Passive Electronic Components Market Size

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 48.45 Billion |

| Market Size (2030) | USD 66.10 Billion |

| Growth Rate (2025 - 2030) | 6.41% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Passive Electronic Components Market Analysis

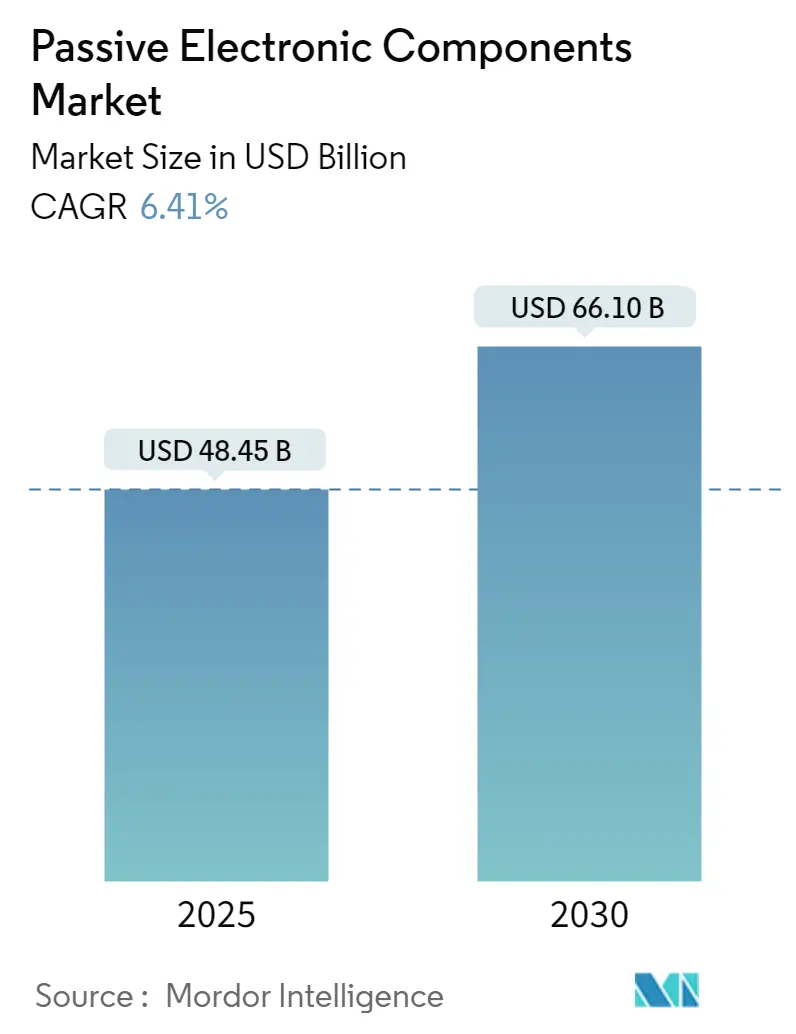

The Passive Electronic Components Market size is estimated at USD 48.45 billion in 2025, and is expected to reach USD 66.10 billion by 2030, at a CAGR of 6.41% during the forecast period (2025-2030).

The passive electronic components industry is experiencing significant transformation driven by the rapid evolution of digital technologies and connectivity solutions. According to Ericsson, global smartphone mobile network subscriptions reached nearly 6.4 billion in 2022 and are projected to exceed 7.7 billion by 2028, with China, India, and the United States leading in subscription numbers. This massive scale of mobile device adoption has created unprecedented demand for passive components across various applications, from basic circuit functionality to advanced power management systems. The integration of voice-enabled smart devices and MEMS gyroscopes has further accelerated this trend, particularly among younger consumers who increasingly prefer smart devices for everyday activities.

The telecommunications sector is witnessing substantial infrastructure development, particularly in 5G technology deployment. In Southeast Asia and Oceania, 5G subscriptions are expected to reach approximately 620 million by 2028, representing a 48% penetration rate. This rapid expansion of 5G networks is driving demand for specialized passive components capable of handling higher frequencies and providing improved signal integrity. The evolution of network technologies has also led to increased requirements for electromagnetic interference (EMI) suppression and power management solutions, further boosting the need for advanced passive components.

The manufacturing landscape is undergoing significant changes, particularly in emerging economies. India's electronics manufacturing sector is projected to reach USD 300 billion by 2026, with mobile phone sales expected to increase from USD 40 billion in 2022 to USD 80 billion by 2026. This growth is supported by government initiatives and increasing foreign investments in local manufacturing capabilities. The trend is particularly evident in India's mobile phone exports, which doubled during April 2022-February 2023 compared to the previous year, driven primarily by major manufacturers like Apple and Samsung.

The healthcare sector has emerged as a significant growth driver for passive electronic components, particularly in wearable technology applications. The industry is witnessing increasing adoption of electronic components for pain management and cardiovascular disease monitoring, requiring highly reliable and precise passive components. This trend is complemented by the broader shift toward home-based healthcare solutions, creating demand for compact, self-use electronic device components such as BP monitors, blood sugar test kits, and physiotherapy devices. The integration of these components into medical devices requires stringent quality standards and specialized designs to ensure patient safety and device reliability.

Passive Electronic Components Market Trends

Increasing Complexity of Electronics

The evolution of electronic components has led to unprecedented complexity in circuit design and component requirements. With the advent of technological advancements, electronics and electronic devices are becoming increasingly sophisticated, primarily driven by consumer demand for slim, compact devices with edge-to-edge screens. This complexity is further amplified by the integration of multiple technologies within single devices, such as smartphones that now incorporate MEMS gyroscopes, advanced sensors, and sophisticated power management systems.

The deployment of 5G technology has significantly impacted component requirements, with devices requiring several antennas, larger processors, and enhanced battery capabilities. According to CAICT, 5G mobile phone shipments reached 214 million in 2022, accounting for 78.8% of total shipments in China. This transition demands more radios, larger processors, increased components, and greater battery capacity, all while maintaining or reducing form factors. The trend extends to various sectors, including automotive electronics, where a single vehicle can contain over 3,000 MLCCs, and this number is expected to increase significantly with the adoption of electric and autonomous vehicles.

Increasing Miniaturized Design Preferences

The consumer electronics industry is experiencing a growing demand for smaller, lighter, and higher-performing electronics, driving the miniaturization of components and elements. This trend is particularly evident in smartphones and IoT devices, where irregular shapes and compact designs can only be achieved through miniaturization. The advent of IoT and IIoT has significantly impacted electronic component market design and size requirements, particularly in applications like smart homes, offices, wearables, and remote monitoring systems.

The automotive sector is witnessing a significant shift toward miniaturization, particularly in electric vehicle applications. According to industry data, an electric vehicle requires ten times more capacitors compared to an internal combustion vehicle. Major manufacturers are actively investing in this trend, with companies like Murata launching the world's smallest and thinnest 1µF LW reversed MLCC for automotive applications in October 2023. This development is particularly significant for electric vehicles, where space optimization is crucial for improving overall vehicle efficiency and performance. The trend toward miniaturization is also evident in medical devices, where compact electronic components are essential for developing portable and wearable healthcare devices.

Segment Analysis: By Type

Ceramic Capacitors Segment in Passive Electronic Components Market

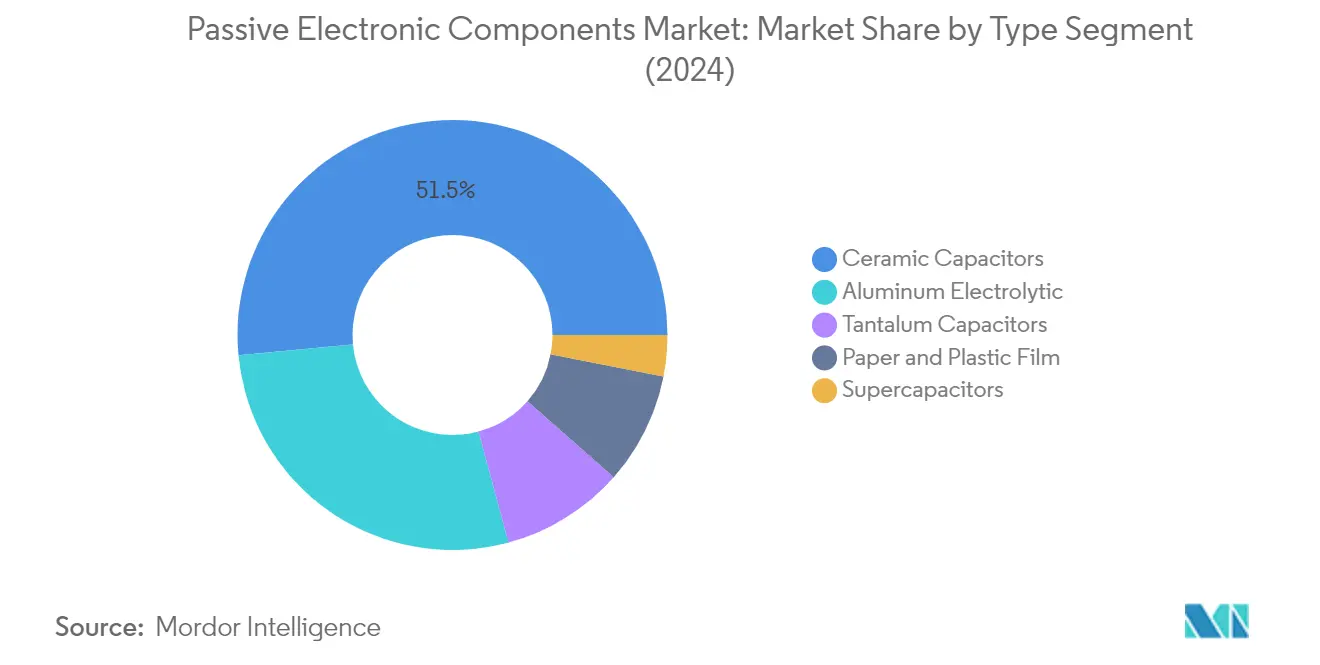

The ceramic capacitors segment continues to dominate the global passive electronic components market, commanding approximately 52% market share in 2024. This significant market position is primarily driven by their widespread adoption in automotive applications, particularly in electric vehicles where a single vehicle can require over 10,000 MLCCs. The segment's dominance is further strengthened by the increasing integration of ceramic capacitors in 5G smartphones, consumer electronics, and advanced driver assistance systems (ADAS). Major passive components manufacturers like Murata and TDK are continuously innovating in this space, developing compact and reliable ceramic capacitors that meet the demanding requirements of modern electronic devices while maintaining high performance and reliability standards.

Supercapacitors Segment in Passive Electronic Components Market

The supercapacitors segment is experiencing remarkable growth in the passive electronic components market, with a projected growth rate of approximately 13% during 2024-2029. This exceptional growth is driven by increasing adoption in electric vehicles, renewable energy storage systems, and industrial applications. The segment's expansion is supported by technological advancements in graphene-based materials and hybrid supercapacitor technologies. The automotive sector, particularly in electric and hybrid vehicles, is creating substantial demand for supercapacitors due to their rapid charging capabilities and high power density. Additionally, the growing focus on sustainable energy solutions and the integration of supercapacitors in smart grid applications are further accelerating the segment's growth trajectory.

Remaining Segments in Passive Electronic Components Market

The other segments in the market include aluminum electrolytic capacitors, tantalum capacitors, and paper and plastic film capacitors, each serving distinct applications in the electronics industry. Aluminum electrolytic capacitors maintain a strong presence in power supply and industrial applications due to their high capacitance values and cost-effectiveness. Tantalum capacitors are crucial in high-reliability applications, particularly in aerospace and medical devices, while paper and plastic film capacitors are essential in high-voltage and AC applications. These segments continue to evolve with technological advancements and changing industry requirements, particularly in areas such as miniaturization and improved performance characteristics.

Segment Analysis: By End-User Industry

Consumer Electronics Segment in Passive Electronic Components Market

The consumer electronics segment dominates the electronic component market, accounting for approximately 38% of the total market share in 2024. This significant market position is driven by the rapid surge in demand for consumer electronics products and the growing adoption of smart appliances. The segment's growth is further fueled by the increasing integration of passive components in smartphones, tablets, and other portable devices, where capacitors are critical for power supply filtering and voltage regulation. The rising demand for 5G smartphones, with their requirement for higher component densities, has particularly boosted the segment's dominance. Additionally, the expansion of IoT devices, wearable technology, and smart home applications has created substantial demand for passive electronic components in consumer electronics applications.

Automotive Segment in Passive Electronic Components Market

The automotive segment is emerging as the fastest-growing sector in the passive electronic components market, with a projected growth rate of approximately 8% from 2024 to 2029. This remarkable growth is primarily driven by the increasing electrification of vehicles and the rising adoption of advanced driver assistance systems (ADAS). The segment's expansion is further accelerated by the growing integration of electronic circuit elements in modern vehicles, particularly in electric and hybrid vehicles which require significantly more passive components than traditional internal combustion engine vehicles. The automotive industry's shift towards autonomous vehicles, connected cars, and sophisticated infotainment systems is creating unprecedented demand for passive devices in electronics, particularly in applications requiring high reliability and performance under demanding conditions.

Remaining Segments in End-User Industry

The other significant segments in the passive electronic components market include energy, industrial, communications/servers/data storage, aerospace and defense, and medical sectors. The energy sector is particularly notable for its growing adoption of renewable energy systems and smart grid applications. The industrial segment is being driven by Industry 4.0 initiatives and increasing automation in manufacturing processes. The communications sector continues to expand with the ongoing deployment of 5G infrastructure and data center expansions. The aerospace and defense sector maintains steady demand for high-reliability components, while the medical sector is seeing increased adoption of electronic medical devices and diagnostic equipment. Each of these segments contributes uniquely to the market's overall growth trajectory, with varying requirements for component specifications and reliability standards.

Passive Electronic Components Market Geography Segment Analysis

Passive Electronic Components Market in the Americas

The Americas region holds approximately 18% of the passive components market share in the global electronic components market in 2024, establishing itself as a significant player in the industry. The region's market position is primarily driven by the robust automotive and electronics sectors, particularly in the United States. The increasing adoption of electric vehicles, supported by government initiatives and infrastructure development, has created substantial demand for passive components. The region demonstrates strong technological innovation capabilities, with numerous research and development centers focusing on next-generation electronic components. The presence of major automotive OEMs and favorable government policies supporting electric vehicle adoption continues to drive market growth. Additionally, the region's advanced manufacturing capabilities and strong focus on industrial automation have created sustained demand for passive components across various industrial applications. The growing investment in 5G infrastructure and data centers further amplifies the market potential, while the increasing adoption of IoT devices across industries creates new opportunities for market expansion.

Passive Electronic Components Market in Europe, Middle East & Africa

The Europe, Middle East & Africa region has demonstrated remarkable resilience and growth in the passive electronic components market from 2019 to 2024. The region's market dynamics are shaped by strong automotive manufacturing capabilities, particularly in countries like Germany, France, and Spain. The increasing focus on electric vehicle production and the presence of prominent automotive manufacturers have created sustained demand for passive components. The region's commitment to renewable energy and industrial automation has fostered market growth across various sectors. The strong emphasis on research and development, particularly in countries like Germany and France, has led to technological advancements in component manufacturing. The growing adoption of Industry 4.0 practices and the increasing focus on smart manufacturing have created new opportunities for market expansion. Additionally, the region's robust aerospace and defense sector continues to drive demand for high-reliability passive components, while the increasing investments in 5G infrastructure development further support market growth.

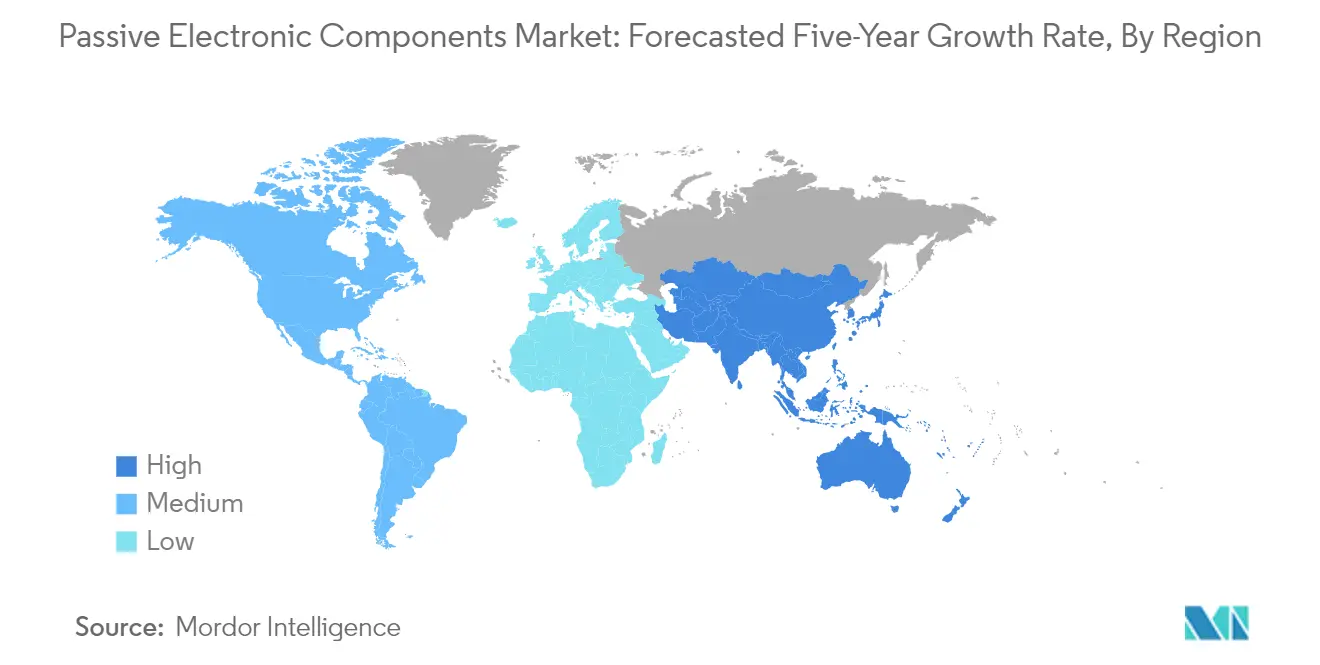

Passive Electronic Components Market in Asia-Pacific (Excluding Japan and Korea)

The Asia-Pacific region (excluding Japan and Korea) is projected to demonstrate strong growth in the passive electronic components market, with an expected CAGR of 8% during 2024-2029. The region's market is characterized by its strong manufacturing capabilities and the presence of numerous electronic component manufacturers. China's dominant position in electronic component manufacturing, coupled with India's growing electronics manufacturing sector, creates substantial market opportunities. The increasing adoption of electric vehicles and the growing focus on renewable energy solutions drive demand for passive components. The region's robust consumer electronics industry and the rapid adoption of smart devices continue to create sustained market demand. The ongoing digital transformation across industries and the increasing focus on industrial automation further amplify market growth potential. Additionally, government initiatives supporting domestic electronics manufacturing and the growing investments in 5G infrastructure development contribute to market expansion.

Passive Electronic Components Market Overview

Top Companies in Passive Electronic Components Market

The passive electronic components market features prominent players like TDK Corporation, Murata Manufacturing, Vishay Intertechnology, and Panasonic Corporation leading the industry through continuous innovation and strategic expansion. These companies are heavily investing in research and development to develop miniaturized electronic components with enhanced performance capabilities, particularly focusing on automotive and consumer electronics applications. The industry witnesses a strong focus on developing multilayer ceramic capacitors (MLCCs) and high-frequency inductors to meet the growing demand from emerging technologies like 5G, IoT, and electric vehicles. Companies are also emphasizing operational excellence through automated manufacturing processes and Industry 4.0 implementation to improve production efficiency and quality control. Strategic partnerships and collaborations with technology providers and end-users have become crucial for product development and market expansion, while geographic expansion, particularly in Asia-Pacific, remains a key growth strategy.

Global Conglomerates Dominate Component Manufacturing Landscape

The passive electronic components market structure is characterized by the dominance of large, vertically integrated multinational corporations, particularly from Japan and other Asian countries, which possess extensive manufacturing capabilities and robust distribution networks. These established players leverage their technological expertise, economies of scale, and strong customer relationships to maintain their market positions, while smaller specialized passive components manufacturers focus on niche applications and regional markets. The industry has witnessed significant consolidation through mergers and acquisitions, as companies seek to expand their product portfolios, gain technological capabilities, and strengthen their presence in key growth markets.

The market demonstrates a moderate to high level of concentration, with the top players accounting for a significant share of the global market. Recent years have seen increased M&A activity, particularly focused on acquiring companies with specialized technologies or strong regional presence. Japanese and European manufacturers have been particularly active in acquiring companies in emerging markets to expand their manufacturing footprint and gain access to new customer bases, while also investing in startups developing innovative electronic component industry technologies.

Innovation and Adaptability Drive Market Success

Success in the electronics components industry increasingly depends on companies' ability to innovate and adapt to rapidly evolving technological requirements while maintaining cost competitiveness. Incumbent players are focusing on developing advanced manufacturing processes, investing in automation and quality control systems, and expanding their product portfolios to include higher-value passive components for emerging applications. Companies are also strengthening their research and development capabilities, forming strategic partnerships with technology providers, and investing in sustainable manufacturing practices to maintain their competitive edge.

For new entrants and smaller players, success lies in identifying and focusing on specific market niches, developing specialized products for high-growth applications, and building strong relationships with key customers in target industries. The market presents moderate barriers to entry due to high capital requirements and technical expertise needed, while customer concentration in certain segments like automotive and telecommunications requires strong quality management systems and long-term relationship building. Regulatory compliance, particularly regarding environmental standards and material restrictions, continues to influence product development and manufacturing processes, while the risk of substitution remains relatively low due to the essential nature of passive components in electronic circuits.

Passive Electronic Components Market Leaders

-

Delta Electronics Inc.

-

Panasonic Corporation

-

TDK Corporation

-

Vishay Intertechnology Inc.

-

Murata Manufacturing Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Passive Electronic Components Market News

- November 2023: Fukui Murata Manufacturing Co. Ltd, a manufacturing subsidiary of Murata Manufacturing Co. Ltd, announced its plans to establish a new R&D base, “Ceramic Capacitor R&D Center,” near Echizen-Takefu Station in Fukui Prefecture. The establishment of the Ceramic Capacitor R&D Center aims to improve the company's technological capabilities in developing and manufacturing ceramic capacitors, which is Murata Manufacturing’s core business. The construction commenced in November 2023, with the inauguration planned for April 2026.

- November 2023: KYOCERA AVX announced the launch of its first safety-certified MLCCs, the new Class X1/Y2 KGK Series and Class X2 KGH Series, and expanded its extensive portfolio of commercial surface-mount MLCCs. The KGK Series Class X1/Y2 and KGH Series Class X2 safety capacitors are available in two dielectrics, NP0/C0G and X7R, and are rated for 250VAC and operating temperatures extending from -55°C to +125°C.

Passive Electronic Components Market Industry Segmentation

Passive electronic components are components that consume energy. They do not produce energy, are incapable of power gain, and require no electrical power to operate. They simply absorb energy. A standard example of passive electronic components would be resistors, inductors, and capacitors. The analysis is based on the market insights captured through secondary research and through the primaries. The market also covers the major factors impacting the growth of the passive electronic components market in terms of drivers and restraints.

The passive electronic components market is segmented by capacitors, inductors, and resistors.

Capacitors are further segmented by type (ceramic capacitors, tantalum capacitors, aluminum electrolytic capacitors, paper and plastic film capacitors, and supercapacitors), end-user industry (automotive, consumer electronics, aerospace and defense, energy, communications/servers/data storage, industrial, and medical), and geography (Americas, Europe, Middle East and Africa, Asia-Pacific (excl. Japan and Korea), and Japan and South Korea).

Inductors are further segmented by type (power and frequency), end-user industry (automotive, consumer electronics and computing, aerospace and defense, and communications), and geography (North America, Europe, Asia-Pacific, and the Rest of the World).

Resistors are further segmented by type (surface-mounted chips, networks, wire-wound, film/oxide/foil, carbon), end-user industry (automotive, consumer electronics and computing, aerospace and defense, and communications), and geography (North America, Europe, Asia-Pacific, and Rest of the World).

The report offers market forecasts and size in value (USD) for all the above segments.

| Capacitors | By Type | Ceramic Capacitors |

| Tantalum Capacitors | ||

| Aluminum Electrolytic Capacitors | ||

| Paper and Plastic Film Capacitors | ||

| Supercapacitors | ||

| By End-user Industry | Automotive | |

| Industrial | ||

| Aerospace and Defense | ||

| Energy | ||

| Communications/Servers/Data Storage | ||

| Consumer Electronics | ||

| Medical | ||

| By Geography | Americas | |

| Europe, Middle East and Africa | ||

| Asia-Pacific (Excl. Japan and Korea) | ||

| Japan and South Korea | ||

| Inductors | By Type | Power |

| Frequency | ||

| By End-user Industry | Automotive | |

| Aerospace and Defense | ||

| Communications | ||

| Consumer Electronics and Computing | ||

| Other End-user Industries | ||

| By Geography | North America | |

| Europe | ||

| Asia-Pacific | ||

| Rest of the World | ||

| Resistors | By Type | Surface-mounted Chips |

| Network | ||

| Wirewound | ||

| Film/Oxide/Foil | ||

| Carbon | ||

| By End-user Industry | Automotive | |

| Aerospace and Defense | ||

| Communications | ||

| Consumer Electronics and Computing | ||

| Other End-user Industries | ||

| By Geography | North America | |

| Europe | ||

| Asia-Pacific | ||

| Rest of the World | ||

| By Type | Ceramic Capacitors |

| Tantalum Capacitors | |

| Aluminum Electrolytic Capacitors | |

| Paper and Plastic Film Capacitors | |

| Supercapacitors | |

| By End-user Industry | Automotive |

| Industrial | |

| Aerospace and Defense | |

| Energy | |

| Communications/Servers/Data Storage | |

| Consumer Electronics | |

| Medical | |

| By Geography | Americas |

| Europe, Middle East and Africa | |

| Asia-Pacific (Excl. Japan and Korea) | |

| Japan and South Korea |

| By Type | Power |

| Frequency | |

| By End-user Industry | Automotive |

| Aerospace and Defense | |

| Communications | |

| Consumer Electronics and Computing | |

| Other End-user Industries | |

| By Geography | North America |

| Europe | |

| Asia-Pacific | |

| Rest of the World |

| By Type | Surface-mounted Chips |

| Network | |

| Wirewound | |

| Film/Oxide/Foil | |

| Carbon | |

| By End-user Industry | Automotive |

| Aerospace and Defense | |

| Communications | |

| Consumer Electronics and Computing | |

| Other End-user Industries | |

| By Geography | North America |

| Europe | |

| Asia-Pacific | |

| Rest of the World |

Passive Electronic Components Market Research FAQs

How big is the Passive Electronic Components Market?

The Passive Electronic Components Market size is expected to reach USD 48.45 billion in 2025 and grow at a CAGR of 6.41% to reach USD 66.10 billion by 2030.

What is the current Passive Electronic Components Market size?

In 2025, the Passive Electronic Components Market size is expected to reach USD 48.45 billion.

Who are the key players in Passive Electronic Components Market?

Delta Electronics Inc., Panasonic Corporation, TDK Corporation, Vishay Intertechnology Inc. and Murata Manufacturing Co. Ltd are the major companies operating in the Passive Electronic Components Market.

Which is the fastest growing region in Passive Electronic Components Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Passive Electronic Components Market?

In 2025, the Asia-Pacific accounts for the largest market share in Passive Electronic Components Market.

What years does this Passive Electronic Components Market cover, and what was the market size in 2024?

In 2024, the Passive Electronic Components Market size was estimated at USD 45.34 billion. The report covers the Passive Electronic Components Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Passive Electronic Components Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: