Chromatography Data Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

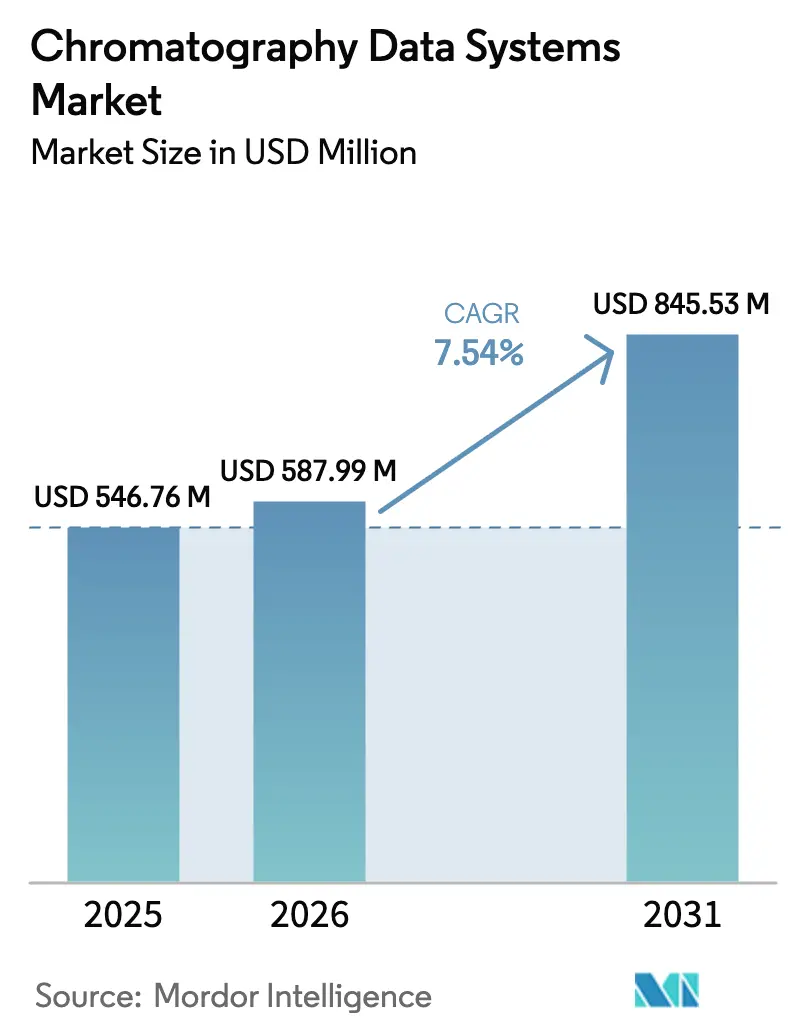

| Market Size (2026) | USD 587.99 Million |

| Market Size (2031) | USD 845.53 Million |

| Growth Rate (2026 - 2031) | 7.54% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chromatography Data Systems Market Analysis by Mordor Intelligence

Chromatography data systems market size in 2026 is estimated at USD 587.99 million, growing from 2025 value of USD 546.76 million with 2031 projections showing USD 845.53 million, growing at 7.54% CAGR over 2026-2031. Integrated, cloud-ready platforms are displacing legacy standalone offerings as laboratories aim to digitize workflows and satisfy tightening data-integrity rules under 21 CFR Part 11 and EU Annex 11. Regulatory scrutiny, rapid AI adoption for method development, and the need to manage large multi-omics data sets are collectively accelerating enterprise upgrades. Laboratories also seek to eliminate validation bottlenecks, foster cross-site collaboration, and lower total cost of ownership, all of which favor subscription-based deployments. As cloud providers bolster ISO 27001 and GxP capabilities, smaller labs are able to access enterprise-grade functionality without heavy capital investment, further widening the addressable base of the chromatography data systems market.[1]U.S. Food and Drug Administration, “Guidance for Industry: Electronic Systems in Clinical Investigations,” fda.gov

Key Report Takeaways

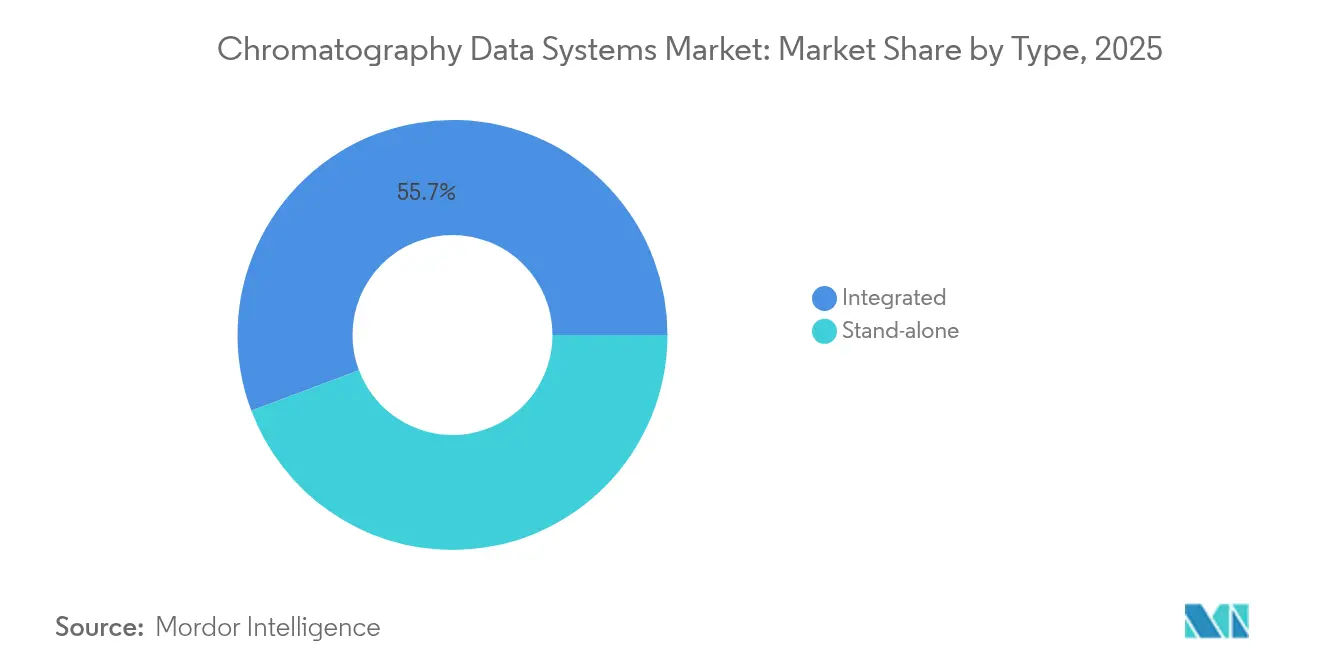

- By type: Integrated systems held 55.74% of the chromatography data systems market share in 2025; the same segment is projected to advance at a 9.41% CAGR to 2031.

- By deployment model: On-premise solutions accounted for 62.02% of the chromatography data systems market size in 2025, while cloud deployments expanded at a 12.03% CAGR through 2031.

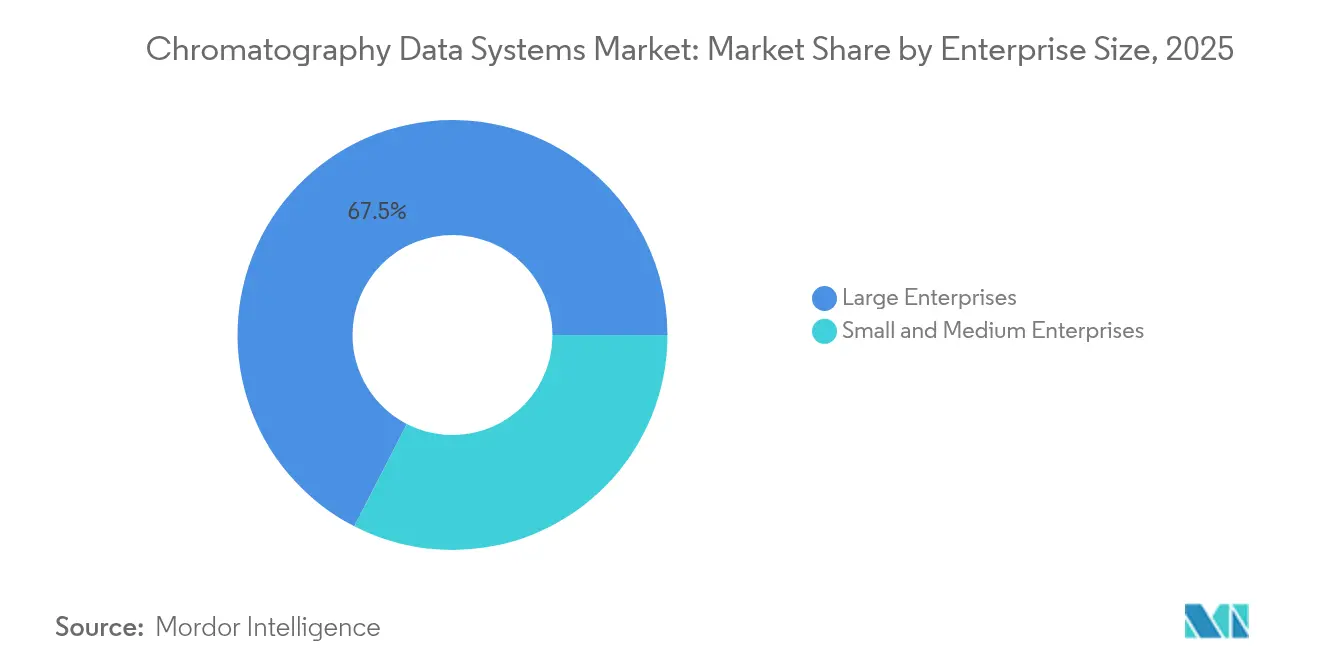

- By enterprise size: Large enterprises controlled 67.45% revenue share in 2025; small and medium enterprises register the highest growth at 11.23% CAGR to 2031.

- By end user: Pharmaceutical and biopharmaceutical laboratories captured 47.35% revenue in 2025; environmental and petrochemical labs exhibit the fastest momentum with a 9.99% CAGR to 2031.

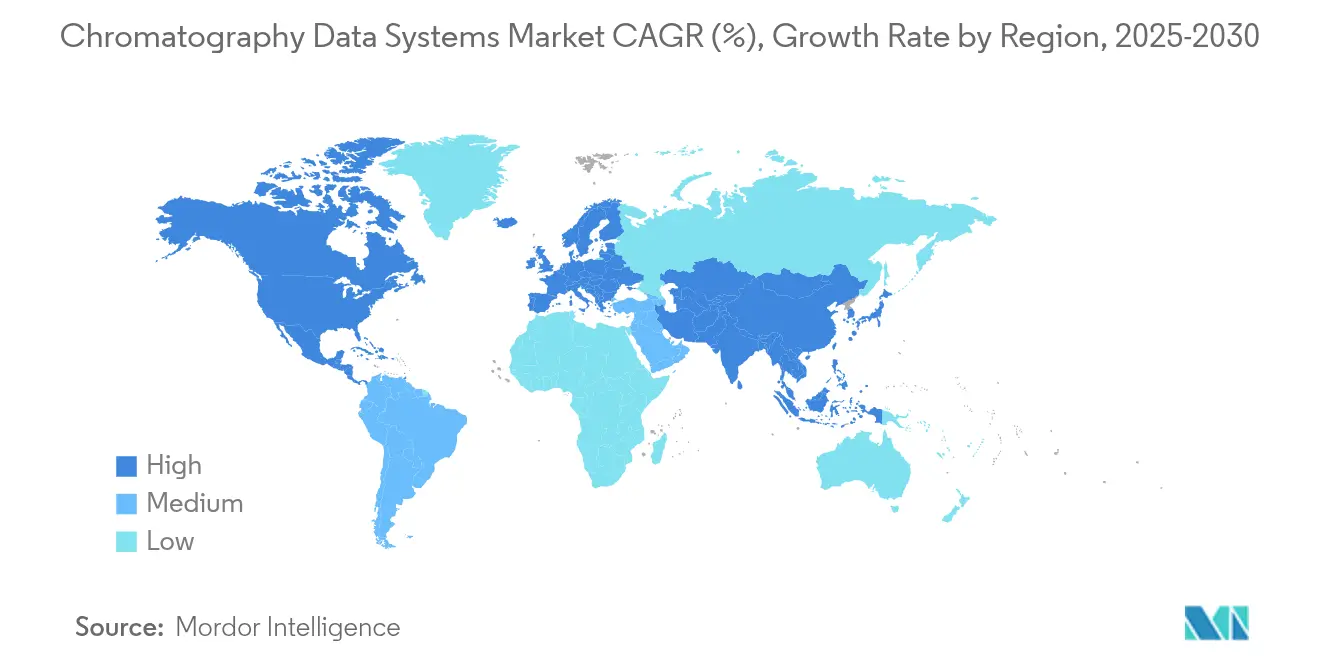

- By geography: North America led with 34.86% revenue share in 2025, whereas Asia Pacific is poised for the fastest expansion at 8.33% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Chromatography Data Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising R&D spend in life-sciences labs | +1.80% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Stricter data-integrity regulations (21 CFR Part 11, GMP Annex 11) | +2.10% | Global, led by North America & EU | Short term (≤ 2 years) |

| Expansion of third-party food-testing outsourcing | +0.90% | Global, emerging markets acceleration | Medium term (2-4 years) |

| Rapid cloud adoption in lab informatics | +1.40% | Global, APAC leading adoption | Short term (≤ 2 years) |

| AI-driven autonomous method development | +1.00% | North America & Europe early adoption | Long term (≥ 4 years) |

| Subscription-based SaaS pricing lowering entry barriers | +0.60% | Global, SME segment focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising R&D Spend in Life-Sciences Labs

Pharmaceutical companies continue to expand analytical budgets to support AI-enabled drug-discovery pipelines and complex biologics characterization. Life-science firms increased capital allocation to chromatography-mass spectrometry integration, elevating the need for data platforms that can handle heterogeneous outputs while ensuring compliance. R&D clusters in Boston and Basel are driving demand for systems that interoperate with electronic lab notebooks and LIMS, favoring comprehensive solutions over point tools. As personalized therapeutics progress, validated data handling becomes mission-critical for method transfer across global networks. These dynamics sustain double-digit growth for the chromatography data systems market in innovation-centric geographies.

Stricter Data-Integrity Regulations

The FDA’s 2024 guidance on electronic records reinforces expectations for complete audit trails and secure electronic signatures, directly influencing vendor selection criteria.[2]U.S. Food and Drug Administration, “Data Integrity and Compliance With Drug CGMP,” fda.gov Parallel updates in EU Annex 11 now cover AI and machine-learning use in GMP workflows, prompting heightened validation requirements. Industry reports show that more than half of 2024 FDA observations in analytical labs stemmed from inadequate audit-trail review, intensifying the shift toward integrated systems with embedded compliance modules. Laboratories are prioritizing platforms that generate immutable records and enable real-time deviation alerts, accelerating refresh cycles in the chromatography data systems market.

Expansion of Third-Party Food-Testing Outsourcing

Brand owners increasingly send contaminant, pesticide-residue, and authenticity tests to contract laboratories, spurring demand for high-throughput data systems capable of segregating multi-client workflows. Contract labs require traceability tools for chain-of-custody management and automated certificate-of-analysis generation, steering purchases toward configurable, cloud-enabled solutions. Providers that bundle chromatography data management with LIMS connectors are gaining share among regional testing networks in Asia and Latin America. As import-export food checks tighten, scalable platforms that support round-the-clock analysis underpin the rising contribution of this vertical to the chromatography data systems industry.[3]U.S. Department of Health & Human Services, “FoodSafety.gov—Consumer Food Safety Information,” foodsafety.gov

Rapid Cloud Adoption in Lab Informatics

SaaS subscription models in the chromatography data systems market offer entry pricing from USD 275 to USD 425 per user per month, an attractive alternative to six-figure perpetual licenses for smaller labs. Cloud deployments furnish immediate scalability for new projects and enable global teams to review chromatograms in real time. Vendors emphasize ISO 27001 and SOC 2 certifications, multi-factor authentication, and encrypted storage to alleviate security anxiety. Hybrid architectures, local instrument control paired with cloud analytics, are emerging as a preferred migration path for regulated environments, encouraging broader uptake of cloud modules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security & IP-protection concerns | -1.20% | Global, heightened in pharmaceutical sector | Short term (≤ 2 years) |

| High integration & validation costs | -0.80% | Global, acute for SMEs | Medium term (2-4 years) |

| Shortage of CDS-skilled workforce | -0.70% | Global, severe in APAC & emerging markets | Long term (≥ 4 years) |

| Vendor lock-in limiting multivendor interoperability | -0.50% | Global, enterprise segment focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cyber-security & IP-Protection Concerns

Average breach costs in life-science firms surpassed USD 5 million in 2024, raising hesitation over cloud migration for sensitive chromatographic data. Attackers increasingly target electronic lab notebooks and data warehouses, prompting laboratories to harden perimeter defenses and adopt end-to-end encryption. Vendors respond with zero-trust architectures and dedicated private-cloud options, yet perceived risk still stalls purchase decisions for some GxP environments. Balancing openness for collaboration with the protection of proprietary methods remains a key sticking point for the broader adoption of cloud-native chromatography data solutions.

High Integration & Validation Costs

Full GxP validation of a new chromatography data platform can extend project timelines by six months and add significant consulting expenses. Integration with legacy chromatographs, LIMS, and ERP systems often demands custom drivers and scripted workflows, inflating costs, particularly for laboratories lacking in-house IT resources. While SaaS offerings reduce hardware spending, validation documentation, user-acceptance testing, and SOP updates still consume labor budgets. These financial pressures lead many small organizations to defer upgrades or limit functional scope, constraining the overall expansion rate of the chromatography data systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Integrated Systems Drive Market Consolidation

Integrated platforms captured 55.74% of the chromatography data systems market in 2025 and are forecast to grow at a 9.41% CAGR owing to built-in compliance functions and seamless interoperability with instruments and informatics layers. Laboratories appreciate centralized user management, unified audit-trail reporting, and reduced validation effort compared with patching together multiple tools. Consequently, the chromatography data systems market size for integrated solutions is projected to widen its lead through 2031.

Instruments now ship with APIs that feed live chromatograms into enterprise data lakes, enabling AI models to optimize gradients and flag anomalies. Providers embed predictive-maintenance dashboards to minimize downtime. These differentiators strengthen integrated offerings as pharmaceutical enterprises standardize global analytics on single platforms, limiting future opportunity for standalone suppliers.

By Deployment Model: Cloud Migration Accelerates Despite Security Concerns

On-premise deployments retained 62.02% revenue in 2025, reflecting entrenched validation practices in regulated labs. Yet the cloud cohort is growing at 12.03% annually, highlighting a pivotal architectural shift in the chromatography data systems market. Subscription pricing, automated updates, and elastic compute for data re-processing attract both startups and contract research organizations.

Hybrid models are bridging the transition, housing raw data on local servers while exporting metadata and processed results for collaborative analytics in the cloud. Early adopters report up to 25% faster project onboarding owing to pre-configured virtual instances. Continued FDA clarification on cloud validation is expected to accelerate uptake, provided cybersecurity frameworks keep pace with emerging threats.

By Enterprise Size: SME Adoption Drives Market Democratization

Large enterprises commanded 67.45% revenue share in 2025 due to expansive instrument fleets and regulatory obligations. However, small and medium enterprises are projected to log an 11.23% CAGR through 2031, signaling a democratization of advanced data-handling tools. Subscription offerings and no-code workflow builders lower adoption barriers, allowing smaller labs to comply with GxP standards without dedicated IT teams.

The chromatography data systems market size for SMEs is also rising as contract organizations build data-rich service offerings to differentiate bids. Workforce shortages in analytical chemistry magnify demand for intuitive interfaces that shorten training cycles. Vendors respond with AI-driven help bots and template libraries that embed best practices directly into the user experience.

By End User: Environmental Testing Emerges as High-Growth Segment

Pharmaceutical laboratories held 47.35% revenue in 2025, yet environmental and petrochemical labs are forecast to expand at a 9.99% CAGR to 2031 as governments stiffen monitoring standards for PFAS and volatile organic compounds. These users require modules for limit-of-detection reporting and automated chain-of-custody, steering demand toward specialized providers.

The chromatography data systems market share for environmental applications increases as labs pursue solvent-reduction strategies and green-chemistry metrics. Platforms offering embedded sustainability dashboards gain favor among industry and municipal water authorities alike. Integration with geospatial mapping tools enables rapid visualization of contaminant hot spots, enhancing situational awareness for regulators and field teams.

Geography Analysis

North America generated 34.86% revenue in 2025 and remains a stable contributor through 2031, thanks to dense biotech clusters in Massachusetts and California. Recent FDA guidance on electronic data integrity reinforces continuous investment in validated platforms, particularly for biologics analytics. Regional cloud uptake gains momentum among contract organizations that prioritize agility over on-premise control, yet cyber-risk perceptions keep large pharmaceutical firms cautious.

Asia Pacific is the fastest-growing region with an 8.33% CAGR, underpinned by contract research expansion in China, India, and South Korea. Government incentives attract multinational companies to set up regional R&D centers, driving orders for compliant data systems that support global technology transfer. Local regulators are aligning with ICH Q2(R2) and Q14, cementing the need for audit-ready solutions. Vendor localization efforts-language packs, regional server options, and local technical support-further accelerate sales in the chromatography data systems market across Asia Pacific.

Europe posts moderate gains as Annex 11 revisions push manufacturers to upgrade legacy software, especially in Germany, Switzerland, and Ireland. A pronounced emphasis on green chemistry motivates laboratories to track solvent consumption and carbon impact through embedded analytics. Collaborative research frameworks such as Horizon Europe require cross-border data exchange, spurring the adoption of interoperable, multi-language platforms. Overall, regulatory harmonization and sustainability imperatives sustain momentum across the continent.

Competitive Landscape

The chromatography data systems market exhibits moderate concentration. Waters, Agilent Technologies, and Thermo Fisher Scientific anchor the field through the tight coupling of instruments and proprietary software, building switching costs for installed bases. Empower, OpenLab, and Chromeleon remain reference platforms in GxP laboratories, each offering validated modules for 21 CFR Part 11 compliance. These incumbents invest heavily in artificial intelligence to automate peak integration and instrument-health prediction, preserving premium pricing power.

Emerging SaaS vendors emphasize API-first frameworks, rapid deployment, and flexible subscription models. Their cloud-native architectures resonate with SMEs and contract organizations seeking lighter validation footprints and lower entry fees. Strategic alliances with instrument manufacturers are proliferating, enabling new entrants to pre-load drivers and certify performance out of the box. Large players counter by opening selected APIs and launching managed-service offerings to retain customers transitioning to the cloud.

Danaher integrated Cytiva to solidify bioprocess analytics while bolstering data-centric capabilities around the ÄKTA platform. Bruker added turnkey clinical mass spectrometry assays to expand adjacent workflows. Private equity interest is rising in niche data-integration providers that bridge chromatography with multi-omics analytics. Competitive differentiation increasingly hinges on real-time compliance dashboards, AI-based method optimization, and ecosystem openness for third-party connectivity.

Chromatography Data Systems Industry Leaders

Agilent Technologies, Inc

PerkinElmer Inc

Shimadzu Corporation

Thermo Fisher Scientific Inc

Waters Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Thermo Fisher Scientific launched Orbitrap Astral Zoom and Orbitrap Excedion Pro mass spectrometers, delivering 35% faster scan rates and 40% higher throughput to enhance omics workflows.

- June 2025: Bruker introduced integrated ClinMass kits with EVOQ DART-TQ+ and unveiled the timsMetabo platform for PFAS detection in environmental samples.

- May 2025: Waters integrated Empower Software with multi-angle light-scattering and dRI detectors to shorten validation time by up to six months.

- May 2025: Waters integrated Empower Software with multi-angle light-scattering and dRI detectors to shorten validation time by up to six months

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the chromatography data systems market as all licensed software platforms and tightly integrated modules that control chromatographic instruments, capture raw detector signals, process peaks, generate regulatory-compliant reports, and securely archive files across HPLC, GC, SFC, IC, and CE workflows worldwide. We track revenue earned from first-time licenses, subscription fees, maintenance contracts, and validated upgrades delivered to laboratories in pharmaceuticals, biotech, food testing, environmental monitoring, petrochemical analysis, and academia.

Scope exclusion: hardware chromatographs, generic laboratory information management systems, and standalone spreadsheet or macro solutions are kept outside this assessment.

Segmentation Overview

- By Type

- Integrated

- Stand-alone

- By Deployment Model

- Cloud

- On-Premise

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small & Medium Enterprises

- By End-User

- Academic & Research Institutes

- Pharmaceutical & Biopharmaceutical Industry

- Food & Beverage Industry

- Environmental & Petrochemical Labs

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed instrument product managers, QA directors in FDA-inspected plants, contract research scientists in Europe and Asia, and IT administrators migrating to cloud deployments. Insights from these conversations helped us validate average license fees, cloud uptake pace, and service attach rates that were only partly visible in secondary data.

Desk Research

We collected baseline facts from public sources such as the US Food & Drug Administration 21 CFR Part 11 warning-letter database, European Medicines Agency GMP Annex 11 updates, OECD trade statistics on analytical instruments, and publication trends in journals like Analytical Chemistry and Journal of Chromatography A. Our team also reviewed industry outlooks published by trade bodies, for example, the American Society for Mass Spectrometry and the International Society for Pharmaceutical Engineering, which shed light on adoption cycles.

Corporate filings, investor presentations, and patent families accessed through D&B Hoovers, Dow Jones Factiva, and Questel added clarity on vendor pipelines, installed bases, and pricing shifts. These are indicative sources only; several other open and paid references informed data validation.

Market-Sizing & Forecasting

A blended top-down and bottom-up model underpins the numbers. Global chromatograph shipments and regional trade flows reconstructed total addressable laboratories, which were then refined with penetration rates drawn from primary interviews. Supplier roll-ups of sampled license sales and average selling price checkpoints provided a reality check before finalizing totals. Key variables inside the model include the installed base of HPLC and GC units, the percentage of instruments operating under validated electronic records, the mean CDS license cost by deployment mode, pharma R&D expenditure, and annual FDA data-integrity citations that stimulate upgrades. Forecasts rely on multivariate regression where cloud adoption, R&D spend, and regulatory audits act as leading indicators, with scenario analysis applied to exchange-rate swings and subscription pricing shifts.

Data Validation & Update Cycle

Mordor analysts run variance screens that compare model outputs with fresh shipment data, cloud usage logs, and compliance audit counts. Outliers trigger rechecks with respondents before senior review. Reports refresh once a year, and material events such as major regulatory changes prompt interim revisions so clients always receive our latest view.

Why Our Chromatography Data Systems Baseline Commands Reliability

Published figures differ because firms choose unlike scopes, price stacks, and refresh rhythms. We acknowledge these gaps upfront and show how disciplined variable selection keeps our estimate grounded.

Key gap drivers are often tied to whether service revenue is bundled, whether cloud subscriptions are annualized or capitalized, how aggressively emerging-market labs are counted, and the cadence at which currency conversions are normalized.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 503.46 M | Mordor Intelligence | - |

| USD 476 M | Regional Consultancy A | excludes SaaS fees and multi-year validation services |

| USD 1.38 B | Trade Journal B | applies instrument-to-software ratio without auditing duplicate licenses |

| USD 3.70 B | Global Consultancy C | clubs broader lab software and applies uniform ASP across regions |

The comparison shows that our balanced scope, variable-level cross-checks, and annual update cadence deliver a dependable baseline that decision-makers can trace back to transparent inputs and reproducible steps.

Key Questions Answered in the Report

How big is the Chromatography Data Systems Market?

The Chromatography Data Systems Market size is expected to reach USD 587.99 million in 2026 and grow at a CAGR of 7.54% to reach USD 845.53 million by 2031.

What is the current Chromatography Data Systems Market size?

In 2026, the Chromatography Data Systems Market size is expected to reach USD 587.99 million.

Who are the key players in Chromatography Data Systems Market?

Agilent Technologies, Inc, PerkinElmer Inc, Shimadzu Corporation, Thermo Fisher Scientific Inc and Waters Corporation are the major companies operating in the Chromatography Data Systems Market.

Which is the fastest growing region in Chromatography Data Systems Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Chromatography Data Systems Market?

In 2026, the North America accounts for the largest market share in Chromatography Data Systems Market.

What years does this Chromatography Data Systems Market cover, and what was the market size in 2025?

In 2025, the Chromatography Data Systems Market size was estimated at USD 587.99 million. The report covers the Chromatography Data Systems Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Chromatography Data Systems Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: