Pharmaceutical Glass Vials And Ampoules Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

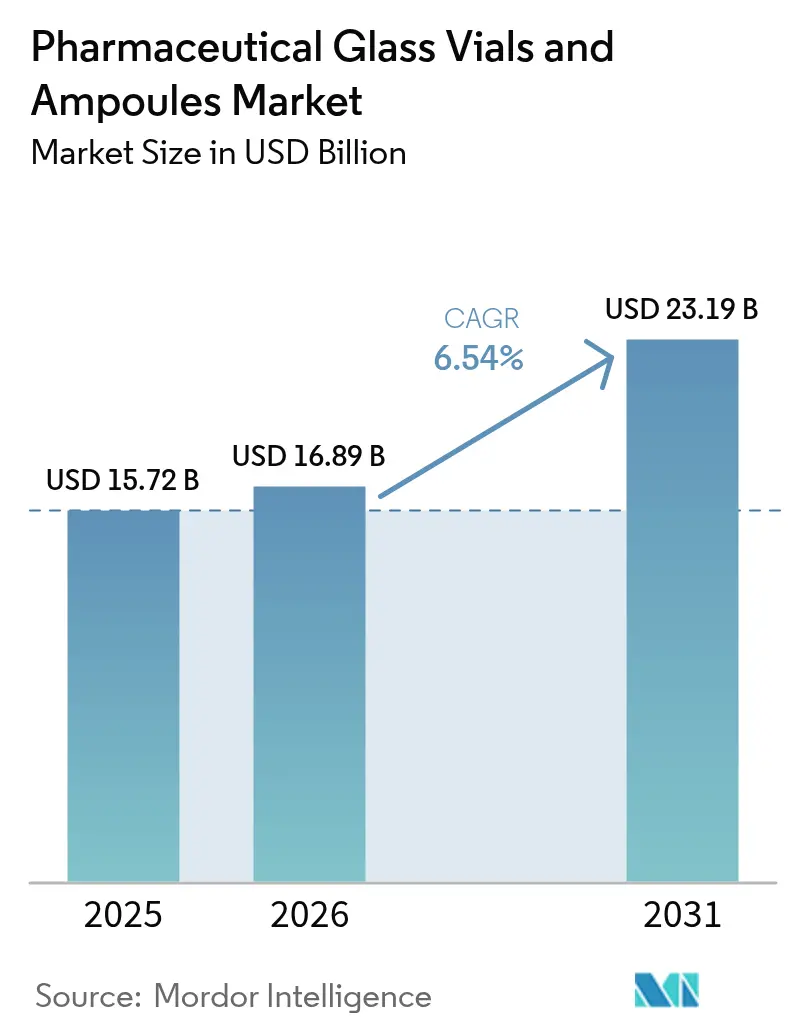

| Market Size (2026) | USD 16.89 Billion |

| Market Size (2031) | USD 23.19 Billion |

| Growth Rate (2026 - 2031) | 6.54% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmaceutical Glass Vials And Ampoules Market Analysis by Mordor Intelligence

The Pharmaceutical Glass Vials And Ampoules Market size is projected to be USD 15.72 billion in 2025, USD 16.89 billion in 2026, and reach USD 23.19 billion by 2031, growing at a CAGR of 6.54% from 2026 to 2031.

Demand is riding on three structural pillars: the fast-growing biologics pipeline, post-pandemic vaccine programs, and policy-led sustainability targets that explicitly prioritize infinitely recyclable glass over polymers. Type I borosilicate remains the default container for high-value drugs because its low alkali release avoids protein aggregation, a property essential for monoclonal antibodies now filling late-stage pipelines. At the same time, ready-to-use sterile formats are reshaping fill-finish economics by compressing batch lead times for contract manufacturers. Competitive intensity is moderate, yet regional specialists in Asia are leveraging shorter lead times to chip away at incumbents’ positions.

Key Report Takeaways

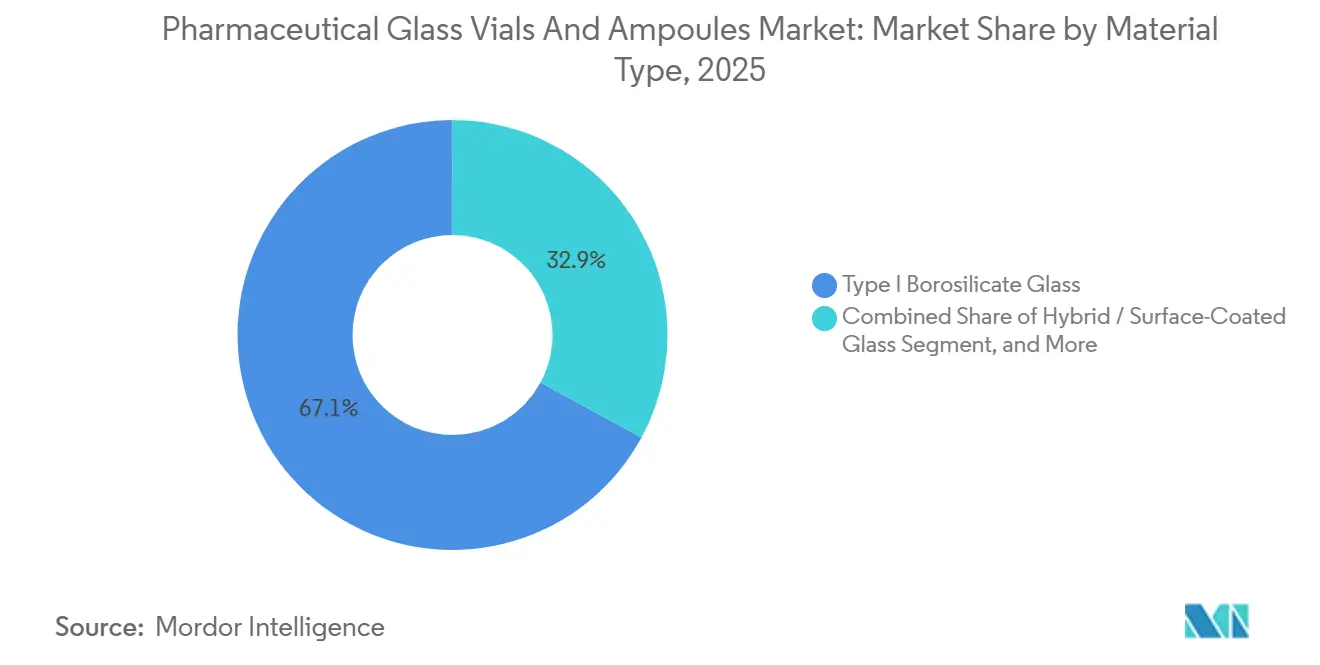

- By material type, Type I borosilicate glass led with 67.10% revenue share in 2025, while hybrid and surface-coated variants are projected to advance at a 7.31% CAGR through 2031.

- By application, vaccines accounted for 46.43% of 2025 revenue; biologics and biosimilars are on track for the fastest growth, with a 7.57% CAGR to 2031.

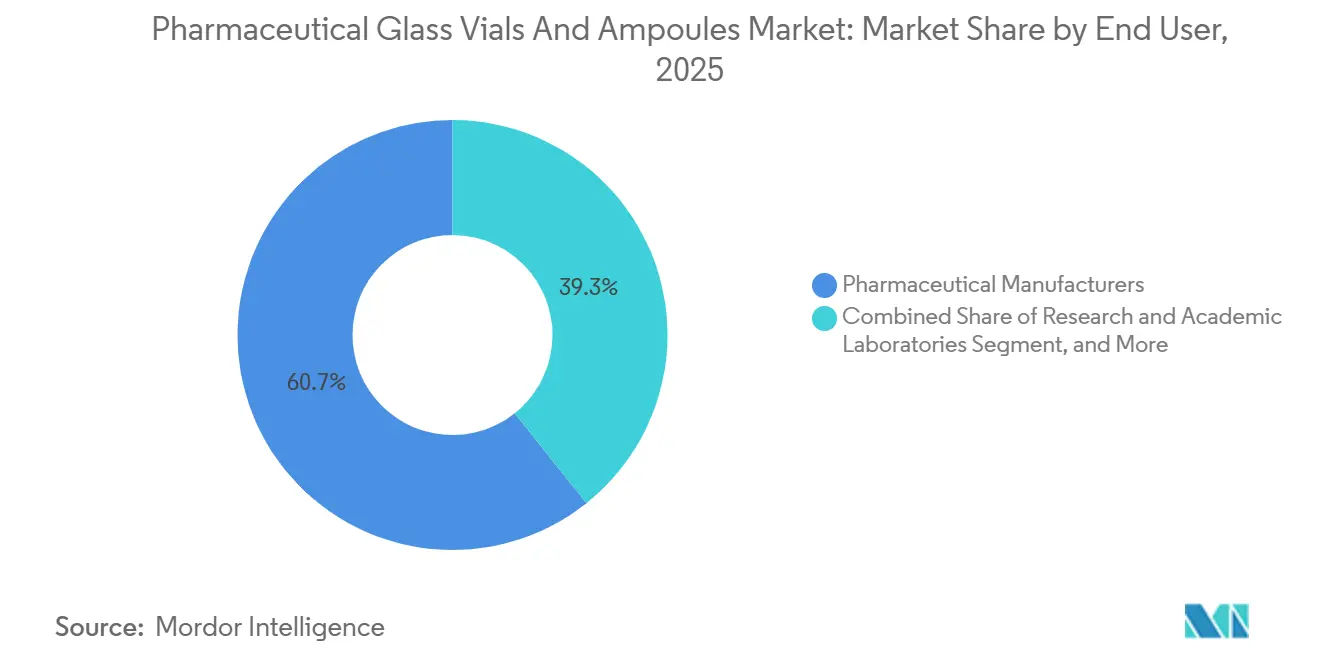

- By end user, pharmaceutical manufacturers held 60.71% share in 2025, whereas biotechnology companies are forecast to grow at 7.63% CAGR through 2031.

- By manufacturing technology, tubular glass forming accounted for 71.21% of 2025 revenue, yet ready-to-use sterile vials are projected to exhibit the highest CAGR of 7.12% to 2031.

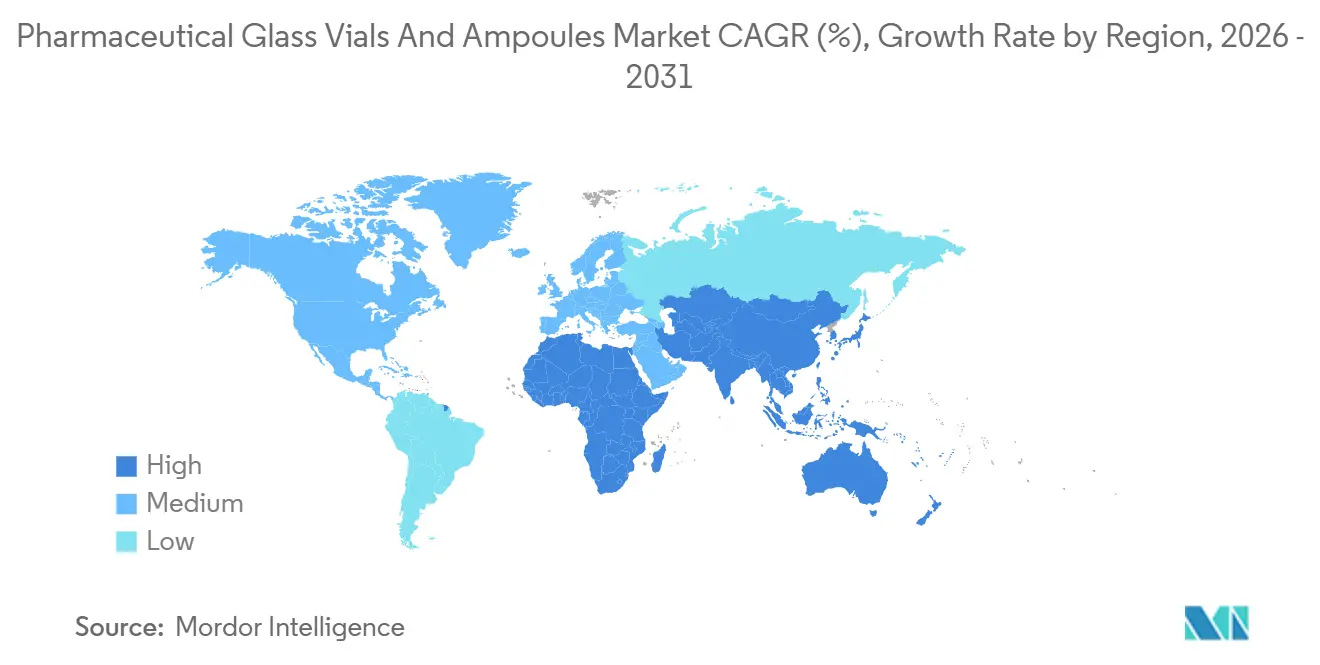

- By geography, North America captured 37.64% revenue in 2025; Asia-Pacific is expected to post the strongest regional CAGR at 7.53% over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pharmaceutical Glass Vials And Ampoules Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-Pandemic Vaccine Pipeline Boosts Vial Demand | +1.8% | Global, Led by North America, Europe, Asia-Pacific | Medium Term (2–4 Years) |

| Biologics Shift Toward Chemically Inert Borosilicate | +1.5% | North America and Europe | Long Term (≥4 Years) |

| Sustainability and Recyclability Regulations Favor Glass | +1.2% | Europe and North America, Emerging in Asia-Pacific | Long Term (≥4 Years) |

| mRNA Cold-Chain Needs Ultra-Low Expansion Glass | +1.0% | Early Adoption in North America and Europe | Medium Term (2–4 Years) |

| AI-Driven Inline Inspection Enables Zero-Defect Pricing | +0.8% | North America, Europe, Advanced Asia-Pacific | Short Term (≤2 Years) |

| Pharma 4.0 QC Digital Twins Accelerate RTU Vial Adoption | +0.7% | North America, Europe, Select Asia-Pacific Contract Facilities | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Post-Pandemic Vaccine Pipeline Boosts Vial Demand

A record 284 vaccine candidates were active worldwide in December 2025, up 37% year on year, with mRNA and viral-vector platforms making up almost two-thirds of that pipeline.[1]World Health Organization, “WHO Vaccine Pipeline Tracker,” who.int New approvals for respiratory syncytial virus vaccines across the United States, the European Union, and Japan are driving demand for single-dose vials to support pediatric and geriatric campaigns.[2]U.S. Food and Drug Administration, “Drugs@FDA: FDA-Approved Drugs,” fda.govOncology-focused therapeutic vaccines have reached Phase III, each requiring borosilicate containers compatible with lyophilization and cryogenic storage. Governments allocated USD 4.2 billion in 2025 to stockpile vaccines, a budget that translated directly into forward-vial contracts with leading suppliers. Finally, the industry shift from multi-dose to single-dose formats is increasing per-capita vial consumption even where inoculation rates are stable.

Biologics Shift Toward Chemically Inert Borosilicate

Biologics and biosimilars accounted for 43% of FDA approvals in 2025, up from 31% in 2020, and most require Type I borosilicate to prevent protein denaturation. Subcutaneous launches favor small-volume vials with strict dimensional controls that eliminate overfill waste. The European Pharmacopoeia tightened hydrolytic-resistance limits in 2024, effectively excluding lower-grade glass from premium injectables. Biosimilar producers in India and South Korea are switching from polymer to borosilicate to match originator packaging, adding incremental Asian demand. Continued sterilization compatibility with gamma and electron-beam methods cements borosilicate’s long-term position.

Sustainability and Recyclability Regulations Favor Glass

The European Union now requires 75% of pharmaceutical packaging to be recyclable by 2030, a threshold that glass effortlessly meets. California’s extended producer responsibility law adds costs to non-recyclable formats from mid-2025, nudging U.S. drugmakers toward glass. ISO life-cycle assessments in 2025 showed 22% lower emissions for glass vials when recycling infrastructure is in place. Major pharmaceutical companies have pledged to achieve 100% recyclable primary packaging by 2030, naming glass as the baseline material in their roadmaps. China’s draft rules on recycled content are catalyzing investment in cullet processing, broadening the sustainability case worldwide.

mRNA Cold-Chain Needs Ultra-Low Expansion Glass

mRNA vaccines must endure storage from −80 °C to −20 °C, conditions that crack soda-lime glass, so drugmakers specify ultra-low-expansion borosilicate with coefficients below 3.3 × 10⁻⁶ K⁻¹. SCHOTT’s RFID-enabled vials record temperature history, reducing spoilage by 14% in European pilots. Pfizer and BioNTech scaled to 4 billion doses annually by mid-2025, each in 2 ml vials, meeting demanding expansion specs. U.S. public-health spending of USD 1.8 billion on ultra-cold infrastructure in 2025 indirectly subsidizes premium glass HHS.GOV. Decentralized manufacturing hubs in emerging regions are creating new demand for compliant vials as technology transfers roll out.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Polymer Vials Cannibalizing Commodity Glass Share | -0.9% | North America and Europe | Medium Term (2–4 Years) |

| Fragility or Breakage Recalls Increase Cost | -0.7% | High-Volume Manufacturing Regions Worldwide | Short Term (≤2 Years) |

| Energy-Intensive Furnaces Face Carbon Pricing | -0.5% | Europe, Asia-Pacific, North America | Long Term (≥4 Years) |

| Sodium-Ion Leaching in High-pH Gene Therapy Fills | -0.4% | North America and Europe | Medium Term (2–4 |

| Source: Mordor Intelligence | |||

Polymer Vials Cannibalizing Commodity Glass Share

Cyclic olefin polymer vials rose to 12% of the small-molecule injectable segment in 2025, benefiting from 60% lower weight and shatter resistance that cuts transit losses.[3]West Pharmaceutical Services, “Containment Solutions,” westpharma.com FDA acceptance for 18 finished drugs eases regulatory risk and accelerates uptake.[4] Daikyo Seiko, “Crystal Zenith Technical Documentation,” daikyoseiko.com Generic makers in India and China are moving insulin and antibiotics into polymer containers to save costs, while revised U.S. Pharmacopeia protocols clarified extractables testing, further legitimizing the format USP.ORG. Yet polymer’s permeability and higher unit cost limit its reach to neutral-pH liquids, preserving glass leadership in biologics, vaccines, and lyophilized drugs.

Fragility or Breakage Recalls Increase Risk-Mitigation Cost

The FDA documented 27 recalls in 2024 tied to glass particulate contamination, up 18% year on year, driving universal adoption of 100% automated inspection. Breakage during transit accounted for 1.8% of worldwide shipments in 2025, totaling USD 283 million in product losses. Reinforced formats such as Stevanato’s EZ-Fill cut breakage to 0.4% but carry a 22% price premium. Pharmaceutical buyers are pushing liability back onto glass suppliers through warranty clauses, compressing margins, and accelerating the move toward ready-to-use vials that undergo inspection before delivery.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Type I Borosilicate Retains the Lion’s Share

Type I borosilicate captured 67.10% of 2025 revenue, an advantage rooted in proven compatibility with sensitive biologics and vaccines. The pharmaceutical glass vials and ampoules market size for hybrid and surface-coated glass is set to expand fastest, supported by coatings that suppress delamination in high-pH gene therapies. The pharmaceutical glass vials and ampoules market responds to drug-formulation shifts faster than many packaging categories because regulatory filings now require container stability data early in development. Valor Glass, a joint innovation by Gerresheimer and Corning, furthers this momentum by halving breakage without sacrificing hydrolytic resistance. Meanwhile, soda-lime variants still service veterinary and diagnostic uses, underlining that value migration coexists with commodity resilience.

Demand for aluminum-silicate is strengthening in oncology fill-finish suites, but higher melting temperatures translate into production costs that only premium indications can absorb. Niche segments such as amber-tinted or low-actinic glass protect light-sensitive compounds and, although small, command healthy margins. Across all grades, the pharmaceutical glass vials and ampoules market increasingly values documented extractables performance, a requirement that encourages global suppliers to invest in analytical labs near customer hubs. That geographic spread also blunts supply-chain risk, a lesson reinforced during pandemic-era logistics disruptions.

By Application: Vaccine Volume Versus Biologic Value

Vaccines delivered the largest 2025 slice, 46.43% of revenue, on the strength of routine immunization and booster programs. Biologics and biosimilars, however, represent the highest growth path at 7.57% CAGR through 2031, so the pharmaceutical glass vials and ampoules market will pivot toward smaller but higher-value fills. Insulin remains important but is shifting into device cartridges, trimming standalone vial demand. Small-molecule injectables still absorb meaningful glass capacity even as cyclic olefin formats nibble at commodity volumes in anesthesia and antibiotics.

Diagnostic reagents, though accounting for only 8% of sales, place strict tolerance and clarity demands on containers, an attribute that aligns with rising lab-automation adoption. Combination products joining biologics to delivery devices are introducing vials with tamper-evident closures and needle-shield integration, adding complexity that supports price premiums. Taken together, these trends underscore that application mix, not just unit volume, will dictate revenue growth trajectories.

By End User: Contract Manufacturing Reshapes Procurement

Pharmaceutical manufacturers controlled 60.71% of 2025 revenues but are selectively outsourcing fill-finish for niche biologics, a decision that shifts purchasing power toward contract development and manufacturing organizations. Biotechnology firms, expanding at 7.63% CAGR, are structurally reliant on outsourced capacity because many lack internal sterile suites. Ready-to-use vials allow these firms to defer investment in depyrogenation ovens and to turn capital toward clinical development, reinforcing RTU demand within the pharmaceutical glass vials and ampoules market.

Academic centers and hospitals collectively form a small yet lucrative niche characterized by frequent small-lot orders and demand for rapid lead times. Suppliers serving this space differentiate on technical support and flexible scheduling rather than scale. Across all end users, serialization and supply-chain visibility are now baseline expectations, encouraging vial makers to integrate RFID and optical codes at the point of manufacture.

By Manufacturing Technology: Tubular Line Efficiency Meets RTU Convenience

Tubular forming dominated at 71.21% in 2025 because its continuous process achieves high speed and tight tolerances at a competitive cost. Nevertheless, ready-to-use sterile vials show the strongest expansion prospects, courtesy of a 7.12% forecast CAGR. The pharmaceutical glass vials and ampoules market weighs the unit-price premium of RTU against savings from eliminating wash and sterilize steps, and the cost balance tilts in favor of RTU whenever capacity utilization in fill-finish plants is high.

Molded glass remains indispensable for special geometries such as dual-chamber vials, a design frequent in lyophilized-plus-diluent kits. The Alliance for Ready-to-Use Vials is standardizing nest-and-tub dimensions so that pharmaceutical customers can dual-source without fresh validation, lowering the hurdle for RTU adoption. Meanwhile, robotic handling systems require flawless dimensional consistency, a requirement more easily met by tubular and RTU formats than by molded containers.

Geography Analysis

North America accounted for 37.64% of 2025 revenue, a position anchored by the United States’ unparalleled biologics pipeline and the region's 1,847 injectable clinical trials, more than any other region. Regional demand benefits additionally from pandemic preparedness stockpiles that lock in long-term vial contracts. The pharmaceutical glass vials and ampoules market share in Asia-Pacific is rising fastest, supported by capacity expansions in China and India and a strategic pivot from active pharmaceutical ingredient production to finished-dose exports. China alone added 18% glass capacity in 2025, allowing local suppliers to shorten lead times for domestic CAR-T developers.

Europe, responsible for 28% of 2025 sales, leverages stringent pharmacopoeial rules that favor established glass grades and a dense network of contract manufacturers. The pharmaceutical glass vials and ampoules market size in the region is buffered by ongoing investments in furnace electrification to meet rising carbon-pricing obligations. South America and the Middle East, and Africa remain comparatively small but are woven into global vaccine-supply strategies that aim for regional self-sufficiency. Brazil’s approval of 14 biosimilars in 2025 and Saudi Arabia’s localization incentives are early indicators of future demand curves.

Cross-border investment also influences geography dynamics. The Corning-SGD venture in Telangana will put 2.4 billion units of annual capacity within reach of Southeast Asia by 2026, narrowing supply-chain gaps and challenging European imports. Japan’s pivot toward multinational suppliers as its own biologics docket thickens illustrates how regulatory harmonization can redirect procurement patterns. In aggregate, regional differences in energy cost, carbon regulation, and logistics reliability increasingly inform sourcing strategies alongside the traditional variables of price and quality.

Mordor Intelligence provides coverage of the pharmaceutical glass vials and ampoules market across other key regional markets, including Asia, Latin America, Europe, North America, and Middle East and Africa, each with their regulatory frameworks and demand patterns.

Competitive Landscape

Market concentration is moderate: the top five producers controlled roughly 55% of 2025 capacity, yet regional rivals in China and India are gaining share with prices up to 25% lower than those of European incumbents. Scale leaders such as SCHOTT and Gerresheimer practice vertical integration, operating everything from glass tubing to coating lines, which secures access to raw materials and simplifies validation for pharmaceutical buyers. Stevanato Group’s 2025 purchase of Balda Medical’s syringe business expands its presence in combination devices, mapping neatly onto the drug-delivery convergence trend.

Technology is a core differentiator. SCHOTT Pharma’s RFID-encoded vials satisfy serialization mandates while enabling chain-of-custody tracking, capabilities that won contracts with three top-10 vaccine makers. Gerresheimer’s Valor Glass collaboration tackles delamination, a key failure mode in high-pH biologics, and has already entered late-stage trials. At the same time, local champions like Shandong Pharmaceutical Glass secure national certifications that unlock Chinese and Southeast Asian biosimilar programs, putting margin pressure on established exporters.

Regulatory expertise remains a barrier to entry. United States Pharmacopeia Type I certification, FDA drug master file recognition, and EMA audit readiness require multi-year investments in analytical infrastructure. These hurdles slow new entrants but do not entirely block them; rather, they concentrate competition among firms able to prove compliance rapidly. Sustainability commitments add another axis of rivalry, as producers race to electrify furnaces or secure renewable-power contracts to satisfy customers’ net-zero roadmaps.

Pharmaceutical Glass Vials And Ampoules Industry Leaders

Gerresheimer AG

Nipro Corporation

SGD S.A. (SGD Pharma)

SCHOTT AG

Stevanato Group S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: SCHOTT Pharma announced a EUR 150 million (USD 170 million) expansion of its Müllheim, Germany, facility that will lift ready-to-use vial capacity by 30% by Q4 2027.

- October 2025: Stevanato Group opened a 12,000 m² extension at Piombino Dese, Italy, adding EZ-Fill lines with AI-driven inspection that lowers defect rates by 34%.

- September 2025: Corning and SGD Pharma inaugurated a USD 60 million glass-tubing plant in Telangana, India, powered by renewable electricity and designed for 2.4 billion vials annually.

- September 2025: SCHOTT Pharma activated a new ampoule line in Lukavac, Serbia, boosting Eastern European output by 500 million units per year.

Global Pharmaceutical Glass Vials And Ampoules Market Report Scope

The Pharmaceutical Glass Vials and Ampoules Market Report is Segmented by Material Type (Type I Borosilicate Glass, Type II or III Soda-Lime Glass, Aluminum-Silicate Glass, Hybrid or Surface-Coated Glass), Application (Vaccines, Insulin, Biologics and Biosimilars, Small-Molecule Injectables, Diagnostic Reagents), End User (Pharmaceutical Manufacturers, Biotechnology Companies, CDMOs or CMOs, Research and Academic Laboratories, Hospitals and Clinics), Manufacturing Technology (Tubular Glass Forming, Moulded Glass Forming, Ready-To-Use Sterile), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Type I Borosilicate Glass |

| Type II Or III Soda-Lime Glass |

| Aluminum-Silicate Glass |

| Hybrid / Surface-Coated Glass |

| Vaccines |

| Insulin |

| Biologics And Biosimilars |

| Small-Molecule Injectables |

| Diagnostic Reagents |

| Pharmaceutical Manufacturers |

| Biotechnology Companies |

| CDMOs / CMOs |

| Research And Academic Laboratories |

| Hospitals And Clinics |

| Tubular Glass Forming |

| Moulded Glass Forming |

| Ready-To-Use (RTU) Sterile |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest Of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest Of Asia-Pacific | ||

| Middle East | Saudi Arabia | United Arab Emirates |

| Turkey | ||

| Rest Of Middle East | ||

| Africa | South Africa | Nigeria |

| Kenya | ||

| Rest Of Africa | ||

| By Material Type | Type I Borosilicate Glass | ||

| Type II Or III Soda-Lime Glass | |||

| Aluminum-Silicate Glass | |||

| Hybrid / Surface-Coated Glass | |||

| By Application | Vaccines | ||

| Insulin | |||

| Biologics And Biosimilars | |||

| Small-Molecule Injectables | |||

| Diagnostic Reagents | |||

| By End User | Pharmaceutical Manufacturers | ||

| Biotechnology Companies | |||

| CDMOs / CMOs | |||

| Research And Academic Laboratories | |||

| Hospitals And Clinics | |||

| By Manufacturing Technology | Tubular Glass Forming | ||

| Moulded Glass Forming | |||

| Ready-To-Use (RTU) Sterile | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest Of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest Of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest Of Asia-Pacific | |||

| Middle East | Saudi Arabia | United Arab Emirates | |

| Turkey | |||

| Rest Of Middle East | |||

| Africa | South Africa | Nigeria | |

| Kenya | |||

| Rest Of Africa | |||

Key Questions Answered in the Report

How large will global demand for pharmaceutical glass vials be in 2031?

The pharmaceutical glass vials and ampoules market is forecast to reach USD 23.19 billion by 2031, expanding at a 6.54% CAGR from 2026.

Which application segment is growing fastest after 2025?

Biologics and biosimilars show the highest projected CAGR at 7.57% thanks to sustained monoclonal antibody and cell-therapy launches.

Why is Type I borosilicate still dominant despite higher cost?

Its low alkali release avoids protein aggregation, meeting FDA and European Pharmacopoeia standards that biologics and vaccines cannot compromise.

What region offers the strongest growth outlook?

Asia-Pacific is expected to post a 7.53% CAGR through 2031 as China and India scale both glass production and finished-dose manufacturing.

How are suppliers addressing sustainability mandates?

Leading producers are electrifying furnaces, increasing cullet recycling, and offering life-cycle-data packages that document at least 22% lower emissions versus polymer formats.

Will polymer vials overtake glass in injectables?

Polymer formats are encroaching on small-molecule liquids but remain limited by permeability and cost, keeping glass firmly in control of biologics, vaccines, and lyophilized drugs.

Page last updated on: