, well ahead of the euro-area average, signals a payment culture ready for tap-to-pay ubiquity, yet merchant infrastructure and acquirer mark-ups still temper roll-out speed. Consolidation among service providers, illustrated by the EUR 15 billion (USD 17 billion) Nexi-SIA merger, bundles hardware, loyalty software, and acquiring in one contract, increasing switching costs but streamlining on-boarding for small businesses. Simultaneously, semiconductor shortages and PCI-PTS v6 certification queues lengthen hardware delivery cycles, encouraging merchants to favor software-based upgrades when possible.

Key Report Takeaways

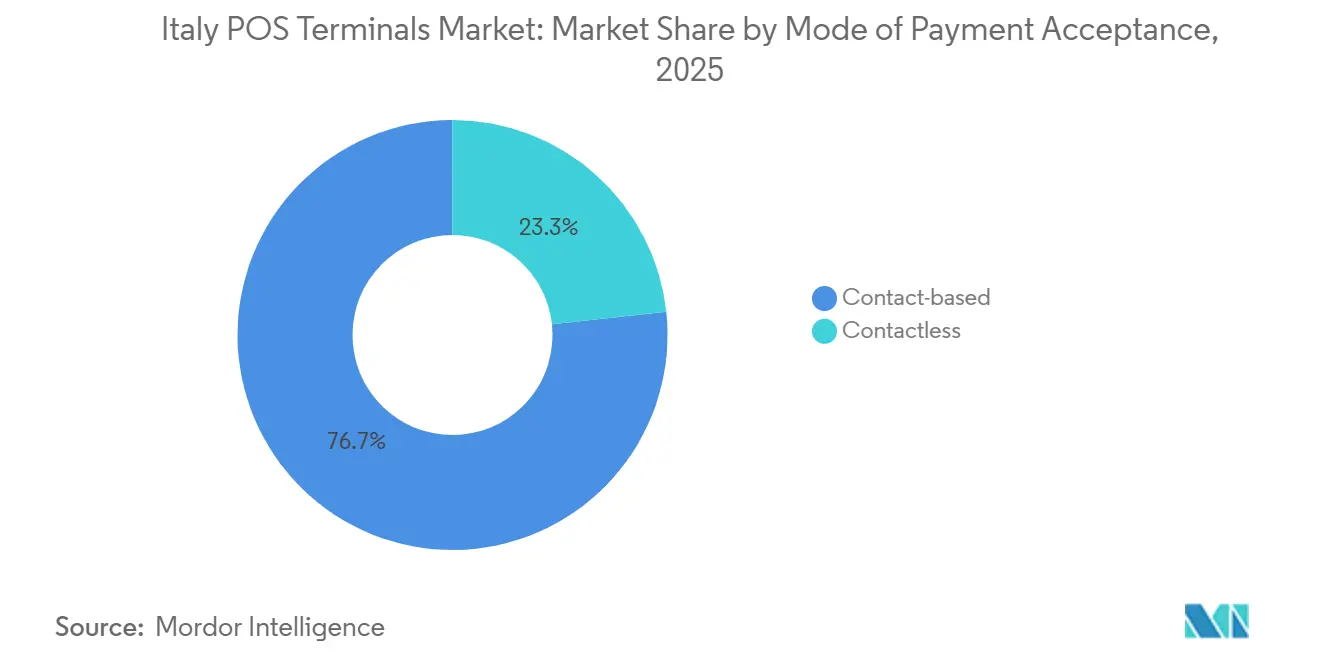

- By mode of payment acceptance, contactless transactions held 76.72% revenue share in 2025, while the same segment is projected to expand at a 5.81% CAGR through 2031.

- By POS type, fixed countertop systems accounted for 71.68% of the Italy POS terminals market size in 2025, whereas portable devices are forecast to grow at a 6.54% CAGR between 2026-2031.

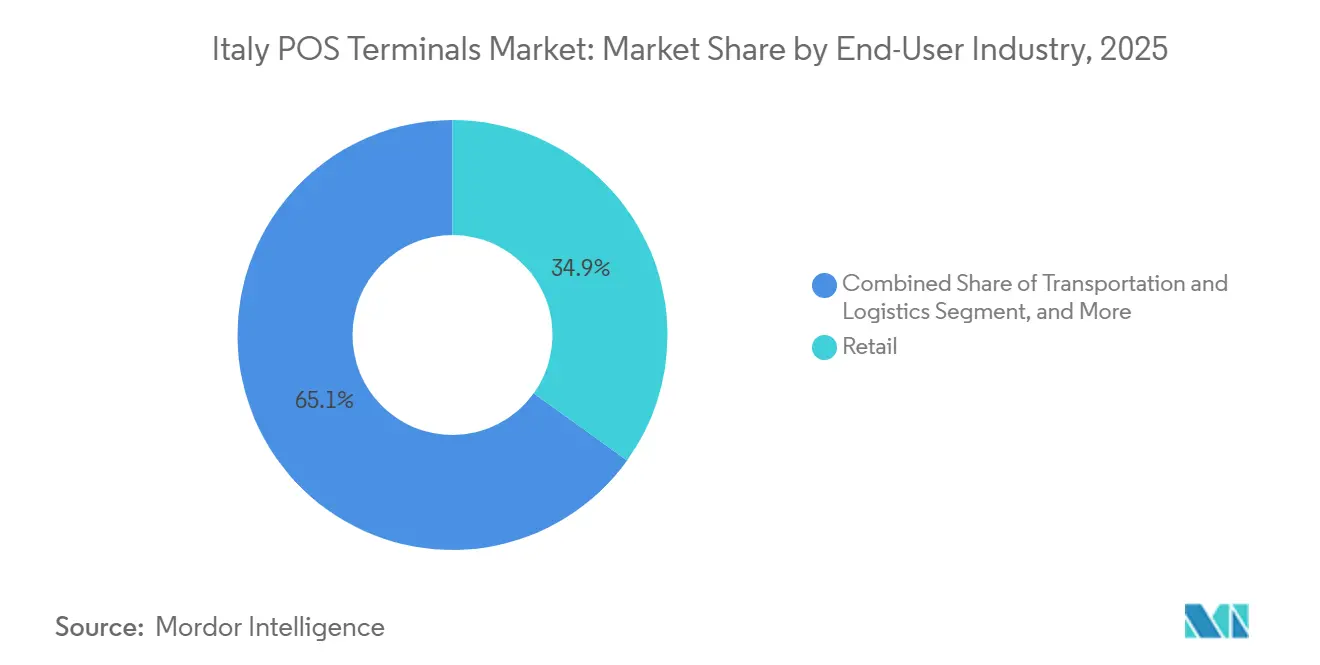

- By end-user industry, retail led with 34.92% of the Italy POS terminals market share in 2025, while healthcare is advancing at a 7.27% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy POS Terminals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| mPOS Adoption Accelerated by Italy's Small-Merchant Tax Incentives | +1.2% | National, southern micro-merchant clusters | Medium term (2-4 years) |

| Mandatory Electronic Invoice and Fiscal Receipt Laws | +1.0% | National, retail and hospitality | Short term (≤ 2 years) |

| Contactless and NFC Penetration Outpacing Cardholder Base | +0.9% | Urban centers, nationwide | Medium term (2-4 years) |

| Migration to Cloud POS for Omnichannel Retail | +0.7% | Fashion, electronics, specialty retail | Long term (≥ 4 years) |

| Banking Consolidation Fueling Integrated Payments (Nexi-SIA Merger) | +0.6% | Northern commercial hubs | Long term (≥ 4 years) |

| Tourism Rebound Driving Hospitality POS Upgrades | +0.5% | Venice, Florence, Rome, coastal resorts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

mPOS Adoption Accelerated by Italy's Small-Merchant Tax Incentives

Italy’s 30% tax credit on acquiring fees lowers out-of-pocket costs for the nation’s 1.5 million sole proprietors, compressing the pay-back period for mobile card readers from 18 months to less than a year. Device vendors such as SumUp and myPOS harness the incentive by bundling flat-rate pricing with same-day settlement, an approach that sidesteps the tiered MDR grids prevalent among incumbent acquirers. Southern regions, Campania, Calabria, and Sicily, shifted from more than 75% cash usage in 2022 to near-parity with the north by 2025, narrowing the regional digital-payments gap by 8 percentage points.[1]Ministero dell’Economia e delle Finanze, “Tax Incentives for Digital Payments,” mef.gov.it The subsidy’s sunset clause in 2026, however, threatens to stall deployment among the most price-sensitive micro-merchants, making renewal a key policy variable. Hardware makers respond by pushing lower-cost, Android-based terminals that double as inventory scanners, ensuring price elasticity does not reverse adoption gains.

Mandatory Electronic Invoice and Fiscal Receipt Laws

The 2026 requirement to route every sales receipt through the Sistema di Interscambio (SDI) compels businesses to upgrade or retrofit 3.27 million terminals, many of which lack APIs for real-time data exchange.[2]Agenzia delle Entrate, “Sistema di Interscambio – Electronic Invoicing,” agenziaentrate.gov.it Vendors now pre-install SDI modules and cloud connectors, converting the POS device into a compliance gateway that automatically archives VAT data and invoice images. Retail and hospitality chains began early roll-outs in 2024 to avoid fines, prompting secondary demand for automated patch-management services that push firmware updates across multiple stores. Integration challenges persist because fiscal printers from Epson, Custom, and Olivetti use proprietary protocols, adding EUR 100-200 (USD 119-237) per lane to bridge software. Nevertheless, linkage between payment capture and tax reporting improves cash-flow transparency, a benefit that resonates with lenders and insurance providers underwriting small businesses.

Contactless and NFC Penetration Outpacing Cardholder Base

Italy reached 80% contactless share of card transactions in 2024, outstripping the euro-area mean of 62%. Yet the cards-per-capita ratio remains below 2.0, indicating deep rather than broad usage. This saturation ceiling forces terminal vendors to pivot toward NFC-enabled mobile wallets and wearables, which bypass the need for plastic issuance. Public-transport deployments act as social proof: Rome’s ATAC augmented validators to accept JCB and UnionPay in 2024, driving a spike in tourist ticket sales.[3]ATAC S.p.A., “ATAC Expands Contactless Payment Options,” atac.roma.it Milan’s ATM registered a 35% year-on-year jump in digital tickets after fitting 1,500 on-board readers in 2023. As consumers normalize tap-to-pay for micro-fares, merchants in adjacent sectors treat NFC acceptance as table stakes, reinforcing the migration away from mag-stripe and signature workflows.

Migration to Cloud POS for Omnichannel Retail

E-commerce penetration rose from 13% of Italian retail sales in 2022 to 18% in 2025, spurring chains to unify web and in-store checkouts. Cloud POS platforms, epitomized by the December 2025 Nexi-Zucchetti tie-up, offer real-time inventory sync, loyalty accrual, and analytics via a browser dashboard, removing the silos that hamper legacy tills.[4]Nexi S.p.A., “Nexi and Zucchetti Expand Partnership,” nexi.it Retailers that shifted to cloud architecture trim PCI-DSS audit scope because cardholder data is tokenized off-site, cutting compliance consulting fees by up to 30%. The model’s revenue-share pricing, usually 2-3% of gross sales, suits higher-margin apparel and electronics but strains grocery and discount stores where net margins rest below 1%. Still, statutory demands for software-managed fiscal receipts drive even thin-margin merchants to consider cloud migration as an unavoidable compliance cost rather than a discretionary upgrade.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Interchange and MDR Fees on Low-Value Transactions | -0.8% | Nation-wide, groceries, fuel, tobacco | Medium term (2-4 years) |

| Fragmented Legacy Fiscal Printer Infrastructure | -0.5% | Retail and hospitality segments | Short term (≤ 2 years) |

| Cybersecurity Breach Concerns Among SMEs | -0.4% | All regions, limited IT resources | Medium term (2-4 years) |

| Supply-Chain Lead-times for PCI-PTS v6 Hardware | -0.3% | Global parts, local deployment | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Interchange and MDR Fees on Low-Value Transactions

EU Regulation 2015/751 caps interchange at 0.2% for debit and 0.3% for credit, but Italian merchants still shoulder all-in processing costs of 1.5-2.5% once acquirer mark-ups and terminal rentals are factored in. For cafés selling EUR 2.00 (USD 2.37) espressos, fixed per-transaction fees as high as EUR 0.10 (USD 0.12) can erase margin entirely, prompting minimum-purchase rules that nudge consumers back to cash. The government’s EUR 30 (USD 35.6) fine plus 4% of invoice value for refusing cards has improved visibility rather than economics, creating resentment among low-ticket operators. Acquirers struggle to cut rates further because network assessments from Visa and Mastercard are non-negotiable, shifting pressure toward hardware subsidies that vertically-integrated players like Nexi can absorb. Without a cost-down mechanism, fee sensitivity may slow mPOS adoption once tax credits disappear.

Fragmented Legacy Fiscal Printer Infrastructure

Roughly 2 million fiscal printers, many more than a decade old, must pair with upgraded POS terminals to satisfy the 2026 SDI real-time reporting rule. Each brand speaks a proprietary command set, so middleware or retro-fit kits add EUR 100-200 (USD 119-237) and slow each transaction by up to half a second, a latency consumers notice in peak retail periods. Smaller acquirers lack the engineering capacity to maintain twenty-plus driver packages, ceding ground to integrated bundles that combine printer, POS, and service contract in one lease. Merchants confronting end-of-life devices must decide between patching aging hardware or investing EUR 500-1,500 (USD 593.6-1,781) in an entirely new fiscal stack, a capital hit that many independent retailers defer until inspectors visit. This fragmentation undermines vendor competition because once a merchant locks into a specific printer-POS ecosystem, switching carries both financial and training costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment Acceptance: Contactless Dominance Reshapes Merchant Expectations

Contactless transactions captured 76.72% of overall acceptance volume in 2025, mirroring consumer appetite for frictionless, card-on-file experiences. That share is forecast to climb steadily at a 5.81% CAGR through 2031, propelled by wallet-based credentials and wearables that extend NFC beyond plastic cards. Italy POS terminals market size expansion in this segment dovetails with Rome’s public-transport upgrades, where contactless validators eliminated the need for paper tickets and set behavioral norms commuters carry into retail. Mobile-first tourists arriving in post-pandemic record numbers reinforce demand peaks in heritage cities, while the European Central Bank’s EUR 50 (USD 59.4) contactless limit renders PIN-less payments viable for most daily spend. Legacy contact-based workflows persist only where value exceeds the tap ceiling or where age-based verification is compulsory, such as jewelry and regulated goods. As saturation nears, acquirers shift focus from volume to value-added data services that monetize contactless behavioral insights, a strategy visible in Nexi’s spend-analytics dashboards bundled into 2025 contracts. For merchants, the incentive pivots from hygiene to queue-time reduction, measured in purchases per labor hour, which aligns directly with profitability.

The residual contact-based segment now functions as a compliance back-stop rather than a growth engine. AML and KYC checks linked to chip-and-PIN flows remain essential for high-ticket or cross-border refunds, but device makers embed dual-interface chips so that no countertop terminal ships without NFC. Consumer education campaigns led by banks in 2024 and 2025 further erode reluctance among seniors, while social-transfer programs disburse welfare benefits via prepaid contactless cards, lifting rural usage. Consequently, the Italy POS terminals market embeds contactless capability as a default specification, making older swipe-only hardware obsolete well ahead of physical end-of-life expectations.

By POS Type: Portable Systems Gain Ground in Service-Intensive Verticals

Fixed countertop stations dominated deployment with a 71.68% share in 2025, sustained by supermarket, department-store, and QSR environments where peripheral density outweighs mobility needs. Their robust casings, thermal printers, and multiple I/O ports keep integration costs predictable, which is crucial for chains running thousands of lanes nationwide. Still, portable terminals are projected to post the segment’s fastest 6.54% CAGR, carving share where bedside or tableside service shortens wait-times and raises average tickets. This growth illustrates a shift in the Italy POS terminals market size allocation from single-purpose hardware toward multipurpose smart devices. Android-based handhelds double as barcode scanners or loyalty sign-up kiosks, reducing device sprawl on the merchant countertop.

Healthcare illustrates the portable thesis vividly. Pilot programs in 2024 allowed outpatient clinics to collect co-payments at bedside, reducing registration bottlenecks and lifting cash-flow predictability. Hospitality follows closely: hotels lining the Amalfi Coast swap paper folios for tablet checkouts that email invoices in SDI format, aligning with 2026 compliance without burdening front-desk staff. Fixed systems, however, remain mandated where telematic cash registers draw substantial power or where connectivity relies on Ethernet rather than cellular back-haul. Hybrid roll-outs, tablets paired with fixed printers, allow mid-sized retailers to add seasonal capacity without breaching existing lease covenants, demonstrating that flexibility, not outright hardware displacement, defines the competitive narrative.

By End-User Industry: Healthcare Emerges as Growth Catalyst

Retail commanded 34.92% of deployments in 2025, naturally reflecting its sheer store-count dominance across grocery, fashion, and home-improvement formats. Yet the Italy POS terminals market share profile is tilting toward healthcare, where a 7.27% forecast CAGR captures tele-consultation fees, at-home nursing visits, and private clinic modernizations previously outside the card ecosystem. Cloud-linked portable units now interface directly with electronic health-record systems, allowing practitioners to charge, code, and reconcile in one workflow, a capability prized by insurers auditing claim accuracy. The retail sector is hardly static: omnichannel loyalty programs push chains to embed QR issuance and scan-to-pay inside the same device, marginally raising the average selling price per unit.

Tourism-rich hospitality layers on incremental demand. Hotel and restaurant operators exploited the 2024 visitor rebound by upgrading to multi-currency enabled terminals that settle in real time, avoiding FX margin leakage. Transportation contributes an emerging but meaningful tailwind; investment of EUR 3.0 million (USD 3.4 million) by Bologna’s TPER into EMV validators in 2023 proves mobile devices can handle five-million-plus annual ticket scans without failure. Government kiosks, education canteens, and live-event venues round out long-tail verticals, each scaling gradually yet cumulatively adding volume that densifies acquirer networks and lowers per-transaction telecom costs.

Geography Analysis

Northern Italy anchors 55-60% of installed POS devices, a function of higher per-capita GDP and dense retail corridors radiating from Milan. Lombardy’s regional tax agency rigorously enforces SDI compliance, nudging merchants to modernize ahead of the 2026 deadline, while urban commuters acclimate to contactless fares on Milan’s 1,500 bus validators. Central provinces centered on Rome and Florence lean on tourism to justify upgrades; ATAC’s expansion to JCB and UnionPay acceptance in 2024 encouraged hoteliers and restaurants to follow suit, locking international cardholders into frictionless spend loops. The Italy POS terminals market thus mirrors regional GDP dispersion, yet fiscal incentives have started to compress disparities.

Southern regions exhibit the steepest growth curves. A 30% tax credit for card fees collapsed the cost barrier for micro-enterprises and lifted acceptance density in Campania and Sicily, shrinking the north-south digital divide by eight percentage points between 2023 and 2025. Enforcement remains lighter, so some single-location retailers postpone upgrades until inspectors arrive, elongating the sales cycle for acquirers. Seasonal surges along the Amalfi Coast and Sardinia compel merchants to favor portable terminals rented for summer months, a model that eases cap-ex but presses acquirers to develop usage-based pricing. Island geographies suffer from higher telecom back-haul costs, inflating total cost of ownership by 15-20% and advantaging national players able to negotiate wholesale data bundles.

White-space persists across regional rail, municipal parking, and open-air markets where POS penetration stays under 50%. Vendors courting these sectors stress ruggedized casings and offline-first operation that synchronizes once the signal returns, features essential for hillside towns where fiber coverage lags. The Italy POS terminals market therefore advances unevenly but irrevocably, with policy levers, tourism flows, and telecom infrastructure jointly dictating the adoption slope.

Competitive Landscape

Nexi commands roughly 35-40% of merchant acquiring and terminal deployment, leveraging its 2021 absorption of SIA to bundle gateway, fraud tools, and hardware under a single contract, locking in small businesses that prize one-stop service. Worldline’s Ingenico line, Verifone’s V-series, and PAX Technology fight for share through faster PCI-PTS v6 certification and modular add-ons, yet their go-to-market depends heavily on Italian integrators such as Zucchetti. SumUp and myPOS angle for the 1.5 million freelancers outside traditional banking by pairing flat-rate fees with no-strings hardware, trading feature depth for transparency. This fragmentation means competition is asymmetric: acquirers cross-subsidize hardware, while stand-alone manufacturers must rely on differentiation in form factor or vertical specificity.

Regulation shapes rivalry. The 2026 SDI mandate acts as a moat because vendors with Italian engineering teams can ship compliant firmware months ahead of global peers. Nexi’s December 2025 pact with Zucchetti embeds payments inside ERP modules, proving that software compatibility, not raw terminal specs, increasingly seals the deal. Transportation validators form a niche battlefront: Axerve and PAX chase contracts from intercity bus operators still mired in paper ticketing. Cybersecurity posture is rising in procurement checklists after a rash of SME malware breaches in 2024, driving interest in devices supporting remote-key injection and multi-factor admin log-ins. As vertical SaaS providers from booking to invoicing embed payments directly, the Italy POS terminals market witnesses convergence between banking and software, pressuring incumbents to defend share with loyalty, lending, and analytics add-ons.

Strategic moves underline the contest. Nexi’s November 2025 launch of a working-capital advance tied to terminal throughput illustrates data-driven monetization absent in hardware-alone models. Verifone’s June 2024 V400c rollout, pre-certified for SDI, shows time-to-compliance as a sales lever. Olivetti’s alliances bundle fiscal printers and terminals, capturing retrofit spend that smaller acquirers cannot finance. Fintech entrants like Adyen seek to bypass domestic processors altogether by offering a unified European gateway, but local compliance quirks make partnerships unavoidable, preserving a measure of insulation for incumbents.

Italy POS Terminals Industry Leaders

NCR Corporation

Panasonic Corporation

NEC Corporation

Casio Computer Co. Ltd

Ingenico ( Worldline SA )

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Nexi and Zucchetti deepened their partnership to stitch card acceptance into Zucchetti’s cloud retail and hospitality suite, enabling unified reconciliation across channels.

- November 2025: Nexi introduced a merchant-solutions stack coupling POS hardware with automated cash-advance offers based on live turnover metrics.

- October 2024: SumUp released a rugged portable terminal boasting 12-hour battery life, aimed at outdoor vendors and food trucks.

- September 2024: Axerve launched an API-first cloud POS platform that embeds payments into vertical SaaS applications within days.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Italy POS terminals market as the value generated from every new fixed workstation, self-checkout lane, tablet, and handheld reader sold inside Italy that ships with an embedded or attachable payment interface and is invoiced as one physical unit in U.S. dollars. Fiscal printers, software-only SoftPOS applications, and post-sale service contracts sit outside this scope.

Scope exclusions: aftermarket maintenance, stand-alone gateways, and purely software apps are not counted.

Segmentation Overview

- By Mode of Payment

- Contact-based

- Contactless

- By POS Type

- Fixed Point-of-Sale Systems

- Mobile and Portable Point-of-Sale Systems

- By End-User Industry

- Retail

- Hospitality

- Healthcare

- Transportation and Logistics

- Other End-User Industries

Detailed Research Methodology and Data Validation

Primary Research

Conversations with merchant acquirers, POS hardware distributors, hospitality chains, and software integrators across Northern, Central, and Southern Italy helped us verify replacement cycles, discount structures, and upcoming fiscal-register integrations. Feedback from local SME retailers confirmed the pace at which on-premise systems are switching to cloud-managed devices.

Desk Research

Mordor analysts first assembled a fact base from freely available, authoritative sources such as the Bank of Italy's payment instrument bulletin, ECB Statistical Data Warehouse card figures, Eurostat customs codes for HS 847050, and releases from the Italian Revenue Agency on mandatory e-receipt rollouts. Trade insights were taken from the Politecnico di Milano Digital Innovation Observatory and press releases that detail annual terminal rollouts by leading acquirers.

These materials were supported by company filings accessed through D&B Hoovers, news archives on Dow Jones Factiva, and press coverage that tracked SoftPOS pilot counts. Together, they framed shipment trends, ASP drift, and regulation timelines. The sources listed are illustrative; many others were reviewed to cross-check facts and fill minor gaps.

Market-Sizing & Forecasting

A top-down build starts with the installed base of terminals reported for the base year, multiplies expected replacement rates, and then layers new-merchant additions derived from VAT registration data. Select bottom-up checks, sampled supplier shipments, and observed average selling price multiplied by volume in distribution channels keep totals grounded. Key variables in our model include contactless card transaction growth, mandated deadline for e-receipt linkage, average selling price movement, and the share of mobile units in total installs. Multivariate regression projects each driver and produces a market value for the forecast period, with forecasts refined through scenario analysis to reflect macro and regulatory swings.

Data Validation & Update Cycle

Outputs pass anomaly screens, peer review, and reconciliation against external payment and trade indicators before sign-off. Reports refresh annually, and an interim update is triggered when material policy or pricing shifts occur, ensuring clients always receive the latest vetted view.

Why Mordor's Italy POS Terminals Baseline Earns Trust

Published estimates often diverge because firms mix hardware with services, fix FX rates differently, or overlook looming fiscal mandates.

Our disciplined scope selection, live regulatory tracking, and yearly refresh cadence narrow those gaps and give decision-makers a steady compass.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.34 B (2025) | Mordor Intelligence | |

| USD 3.50 B (2024) | Global Research Firm A | Bundles maintenance and refurb units; uses constant 2024 FX with no inflation restatement |

| USD 2.83 B (2024) | International Publisher B | Counts hardware units only, applies lower ASPs, and extends pre-2020 trend without factoring the 2026 e-receipt mandate |

In sum, Mordor's balanced hardware-only baseline, cross-checked against shipment audits and regulatory milestones, offers the most transparent and repeatable starting point for strategy or investment planning in Italy's fast-evolving POS landscape.

Key Questions Answered in the Report

How large will Italy's POS terminal opportunity become by 2031?

The market is projected to reach USD 4.76 billion by 2031, reflecting a 5.69% CAGR from 2026.

Which acceptance mode drives most device demand today?

Contactless transactions already account for 76.72% of volume in 2025 and keep expanding due to NFC wallets and tourist usage.

Why are portable terminals growing faster than fixed units?

Healthcare, hospitality, and field-service operators favor mobile form factors that enable bedside or tableside billing, pushing a 6.54% CAGR in portable devices through 2031.

What makes healthcare a standout vertical?

Telemedicine, outpatient co-payment digitization, and private-clinic upgrades translate into a 7.27% forecast CAGR, the fastest among end-users.

How does the 2026 fiscal-receipt mandate influence buying cycles?

It forces 3.27 million existing terminals to integrate with SDI, accelerating replacement and giving SDI-ready models a regulatory edge.

Which player holds the strongest competitive position?

Nexi combines a 35-40% acquiring share with bundled hardware and data services, reinforced by the 2021 SIA merger and 2025 Zucchetti integration.

Page last updated on: