Military Parachute Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

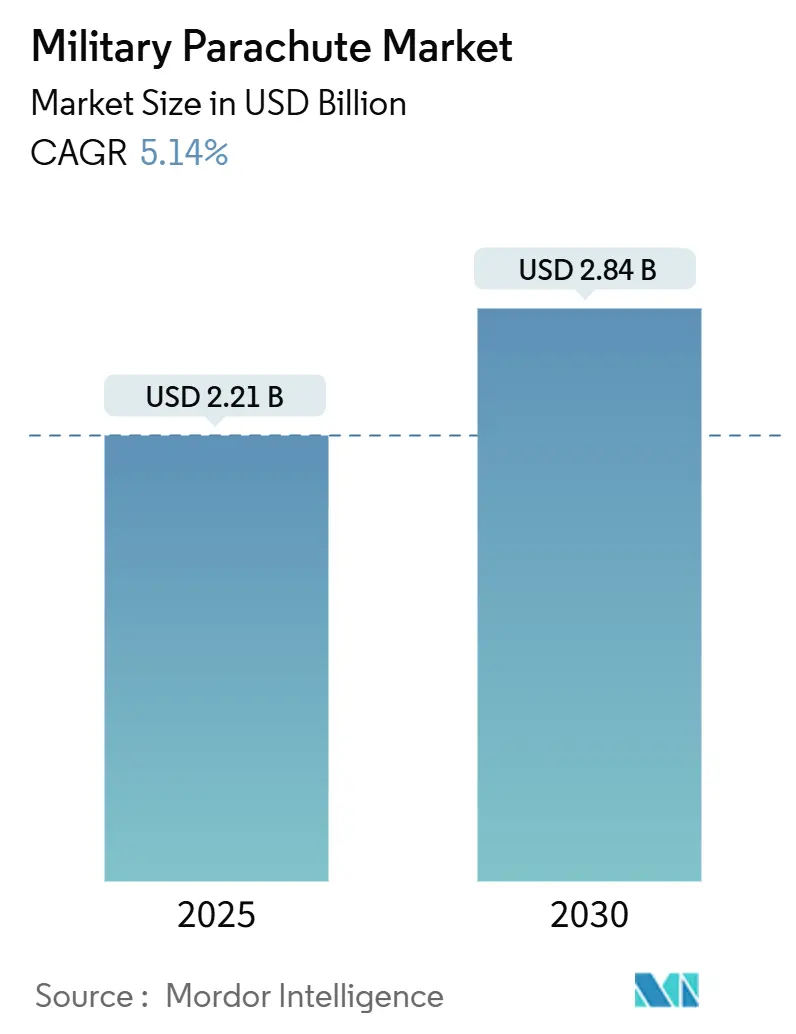

| Market Size (2025) | USD 2.21 Billion |

| Market Size (2030) | USD 2.84 Billion |

| Growth Rate (2025 - 2030) | 5.14% CAGR |

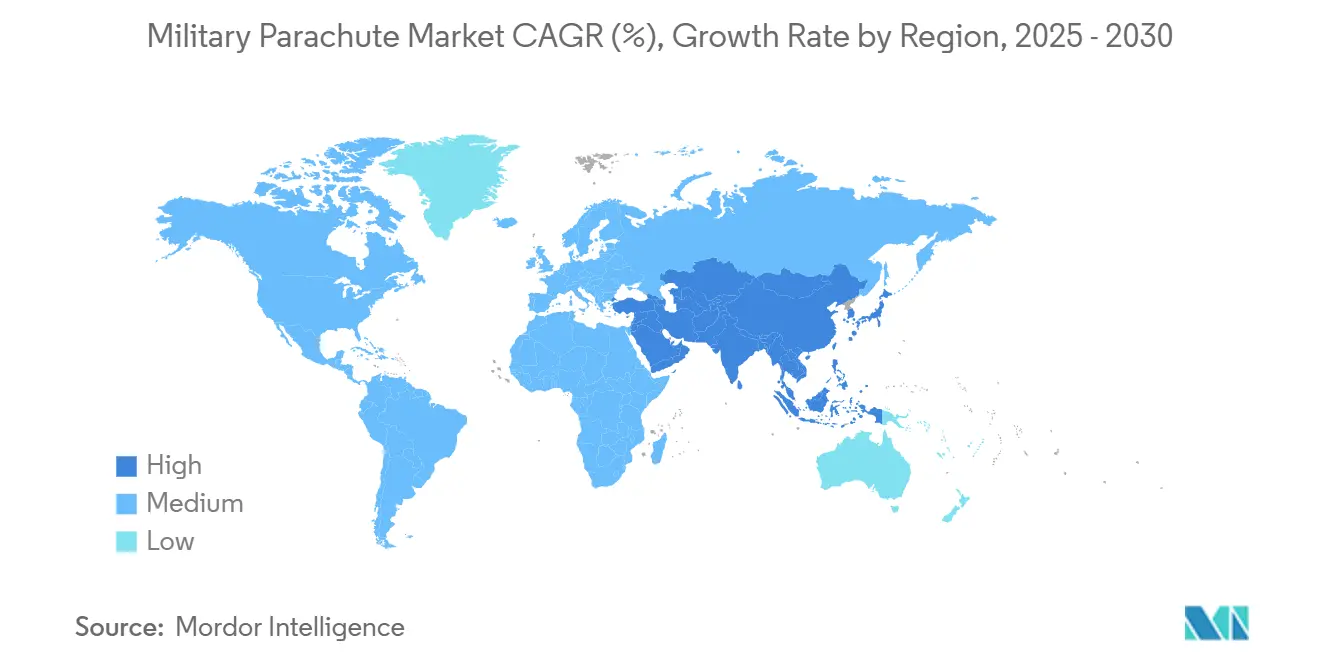

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Military Parachute Market Analysis by Mordor Intelligence

The military parachute market stood at USD 2.21 billion in 2025 and is forecast to reach USD 2.84 billion by 2030, reflecting a 5.14% CAGR. Budget expansions across NATO and the Indo-Pacific, combined with the shift from round to precision-guided ram-air systems, continue to unlock new procurement cycles despite cost pressures. Humanitarian airdrop missions and the need to sustain dispersed operations have increased demand for steerable cargo canopies that minimise drop-zone exposure. Meanwhile, emerging drone-glider hybrids are altering the competitive calculus, nudging manufacturers toward integrated guidance kits and smart-fabric offerings that improve glide ratios, cut weight, and support autonomous flight. Moderate consolidation persists, yet private-equity interest and defense prime acquisitions are widening the technology pipeline and intensifying rivalry in the military parachute market.

Key Report Takeaways

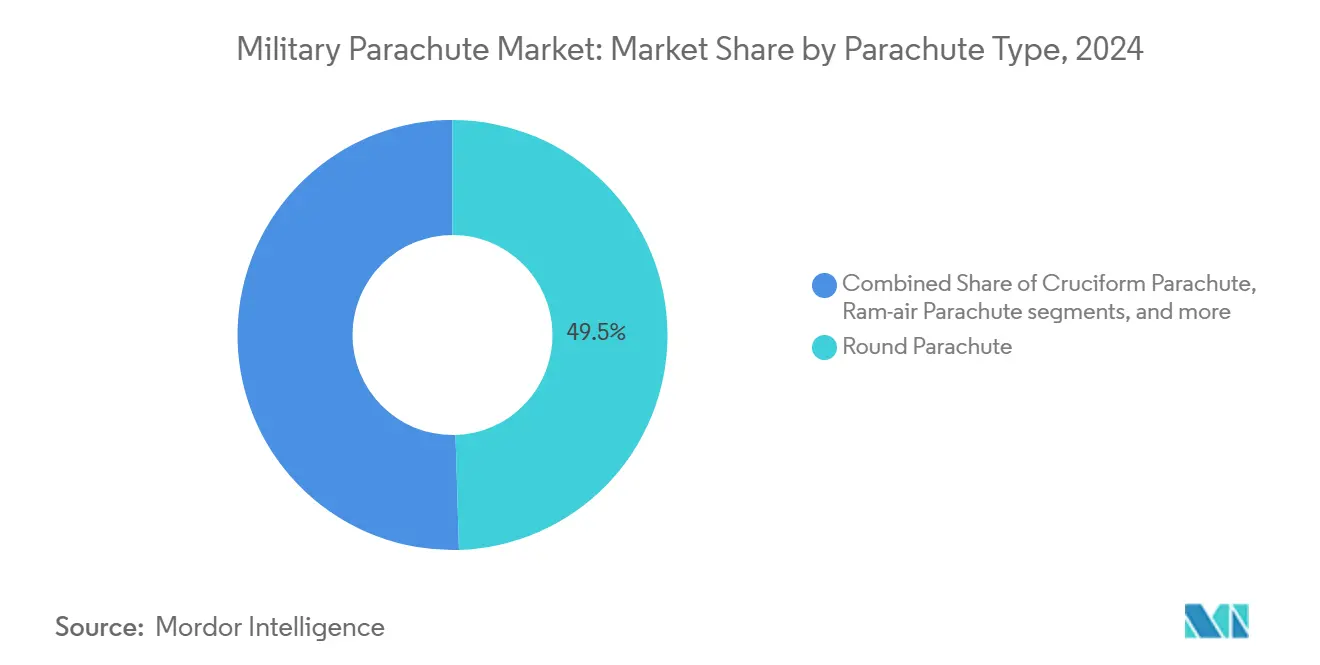

- By parachute type, round designs led with 49.52% of military parachute market share in 2024; ram-air systems are projected to grow at a 6.12% CAGR through 2030

- By application, personnel airdrop accounted for 55.45% of the military parachute market size in 2024, whereas cargo delivery is advancing at a 5.78% CAGR to 2030

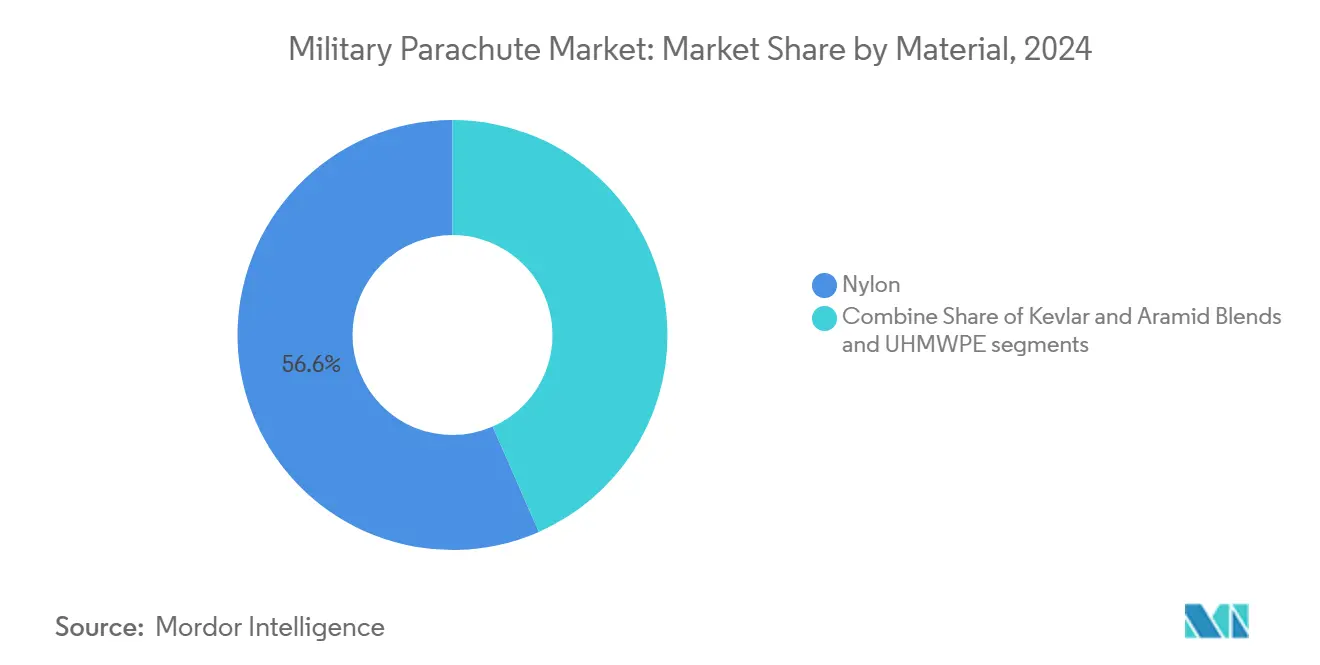

- By material, nylon captured 62.24% share of the military parachute market in 2024; UHMWPE is expanding at 7.10% CAGR over the same period.

- By deployment system, static-line held 54.58% share in 2024, while free-fall solutions are rising at 6.25% CAGR thanks to special-operations requirements.

- By geography, North America commanded 41.25% of the global military parachute market in 2024; Asia-Pacific is the fastest-growing region at 5.59% CAGR to 2030.

Global Military Parachute Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising defense outlays in key NATO and Indo-Pacific nations | +1.8% | North America and Europe, APAC core | Medium term (2-4 years) |

| Expansion of special-operations and airborne units | +1.2% | Global, with concentration in NATO allies | Long term (≥ 4 years) |

| Shift toward precision-guided ram-air systems | +0.9% | North America and EU, spill-over to APAC | Medium term (2-4 years) |

| Surge in humanitarian airdrop missions | +0.7% | Global, with focus on conflict zones | Short term (≤ 2 years) |

| Training modernization programs | +0.6% | Global, with emphasis on advanced military nations | Medium term (2-4 years) |

| Miniaturised sensors enabling health-monitoring canopies | +0.4% | North America and EU initially, global expansion | Long term (≥ 4 years) |

Source: Mordor Intelligence

Rising Defense Outlays in Key NATO and Indo-Pacific Nation

Alliance members reassessed threat scenarios and elevated 2%-of-GDP spending norms, signalling multi-year procurement pipelines for next-generation parachute delivery assets.[1]Source: Anthony Capaccio, “Russia-China Twin Threat Sees EU, US Face Vast Increase in Defense Spending,” Bloomberg, bloomberg.com Indo-Pacific programs followed a similar path, with Japan hosting 12-nation island-defense drills and Indonesia adding CN235-220 transports configured for 34 paratroopers. These initiatives shorten replacement cycles, promote interoperability, and drive recurring orders for systems capable of resisting electronic-warfare interference while sustaining GPS-denied navigation. Procurement budgets increasingly pair hardware outlays with sustainment funds, prioritizing smart-fabric maintenance diagnostics and raising the addressable military parachute market. Vendors demonstrating rapid certification turnarounds and digital-thread support ecosystems remain best positioned to capture funding allocations earmarked for near-peer operations.

Expansion of Special-Operations and Airborne Units

Great-power competition triggered a global expansion of elite airborne formations, from Russia’s 45,000-strong VDV to the US Army’s reactivated 11th Airborne Division. These units seek high-altitude, low-signature insertion kits that merge glide performance with autonomous steering for pinpoint landings. Programs such as Personnel Air Mobility Systems—motorised paragliders with 62-mile range—underscore how powered-parachute hybrids blur category lines and swell the tactical envelope. As altitude ceilings rise toward 30,000 feet, demand intensifies for oxygen-integration, thermal-protection layers, and rapid-rigging solutions that reduce pre-jump timelines. The net effect is a steady uptick in premium-priced specialised canopies within the military parachute market.

Shift Toward Precision-Guided Ram-Air Systems

Ram-air technology transitioned from niche to mainstream as manoeuvrability became critical for contested drop zones.[2]Source: Safran Group, “Ram Air Parachutes for High Altitude High Opening Missions,” Safran, safran-group.com Safran’s MMS-360 HG delivers 5:1 glide ratios, while India’s MCPS integrates fabric vents that enable 200 kg payloads at 30,000 feet. The DRDO-built CADS obtains 100-metre circular-error-probable accuracy using autonomous flight logic tied to terrain-avoidance algorithms. Airborne cargo variants now couple JPADS-compatible electronics with UHMWPE reinforcement tapes, promoting line-of-sight independence and lowering total system weight.

Surge in Humanitarian Airdrop Missions

Conflict-zone access constraints increased the frequency of relief airdrops, most visibly in Gaza, where C-130 crews released 38,000 meals under adverse conditions. The Royal Air Force followed with 110 tonnes of humanitarian cargo delivered by 120 parachutes, highlighting parachute-centric logistics for non-combat operations. Yet, a Gaza-incident parachute failure, causing five fatalities, propelled reliability concerns into the policy spotlight. Consequently, NGOs and defense agencies initiated joint working groups on canopy-material redundancy and dual-trigger release mechanisms, signalling fresh demand for validation services within the military parachute market.[3]Source: MDPI Editors, “Current Research Status of High-Performance UHMWPE Fiber,” MDPI, mdpi.com Even as unit costs remain higher than ground transport, the growing operational necessity keeps humanitarian airdrops a net positive driver.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced fabrics and guidance kits | -0.8% | Global, with acute impact in cost-sensitive markets | Medium term (2-4 years) |

| Stringent safety/air-worthiness certification | -0.6% | Global, with varying regulatory intensity | Long term (≥ 4 years) |

| High-tenacity nylon and Kevlar supply-chain risk | -0.5% | Global, with concentration in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Emerging drone-based resupply alternatives | -0.3% | North America and EU initially, expanding globally | Medium term (2-4 years) |

Source: Mordor Intelligence

High Cost of Advanced Fabrics and Guidance Kits

Kevlar fibres offering 23 g/d break tenacity and 425-480 °C decomposition temperatures remain energy-intensive, driving up end-item pricing. UHMWPE yarns require specialised extrusion and gel-spinning lines that restrict supplier bases and elevate lead times. Precision kits that embed GPS, Inertial, and Bluetooth-mesh links multiply bill-of-material line items, making guided systems three to five times costlier than legacy round canopies. Fiscal trade-offs sharpen as programs juggle parachutes, UAVs, and loitering munitions within finite procurement envelopes. Unless volume production scales or alternative fibres emerge, cost inflation will restrain adoption rates in segments of the military parachute market.

Stringent Safety/Air-Worthiness Certification

FAA Part 105 mandates repack cycles of 180 days for synthetic reserves and ties equipment compliance to rigger licence availability, prolonging entry-into-service timelines. ASTM F3322-18 now governs unmanned parachute recovery systems, extending test-matrix complexity to small cargo gliders. Certification bottlenecks intensified as aviation authorities harmonised civilian and military requirements, driving paperwork overheads that smaller suppliers struggle to absorb. Concurrently, service-specific airworthiness boards imposed climate-chamber and wind-tunnel trials that lengthen development spirals by 18-24 months. These hurdles raise switching costs and temper growth in the military parachute market.

Segment Analysis

By Parachute Type: Ram-Air Systems Drive Precision Evolution

Round canopies held 49.52% of the military parachute market in 2024, retaining dominance through cost-effective mass-drop capability and legacy inventory integration. Though smaller in unit volumes, Ram-air designs are accelerating at a 6.12% CAGR thanks to 5:1 glide ratios and steerable profiles for GPS-denied insertions. The military parachute market size for ram-air variants is projected to rise steadily as NATO mandates include steerability and autonomous options in new tenders. Cruciform models meet niche cargo missions, offering balanced drag and oscillation control that protects fragile loads upon landing. Annular and drogue parachutes serve as egress and recovery solutions for fast-jet seats, where rapid inflation and quasi-stable drag characteristics are imperative.

Industry focus shifted toward integrating hybrid propulsion pods into ram-air frames, creating semi-powered descent profiles that stretch glide envelopes beyond 60 km. This convergence with ultralight aviation calls for new rigging curricula and multi-domain airworthiness baselines that combine manned and unmanned standards. Vendors experimenting with active-fabric control surfaces are engineering canopies whose cell-deformation mechanics adjust in flight, positioning ram-air systems at the frontier of the military parachute market. Adoption continues to hinge on cost-efficiency tipping points and the availability of battery chemistries that tolerate extreme-altitude cold-soak conditions.

Note: Segment shares of all individual segments available upon report purchase

By Application: Cargo Delivery Gains Strategic Importance

Personnel drops commanded 55.45% of 2024 revenue as airborne brigades and special-operations units relied on parachutes for contested-area insertions. Yet, cargo airdrop expanded at 5.78% CAGR, propelled by distributed-operations doctrine and low-level resupply missions that demand sub-100-metre accuracy. The military parachute market size allocated to cargo applications will climb alongside conflict-zone humanitarian needs and high-altitude, high-speed delivery platforms. Training segments preserve steady budgets; simulators and VR-based rigging aids fill instructor gaps while lowering accident rates during live jumps.

Technology fusion is most apparent in cargo drops where autonomous gliders such as Grasshopper complement parachutes by extending standoff distance while preserving disposable cost profiles. Glide-and-flare algorithms work with canopy reefing stages to adjust descent as wind vectors shift, enhancing supply reliability for platoon-level units. Such cross-pollination widens addressable spend and invites inter-modal competition that can cap volume growth for conventional cargo canopies. As a result, suppliers embed modular guidance kits that retrofit round or cruciform systems, preserving legacy stock while meeting precision mandates, thereby sustaining momentum in the military parachute market.

By Material: Advanced Composites Challenge Nylon Dominance

Nylon retained 62.24% of the military parachute market share in 2024, underpinned by mature supply chains and low-temperature resilience. UHMWPE captured the fastest trajectory at 7.10% CAGR by supplying a 60% strength-to-weight improvement that permits higher payloads and altitude ceilings. The military parachute market size for UHMWPE-based systems is expected to grow as procurement offices prioritise fatigue life and ballistic tolerance in canopy specifications. Kevlar and para-aramid blends fill critical-risk applications, including pilot rescue and special-forces infiltration, where heat and abrasion tolerance override cost concerns.

Composite adoption, however, raises recyclability and field-repair questions. Nylon fabrics accept conventional sewing repairs, whereas UHMWPE requires hot-knife sealing and specialised adhesives, complicating forward-depot logistics. Manufacturers answer this by offering kit-based mobile repair stations and bundling composite patches with UV-curable resins that harden in under three minutes. Meanwhile, the research frontier explores electro-conductive threads that monitor canopy stress in flight, allowing riggers to predict life-cycle endpoints and cut premature disposals. These smart-fabric initiatives could propel another wave of differentiation within the military parachute market.

Note: Segment shares of all individual segments available upon report purchase

By Deployment System: Free-Fall Technology Advances

Static-line systems accounted for 54.58% of revenue in 2024, and their reliability made them indispensable for brigade-level drops and basic airborne training. Free-fall variants climbed at a 6.25% CAGR, mirroring special-operations growth and the quest for high-altitude, low-signature infiltration profiles. The military parachute market size attached to free-fall systems receives a further push from modern automatic activation devices that reduce mishap rates at altitudes above 25,000 feet. India’s 27,000-foot MCPS free-fall test highlighted national self-reliance drives, while Russia’s Stayer system widened payload envelopes to 180 kg across a 700–10,000 metre band.

Progress in sensor-fusion has shrunk required canopy opening altitudes without sacrificing structural integrity, giving jumpers larger glide boxes and shorter exposure windows. Like those proven on the T-7A Red Hawk program, extended-duration ejection-seat parachutes borrow free-fall fabric construct concepts to lower spine-loading on pilots. Going forward, manned-unmanned teaming models will see free-fall personnel guide expendable supply pods during descent, merging situational awareness and logistic delivery in a single lift sortie. Such operational blending ensures that free-fall innovation remains a steady pillar of growth in the military parachute market.

Geography Analysis

North America dominated the military parachute market with a 41.25% share in 2024, aided by the US Department of Defense’s USD 842 billion request prioritising survivability upgrades, hazard-pay increases, and next-generation aerial-delivery trials. Contractual vehicles such as multi-year Indefinite-Delivery and Indefinite-Quantity awards underpin long-run volume stability and create favourable economies of scale for incumbent US suppliers. Canada’s joint jumps with US units at Fort Liberty reinforced interoperability agendas that stimulate cross-border standardisation and pooling of reserve-parachute stocks.

Europe follows as a mature yet innovation-centric arena, where France’s Airbus A400M supply-glider tests and the UK’s large-scale Gaza aid drops spotlight niche technologies unavailable elsewhere. NATO harmonisation projects continue to press for interchangeable static-line and ram-air assemblies, reducing duplication and expanding competitive tender fields. Eastern-front security concerns further anchor spending on airborne brigade refits, ensuring sustained demand even as fiscal discipline tightens.

Asia-Pacific exhibits the fastest 5.59% CAGR through 2030, propelled by China’s long-range gliding airdrop mechanics breakthroughs and India’s indigenous MCPS roll-out. Japan’s 12-nation remote-island drill and Indonesia’s CN235-220 order illustrate regional commitment to strategic lift and rapid-response capability. Emerging economies such as the Philippines, Malaysia, and Vietnam now participate in multilateral airborne exercises, opening new addressable segments for mid-tier suppliers willing to localise rigging and maintenance support. Collectively, these vectors cement Asia-Pacific as the pivotal expansion theatre within the global military parachute market.

Competitive Landscape

The military parachute market remains moderately consolidated. Legacy leaders Airborne Systems, Safran, and Mills Manufacturing hold multi-decade supply positions founded on integrated design, production, and certification capacities. Their portfolios now span tactical ram-air, mass-drop round, and specialised cargo kits, supported by global repair-centre footprints that anchor lifetime-support revenues. Competitive tensions sharpened as HEICO acquired Capewell’s Aerial Delivery and Descent Devices divisions, bolstering cockpit-egress and cargo-delivery integration under a single banner.

Private-equity entrants like Argyle Capital Partners injected fresh capital into niche textile houses like International Custom Products, accelerating automated-loom upgrades and ISO 9001 process digitisation that benefit mid-volume customers. Start-ups concentrate on autonomous guidance, sensorised fabrics, and hybrid glider-parachute systems that undercut traditional canopies on accuracy metrics while promising rapid field integration. To defend share, incumbents are bundling software-enabled maintenance services—exemplified by BANC3’s SAFEDROP XR augmented-reality platform—to offset potential volume erosion with high-margin support contracts.

Supplier strategies converge around vertical fabric integration, rigging hardware, and avionics. Safran, for instance, couples its MMS ram-air family with oxygen consoles and thermal suits, delivering all-inclusive HAHO mission kits that simplify procurement audits. Airborne Systems pilots blockchain-based serial-number registries to track canopy life cycles and anticipate repack deadlines, differentiating on data transparency in an environment of rising certification scrutiny. Technological leapfrogging and service-oriented bundling ensure the military parachute market remains attractive to innovators despite entry-barrier persistence.

Military Parachute Industry Leaders

-

Airborne Systems North America

-

Safran SA

-

IrvinGQ

-

Aerodyne Research LLC

-

Mills Manufacturing Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The US Department of Defense (DoD) selected BANC3, Inc., a frontrunner in advanced C4ISR and defense product innovation, to create SAFEDROP. This next-generation augmented/mixed reality (AR/MR) and computer vision (CV) tool aims to enable non-expert soldiers to efficiently rig equipment and cargo for aerial delivery missions.

- June 2025: SERT announced its contract to supply HALO/HAHO parachute systems to Indonesia’s KOPASSUS. These systems, featuring the CPS Military Silhouette Series, will enhance operational free-fall programs. This collaboration underscores SERT’s commitment to delivering advanced solutions to Southeast Asia’s military and law enforcement agencies.

- March 2025: The Aerial Delivery Research and Development Establishment (ADRDE), a lab based in Agra and part of the DRDO, in collaboration with the Indian Air Force (IAF), showcased a combat freefall jump. This was executed using an indigenously designed military combat parachute system (MCPS) from an altitude of 27,000 ft (8.23 km). With full combat gear, this leap marks the MCPS as the sole parachute system currently used by the Indian armed forces, capable of deployment above 25,000 ft.

Global Military Parachute Market Report Scope

A parachute is a device designed to slow the rate of descent of a body under free fall by creating drag. Modern parachutes are designed to reduce the terminal velocity of the user by as much as 90%.

The military parachute market is segmented by type, application, and geography. By type, the market is segmented into round, cruciform, ram-air, and other types. By application, the market is segmented into military, cargo, and other applications. The report also covers the market sizes and forecasts for the military parachute market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| By Parachute Type | Round Parachute | |||

| Cruciform Parachute | ||||

| Ram-air Parachute | ||||

| Annular/Drogue Parachute | ||||

| Others | ||||

| By Application | Personnel Airdrop | |||

| Cargo Airdrop | ||||

| Training | ||||

| By Material | Nylon | |||

| Kevlar and Aramid Blends | ||||

| Ultra-high-molecular-weight Polyethylene (UHMWPE) | ||||

| By Deployment System | Static-Line | |||

| Free-Fall | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Russia | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| India | ||||

| Japan | ||||

| South Korea | ||||

| Australia | ||||

| Rest of Asia-Pacific | ||||

| South America | Brazil | |||

| Rest of South America | ||||

| Middle East and Africa | Middle East | Saudi Arabia | ||

| United Arab Emirates | ||||

| Israel | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Rest of Africa | ||||

| Round Parachute |

| Cruciform Parachute |

| Ram-air Parachute |

| Annular/Drogue Parachute |

| Others |

| Personnel Airdrop |

| Cargo Airdrop |

| Training |

| Nylon |

| Kevlar and Aramid Blends |

| Ultra-high-molecular-weight Polyethylene (UHMWPE) |

| Static-Line |

| Free-Fall |

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the military parachute market?

The military parachute market stood at USD 2.21 billion in 2025 and is forecast to reach USD 2.84 billion by 2030, reflecting a 5.14% CAGR.

Which parachute type is growing fastest?

Ram-air systems are expanding at a 6.12% CAGR through 2030 thanks to their steerable, precision-guided profiles.

Why is cargo airdrop demand increasing?

Distributed-operations doctrine and humanitarian relief needs are pushing cargo airdrop revenues upward at 5.78% CAGR.

Which material segment shows the highest growth?

UHMWPE fabrics, valued for their strength-to-weight benefits, are advancing at a 7.10% CAGR.

Which region offers the greatest future growth?

Asia-Pacific leads with a 5.59% CAGR as China, India and regional partners accelerate airborne-modernisation programs.

What key restraint could slow market expansion?

Rising costs for advanced fabrics and integrated guidance kits pose the largest cost-related drag on new-system adoption.

Page last updated on: June 23, 2025